June 12, 2026

The Quiet Transformation Happening Inside One of Europe's Largest Aluminium Companies

The global aluminium industry is undergoing a structural shift that extends well beyond commodity price cycles. Decades of reliance on energy-intensive primary smelting are giving way to a more complex, hybrid model where recycled material, renewable energy procurement, and low-carbon certification are becoming genuine sources of competitive advantage. Against this backdrop, the Norsk Hydro Q1 results in aluminium and recycling for 2026 offer a revealing window into how an integrated producer navigates simultaneous headwinds and tailwinds across multiple business segments.

Understanding what these results actually signal requires looking past the headline numbers. On the surface, a 9% year-on-year decline in adjusted EBITDA and a 26% fall in net income suggest a company under pressure. However, the underlying mechanics tell a different story — one where operational discipline, favourable upstream pricing, and strategic positioning in recycled aluminium are quietly building a more durable earnings base.

When big ASX news breaks, our subscribers know first

Decoding the Financial Performance: What the Numbers Actually Reveal

Headline Metrics and the Divergence Worth Noting

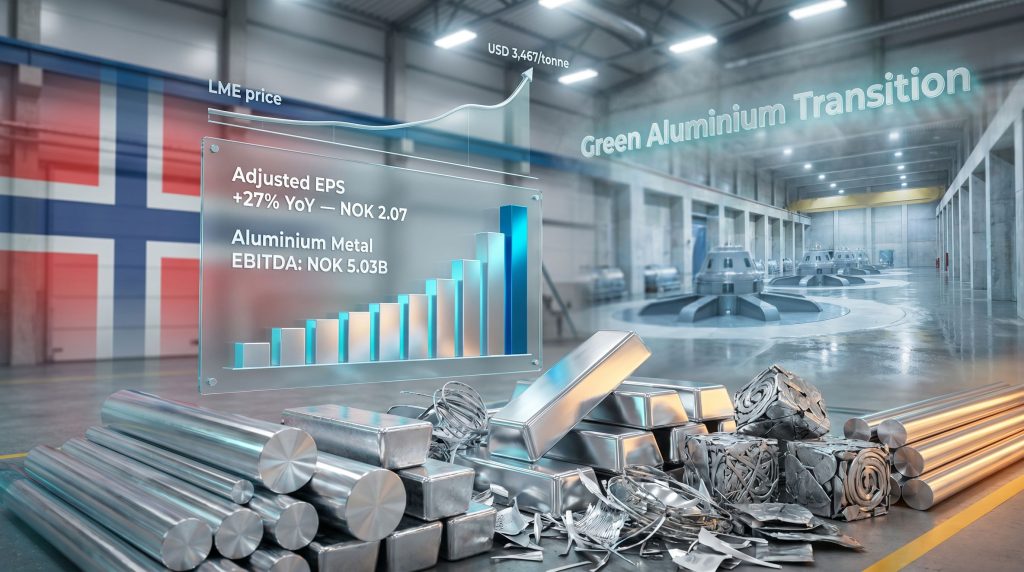

The financial summary for Q1 2026 presents an apparent contradiction that rewards closer examination.

| Metric | Q1 2026 | Q1 2025 | Change |

|---|---|---|---|

| Adjusted EBITDA | NOK 8.67B (USD 928.88M) | NOK 9.5B (USD 1.02B) | Down 9% YoY |

| Net Income | NOK 4.34B (USD 465.18M) | NOK 5.86B (USD 628M) | Down 26% YoY |

| Adjusted EPS | NOK 2.07 (USD 0.22) | NOK 1.63 (USD 0.17) | Up 27% YoY |

| Revenue | NOK 50.39B | ~NOK 57B (est.) | Down ~11.7% YoY |

| Adjusted RoaCE | 10.1% | N/A | N/A |

| Free Cash Flow | Negative NOK 4B | N/A | Working capital build |

The 26% decline in net income was driven by derivative losses and one-off items rather than core operational deterioration. Adjusted EPS simultaneously surged 27%, highlighting that accounting-level distortions were masking genuine underlying business strength.

