June 23, 2026

Why small imbalances can still move the palladium market

In commodity investing, the most misleading word is often surplus. A market can look loose in a spreadsheet yet remain highly vulnerable in practice when supply is concentrated, inventories are opaque, and discretionary buying can change the balance quickly. That is exactly why the Norilsk Nickel palladium surplus forecast matters beyond a single producer update.

Palladium is not a giant bulk commodity with deep liquidity and broad geographic diversification. It is a narrower market where mine output is concentrated in a small number of regions, recycling plays a meaningful role, and shifts in autocatalyst demand, substitution, and investment flows can alter sentiment fast.

Furthermore, for analysts, the key question is not simply whether the market is in surplus, but what kind of surplus it is. That wider lens also helps when comparing the PGM complex with broader critical minerals demand trends across global resource markets.

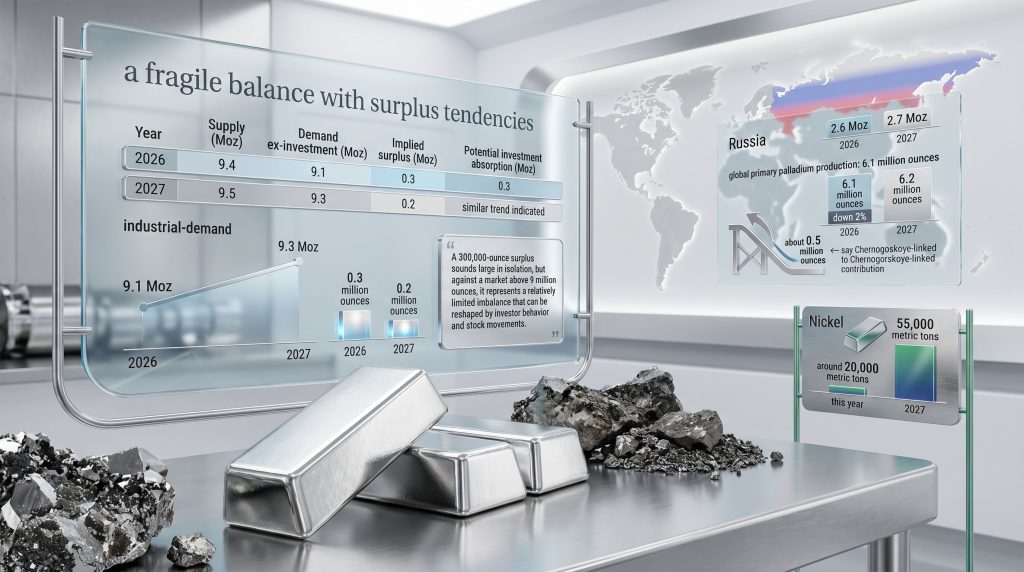

The Norilsk Nickel palladium surplus forecast refers to an expected global oversupply of palladium in which total supply exceeds industrial demand. For 2026, the projected gap is 0.3 million ounces before investment demand and stock changes are included, so the real-world market may appear tighter than the headline suggests.

When big ASX news breaks, our subscribers know first

Which hard numbers define the current palladium balance?

The core figures point to a market that is only modestly oversupplied on an underlying basis.

| Year | Supply (Moz) | Demand ex-investment (Moz) | Implied surplus (Moz) | Potential investment absorption (Moz) |

|---|---|---|---|---|

| 2026 | 9.4 | 9.1 | 0.3 | 0.3 |

| 2027 | 9.5 | 9.3 | 0.2 | similar balancing trend indicated |

These numbers are important because they reshape the tone of the discussion:

- 2026 supply is estimated at 9.4 million ounces, against 9.1 million ounces of demand excluding investment.

- 2027 supply is estimated at 9.5 million ounces, versus 9.3 million ounces of demand excluding investment.

- The resulting surplus narrows from 0.3 million ounces in 2026 to 0.2 million ounces in 2027.

- Preliminary investment demand in 2026 is estimated at 0.3 million ounces, enough to absorb the entire headline surplus if it materialises.

Consequently, a 300,000-ounce surplus sounds dramatic in isolation, yet in a market exceeding 9 million ounces, it represents a limited imbalance rather than an overwhelming glut.

What does excluding investment and stock movements mean?

Many readers misread palladium market balance figures because they assume supply and demand tables capture every force acting on the metal. However, they do not. In this framework, analysts isolate the industrial market first and only then consider discretionary flows.

