August 4, 2026

Norway Transforms European Rare Earth Landscape with Massive Resource Upgrade

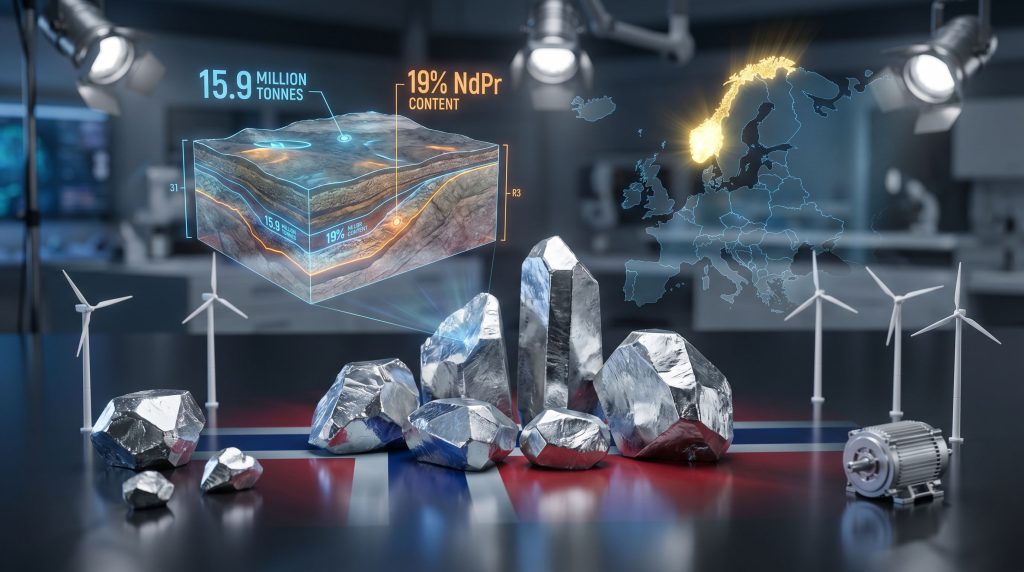

The recent discovery that Norway's largest rare earth deposit contains 15.9 million metric tonnes of rare earth oxides has fundamentally altered Europe's strategic mineral outlook. This extraordinary resource upgrade represents an 81% increase from previous estimates, positioning the Fen complex as a cornerstone of European supply security initiatives. Furthermore, this development addresses critical minerals energy security concerns that have intensified across the continent.

When big ASX news breaks, our subscribers know first

What Makes Norway's Fen Deposit Europe's Most Critical Rare Earth Discovery?

Resource Scale Analysis – 15.9 Million Tonnes Transforms European Supply Security

Norway's largest rare earth deposit represents a fundamental shift in European mineral autonomy potential. The Fen complex now contains 15.9 million metric tons of rare earth oxide across indicated and inferred resource categories. This marks an extraordinary 81% increase from the previous 2024 estimate of approximately 8.8 million tonnes.

This massive resource upgrade positions the Norwegian deposit among the world's most significant undeveloped rare earth assets. The scale transformation occurred following comprehensive geological reassessment. Consequently, initial exploration programs substantially underestimated the deposit's true extent.

| Resource Classification | Volume (Million Tonnes REO) | Confidence Level |

|---|---|---|

| Indicated Resources | 11.2 | High geological confidence |

| Inferred Resources | 4.7 | Moderate geological confidence |

| Total Resources | 15.9 | Combined assessment |

The distinction between indicated and inferred resources carries important implications for development timelines. Indicated resources demonstrate sufficient geological evidence to estimate grade and quantity with reasonable confidence. However, inferred resources require additional drilling and analysis before achieving bankable feasibility status.

From a continental perspective, this resource scale addresses a critical gap in European supply security infrastructure. Unlike other regions where rare earth deposits remain fragmented across multiple smaller projects, the Fen complex concentrates substantial resources within a single, cohesive geological formation. This consolidation supports the broader mining industry evolution towards large-scale operations.

