May 21, 2026

The Commercial Logic Behind Long-Term Offtake Agreements in Critical Minerals Mining

Before a single tonne of ore moves through a processing circuit, the financial architecture of a mine restart is built on one foundational question: who is buying the output, and under what terms? In critical minerals, the answer determines whether a project transitions from care-and-maintenance status to active capital deployment. Without contracted revenue visibility, the internal rate-of-return calculations that govern board-level capital decisions remain speculative. With it, they become defensible.

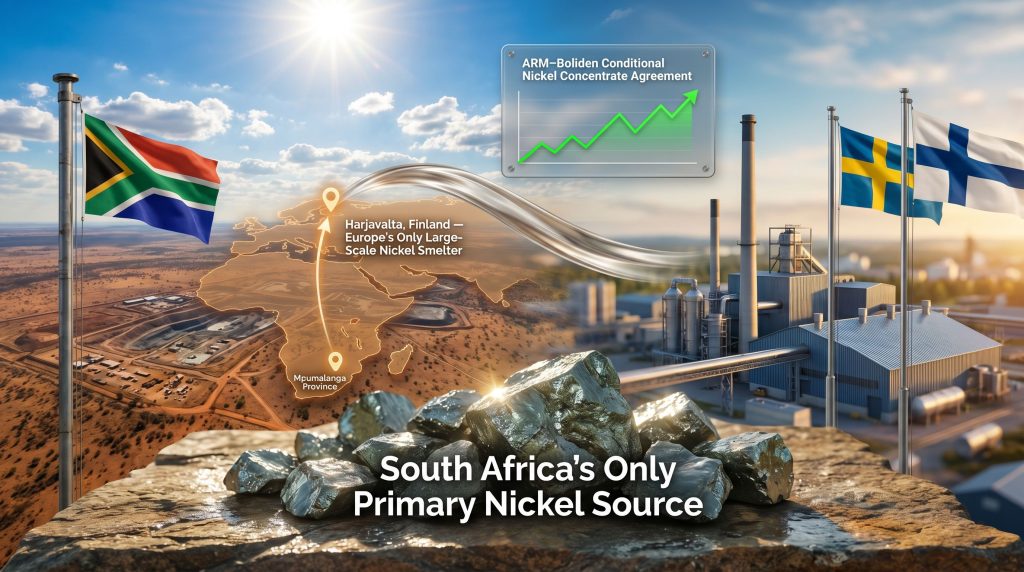

This mechanism sits at the heart of the Nkomati nickel mine restart deal with Boliden, a conditional offtake arrangement between South African diversified miner African Rainbow Minerals (ARM) and Swedish metals company Boliden Commercial AB. The agreement, reported by Bloomberg on 28 April 2026, would see nickel concentrate from the Mpumalanga-based Nkomati operation shipped to Boliden's Harjavalta smelter in Finland across a multi-year supply window — provided both parties satisfy their respective pre-conditions.

The deal is not yet binding. However, its commercial and strategic implications extend well beyond the two counterparties.

When big ASX news breaks, our subscribers know first

What the Conditional Agreement Actually Involves

Under the proposed arrangement, ARM would supply nickel concentrate produced at the Nkomati mine to Boliden's Harjavalta processing facility in Finland. The deal is structured as a multi-year offtake, though specific volume commitments, pricing mechanisms, and duration have not been disclosed publicly, with ARM citing confidentiality provisions.

Two conditions must be satisfied before the agreement becomes binding:

- ARM's board must grant formal approval to proceed with the mine restart

- Boliden must complete a responsible sourcing due diligence process assessing Nkomati's environmental management, labour standards, and governance frameworks

The Harjavalta smelter's strategic position amplifies the significance of this supply arrangement. It operates as the only large-scale nickel smelting facility on the European continent, functioning as an integrated smelter-refinery capable of converting nickel concentrate into refined cathode-grade metal suitable for battery and industrial end-uses. For any African nickel producer seeking European market access at scale, Harjavalta represents the sole viable processing node without routing through non-European jurisdictions.

The ARM-Boliden arrangement is structurally significant not just as a bilateral commercial transaction, but as a direct operationalisation of the Africa-to-Europe critical minerals supply corridor that European industrial policy is actively working to construct.

Why Nkomati Has Been Idle Since 2021 — And What Changed?

