May 19, 2026

Nordic Energy Infrastructure Creates Perfect Storm for Manufacturing Revolution

The convergence of abundant renewable energy resources, established industrial infrastructure, and aggressive decarbonisation policies has positioned northern European economies at the forefront of a fundamental shift in heavy manufacturing. Traditional energy-intensive industries face unprecedented pressure to eliminate carbon emissions while maintaining competitive production costs and global market access. This transformation extends far beyond environmental compliance, representing a complete reimagining of how the green steel project in Sweden and other carbon-intensive materials will be produced in the coming decades.

Sweden's unique combination of hydroelectric power generation, advanced grid infrastructure, and proximity to high-grade raw materials has created optimal conditions for pioneering next-generation manufacturing technologies. The country's industrial policy framework emphasizes technology leadership in clean production methods, attracting significant international investment and establishing Sweden as a testing ground for scalable solutions that could reshape global supply chains.

When big ASX news breaks, our subscribers know first

What Makes Sweden the Global Leader in Green Steel Innovation?

Nordic Advantages in Renewable Energy Infrastructure

Sweden's renewable energy foundation provides unparalleled advantages for energy-intensive manufacturing processes. The country generates approximately 96% of its electricity from renewable and nuclear sources, with hydroelectric power providing baseload stability crucial for industrial operations. This energy mix offers both cost predictability and carbon-free production, essential requirements for competitive green steel manufacturing.

The Swedish electrical grid demonstrates exceptional reliability and stability, critical factors for continuous industrial processes that cannot tolerate power interruptions. Advanced grid management systems integrate variable renewable sources while maintaining the consistent power quality required for precision manufacturing equipment. Long-term power purchase agreements with renewable energy providers offer industrial customers electricity pricing that remains competitive with fossil fuel-based alternatives.

Strategic positioning within the Nordic power market provides additional flexibility through interconnected transmission networks. During periods of excess renewable generation, Swedish manufacturers can access surplus clean electricity from neighbouring countries, while grid exports during lower demand periods help optimise overall system efficiency.

Raw Material Access and Logistics Advantages

Northern Sweden hosts some of Europe's highest-grade iron ore deposits, with ore purity levels exceeding 65% iron content. This superior raw material quality reduces processing requirements and energy consumption compared to lower-grade ores used in many global steel production facilities. The established mining infrastructure includes specialised transportation networks designed for efficient bulk material movement.

The existing logistics framework connecting mining regions to coastal ports provides direct access to international markets without requiring extensive new infrastructure development. Rail transportation networks specifically designed for iron ore transport offer energy-efficient material movement while minimising additional carbon emissions from logistics operations.

Supply chain optimisation benefits extend beyond raw materials to include specialised equipment and technical expertise. Sweden's established industrial ecosystem includes engineering firms, equipment manufacturers, and technical service providers experienced in large-scale industrial projects, reducing implementation risks and project development timelines.

The Technology Behind Sweden's Green Steel Breakthrough

Hydrogen-Based Direct Reduction Process Explained

Green steel production replaces traditional coal-based blast furnace technology with hydrogen-based direct reduction systems that eliminate carbon dioxide emissions from the iron-making process. Hydrogen gas serves as the reducing agent, chemically removing oxygen from iron ore to produce direct reduced iron (DRI) suitable for electric arc furnace steelmaking.