Strategic Mineral Composition – Why 19% NdPr Content Changes Everything

The strategic value of Norway's largest rare earth deposit extends beyond total tonnage to its exceptional mineral composition. Approximately 19% of the rare earth oxides consist of neodymium and praseodymium (NdPr). These represent the two elements driving permanent magnet technology across critical industrial applications.

This NdPr concentration translates to roughly 3.02 million tonnes of these strategic elements within the total 15.9 million tonne resource. Such substantial NdPr content positions the Fen deposit to address specific technological bottlenecks. In addition, this differs from simply contributing generic rare earth supply.

Key Applications of NdPr Elements:

• Electric Vehicle Motors: Permanent magnet synchronous motors require high-strength NdPr magnets for optimal efficiency and power density

• Wind Turbine Generators: Direct-drive wind systems depend on NdPr permanent magnets to eliminate gearbox complexity and maintenance requirements

• Consumer Electronics: Smartphones, laptops, and audio equipment utilise miniaturised NdPr magnets for speaker and motor applications

• Defense Technologies: Military navigation systems, radar equipment, and precision guidance systems require consistent NdPr magnet performance

The 19% NdPr grade significantly exceeds many global competitors. In contrast, these critical elements often represent 10-15% of total rare earth content elsewhere. This composition advantage reduces downstream processing complexity and enhances project economics through higher-value mineral concentration.

Processing facilities designed for the Fen deposit can optimise separation techniques specifically for NdPr extraction. Therefore, they may achieve higher recovery rates compared to mixed rare earth operations. The relatively clean elemental profile minimises contamination challenges that complicate separation processes in deposits with complex heavy rare earth distributions.

Geological Formation Advantages – Ancient Carbonatite Complex Benefits

The Fen complex represents an ancient carbonatite intrusion, a rare geological formation that concentrates rare earth elements through specific magmatic processes. Carbonatite-hosted deposits typically offer several advantages over other rare earth geological environments.

Geological Characteristics:

• Uniform Mineralisation: Carbonatite intrusions often display consistent grade distribution, reducing mining selectivity requirements

• Simple Mineralogy: Fewer gangue minerals compared to sedimentary or placer deposits simplify beneficiation processes

• Structural Integrity: Competent rock formations support efficient underground mining methods with enhanced safety profiles

• Predictable Geometry: Intrusive bodies follow established geological patterns, enabling accurate resource modelling and mine planning

The ancient nature of the Fen carbonatite suggests extensive weathering and alteration processes. These may have concentrated rare earth minerals near surface zones. This geological evolution potentially reduces strip ratios and enables cost-effective extraction methods during initial development phases.

How Does Government Intervention Accelerate Critical Mineral Development?

Planning Authority Transfer – From Local to National Strategic Control

The Norwegian government's decision to assume planning authority for the Fen project represents unprecedented intervention in critical mineral development. This transfer occurred following a formal request from local authorities who acknowledged the project's complexity exceeded municipal planning capabilities.

Government officials cited two primary justifications for intervention: land-use dispute prevention and the need to balance competing national interests. These concerns transcend local decision-making frameworks. This escalation reflects recognition that strategic mineral infrastructure requires governance structures aligned with continental supply security objectives.

The planning authority transfer mechanism demonstrates how European governments are adapting regulatory frameworks. Furthermore, they address critical mineral development urgency. Traditional municipal planning processes, designed for conventional development projects, prove inadequate when projects carry national security implications.

The Fen field could be of major significance for Telemark, Norway and Europe's supply security and competitiveness – Prime Minister Jonas Gahr Stoere

This governmental intervention establishes precedent for how European nations may approach future critical mineral projects. Moreover, it shows how they address situations where local planning processes conflict with strategic resource development timelines. This approach aligns with modern mining permitting insights that recognise the need for streamlined approval processes.