The sequential improvement is equally important context. Adjusted EBITDA of NOK 8.67 billion represented a significant recovery from NOK 5.59 billion recorded in Q4 2025, with stronger metal prices and seasonal downstream recovery driving the rebound. Negative free cash flow of NOK 4 billion reflected working capital accumulation tied to elevated aluminium prices and higher sales volumes — a dynamic that signals commercial strength rather than operational deterioration.

Adjusted non-GAAP EPS of NOK 2.07 exceeded analyst consensus by approximately NOK 0.53, an outperformance driven by stronger-than-expected aluminium metal margins and recycling contributions. For investors focused on earnings quality, the EPS beat is arguably the most significant data point in the entire release.

Aluminium Metal: The Engine Behind the Quarter

Price Dynamics and the Supply Tightening Story

The primary aluminium segment delivered the standout earnings result of the quarter. Adjusted EBITDA for Aluminium Metal climbed to NOK 5.03 billion, more than doubling from NOK 2.55 billion in Q1 2025. This was not a marginal improvement driven by incremental volume growth. It was a step-change driven by a confluence of pricing, cost, and geopolitical forces converging simultaneously.

LME aluminium prices appreciated approximately 15.8% across the quarter, rising from around USD 2,995 per tonne in January to USD 3,467 per tonne by the end of March 2026. This trajectory reflected genuine supply market tightening. Global primary aluminium consumption grew 1.5% year-on-year, with demand outside China expanding at a slightly faster pace of 1.7%. Furthermore, this demand backdrop, while supportive, would not typically generate price movements of this magnitude in isolation.

The accelerant was geopolitical disruption. Supply constraints linked to the Iran conflict compressed global availability and supported elevated price floors. European billet premiums surged as Middle East supply disruptions reduced regional metal availability, creating a regional scarcity premium on top of the already elevated LME benchmark. Consequently, total primary aluminium production reached 5,034 kilotonnes (kmt), representing a 2.7% year-on-year increase.

Norwegian smelter capacity reactivation offset production curtailments linked to Middle East supply disruptions — a logistically complex balancing act that management executed without disrupting supply continuity. In addition, for context on where Hydro fits within the broader competitive landscape, it remains one of the major aluminium producers operating at scale across the full value chain.

The key earnings drivers across the segment can be summarised as:

- Higher all-in metal prices reflecting global supply tightening

- Lower carbon costs and energy input costs

- Higher CO₂ compensation receipts from European carbon market mechanisms

- Positive currency effects, partially offset by Norwegian krone strength against the USD

- Reduced alumina input costs flowing through from upstream

The Hidden Significance of CO₂ Compensation Receipts

One factor that receives limited mainstream attention but materially influenced segment earnings was the increase in CO₂ compensation receipts. Under the European Union's Emissions Trading System (EU ETS), energy-intensive industries including aluminium smelting can receive indirect cost compensation to offset the carbon cost passed through by electricity generators.

Higher carbon prices and favourable compensation calculations during the quarter contributed to earnings in ways that are structurally underappreciated by generalist investors. This mechanism means that rising European carbon prices — often seen as a pure cost headwind for industrial producers — can paradoxically support aluminium smelter profitability when compensation structures are correctly calibrated. The broader mining decarbonisation benefits increasingly extend to pricing and market positioning advantages as well.

Recycling Performance: A Tale of Two Continents

North America Leads, Europe Lags

Norsk Hydro's recycling operations delivered their strongest quarterly results since 2023 — a performance that was geographically bifurcated in ways that reveal important structural dynamics within the global recycled aluminium market.

| Region | Margin Trend | Primary Driver |

|---|---|---|

| North America | Improving | Widening scrap-to-primary price spread; seasonal demand recovery |

| Europe | Under pressure | Weak downstream demand; tight scrap availability; lagging scrap prices |

In North America, the critical metric was the spread between scrap input costs and primary aluminium prices. When this spread widens, recyclers benefit because they can acquire scrap at relatively lower costs while selling recycled metal at prices benchmarked closer to elevated primary aluminium levels. During Q1 2026, this spread widened meaningfully, combined with seasonal demand recovery to produce expanded margins.