When a forecast says excluding investment and stock movements, it usually means the following:

- Mine supply and recycled supply are added together.

- Fabrication and industrial use are measured across key end markets.

- Exchange-traded holdings, bar-and-coin demand, private investment accumulation, and inventory changes are excluded.

- The result is the underlying physical-industrial balance.

- Investment demand is then layered back in to test whether the apparent surplus still exists.

This distinction matters because a market can appear oversupplied on paper while remaining effectively balanced once investor buying or stock draws are considered.

Where is the surplus coming from if primary palladium output is falling?

At first glance, the supply story looks contradictory. Global primary palladium production is forecast to fall 2% year on year to 6.1 million ounces in 2026, yet the broader market still shows a surplus. The explanation is that total available supply depends on more than fresh mine output alone.

A few moving parts help explain the resilience:

- Primary palladium production falls to 6.1 million ounces in 2026.

- It is expected to recover slightly to 6.2 million ounces in 2027.

- South African output is described as broadly stable.

- North American producers remain cautious, limiting aggressive supply expansion.

- Recycling and pre-existing production streams help cushion the market even when mined output softens.

- New feed from ramp-up projects can support future refined metal availability.

Lower grades are a critical but often overlooked detail. In mining terms, lower grades mean less payable metal is recovered per tonne of ore. As a result, more material must be mined, unit costs can rise, and producers may delay expansion if margins tighten.

Why Russia remains central to the global palladium outlook

Russia continues to occupy an outsized position in the palladium supply chain. Forecast output is 2.6 million ounces in 2026 and 2.7 million ounces in 2027, which means even a relatively small percentage change in Russian production can shift the global market balance.

That concentration creates two parallel realities:

- The market can appear numerically comfortable.

- The market can still be functionally fragile.

According to a Nornickel market review, the company sees both palladium and nickel moving into surplus conditions over the medium term. In addition, Reuters-reported coverage on projected global palladium surplus has reinforced how closely the market watches Russian supply assumptions.

One of the most important medium-term variables is the ramp-up associated with the Chernogorskoye deposit. The project is expected to contribute to Russian supply recovery in 2027, and over the longer term it could add about 0.5 million ounces per year to Russian palladium output.

In a market with a projected surplus of only 0.2 million to 0.3 million ounces, that is material. Furthermore, the same sensitivity is often seen in other concentrated metal chains, including platinum and palladium market dynamics.

Is palladium demand weak or just changing shape?

The demand figures do not point to collapse. Demand excluding investment rises from 9.1 million ounces in 2026 to 9.3 million ounces in 2027. That suggests palladium is still seeing meaningful end-use demand, but growth may be too slow to absorb supply comfortably if recycling and mine supply remain resilient.

The main demand buckets likely include:

- Automotive autocatalysts

- Electronics

- Chemical applications

- Jewellery

- Hydrogen-related uses

One structural issue investors should not ignore is substitution with platinum. If relative pricing makes platinum more attractive for autocatalyst formulations, palladium demand growth can be capped even when vehicle production is stable.

This is also why silver is sometimes discussed as a precious and industrial metal: industrial usage patterns can reshape price expectations well beyond simple supply headlines.

The next major ASX story will hit our subscribers first

Could investment demand erase the palladium surplus?

Yes, at least on the current numbers. If investment demand reaches 0.3 million ounces in 2026, it could absorb the full projected surplus. That is why price forecasting cannot rely on mine supply alone.

| Scenario | Investment demand assumption | Balance impact | Likely price implication | Risk level |

|---|---|---|---|---|

| Base case | Moderate | Surplus remains visible | Range-bound to soft | Medium |

| Investment absorption case | Around 0.3 Moz | Market roughly balances | Firmer than headline surplus implies | Medium |

| Weaker investment case | Below expected | Visible oversupply expands | Greater downside pressure | High |

| Stronger industrial recovery case | Stable to positive | Surplus narrows faster | Supportive for prices | Medium to High |

Palladium is especially sensitive to this dynamic because it is a relatively small market. Investor behaviour, ETF changes, private stock accumulation, and sentiment shifts can all have an outsized impact compared with larger commodity markets.

How should investors interpret a surplus in a concentrated market?

A headline palladium surplus does not remove geopolitical, processing, logistics, or operational risk. It simply indicates that projected supply exceeds projected industrial demand under a specific methodology.