Intervention Timeline:

- April 2026: Government assumes planning authority

- 2026-2027: National-level environmental and technical assessments

- 2028-2029: Infrastructure planning and permitting

- 2030-2031: Construction and development phases

- Late 2031: Targeted production commencement

Land-Use Conflict Resolution – Balancing Environmental and Economic Priorities

European infrastructure development faces systematic opposition from environmental and agricultural constituencies. This creates delays that threaten strategic project timelines. The Norwegian government explicitly acknowledged this challenge, noting that infrastructure projects including wind farms have encountered significant resistance that delays development across the region.

The Fen project's land-use considerations involve multiple competing interests:

Environmental Concerns:

• Biodiversity impact assessments for sensitive ecosystems

• Water resource protection and contamination prevention

• Air quality maintenance during construction and operation

• Long-term landscape restoration and closure planning

Agricultural Interests:

• Productive farmland preservation and compensation frameworks

• Rural community economic impact mitigation

• Traditional land-use pattern maintenance

• Food security considerations in agricultural regions

Economic Development Priorities:

• Regional employment creation and skills development

• Infrastructure investment and modernisation

• Export revenue generation and national competitiveness

• Supply chain independence and strategic autonomy

The government's intervention strategy suggests a framework for balancing these competing priorities. Consequently, this occurs through centralised decision-making rather than local consensus-building processes. These historically generate extended delays.

Infrastructure Development Framework – Supporting Large-Scale Mining Operations

Large-scale rare earth extraction requires coordinated infrastructure investment across multiple systems. These include transportation networks, electrical supply, water management, processing facilities, and workforce development programmes. The production target of 800 tonnes NdPr annually by 2032 necessitates substantial supporting infrastructure.

Critical Infrastructure Requirements:

• Transportation Corridors: Heavy-haul rail or road systems for ore transport and equipment delivery

• Electrical Supply: High-voltage connections for energy-intensive processing operations

• Water Infrastructure: Supply systems for processing and tailings management

• Processing Facilities: Beneficiation, separation, and refining infrastructure

• Waste Management: Tailings storage and environmental protection systems

The government's planning authority enables integrated infrastructure development. This differs from fragmented municipal approvals. This coordination reduces project risk and potentially accelerates development timelines through streamlined permitting processes.

Processing rare earth ores requires sophisticated separation chemistry and substantial electrical input. The 800-tonne annual NdPr target suggests processing facilities capable of handling approximately 4,200 tonnes of rare earth concentrate annually. This assumes typical beneficiation and separation efficiencies.

What Are the Production Timeline and Economic Projections?

Phase 1 Development Schedule – Late 2031 Production Launch

The Fen project timeline targets production commencement in late 2031. This represents approximately 5.5 years from the government's planning intervention announcement. This development schedule reflects the complex technical and regulatory requirements for establishing new rare earth production capacity in Europe.

Development Phase Breakdown:

| Phase | Timeline | Key Activities |

|---|---|---|

| Planning & Permitting | 2026-2027 | Environmental assessments, regulatory approvals |

| Engineering & Design | 2027-2028 | Processing facility design, infrastructure planning |

| Construction | 2029-2031 | Mine development, facility construction |

| Commissioning | 2031 | Equipment testing, production ramp-up |

| Commercial Production | Late 2031+ | Full-scale operations |

The late 2031 production target assumes successful navigation of European environmental regulations. These typically require comprehensive impact assessments for mining projects. Unlike jurisdictions with established mining frameworks, Norway must develop regulatory pathways specific to rare earth extraction and processing.

Critical Success Factors:

• Permitting Efficiency: Streamlined approvals under national planning authority

• Technology Selection: Proven processing methods adapted to Fen ore characteristics

• Workforce Development: Training programmes for specialised rare earth processing skills

• Market Preparation: Offtake agreements with European industrial consumers

The 5.5-year development timeline compares favourably with global rare earth projects. These often require 7-10 years from discovery to production. Government intervention and established infrastructure in southern Norway contribute to this accelerated schedule.

Output Capacity Modelling – 800 Tonnes NdPr by 2032 Targeting 5% EU Demand

The production target of 800 tonnes NdPr annually by 2032 represents approximately 5% of European Union demand for these critical elements. This output level positions the Fen project as a meaningful but not dominant supplier to European industrial consumers.