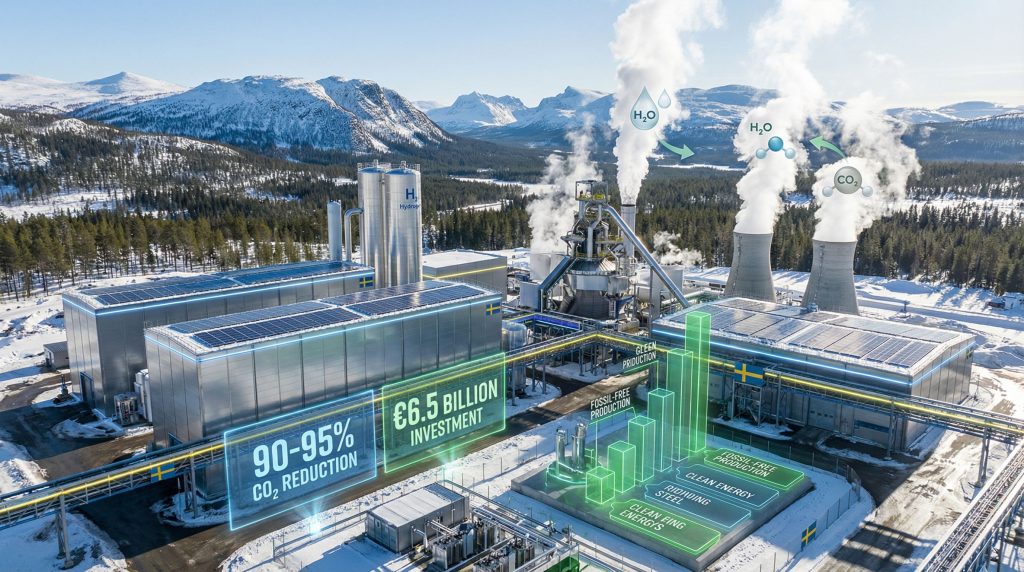

The chemical reaction produces water vapour instead of CO₂, fundamentally altering the environmental impact of steel production. Traditional blast furnace operations generate approximately 2.3 tons of CO₂ per ton of steel produced, while hydrogen-based systems reduce emissions by 90-95% when powered by renewable electricity.

Key Process Advantages:

- Energy Efficiency: Hydrogen reduction requires approximately 3.5 MWh of renewable electricity per ton of steel

- Output Quality: DRI produces high-purity steel suitable for premium applications

- Operational Flexibility: Production can be adjusted based on renewable energy availability

- Scalability: Technology proven at demonstration scale with clear pathways to commercial implementation

Integrated Production Systems and Circular Economy Design

Modern green steel facilities integrate multiple production systems to maximise energy efficiency and minimise waste streams. On-site electrolyser installations produce green hydrogen directly from renewable electricity, eliminating transportation costs and ensuring consistent hydrogen supply for steel production operations.

Waste heat recovery systems capture thermal energy from various production processes to power auxiliary operations and improve overall energy efficiency. Digital automation technologies optimise production scheduling to align with renewable energy availability patterns, maximising the utilisation of low-cost clean electricity.

Industry 4.0 Implementation Features:

- Predictive maintenance systems reduce unplanned downtime

- Real-time energy management optimises electricity consumption

- Quality control automation ensures consistent product specifications

- Supply chain integration coordinates raw material delivery with production schedules

| Production Method | CO₂ Emissions | Energy Source | Output Quality | Investment Required |

|---|---|---|---|---|

| Traditional Blast Furnace | 2.3 tons CO₂/ton steel | Coal/Coke | Standard | Moderate |

| Green Steel (H2-DRI) | 0.1-0.2 tons CO₂/ton steel | Green Electricity | Premium | High Initial |

Economic Impact Analysis of Sweden's Green Steel Initiative

Investment Flows and Financial Structure

The Swedish green steel sector has attracted over €6.5 billion in committed funding, representing one of Europe's largest industrial decarbonisation investments. This includes significant EU Innovation Fund support and private sector partnerships across the value chain. Stegra's €1.4 billion funding commitment demonstrates the scale of capital allocation required for commercial-scale green steel production facilities.

Funding Sources Include:

- European Union Innovation Fund grants supporting first-of-kind technology deployment

- Development bank financing providing long-term capital at favourable rates

- Strategic investor partnerships from steel customers seeking secure green supply chains

- Government-backed loan guarantees reducing project financing costs

The financial structure reflects both the technological risks associated with scaling emerging technologies and the market opportunities created by increasing demand for low-carbon steel products. Risk-sharing mechanisms between public and private investors help bridge the gap between demonstration projects and commercial-scale operations.

Job Creation and Regional Economic Development

Construction phase employment for major green steel projects creates over 4,000 temporary positions during peak development periods, providing significant economic stimulus for northern Swedish communities. Permanent operational workforce requirements exceed 2,000 specialised roles, including engineers, technicians, and skilled operators trained in advanced manufacturing technologies.

Regional Economic Multiplier Effects:

- Local supplier development for maintenance and operational services

- Training institution partnerships developing specialised technical skills

- Housing and infrastructure investment supporting workforce expansion

- Service sector growth driven by increased regional employment and income

The skills development programmes created to support green steel operations provide transferable expertise applicable to other clean technology industries. Furthermore, these developments leverage extensive decarbonisation benefits that position the region as a centre of excellence for sustainable manufacturing technologies.

The Swedish green steel sector represents one of Europe's most significant industrial transformation projects, combining cutting-edge technology with substantial economic development opportunities for traditionally manufacturing-dependent regions.