The distinction between a headline surplus and functional fragility is useful:

- Market size: relatively small compared with bulk metals

- Supply concentration: high, with major reliance on a few regions

- Recycling role: important secondary supply source

- Sensitivity to investor flows: high

- Price behaviour: often volatile due to thin liquidity and concentrated supply

However, traders often react not to the absolute size of a surplus, but to whether that surplus seems durable. In concentrated metals markets, confidence can disappear quickly if one supply region underperforms, stock movements become less transparent, or investor demand returns faster than expected.

Why the parallel nickel surplus forecast matters

The same market review also points to a nickel market surplus of around 20,000 metric tons this year, rising to 55,000 metric tons in 2027. That does not make nickel a direct proxy for palladium, but it does show a broader producer view that several metals markets are experiencing supply growth that is outpacing some demand segments.

The comparison adds value for three reasons:

- It suggests surplus conditions are not unique to palladium.

- It highlights a wider cyclical backdrop of producer caution and uneven demand absorption.

- It reinforces the role of geography, especially because the nickel outlook is highly dependent on Indonesian nickel risk.

Still, caution is needed. Palladium and nickel have different liquidity, end markets, substitution pathways, and pricing behaviour. Therefore, the nickel reference is context, not a forecasting shortcut.

What are the biggest risks to the 2026 and 2027 palladium forecasts?

No palladium model should be treated as certain. In a market this concentrated, small changes can have large effects. For that reason, understanding broader commodity price impacts can improve how investors frame producer guidance.

Supply-side risks

- Deeper-than-expected grade deterioration

- Delays in ramp-up projects

- Processing interruptions

- Logistics bottlenecks

- Political or sanctions-related complications affecting trade flows

Demand-side risks

- Faster automotive recovery

- Stronger investment demand

- More aggressive substitution away from palladium

- Recycling swings linked to scrap availability

Market-structure risks

- Inventory drawdowns that mask tightness

- Opaque stock movements

- Thin liquidity amplifying price volatility beyond fundamentals

What should a robust palladium market model include?

For analysts building a serious framework around the Norilsk Nickel palladium surplus narrative, a simple supply-minus-demand chart is not enough.

A stronger model should track:

- Primary supply by country

- Ore grade trends and mining sequence effects

- Ramp-up assumptions for new deposits

- Secondary supply from recycling

- Industrial demand by end-use segment

- Investment demand scenarios

- Inventory and stock movement assumptions

- Substitution with platinum

- Price elasticity and autocatalyst loadings

For source triangulation, it is sensible to compare producer market reviews with automotive production data, customs statistics, industry associations, and independent PGM datasets. That does not remove uncertainty, but it reduces the risk of relying on one perspective.

Norilsk Nickel palladium surplus FAQ

What is the projected palladium surplus for 2026?

The projected surplus is 0.3 million ounces, before including investment demand and stock changes.

What is the projected palladium surplus for 2027?

The projected surplus is 0.2 million ounces, based on supply exceeding demand excluding investment.

Is palladium demand falling?

Not on these numbers. Demand excluding investment is forecast to increase from 9.1 million ounces in 2026 to 9.3 million ounces in 2027.

Why can a surplus still coexist with a balanced market?

Because investor buying and stock movements can absorb excess physical supply.

What is driving Russian palladium output recovery?

A recovery from low-grade mining areas and incremental contribution from the Chernogorskoye ramp-up are key factors.

How important is investment demand?

Very important. An estimated 0.3 million ounces of investment demand in 2026 could offset the full projected surplus.

The clearest takeaway from the 2026 to 2027 palladium outlook

The projected surplus is real, but it is also narrow. Supply growth, recycling behaviour, Russian output recovery, investment absorption, and autocatalyst demand all matter more than the word surplus on its own.

The most useful interpretation is not palladium glut. It is a fragile balance with surplus tendencies. Ultimately, the Norilsk Nickel palladium surplus story is less about an overwhelming oversupply and more about how thin cushions can still shape price behaviour.

This article is for informational purposes only and should not be treated as financial advice. Commodity markets are volatile, forecasts can change quickly, and scenario analysis involves uncertainty rather than certainty.

Could The Next Discovery Shift The Market?

Discovery Alert’s proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts that help investors spot actionable opportunities before broader market sentiment shifts. See how major discoveries have historically driven exceptional returns on the Discovery Alert discoveries page and start a 14-day free trial at the Discovery Alert home page.