Based on the 5% EU demand metric, total European NdPr consumption approximates 16,000 tonnes annually. This demand scale reflects the rapid expansion of electric vehicle production, wind energy installations, and industrial automation across the continent.

Production Capacity Analysis:

• Processing Volume: 800 tonnes NdPr requires processing approximately 4,200 tonnes REO annually

• Mining Scale: Extracting sufficient ore to produce 4,200 tonnes concentrate suggests 200,000-300,000 tonnes raw ore annually

• Recovery Efficiency: Target assumes 85-90% processing efficiency from ore to final NdPr products

• Capacity Utilisation: Initial production may operate below full capacity during ramp-up phases

The 5% market share strategy offers several advantages:

- Market Access: Significant supply contribution without triggering competitive responses

- Price Stability: Insufficient volume to disrupt global rare earth pricing dynamics

- Customer Diversification: Multiple industrial offtakers reduce concentration risk

- Expansion Flexibility: Proven demand base supports future capacity increases

European industrial consumers currently source NdPr primarily from Chinese suppliers. This creates supply chain vulnerability during geopolitical tensions or trade disputes. The Fen project's 5% contribution provides meaningful diversification whilst maintaining supplier relationships across multiple regions.

Long-Term Scaling Potential – Path Beyond Initial Production

The 15.9 million tonne resource base supports substantial production expansion beyond the initial 800-tonne NdPr annual target. Long-term scaling scenarios depend on market demand evolution, technological advancement, and additional exploration success.

Scaling Scenarios:

• Conservative Growth: Doubling to 1,600 tonnes NdPr (10% EU demand) by 2035

• Moderate Expansion: Tripling to 2,400 tonnes NdPr (15% EU demand) by 2040

• Aggressive Development: Six-fold increase to 4,800 tonnes NdPr (30% EU demand) by 2045

Each scaling increment requires proportional infrastructure investment and market development. The conservative growth scenario utilises existing processing facilities more intensively. However, aggressive development demands entirely new production lines and expanded mining operations.

Resource Longevity Analysis:

At 800 tonnes NdPr annually (4,200 tonnes REO), the 15.9 million tonne resource supports approximately 3,800 years of production. This extraordinary longevity enables multiple expansion phases without resource depletion concerns. Consequently, this contrasts sharply with projects where reserves constrain long-term planning.

The scaling pathway flexibility provides strategic optionality as European demand evolves. Electric vehicle adoption rates, wind energy deployment, and industrial automation expansion will determine optimal production levels throughout the project lifecycle.

Why Does This Discovery Matter for European Mineral Independence?

China Dependency Reduction Strategy – Breaking the 90% Import Reliance

European rare earth consumption currently depends on Chinese suppliers for approximately 90% of total requirements. This creates strategic vulnerability in critical technology supply chains. This concentration risk became apparent during trade tensions and export restriction threats. These demonstrated how quickly geopolitical factors can disrupt industrial material flows.

Norway's largest rare earth deposit offers the first meaningful opportunity to establish domestic European production capacity. While the initial 5% EU demand contribution appears modest, it represents the foundation for broader supply chain diversification initiatives across the continent. This aligns with broader defence critical minerals strategies being developed.

Dependency Reduction Metrics:

| Timeline | Fen Production Share | Chinese Import Dependency | Strategic Impact |

|---|---|---|---|

| 2026 | 0% | 90% | Current vulnerability |

| 2032 | 5% | 85% | Initial diversification |

| 2035 | 10% | 80% | Meaningful reduction |

| 2040+ | 15-30% | 70-75% | Strategic resilience |

The dependency reduction strategy extends beyond simple supply substitution to technology transfer and industrial capability development. European rare earth processing expertise will develop alongside production capacity. Therefore, this creates intellectual property and technical capabilities that support broader mineral independence objectives.