Global Supply Chain Implications for Green Steel Adoption

Automotive Industry Transformation Requirements

Premium automotive manufacturers face increasing pressure to reduce supply chain carbon emissions, with sustainability commitments requiring significant reductions in steel-related emissions by 2030-2035. The green steel project in Sweden represents a critical pathway for meeting these targets while maintaining product quality and performance standards.

Supply Chain Decarbonisation Mandates:

- Scope 3 emissions reporting requiring detailed supplier carbon tracking

- Carbon neutral vehicle production targets driving demand for clean materials

- Customer preference shifts toward environmentally responsible products

- Regulatory requirements in key markets mandating emission reductions

The cost implications of green steel integration vary depending on application requirements and production volumes. Premium vehicle segments can absorb higher material costs more readily than mass-market applications, creating initial market opportunities for green steel producers.

Construction and Infrastructure Sector Adaptation

Building industry carbon footprint reduction targets drive increasing demand for low-emission construction materials. Green building certification programmes award additional points for using materials with verified low-carbon production processes, creating market incentives for green steel adoption.

Market Transformation Factors:

- Public procurement policies prioritising sustainable materials

- Building code updates incorporating carbon emission requirements

- Life-cycle assessment standards quantifying material environmental impact

- Green financing incentives supporting sustainable construction projects

Long-term procurement strategies are shifting toward sustainable materials as construction companies recognise the competitive advantages of early green steel adoption and the risk mitigation benefits of securing low-carbon supply chains.

Competitive Landscape and Market Positioning Analysis

European Green Steel Development Race

Germany's hydrogen steel initiatives include major projects targeting commercial production by 2027-2028, creating competitive pressure for Swedish developers to accelerate deployment timelines. thyssenkrupp and Salzgitter investments in hydrogen-based steel production represent significant competitive challenges requiring differentiated technology approaches.

Cross-Border Collaboration Opportunities:

- Technology sharing agreements reducing development costs and risks

- Joint procurement initiatives for specialised equipment and materials

- Workforce training programmes developing region-wide technical expertise

- Infrastructure coordination optimising renewable energy and hydrogen transportation networks

The Netherlands' sustainable steel transition programmes focus on carbon capture integration with existing blast furnace operations, representing an alternative pathway that may offer faster implementation but potentially higher long-term operating costs compared to hydrogen-based approaches.

Global Competition from Asia-Pacific and North America

China's green steel development strategies emphasise massive production scale and cost optimisation, potentially creating significant competitive pressure on European producers. State-supported investment programmes in China may enable faster capacity scaling than market-driven European approaches.

North American clean energy steel projects benefit from abundant renewable energy resources and substantial policy support through climate legislation providing production tax credits and investment incentives. Technology transfer agreements with European developers may accelerate North American deployment.

Intellectual Property Considerations:

- Patent protection strategies for key production technologies

- Trade secret management for operational optimisation techniques

- Licensing opportunities for international market expansion

- Collaborative research agreements advancing fundamental technology development

The next major ASX story will hit our subscribers first

What Are the Technical Challenges Facing Green Steel Scale-Up?

Electrolyser Technology and Hydrogen Production Scaling

Current electrolyser capacity limitations represent the most significant bottleneck for green steel scale-up. Global electrolyser manufacturing capacity must increase by over 1000% by 2030 to support planned green steel production targets. Technology reliability remains a concern for continuous industrial operations requiring 99%+ uptime.

Scaling Challenges Include:

- Equipment procurement lead times extending 18-24 months for large installations

- Skilled technician shortages for electrolyser operation and maintenance

- Integration complexity with existing steel production systems

- Performance optimisation under varying renewable energy input conditions

Maintenance considerations for electrolyser systems operating at industrial scale require developing new service models and spare parts supply chains. Technology evolution continues rapidly, creating decisions about equipment standardisation versus performance optimisation.

Grid Infrastructure and Renewable Energy Demands

Massive electricity requirements for large-scale green steel operations strain existing grid infrastructure and renewable energy supply systems. A 5-million-ton annual facility requires approximately 17.5 TWh of renewable electricity, equivalent to a large wind farm or hydroelectric installation.

Grid Stability Challenges:

- Peak demand management during maximum production periods

- Power quality maintenance for sensitive industrial equipment

- Backup power systems ensuring continuous operations during grid disturbances

- Load balancing coordination with other industrial customers

Renewable energy procurement strategies must balance cost optimisation with supply security, often requiring complex long-term contract structures and risk management mechanisms. Furthermore, these challenges highlight the importance of comprehensive energy transition insights that can inform strategic planning decisions.

