June 6, 2026

The global energy landscape faces unprecedented volatility as geopolitical tensions reshape traditional supply chains and pricing mechanisms across commodity-dependent economies. The interconnected nature of international petroleum flows means that disruptions in critical chokepoints create cascading effects that extend far beyond the immediate regions of conflict, fundamentally altering the competitive landscape for nations previously insulated by domestic advantages. This interconnectedness has particularly affected the Iran crisis impact on Nigerian diesel prices, demonstrating how quickly domestic energy advantages can erode under global market pressures.

Understanding Nigeria's Diesel Price Transformation in Global Context

Nigeria's energy market dynamics have undergone a fundamental shift as international crude oil volatility reaches unprecedented levels. The nation's diesel pricing structure, historically characterised by competitive regional advantages, now reflects broader macroeconomic pressures stemming from global supply chain disruptions and the Iran crisis impact on Nigerian diesel prices.

For years, Nigeria maintained its position among Africa's five most affordable diesel markets, with pricing structures that supported key economic sectors including transportation, logistics, and manufacturing. This competitive advantage stemmed from a combination of domestic resource availability, regional refining capacity, and favourable import logistics that collectively maintained downward pressure on fuel costs.

Historical Price Positioning and Market Fundamentals

Nigeria's traditional cost advantages in African fuel markets reflected several structural factors that distinguished it from regional competitors. The nation's position as Africa's largest crude oil producer provided a foundation for domestic energy security, while proximity to international shipping routes facilitated efficient petroleum product distribution across West Africa.

Historical data reveals Nigeria consistently ranked within the top five African nations for diesel affordability through 2025, with pricing patterns that reflected both domestic production capabilities and favourable import economics. This positioning supported industrial competitiveness and transportation sector viability, creating multiplier effects throughout the broader economy.

Regional pricing structures across West Africa typically showed Nigeria competing directly with other oil-producing nations including Angola and Equatorial Guinea, while maintaining significant advantages over import-dependent economies such as Ghana and Senegal. Furthermore, economic factors sustaining these low-cost distribution patterns included subsidised fuel policies, efficient port infrastructure, and integrated supply chain management.

Current Market Data and Price Trajectory Analysis

The transformation of Nigeria's diesel market began in early 2026, with accelerating price increases that fundamentally altered the nation's competitive position within African energy markets. According to conflict data from Business Insider Africa, the price trajectory shows a dramatic departure from historical norms.

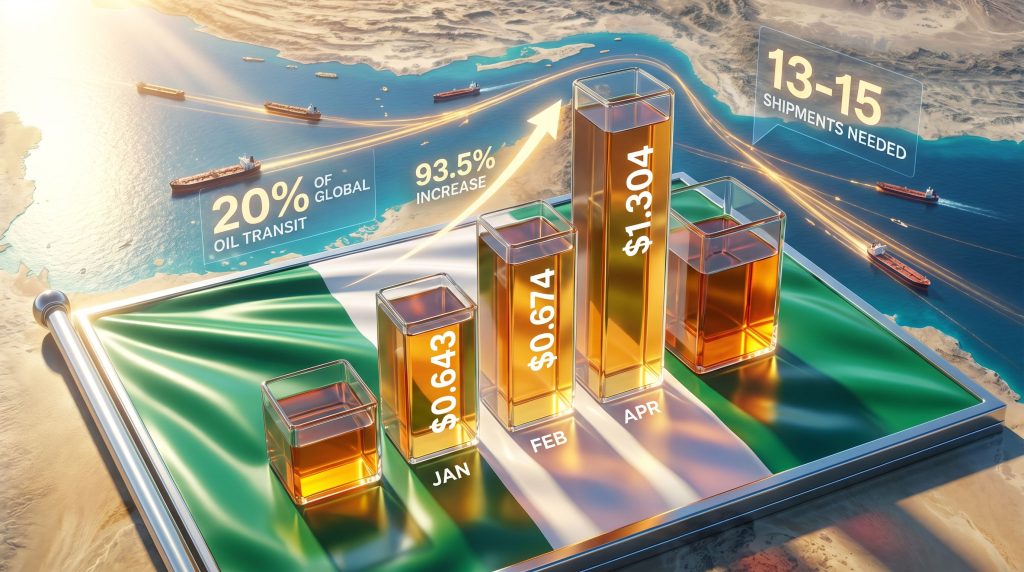

Table: Nigerian Diesel Price Evolution (2026)