Chinese market dominance stems from integrated supply chains encompassing mining, processing, and downstream manufacturing. European diversification requires similar integration. Consequently, this positions the Fen project as a catalyst for broader industrial ecosystem development.

Supply Chain Resilience Building – Domestic Source for Critical Technologies

European technological competitiveness depends on reliable access to rare earth elements across multiple industrial sectors. Supply chain resilience requires geographic diversification, supplier redundancy, and domestic production capacity. These insulate critical industries from external disruption.

Critical Technology Dependencies:

• Automotive Sector: Electric vehicle motor magnets, hybrid powertrains, battery systems

• Renewable Energy: Wind turbine generators, solar panel components, energy storage

• Aerospace & Defence: Navigation systems, radar technology, precision instruments

• Electronics Manufacturing: Consumer devices, industrial automation, telecommunications

The Fen deposit's 19% NdPr concentration directly addresses the most critical bottleneck elements in these technology supply chains. Unlike generic rare earth supply that requires complex processing to isolate specific elements, the deposit's composition targets high-value applications. Furthermore, supply security carries premium pricing in these markets.

Supply chain resilience building involves multiple strategic layers:

- Primary Production: Domestic mining capacity reduces import dependency

- Processing Infrastructure: European separation and refining capabilities

- Technology Integration: Downstream manufacturing using domestic materials

- Strategic Reserves: Government stockpiles for emergency supply continuity

- Research & Development: Innovation in processing efficiency and application technology

The Norwegian project catalyses investment across all resilience layers. In addition, it attracts capital and expertise that strengthens European rare earth industrial capabilities beyond single-project scope. This development supports critical raw materials facility initiatives across Europe.

Geopolitical Risk Mitigation – Securing Strategic Material Access

Rare earth elements qualify as strategic materials due to their criticality in defence applications and emerging technologies. Substitution proves technically challenging or economically prohibitive in these applications. Geopolitical risk mitigation requires supply sources aligned with European security interests and trade relationships.

Geopolitical Risk Categories:

• Export Restrictions: Unilateral limitations on critical material exports during diplomatic tensions

• Trade War Escalation: Rare earths as leverage tools in broader economic conflicts

• Supply Route Disruption: Transportation and logistics vulnerabilities affecting material flows

• Price Manipulation: Artificial supply constraints to disadvantage competitor economies

• Technology Transfer Requirements: Forced partnerships to access critical materials

Norway's NATO membership and European integration provide geopolitical alignment. This insulates the Fen project from many risk categories affecting non-aligned suppliers. This political stability enhances supply security beyond purely commercial considerations.

The strategic material access framework extends to allied nations through technology sharing and joint procurement initiatives. European rare earth production supports broader Western technological independence. Moreover, it reduces collective vulnerability to supply weaponisation.

Defence applications require particular supply security given their national security implications. The Fen project's NdPr output can serve European defence contractors directly. Consequently, this eliminates foreign dependency for sensitive military applications.

How Does Fen Compare to Global Rare Earth Resources?

European Context – Fen vs Other Continental Deposits

Norway's largest rare earth deposit dominates European rare earth resources by substantial margins. This establishes the Fen complex as the continent's premier strategic mineral asset. Comparative analysis reveals the project's exceptional scale and quality advantages over alternative European sources.

Major European Rare Earth Deposits Comparison:

| Location | Resource Size (Mt REO) | Key Minerals | Development Status | Strategic Advantages |

|---|---|---|---|---|

| Norway (Fen) | 15.9 | NdPr (19%) | Government Planning | Largest scale, high NdPr |

| Sweden (Per Geijer) | 2.2 | Mixed REE | Early exploration | Railway infrastructure |

| Greenland (Kvanefjeld) | 11.0 | Mixed REE | Suspended | Environmental concerns |

| Finland (Sokli) | 1.8 | LREE dominant | Exploration | Phosphate co-product |

The Fen deposit's 15.9 million tonne resource exceeds the combined total of other significant European prospects. This provides unmatched scale for continental supply security initiatives. This resource concentration enables economies of scale in processing infrastructure and operational efficiency.