Green steel production requires approximately 3.5 MWh of renewable electricity per ton of steel, compared to traditional methods that rely on coal-based energy. Sweden's abundant hydroelectric resources provide a competitive advantage in meeting these energy-intensive requirements.

Market Adoption Timeline and Commercial Viability

Production Capacity Ramp-Up Scenarios

Phase 1 operations targeting initial production by 2026-2028 focus on technology validation and customer qualification processes. Full-scale commercial operations planned for 2030 require successful completion of financing, construction, and commissioning phases.

Market Penetration Projections:

- 2026-2028: 1-2% of European steel production from green steel sources

- 2030: 5-8% market share assuming successful scaling of multiple projects

- 2035: 15-25% penetration with supportive policy frameworks and cost competitiveness

- 2040: 40-50% market transformation driven by regulatory requirements and customer preferences

Customer adoption patterns vary significantly by end-use application and geographic market. Premium segments adopt green steel earlier despite higher costs, while mass market applications require substantial cost reductions for widespread adoption.

Price Premium Evolution and Cost Competitiveness

Current green steel pricing commands a 10-30% premium over conventional steel, but this gap is expected to narrow significantly by 2030 as production scales and carbon pricing increases. Learning curve effects and economy of scale benefits drive cost reductions as the industry matures.

Cost Competitiveness Factors:

- Carbon pricing impact on traditional steel production costs

- Renewable energy cost trends affecting green steel operating expenses

- Technology improvement reducing capital and operational requirements

- Supply chain optimisation through increased market scale

Price parity scenarios depend heavily on carbon price evolution and regulatory frameworks that internalise environmental costs. Breakthrough cost reductions may occur faster than current projections if technology development accelerates beyond expected rates.

Policy Framework and Regulatory Environment

EU Green Deal Implementation and Steel Sector Requirements

Carbon border adjustment mechanism implementation creates significant competitive advantages for EU green steel producers by imposing carbon costs on imported conventional steel. Emissions trading system reforms increase carbon prices affecting traditional steel production economics.

Key Regulatory Developments:

- State aid rules for green technology investments allowing substantial public support

- Industrial emissions standards tightening requirements for conventional steel production

- Green taxonomy classification providing financing advantages for sustainable steel projects

- Public procurement mandates prioritising low-carbon materials in government contracts

EU Innovation Fund support provides crucial risk mitigation for first-of-kind technology deployment, bridging the gap between demonstration projects and commercial viability. Additionally, the implementation of comprehensive renewable energy solutions supports infrastructure investments required for green steel production.

National Swedish Policy Support and Incentives

Swedish government backing for industrial decarbonisation projects includes research and development funding, infrastructure investment coordination, and regulatory streamlining for green technology deployment. National climate targets create strong policy incentives supporting green steel development.

Policy Support Mechanisms:

- Investment grants for clean technology deployment

- Tax incentives for renewable energy utilisation

- Regulatory fast-tracking for strategic industrial projects

- Skills development funding for workforce training programmes

Infrastructure coordination between national, regional, and local authorities ensures efficient project development and minimised regulatory delays. International cooperation agreements facilitate technology sharing and market development across Nordic countries.

Environmental and Sustainability Metrics

Carbon Footprint Reduction Achievements

Life-cycle assessment comparisons demonstrate green steel's superior environmental performance across multiple impact categories. Scope 1 emissions from hydrogen-based production are essentially zero, while Scope 2 emissions depend entirely on renewable electricity grid intensity.

Scope 3 emissions analysis includes upstream impacts from renewable energy infrastructure construction and raw material extraction, still showing substantial advantages over conventional steel production. Water usage optimisation and waste stream minimisation provide additional environmental benefits.

| Impact Category | Traditional Steel | Green Steel | Improvement |

|---|---|---|---|

| CO₂ Emissions (tons/ton steel) | 2.3 | 0.1-0.2 | 90-95% reduction |

| Water Usage (m³/ton steel) | 25-30 | 15-20 | 30-40% reduction |

| Energy Intensity (GJ/ton steel) | 20-25 | 18-22 | 10-20% reduction |

Circular Economy Integration and Resource Efficiency

Scrap steel utilisation in electric arc furnace operations enables circular material flows while maintaining green production credentials. By-product valorisation strategies convert production waste streams into useful materials for other industries.