| Month | Price per Liter (USD) | Regional Ranking | Price Change (%) |

|---|---|---|---|

| January | $0.643 | Top 5 | – |

| February | $0.674 | Top 5 | +4.8% |

| March | Outside Top 10 | 11th-15th | +15-25% |

| April | $1.304 | 23rd | +93.5% |

The April 2026 price of $1.304 per litre represents a 93.5% increase from February levels, demonstrating the velocity and magnitude of the market disruption. This pricing shift pushed Nigeria from its traditional top-five ranking to 23rd position among African nations, marking one of the most dramatic commodity price adjustments in recent continental economic history.

Market analysts note that the speed of this transition—occurring over approximately three months—suggests supply-side shocks rather than gradual demand-driven inflation. Consequently, the price elasticity implications indicate that Nigeria's diesel market faced external pressures that overwhelmed domestic supply chain resilience mechanisms.

When big ASX news breaks, our subscribers know first

What Economic Forces Drive Nigeria's Fuel Import Dependency?

Despite substantial domestic refining capacity through the Dangote facility, Nigeria's energy security remains vulnerable to international market fluctuations. This paradox reveals deeper structural challenges within the nation's petroleum value chain that extend beyond simple refining capacity calculations.

The Dangote Petroleum Refinery, recognised as the world's largest single-train refinery with approximately 650,000 barrels per day capacity, commenced operations in 2023 with expectations of transforming Nigeria's energy independence profile. However, operational realities demonstrate that refining infrastructure alone cannot guarantee price stability without corresponding crude supply security.

Refinery Capacity vs. Crude Supply Chain Constraints

The fundamental challenge facing Nigeria's energy sector lies in the mismatch between refinery requirements and domestic crude availability. The Dangote facility requires 13-15 crude oil cargo shipments monthly to maintain optimal operational capacity, yet historically sourced only approximately 5 cargoes from domestic production.

This supply gap creates a 67-62% import dependency ratio for crude feedstock, meaning that even with world-class refining infrastructure, Nigeria remains exposed to the same international price volatility affecting global petroleum markets. The arithmetic is stark: 8-10 monthly crude cargoes must be sourced internationally, subject to global pricing mechanisms and supply chain disruptions.

Monthly crude cargo requirements translate to approximately 40,000-50,000+ barrels per day of crude throughput needed to maintain nameplate capacity. Nigeria's domestic crude production, while substantial by continental standards, proves insufficient to feed even this single facility while maintaining export revenue streams that support government fiscal requirements.

Local sourcing limitations reflect broader challenges within Nigeria's upstream petroleum sector, including production capacity constraints, infrastructure bottlenecks, and the competing demands of export markets versus domestic refining needs. In addition, import dependency ratios highlight how quickly domestic advantages can erode when global supply chains face disruption.

Infrastructure Investment and Processing Bottlenecks

Key Insight: The Dangote Refinery, despite being the world's largest single-train facility, requires significant crude oil imports to maintain operational capacity, highlighting the complexity of achieving energy self-sufficiency even with substantial infrastructure investments.

Single-train refinery design maximises processing efficiency through linear crude oil conversion, but creates operational vulnerabilities when feedstock supply faces interruption. Unlike multi-train facilities with parallel processing capabilities, the Dangote structure depends on consistent crude input to maintain optimal throughput rates.

Infrastructure development priorities must therefore address both refining capacity and crude supply security simultaneously. The current model demonstrates that even massive capital investments in downstream processing cannot eliminate import dependency without corresponding upstream production enhancements.

Processing bottlenecks emerge when international crude costs increase rapidly, as higher feedstock expenses translate directly into refined product pricing. Currency exposure amplifies these effects when the Nigerian Naira weakens against the US Dollar, the primary currency for international crude transactions.