Sweden's Per Geijer deposit, whilst substantially smaller, benefits from existing railway infrastructure and established mining expertise. However, the 2.2 million tonne resource constrains long-term production potential compared to Fen's multi-decade supply capacity.

Greenland's Kvanefjeld deposit faces indefinite suspension due to environmental and political concerns. This highlights the importance of stable regulatory environments for rare earth development. The 11.0 million tonne resource remains inaccessible pending resolution of governance and environmental challenges.

Quality Metrics Analysis:

• NdPr Concentration: Fen's 19% grade substantially exceeds typical European deposits (8-12%)

• Processing Complexity: Carbonatite mineralogy simplifies separation compared to complex ore types

• Environmental Profile: Established mining jurisdiction with clear regulatory pathways

• Infrastructure Access: Southern Norway location with existing transportation and utilities

Global Ranking Analysis – Where Norway Fits in Worldwide Resources

The Fen complex ranks among the world's largest undeveloped rare earth deposits. This positions Norway as a significant player in global rare earth resource distributions. International comparison reveals the project's strategic importance extends beyond European supply security. Furthermore, it influences worldwide market dynamics.

Global Major Rare Earth Deposits:

| Country | Deposit | Resource Size (Mt REO) | Development Status | Global Market Share |

|---|---|---|---|---|

| China | Bayan Obo | 48.0 | Producing | Dominant supplier |

| USA | Mountain Pass | 18.0 | Producing | Strategic alternative |

| Norway | Fen | 15.9 | Development | Emerging major |

| Australia | Mount Weld | 8.8 | Producing | Regional supplier |

| Greenland | Kvanefjeld | 11.0 | Suspended | Potential future |

| Vietnam | Dong Pao | 5.0 | Exploration | Southeast Asia |

The Fen deposit's 15.9 million tonne resource positions Norway as the third-largest rare earth resource holder globally. This trails only China's dominant Bayan Obo complex and the United States' Mountain Pass facility. This ranking establishes Norway as a future major supplier capable of influencing global market dynamics.

Strategic Positioning Advantages:

- Western Alliance: NATO membership and democratic governance structure

- Regulatory Stability: Established mining laws and environmental frameworks

- Infrastructure Access: Developed transportation and utility networks

- Technical Expertise: Advanced geological knowledge and mining capabilities

- Market Access: European industrial customers and global shipping routes

Unlike many large global deposits located in politically unstable regions or countries with complex regulatory environments, the Fen project benefits from Norway's institutional stability and international relationships. According to Reuters, this government takeover demonstrates Norway's commitment to developing strategic mineral resources.

Quality Metrics Comparison – Grade and Mineral Distribution Advantages

Rare earth deposit quality involves multiple technical factors beyond total resource tonnage. These include elemental grade, mineral composition, processing complexity, and extraction requirements. The Fen complex demonstrates exceptional quality metrics that enhance its strategic value and economic viability.

Quality Assessment Framework:

• Total Rare Earth Oxide (TREO) Grade: Concentration of all rare earth elements

• NdPr Percentage: Proportion of high-value neodymium and praseodymium

• Heavy vs. Light REE: Distribution between element categories

• Mineralogy: Host rock characteristics affecting processing requirements

• Gangue Minerals: Non-valuable materials requiring separation

The Fen deposit's 19% NdPr content significantly exceeds global averages of 12-15%. This provides higher-value mineral concentration that improves project economics. This NdPr grade compares favourably with producing mines and advanced development projects worldwide.

Processing Complexity Comparison:

| Deposit Type | Processing Requirements | Fen Complex Advantages |

|---|---|---|

| Carbonatite (Fen) | Conventional flotation/acid leach | Simple mineralogy, low gangue |

| Ion Clay | In-situ leaching | Higher grade, less environmental impact |

| Placer/Beach Sands | Physical separation | More concentrated, reliable supply |

| Alkaline Intrusive | Complex acid treatment | Fewer radioactive elements |

The carbonatite geological formation provides processing advantages through simpler mineralogy and reduced gangue mineral content. These characteristics lower processing costs and improve recovery efficiency. Consequently, this compares favourably to complex ore types requiring sophisticated separation techniques.