Resource Efficiency Strategies:

- Sustainable mining practices for raw material sourcing

- Waste heat utilisation for auxiliary processes and heating applications

- Water recycling systems minimising freshwater consumption

- Material recovery programmes capturing and reusing production by-products

Sustainable mining integration ensures raw material sourcing aligns with overall sustainability objectives, including biodiversity protection and community engagement in mining regions.

Future Outlook and Industry Transformation Scenarios

Technology Evolution and Next-Generation Innovations

Advanced electrolyser technologies under development promise higher efficiency and improved reliability for industrial-scale hydrogen production. Integration with carbon capture and utilisation systems may enable additional emission reductions and revenue streams from captured CO₂.

Artificial Intelligence Optimisation:

- Predictive maintenance algorithms reducing equipment downtime

- Energy management systems optimising renewable electricity utilisation

- Quality control automation ensuring consistent product specifications

- Supply chain coordination integrating multiple production facilities

Next-generation innovations may include direct electrification of iron-making processes and advanced material recovery techniques enabling higher circularity rates. Moreover, AI optimization in operations could fundamentally alter production economics and environmental performance.

Market Expansion and Global Replication Potential

Technology transfer to other European steel-producing regions requires addressing site-specific constraints including renewable energy availability, raw material access, and existing infrastructure capabilities. Emerging market adoption depends on economic development priorities and financing availability.

International Cooperation Frameworks:

- Technology sharing agreements accelerating global deployment

- Capacity building programmes developing technical expertise in emerging economies

- Financing mechanisms supporting clean technology investment in developing countries

- Standards development ensuring global compatibility and quality consistency

Global replication scenarios range from rapid technology diffusion driven by climate commitments to gradual adoption constrained by economic and technical barriers. Success factors include supportive policy frameworks, adequate financing, and skilled workforce development.

FAQ Section

How much more expensive is green steel compared to traditional steel?

Current green steel commands a 10-30% premium, but this gap is expected to narrow significantly by 2030 as production scales and carbon pricing increases.

Can green steel meet the same quality standards as conventional steel?

Yes, hydrogen-based direct reduction produces steel that meets or exceeds traditional quality specifications, with some applications showing superior properties.

What renewable energy capacity is needed for large-scale green steel production?

A 5-million-ton annual facility requires approximately 17.5 TWh of renewable electricity, equivalent to a large wind farm or hydroelectric installation.

Investment Implications for Stakeholders

Opportunities for Clean Technology Investors

Equipment manufacturers developing electrolyser technology, electric arc furnaces, and digital control systems benefit from substantial market opportunities as green steel production scales. Renewable energy developers secure long-term power purchase agreements providing stable revenue streams.

Investment Opportunities Include:

- Technology licensing for international market expansion

- Engineering services for project development and optimisation

- Logistics infrastructure supporting material flows and product distribution

- Financial services providing specialised financing for industrial projects

Power purchase agreements with green steel producers offer 20-30 year contract terms providing exceptional visibility for renewable energy investment returns. Infrastructure investments in grid capacity and hydrogen transportation create additional opportunities.

Risks and Mitigation Strategies

Technology deployment risks include performance guarantees, cost overruns, and schedule delays common with first-of-kind industrial projects. Market demand volatility may affect project economics if customer adoption patterns differ from projections.

Risk Mitigation Approaches:

- Insurance products covering technology performance and business interruption

- Long-term sales contracts providing revenue certainty for project financing

- Diversified customer bases reducing dependence on individual market segments

- Flexible production systems enabling response to market conditions

Regulatory stability concerns require policy risk assessment and contingency planning for potential changes in government support or carbon pricing mechanisms. International market access depends on trade policies and standards harmonisation affecting global competitiveness. In conclusion, the green steel project in Sweden represents a transformative opportunity that could revolutionise the global steel industry while delivering substantial economic and environmental benefits.

The information presented in this analysis is based on publicly available data and industry projections. Industrial technology investments involve substantial risks, and potential investors should conduct thorough due diligence and consult with qualified advisors before making investment decisions.

Interested in Investing in Nordic Green Technology Companies?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, including companies involved in critical materials essential for green technology manufacturing like battery metals and rare earth elements. Subscribers gain immediate insights into actionable opportunities in the clean energy transition, positioning themselves ahead of broader market awareness of breakthrough discoveries that could transform the sustainable materials supply chain.