European recycling presented a contrasting picture. Scrap prices lagged behind rising LME aluminium prices, compressing margins for recyclers who had locked in or were exposed to elevated scrap acquisition costs. Weak downstream demand across European construction and manufacturing sectors reduced the volume of recycled material that could be absorbed at margin-accretive pricing.

However, an important compensating dynamic emerged. Supply disruptions from the Middle East conflict tightened metal availability in Europe, pushing billet premiums higher. These elevated premiums partially offset margin compression from the scrap-primary spread, preventing a more severe earnings deterioration in European recycling operations.

EU aluminium scrap exports remained strong during the quarter, with Asian buyers continuing to dominate as the primary destination. This sustained export demand provides an important earnings floor for European recycling operations even when domestic downstream consumption weakens.

Low-Carbon Recycled Aluminium Gaining Commercial Traction

Beyond the quarterly margin dynamics, two commercial developments signal a more significant structural trend. Vode Lighting adopted Hydro CIRCAL low-carbon recycled aluminium for product manufacturing, while a letter of intent was signed with Nemak for low-carbon casting solutions.

These partnerships represent an emerging commercial reality: verified low-carbon aluminium supply chains are transitioning from a compliance-driven specification to a genuine purchasing criterion for industrial manufacturers. For instance, the broader shift is also visible in initiatives such as the aluminium recycling joint venture emerging across the industry, reflecting how recycled content and verified sustainability credentials are now central to commercial strategy rather than peripheral.

Companies seeking to reduce their Scope 3 emissions and meet increasingly stringent supply chain sustainability requirements are creating real demand for certified recycled aluminium content with quantified low-carbon credentials. For Hydro, building these commercial relationships now positions the recycling business to command premium pricing as this demand segment matures. The dynamics of low-carbon metals pricing are evolving rapidly, and early commercial positioning matters significantly.

Segment-by-Segment Weakness: Alumina, Energy, and Extrusions

Bauxite and Alumina: Volume Up, Value Compressed

Alunorte alumina production improved year-on-year through yield gains and improved equipment availability — a genuine operational achievement. The problem was that this volume improvement collided with softer alumina commodity prices and currency headwinds that overwhelmed the financial benefit of higher throughput.

Lower raw material costs provided a partial buffer but were insufficient to neutralise the pricing pressure. The segment maintained operational stability, which matters for upstream supply reliability, but the financial contribution was muted. This pattern reflects a recurring challenge in vertically integrated aluminium producers: upstream operational improvements can be rendered economically irrelevant by commodity pricing cycles that move faster than production optimisation initiatives.

Energy: Scheduled Maintenance Creates Temporary Headwind

Hydro's hydropower operations reported weaker Q1 2026 results driven by scheduled maintenance at generating facilities. This reduced generation volumes during the quarter and partially offset gains recorded in aluminium and recycling segments. Critically, this is a predictable, temporary headwind rather than a structural challenge. The Norwegian krone's appreciation against the US dollar compounded the earnings impact by reducing the NOK value of USD-denominated energy revenues.

Extrusions: Margin Discipline Compensates for Volume Softness

The extrusions segment recorded a modest but meaningful improvement in profitability.

- Adjusted EBITDA rose to NOK 1.3 billion from NOK 1.17 billion in Q1 2025

- North American margins strengthened, providing the primary earnings uplift

- Lower fixed labour, production, and energy costs supported margin expansion

- Recycling efficiency gains within the segment contributed to profitability

Demand trends remained mixed across geographies:

- Europe: Broadly flat year-on-year but improving sequentially, with early signals of recovery in automotive, particularly electric vehicle applications

- North America: Down approximately 4% year-on-year, with subdued activity across most segments and only stable demand in electrical applications

The early signs of EV-related automotive recovery in Europe represent a potentially significant medium-term demand catalyst. Aluminium extrusions are a critical material in electric vehicle battery housings, structural frames, and thermal management systems. As EV production volumes scale across European manufacturing, extrusion-grade aluminium demand should benefit disproportionately relative to conventional automotive applications.