How Do Global Supply Route Disruptions Impact Regional Energy Markets?

The Strait of Hormuz represents a critical chokepoint for international energy flows, with approximately 20% of global oil transit occurring through this maritime corridor. Disruptions in this region create cascading effects across import-dependent economies worldwide, demonstrating how localised geopolitical tensions can reshape global commodity markets and contribute to global tariff impacts on energy pricing.

Regional energy markets face immediate transmission of supply disruptions through multiple mechanisms, including physical supply constraints, risk premium incorporation, and speculative trading behaviours. The Iran crisis has highlighted these transmission pathways with particular clarity, showing how quickly local supply advantages can erode under global market pressures.

Strait of Hormuz: Economic Significance and Vulnerability Assessment

Daily oil flow volumes through the Strait of Hormuz reach approximately 21-22 million barrels during normal operational periods, according to US Energy Information Administration estimates. This represents roughly one-fifth of globally traded crude oil, making the waterway perhaps the world's most critical energy transit route.

The strategic significance extends beyond simple volume considerations to include the types of crude oil transported and destination markets served. Much of the crude flowing through Hormuz supplies Asian refineries, creating global supply chain interdependencies that affect pricing even in markets not directly served by these flows.

Geopolitical risk assessments typically add $5-15 per barrel in risk premiums during periods of elevated Strait disruption probability. These premiums operate independently of actual physical supply loss, demonstrating how market psychology amplifies the economic impact of geopolitical tensions.

Alternative routing costs through longer shipping routes around Africa or through the Suez Canal add 2-3 weeks to transit times and substantial additional expenses. Consequently, logistical challenges include port capacity limitations, vessel availability, and insurance cost increases that collectively reduce global oil supply efficiency.

Transmission Mechanisms from Global to Local Markets

International crude price volatility transmits to domestic fuel pricing through several interconnected pathways that operate at different speeds and magnitudes. Import-dependent economies experience the most rapid transmission, while nations with domestic refining capacity face delayed but substantial impacts through feedstock cost adjustments.

Currency exchange rate impacts compound crude price increases when local currencies weaken against the US Dollar. For Nigeria, Naira depreciation during periods of global oil market stress creates double exposure—both from higher crude prices and reduced purchasing power for international transactions, similar to patterns observed in US-China trade war effects.

Supply chain resilience factors affecting price stability include strategic petroleum reserve levels, alternative supplier relationships, and domestic refining flexibility. Nations with limited reserves and concentrated supplier bases experience more volatile pricing during global supply disruptions.

Risk premium calculations in crude oil pricing models incorporate geopolitical stability assessments, supply route security evaluations, and market speculation effects. These premiums can persist long after physical supply disruptions resolve, creating sustained price elevation even when underlying supply-demand fundamentals normalise.

Which African Economies Face Similar Energy Market Pressures?

Cross-continental analysis reveals varying degrees of vulnerability to international energy price shocks, with oil-producing nations experiencing paradoxical challenges despite resource abundance. The Iran crisis impact on Nigerian diesel prices reflects broader patterns affecting multiple African economies that depend on global energy markets for either crude imports or refined product supply, particularly when considering oil price trade war implications.

African nations display heterogeneous responses to global energy market disruptions based on domestic production capacity, refining infrastructure, import dependency ratios, and fiscal policy frameworks. Oil-producing countries face unique challenges as they balance export revenue optimisation with domestic energy security requirements.

Comparative Regional Analysis: Oil Producers vs. Import-Dependent States

Oil-producing African nations typically experience price impact ranges of 40-95% during major supply disruptions, with adjustment periods spanning 2-4 weeks as domestic pricing mechanisms respond to international market changes. These nations often struggle with the paradox of resource wealth creating domestic energy insecurity.

Table: African Diesel Price Responses to Global Tensions

| Country Category | Average Price Impact | Market Response Time | Policy Interventions |

|---|---|---|---|

| Oil Producers | +40-95% | 2-4 weeks | Limited subsidies |

| Import-Dependent | +25-60% | 1-2 weeks | Increased subsidies |

| Mixed Economies | +30-70% | 2-3 weeks | Targeted support |

Import-dependent economies often show more modest price impacts (+25-60%) but faster response times (1-2 weeks) as their pricing mechanisms directly reflect international market conditions without the complexity of balancing domestic production considerations. These nations frequently employ subsidy mechanisms to cushion consumer impact.