Nkomati holds a unique position within South Africa's mineral endowment as the country's sole primary nickel resource — distinguishing it from secondary nickel sources such as recycling streams or nickel recovered as a byproduct of other processing. Located in Mpumalanga Province, the mine was placed under care-and-maintenance in 2021 following a sustained period of financial losses driven by suppressed global nickel prices and elevated operating costs that made continued production economically unviable.

The mine's suspension reflected a rational capital preservation decision at the time, but it also carried long-term strategic consequences. A care-and-maintenance status means infrastructure remains in place but inactive, workforce numbers are substantially reduced, and equipment is mothballed rather than sold — preserving restart optionality without incurring full operating expenditure. This custodial approach typically costs a mid-scale operation tens of millions of rand annually just to maintain, creating ongoing holding costs without offsetting revenue.

The ownership structure also shifted materially in 2023. Nkomati had previously operated as a 50/50 joint venture between ARM and Russian mining group MMC Norilsk Nickel. ARM subsequently acquired the remaining 50% stake from Norilsk Nickel, achieving full sole ownership of the asset. This transition fundamentally changed the operational and strategic calculus for restart:

- Decision-making authority is now consolidated entirely within ARM, removing the bilateral approval requirement that previously complicated strategic pivots

- Economic upside from any successful restart accrues 100% to ARM rather than being shared with a joint venture partner

- Geopolitical complexity previously associated with a Russian co-ownership structure is eliminated, improving the asset's attractiveness to European ESG-conscious offtakers

The combination of sole ownership, improving battery demand fundamentals for nickel, and the availability of a willing European processor created the conditions under which the Boliden arrangement became commercially feasible.

Deconstructing the Restart Barriers and How This Deal Addresses Them

Prior to the Boliden agreement, the Nkomati restart faced four compounding barriers that made capital commitment to restart essentially unjustifiable from a risk-adjusted return perspective:

| Barrier | Description | Does the Boliden Deal Address It? |

|---|---|---|

| Buyer identification | No confirmed long-term offtaker for nickel concentrate | Yes — Boliden named as contracted buyer |

| Volume absorption | Uncertainty whether markets could absorb output | Yes — multi-year commitment provides absorption certainty |

| Logistics pathway | No established transport route to a named processor | Yes — Harjavalta identified as processing destination |

| Revenue certainty | Reliance on spot market pricing introduces cash flow variability | Partially — pricing terms undisclosed; spot exposure possible |

The deal directly resolves three of the four barriers and partially addresses the fourth, depending on whether the undisclosed pricing mechanism incorporates fixed, indexed, or spot-referenced components. In critical minerals transactions, offtake agreements commonly include price adjustment mechanisms linked to London Metal Exchange (LME) nickel benchmarks, which would still expose ARM to downside price scenarios while providing volume certainty.

In the critical minerals sector, securing an offtake agreement before committing restart capital converts speculative revenue projections into contracted cash flow visibility. It is the standard de-risking mechanism that separates investment-grade restart decisions from speculative capital allocation.

The Responsible Sourcing Due Diligence Requirement

One aspect of this deal that deserves particular attention is Boliden's mandatory responsible sourcing due diligence as a condition precedent. This reflects a structural shift in how European processors approach supply chain verification — driven by the EU Battery Regulation and broader procurement standards that require demonstrable traceability of critical mineral inputs. Furthermore, the growing importance of European critical raw materials supply frameworks has made such verification processes increasingly standard practice.

The due diligence process will evaluate:

- Environmental management practices at Nkomati and surrounding Mpumalanga operations

- Labour standards and community impact frameworks

- Governance structures and transparency reporting

- Alignment with internationally recognised ESG certification standards

A failure to satisfy Boliden's responsible sourcing threshold would effectively terminate the agreement before it becomes binding, representing a non-trivial execution risk that investors and analysts should monitor closely.

Europe's Nickel Supply Vulnerability and the Strategic Fit

Europe's industrial and battery manufacturing sectors face a structural supply challenge with nickel. The continent has minimal domestic primary nickel production capacity, and its historical reliance on Russian-origin nickel has come under intense scrutiny following geopolitical developments that have prompted European procurement managers to actively diversify supply sources. In this context, critical minerals energy security has become a central policy concern across the continent.

Simultaneously, Indonesian nickel industry growth has flooded global markets through high-pressure acid leach (HPAL) and rotary kiln electric furnace (RKEF) processing technologies, creating a structural oversupply dynamic that has weighed heavily on nickel prices. However, this Indonesian supply, while abundant in volume, presents different ESG characteristics compared to sulphide-based nickel from established mining jurisdictions like South Africa — a distinction that matters considerably to European battery manufacturers operating under increasingly stringent supply chain due diligence requirements.