The Green Aluminium Strategy: Renewable Energy and HalZero

Securing Long-Term Power at Competitive Pricing

Norsk Hydro secured approximately 14 TWh of long-term renewable energy supply through three contracts announced during and immediately following the quarter. The strategy of securing renewable power for aluminium production through long-dated agreements is increasingly common across the industry, reflecting how energy sourcing has become central to both cost management and sustainability credentials.

| Contract | Volume | Period | Price Area |

|---|---|---|---|

| Alpiq (signed March 2026) | 0.22 TWh annually | 2031–2038 | NO3 |

| Statkraft Agreement 1 (finalised April 2026) | 0.88 TWh annually | 2029–2038 | NO2 |

| Statkraft Agreement 2 (finalised April 2026) | 0.44 TWh annually | 2031–2038 | NO3 |

Long-term power purchase agreements serve multiple strategic functions simultaneously. They de-risk power cost exposure for Norwegian smelting operations, provide budget certainty for long-term capital allocation decisions, and underpin the green aluminium credentials that are increasingly important for premium commercial relationships. The decade-long contract durations signal confidence in the durability of both Norwegian hydropower supply and the economic case for low-carbon aluminium production.

HalZero: The Long-Term Technological Bet

The commissioning of the HalZero test facility represents one of the most technically significant milestones in Norsk Hydro's strategic roadmap. HalZero is a next-generation aluminium production technology designed to eliminate carbon emissions from the primary smelting process entirely. Conventional aluminium smelting relies on carbon anodes that are consumed during electrolysis, releasing CO₂ as a process byproduct.

Technologies that eliminate this carbon release could fundamentally alter the emissions profile of primary aluminium production. The test facility is designed to conduct controlled experimental testing in a safe environment, meaning this remains an early-stage development initiative. Commercial deployment timelines are not yet confirmed, but the commissioning milestone indicates the technology has advanced beyond theoretical modelling into physical experimentation.

The next major ASX story will hit our subscribers first

Competitive Positioning and the Road to Q2 2026

Cost Reduction Targets and Forward Guidance

Hydro is targeting a USD 20 to 30 per tonne reduction in hot metal costs by 2030, with approximately one-third of targeted reductions expected to have been achieved by end of 2025. This cost trajectory matters because it provides a structural earnings tailwind that operates independently of commodity price cycles. The Norsk Hydro Q1 results in aluminium and recycling demonstrate that operational cost discipline, rather than price-taking alone, is increasingly defining competitive differentiation.

For Q2 2026, the segment outlook breaks down as follows:

- Extrusions: Higher volumes anticipated, stable margins expected

- Recycling: Continued strong margins projected, supported by sustained scrap-to-primary price spreads

- Aluminium Metal: Dependent on LME price trajectory and geopolitical supply chain developments

- Alumina: Pricing recovery remains uncertain; volume stability expected to continue

Key macro risk factors to monitor include Norwegian krone appreciation against the USD as a persistent earnings headwind, the pace of downstream demand recovery in European construction and automotive, and geopolitical developments in the Middle East that continue to influence both supply availability and regional metal premiums. Overall, the Norsk Hydro Q1 results in aluminium and recycling reinforce a picture of a business navigating complex cross-currents with considerable operational steadiness — even as headline metrics obscure the underlying strategic progress being made.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Past performance of any company, commodity price, or financial metric is not indicative of future results. Readers should conduct independent due diligence and consult qualified financial advisers before making investment decisions. Forward-looking statements and projections referenced in this article are subject to material risks and uncertainties.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex geological data into actionable investment insights for both short-term traders and long-term investors — explore historic discoveries and their returns to understand the opportunity. Begin your 14-day free trial at Discovery Alert today and position yourself ahead of the market.