Mixed economies with both domestic production and import requirements typically experience intermediate impacts (+30-70%) over 2-3 week adjustment periods. Their policy responses often involve targeted support measures that balance fiscal sustainability with social stability considerations.

Economic Policy Responses and Market Interventions

Subsidy mechanisms across African nations vary significantly in scope, duration, and fiscal sustainability. Oil-producing countries often limit subsidy interventions due to competing priorities for petroleum revenue, while import-dependent nations may increase subsidies to maintain social stability during price shocks.

Price stabilisation strategies reflect different economic models and fiscal capacity constraints:

• Direct price controls: Government-mandated pricing that absorbs market volatility through fiscal transfers

• Strategic reserve utilisation: Drawing down petroleum stocks to maintain supply during disruptions

• Import diversification: Developing alternative supplier relationships to reduce dependence on disrupted routes

• Currency interventions: Central bank actions to limit exchange rate depreciation during commodity shocks

Long-term energy security planning initiatives increasingly focus on domestic refining capacity development, renewable energy diversification, and regional cooperation frameworks. These strategies aim to reduce vulnerability to external supply shocks while maintaining economic competitiveness.

What Are the Sectoral Economic Impacts of Rising Diesel Costs?

Diesel price increases create multiplier effects throughout Nigeria's economy, particularly affecting transportation, manufacturing, and power generation sectors that rely heavily on fuel-based operations. The 93.5% price increase from February to April 2026 represents a supply-side shock that ripples through interconnected economic systems with varying lag times and magnitudes, as documented in fuel price impact analysis.

Sectoral vulnerability assessments reveal differential impacts based on diesel intensity, substitution possibilities, and price pass-through mechanisms. Transportation and logistics sectors face immediate pressure due to high fuel dependency and limited short-term alternatives, while manufacturing industries experience more complex adjustment patterns.

Transportation and Logistics Sector Analysis

Transportation sectors across Nigeria rely heavily on diesel for freight movement, passenger services, and logistics operations. Commercial trucking, intercity bus services, and cargo distribution networks face immediate cost pressures when diesel prices increase dramatically, creating difficult decisions regarding service levels and pricing structures.

Cost pass-through mechanisms in freight and passenger transport typically operate through:

• Immediate surcharge applications: Additional fees applied to existing contracts to cover fuel cost increases

• Route optimisation strategies: Consolidating deliveries and reducing frequency to minimise fuel consumption

• Service level adjustments: Reducing capacity or eliminating marginally profitable routes

• Price renegotiation cycles: Longer-term contract adjustments reflecting new cost structures

Supply chain disruption patterns create cascading effects as transportation cost increases affect goods distribution across regional markets. Rural areas often experience disproportionate impact due to longer delivery distances and reduced route density that limits economies of scale.

Small business vulnerability assessments highlight particular challenges for operators with limited financial flexibility to absorb temporary cost shocks. Many small-scale transport operators lack access to hedging mechanisms or working capital reserves that could buffer fuel price volatility.

Manufacturing and Industrial Production Effects

Manufacturing sectors face diesel cost pressures through both direct energy consumption and indirect transportation expense increases. Energy-intensive industries including textiles, cement production, and food processing depend on diesel for backup power generation and industrial heating applications.

Energy cost components in production calculations vary by industry but typically represent 10-25% of total operating expenses for diesel-dependent manufacturers. When diesel prices increase by 90%+, these cost structures require fundamental recalibration that may affect production viability.

Competitiveness implications for export-oriented industries become particularly acute when domestic energy costs rise faster than international competitor costs. Nigerian manufacturers competing in regional markets may face disadvantages if their energy cost base increases while competitors maintain stable input costs.