South African sulphide nickel — the type Nkomati produces — carries specific metallurgical advantages worth understanding:

- Sulphide ores typically yield higher-grade concentrates than laterite ores processed via HPAL

- The concentrate produced is more directly amenable to conventional smelting at facilities like Harjavalta

- Sulphide operations generally carry a lower processing energy intensity per tonne of contained nickel compared to laterite hydrometallurgical routes

- The resulting refined nickel is well-suited to battery cathode manufacturing specifications

These metallurgical characteristics, combined with South Africa's established governance frameworks and ESG reporting infrastructure, position Nkomati's future output as a premium-quality supply option for a European processor increasingly constrained by responsible sourcing requirements.

ARM's Broader Portfolio Context and the Nickel Opportunity

African Rainbow Minerals, founded and largely owned by billionaire Patrice Motsepe, operates across a diversified commodity portfolio encompassing coal, gold, manganese, iron ore, and platinum group metals (PGMs). Nickel has historically contributed a relatively modest share of ARM's overall revenue mix, but the energy transition's demand for battery-critical materials has repositioned nickel's long-term strategic value within the portfolio.

The Nkomati nickel mine restart deal with Boliden, if successfully executed, would allow ARM to participate directly in the clean energy supply chain — a positioning the company has explicitly referenced as part of its strategic rationale for pursuing the agreement. This aligns with a broader trend among diversified African miners seeking to reframe legacy mineral assets through the lens of energy transition demand, attracting different categories of institutional investors and ESG-oriented capital.

Boliden's own portfolio spans copper, zinc, nickel, and lead, with operations across Sweden, Finland, Norway, and Ireland. Its Harjavalta facility has historically processed nickel from diverse global origins, making it operationally experienced in handling concentrate from varying geological sources — an operational characteristic that reduces technical integration risk for a new African supply relationship.

The next major ASX story will hit our subscribers first

Key Risks That Could Derail the Nkomati Restart

Nickel Price Economics and the Indonesian Oversupply Problem

The 2021 suspension was directly caused by nickel price weakness relative to Nkomati's operating cost structure. Any restart decision must therefore be stress-tested against realistic downside nickel price scenarios. Monitoring Indonesian nickel price trends is consequently essential for understanding the competitive pressure ARM's restart economics will face. Indonesian production continues to exert structural downward pressure on global nickel prices by adding significant Class 1 and Class 2 nickel supply to global markets.

ARM's restart economics will be acutely sensitive to the all-in sustaining cost (AISC) per tonne at Nkomati relative to prevailing and projected nickel prices. Underground mining configurations — which are reportedly under active evaluation — typically carry higher per-tonne operating costs than open-cut alternatives, setting a higher nickel price threshold for commercial viability.

Underground Mining Complexity and Restart Capital Requirements

Returning a mothballed underground mine to production is operationally and financially demanding. The rehabilitation sequence typically involves:

- Underground infrastructure assessment and structural certification

- Ventilation, dewatering, and ground support rehabilitation

- Workforce mobilisation, training, and safety induction programs

- Equipment recommissioning and capital replacement where deterioration exceeds acceptable thresholds

- Regulatory and environmental compliance updates under South African mining law

- Community engagement and social licence renewal in Mpumalanga

Mine restarts of this complexity historically require 18 to 36 months from board approval to first production, depending on rehabilitation scope and regulatory processing speed. Furthermore, a comprehensive definitive feasibility study will likely be required before capital deployment decisions can be formally sanctioned. This timeline carries its own financial carrying cost that must be modelled into restart feasibility calculations.

Conditions Status at a Glance

| Condition | Responsible Party | Current Status |

|---|---|---|

| Board approval for restart | African Rainbow Minerals | Pending |

| Responsible sourcing due diligence | Boliden Commercial AB | In progress |

| Underground mining feasibility assessment | ARM technical teams | Under evaluation |

| Regulatory and environmental approvals | South African authorities | Not yet initiated |

| Commercial terms finalisation | Both parties | Undisclosed |

How This Deal Compares to Other Africa-Europe Critical Minerals Arrangements

The Nkomati nickel mine restart deal with Boliden is notable within the landscape of Africa-to-Europe critical minerals supply frameworks for its operational specificity — a named mine, a named smelter, a defined product type, and a conditional commercial structure. This distinguishes it from broader government-level framework agreements that typically characterise African-European critical minerals diplomacy, which often lack the granular commercial detail necessary to translate policy intent into physical supply chain reality.