Investment decision impacts include:

• Capacity expansion delays: Postponing growth investments until energy costs stabilise

• Technology upgrades: Accelerating adoption of energy-efficient equipment

• Alternative energy evaluation: Increased interest in renewable power solutions

• Location reassessment: Considering facility relocations to lower-cost energy zones

Capacity utilisation changes reflect manufacturer responses to higher operating costs, with some facilities reducing production schedules or implementing temporary shutdowns during peak energy cost periods. These adjustments can create employment effects and supply chain disruptions that extend beyond the energy sector.

How Might Nigeria's Energy Market Evolve Under Continued Global Tensions?

Forward-looking economic modelling suggests several potential scenarios for Nigeria's energy market development, depending on the duration and intensity of international supply disruptions. The Iran crisis impact on Nigerian diesel prices provides a foundation for understanding how continued geopolitical tensions might reshape domestic energy economics over different time horizons, particularly when considering oil price rally analysis for similar market conditions.

Market evolution trajectories depend on multiple variables including global supply route security, domestic refining capacity utilisation, crude oil production enhancement, and policy intervention effectiveness. Each scenario presents distinct implications for economic competitiveness, fiscal sustainability, and energy security.

Short-term Market Adjustment Mechanisms

Price elasticity considerations suggest that sustained high diesel costs will eventually trigger demand response patterns as consumers and businesses adapt to new cost structures. Initial adjustments typically focus on consumption optimisation rather than fundamental demand destruction, creating temporary market tightness.

Alternative fuel adoption rates may accelerate if diesel prices remain elevated for extended periods. Compressed natural gas (CNG) conversion for commercial vehicles, biodiesel blending programmes, and electric vehicle adoption could gain momentum as relative economics favour substitution.

Emergency policy intervention possibilities include:

• Strategic petroleum reserve releases: Government stockpile utilisation to moderate price spikes

• Import duty adjustments: Temporary tariff reductions on fuel imports

• Subsidy programme expansion: Direct consumer support to maintain affordability

• Exchange rate stabilisation: Central bank intervention to limit currency-driven price increases

Substitution effects become more pronounced as price differentials between diesel and alternatives widen. Industrial users may accelerate switching to natural gas or renewable energy sources, while transportation operators explore route optimisation and vehicle efficiency improvements.

Long-term Structural Transformation Opportunities

Scenario Analysis:

Optimistic Case: Enhanced domestic refining capacity and reduced import dependency through expanded crude production, improved Dangote Refinery feedstock sourcing, and development of additional refining infrastructure. This scenario assumes resolution of current supply chain constraints and successful energy security policy implementation.

Under optimistic conditions, Nigeria could achieve 70-80% energy self-sufficiency within 3-5 years through coordinated upstream and downstream development. Domestic crude production increases combined with refinery capacity optimisation would reduce vulnerability to external price shocks.

Base Case: Gradual market stabilisation with moderate price normalisation as global supply routes adapt to geopolitical realities. This scenario anticipates continued elevated energy costs relative to historical norms but avoids the extreme volatility experienced during acute crisis periods.

Base case assumptions include partial resolution of Strait of Hormuz disruptions, development of alternative supply routes, and moderate success in domestic energy security initiatives. Energy costs stabilise at 20-40% above pre-crisis levels while economic adaptation proceeds gradually.

Pessimistic Case: Prolonged elevated prices and economic adjustment challenges as global supply disruptions persist and domestic capacity enhancement faces implementation delays. This scenario involves sustained energy market stress testing economic resilience.

Pessimistic conditions could trigger broader economic adjustments including industrial restructuring, transportation sector consolidation, and fiscal policy strain as subsidy requirements exceed sustainable levels. Regional competitiveness deterioration may affect trade patterns and investment flows.

The next major ASX story will hit our subscribers first

What Investment and Policy Implications Emerge from This Crisis?

The current energy market disruption highlights critical infrastructure gaps and policy priorities for achieving greater energy security and economic resilience. The Iran crisis impact on Nigerian diesel prices demonstrates how quickly external shocks can erode domestic competitive advantages, emphasising the importance of comprehensive energy independence strategies.

Investment implications span both public and private sector priorities, requiring coordinated approaches to upstream production enhancement, downstream capacity optimisation, and alternative energy development. Policy frameworks must balance immediate crisis response with long-term structural transformation objectives.

Infrastructure Development Priorities

Refinery expansion and crude oil supply chain optimisation represent immediate priorities for reducing import dependency and enhancing price stability. Beyond the Dangote facility, Nigeria requires additional refining capacity and improved crude supply logistics to achieve meaningful energy security.

Key infrastructure development areas include:

• Upstream production enhancement: Increased domestic crude oil production to support refinery feedstock requirements

• Pipeline infrastructure: Improved crude transport from production areas to refining facilities

• Port capacity expansion: Enhanced petroleum product import/export handling capabilities

• Storage facility development: Strategic petroleum reserves and commercial inventory capacity

• Distribution network optimisation: Improved fuel delivery infrastructure to reduce transportation costs

Alternative energy source development and diversification strategies gain urgency as traditional energy security models prove vulnerable to external shocks. Solar, wind, and natural gas infrastructure development could provide hedging benefits against petroleum price volatility.

Strategic petroleum reserve establishment considerations involve determining optimal reserve sizes, crude versus product storage allocation, and funding mechanisms for maintaining emergency stockpiles. International best practices suggest reserves equivalent to 60-90 days of consumption provide meaningful price stabilisation capability.

Regulatory Framework Adaptations

Market mechanism improvements for price stability require balancing market efficiency with social protection objectives. Regulatory frameworks should facilitate private sector investment while maintaining oversight of essential services and strategic infrastructure.

International partnership strategies for energy security may include:

• Bilateral crude supply agreements: Long-term contracts with producing nations

• Regional refining cooperation: Shared infrastructure development with neighbouring countries

• Technology transfer partnerships: Collaboration on advanced refining and alternative energy technologies

• Financial cooperation: Development finance for energy infrastructure projects

Fiscal policy adjustments to manage transition costs include reviewing subsidy mechanisms, optimising petroleum revenue allocation, and developing sustainable financing structures for energy infrastructure investment. Balancing immediate crisis response with long-term fiscal sustainability requires careful policy calibration.

Frequently Asked Questions

Why hasn't the Dangote Refinery prevented Nigeria's diesel price increases?

Despite significant processing capacity, the refinery requires substantial crude oil imports due to local supply limitations, making it vulnerable to the same international price pressures affecting global markets. The facility needs 13-15 crude cargoes monthly but sources only about 5 domestically, creating 67-62% import dependency.

How long might elevated diesel prices persist in Nigeria?

Duration depends on geopolitical developments affecting global oil supply routes, with economists projecting potential price normalisation only after resolution of current international tensions. Base case scenarios suggest 20-40% elevation above historical norms may persist for 12-24 months.

Which sectors of Nigeria's economy face the greatest risk from continued high diesel prices?

Transportation, logistics, and manufacturing sectors face immediate pressure due to high fuel dependency, with potential cascading effects on food distribution and consumer goods pricing. Energy-intensive industries may experience particular challenges maintaining international competitiveness.

What alternative energy sources could reduce Nigeria's diesel dependency?

Compressed natural gas (CNG) for commercial vehicles, expanded electricity grid access for industrial applications, and renewable energy development for power generation represent the most viable near-term alternatives. Biodiesel blending programmes could provide additional supply diversification.

How do currency fluctuations affect Nigeria's fuel import costs?

Naira depreciation against the US Dollar compounds diesel price increases since international crude oil trades in dollars. Currency weakness creates double exposure through both higher commodity prices and reduced purchasing power for imports.

Disclaimer: This analysis involves forecasts and projections based on current market conditions and geopolitical developments. Actual outcomes may vary significantly based on evolving circumstances. Energy market investments carry substantial risk, and readers should conduct independent research before making financial decisions.

Are You Searching for Investment Opportunities in Nigeria's Evolving Energy Market?

The dramatic transformation of Nigeria's diesel market demonstrates how quickly global disruptions can create compelling opportunities for informed investors. Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries, including energy and commodity plays that could benefit from market volatility, helping subscribers stay ahead of emerging investment themes. Begin your 14-day free trial today to position yourself for potential market opportunities arising from global energy sector shifts.