| Arrangement | African Producer | European Partner | Mineral | Structure |

|---|---|---|---|---|

| ARM-Boliden (Nkomati) | African Rainbow Minerals, South Africa | Boliden AB, Sweden/Finland | Nickel concentrate | Conditional bilateral offtake |

| EU-DRC Critical Minerals MOU | DRC Government | European Commission | Cobalt, lithium | Government framework |

| Glencore-European battery offtakes | Glencore, multi-jurisdiction | Various EU battery manufacturers | Cobalt, nickel | Active commercial contracts |

The ARM-Boliden model represents the most commercially advanced stage of Africa-Europe nickel supply chain development currently publicly known — a bilateral arrangement between two named commercial counterparties with defined product specifications and conditional contract structure, rather than aspirational framework language. Mining Weekly has noted that this offtake deal sets a meaningful precedent for how future African-European mining partnerships may be structured.

What the Nkomati Deal Signals for South Africa's Mining Sector

Beyond the specific economics of Nkomati, this arrangement carries broader implications for South Africa's positioning as a critical minerals supplier to Western industrial economies. The country's established mining regulatory framework, its rule-of-law governance environment relative to other African mining jurisdictions, and its existing ESG reporting infrastructure collectively position it as a preferred partner for European processors.

A successful restart would also validate a wider thesis: that mothballed African mining assets previously considered economically unviable at pre-energy-transition nickel prices may be commercially rehabilitatable as battery demand reshapes the long-run price floor for battery-grade nickel. This thesis, if proven at Nkomati, could encourage similar feasibility reassessments at other idled operations across the Southern African mineral belt.

For Mpumalanga Province specifically, a restart would reinstate direct mining employment in a region with significant economic dependence on the extractive sector — a social dimension that strengthens the project's community licence to operate and aligns with South African government priorities around mining-led economic development, though no specific government support for the Nkomati restart has been confirmed.

Frequently Asked Questions About the Nkomati Nickel Mine Restart Deal with Boliden

What is the Nkomati nickel mine?

Nkomati is South Africa's only known primary nickel mining operation, located in Mpumalanga Province. It has been under care and maintenance since 2021 and is currently 100% owned by African Rainbow Minerals following the exit of former joint venture partner MMC Norilsk Nickel in 2023.

Who is Boliden and what is the Harjavalta facility?

Boliden AB is a Swedish metals company producing copper, zinc, nickel, and lead across multiple European operations. Its Harjavalta facility in Finland is the only large-scale nickel smelter on the European continent, making it the critical processing intermediary between African mining output and European battery and industrial end-users.

Is the Nkomati mine restart confirmed?

No. The restart remains subject to formal board approval from ARM and the successful completion of responsible sourcing due diligence by Boliden. The current agreement is conditional, not binding.

What type of nickel does Nkomati produce?

Nkomati produces sulphide-based nickel concentrate, a metallurgically distinct product from the laterite-derived nickel that dominates Indonesian production. Sulphide nickel typically yields higher-grade concentrate more directly amenable to conventional smelting and is generally considered better suited to European battery cathode manufacturing specifications.

Why does Europe need African nickel specifically?

European battery manufacturing requires responsibly sourced, traceable nickel inputs under increasingly stringent supply chain regulations. Limited domestic European production and growing policy pressure to reduce dependence on Russian and Indonesian supply have elevated African producers operating under internationally recognised ESG frameworks to strategically preferred supplier status.

What happened to Norilsk Nickel's stake in Nkomati?

MMC Norilsk Nickel held a 50% interest in Nkomati through a joint venture with ARM. Following the mine's 2021 suspension, Norilsk Nickel divested its 50% stake and ARM acquired full ownership of the operation in 2023.

This article is based on publicly available information reported by Business Insider Africa on 28 April 2026. It contains forward-looking analysis and speculative assessments regarding mine restart timelines, market conditions, and commercial outcomes. These represent analytical perspectives and not investment advice. Readers should conduct independent due diligence before making any investment decisions related to companies or assets discussed herein.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across nickel, copper, and more than 30 other commodities — translating complex data into actionable investment insights for traders and long-term investors alike. Explore historic discoveries and their exceptional market returns, then begin your 14-day free trial to position yourself ahead of the broader market.