Environmental considerations also favour the Fen deposit's quality profile. Carbonatite ores typically contain lower radioactive element concentrations compared to some major global deposits. Therefore, this reduces regulatory complexity and waste management requirements.

The next major ASX story will hit our subscribers first

What Are the Technology Applications Driving Demand?

Electric Vehicle Market Growth – Permanent Magnet Requirements

The global electric vehicle transition drives unprecedented demand for NdPr permanent magnets. Each electric vehicle requires approximately 1-2 kilograms of rare earth elements for motor and powertrain applications. European EV production targets create substantial domestic demand for the Fen project's output.

European EV Market Projections:

| Year | EV Production Target | NdPr Demand (tonnes) | Fen Supply Contribution |

|---|---|---|---|

| 2030 | 6 million units | 9,000 | Pre-production |

| 2032 | 10 million units | 15,000 | 800 tonnes (5.3%) |

| 2035 | 15 million units | 22,500 | 1,200 tonnes (5.3%) |

| 2040 | 20 million units | 30,000 | 2,000+ tonnes (6.7%) |

Electric vehicle motors utilise permanent magnet synchronous motors (PMSMs) that deliver superior power density and efficiency. These outperform alternative motor technologies. These performance advantages make rare earth permanent magnets technically essential rather than simply preferred for high-performance EVs.

Motor Technology Comparison:

• PMSM (NdPr Magnets): Highest efficiency (95%+), compact size, optimal torque

• Induction Motors: Lower efficiency (90-93%), larger size, no rare earths required

• Switched Reluctance: Lowest efficiency (88-92%), noise concerns, rare earth-free

Premium electric vehicle brands prioritise PMSM technology for performance advantages. This creates inelastic demand for NdPr elements. While alternative motor technologies exist, consumer expectations for range, acceleration, and efficiency favour rare earth-dependent solutions.

The European automotive industry's commitment to domestic supply chains enhances demand security for Norwegian production. Major manufacturers including BMW, Mercedes-Benz, and Volkswagen Group prioritise supplier diversification. Furthermore, they emphasise regional sourcing to reduce Chinese dependency.

Wind Energy Expansion – Turbine Generator Dependencies

European wind energy deployment relies heavily on direct-drive generators that utilise NdPr permanent magnets. These eliminate gearbox complexity and reduce maintenance requirements. Offshore wind farms particularly favour this technology due to accessibility constraints and reliability priorities.

Wind Turbine Technology Analysis:

| Generator Type | Rare Earth Content | European Market Share | Technical Advantages |

|---|---|---|---|

| Direct-Drive PMSG | 150-200 kg NdPr per MW | 60%+ | High reliability, low maintenance |

| Geared PMSG | 30-50 kg NdPr per MW | 25% | Moderate rare earth usage |

| Doubly-Fed Induction | 0 kg rare earths | 15% | Lower cost, higher maintenance |

European wind capacity targets require substantial NdPr supply for optimal technology deployment. The European Union's REPowerEU initiative targets 1,236 GW of wind capacity by 2030. Furthermore, offshore installations drive permanent magnet generator demand.

Wind Energy NdPr Demand Projections:

• 2030 Target: 200 GW additional capacity = 30,000-40,000 tonnes NdPr requirement

• Offshore Focus: Higher permanent magnet adoption rates due to maintenance considerations

• Technology Trends: Larger turbines with higher rare earth intensity per unit

• Supply Security: European manufacturers seeking domestic rare earth sources

Offshore wind development particularly drives permanent magnet demand due to maintenance accessibility challenges. Gearbox failures in offshore environments require expensive vessel operations and extended downtime. Therefore, this makes direct-drive generators economically superior despite higher rare earth content.

The Fen project's production timeline aligns with European wind energy expansion phases. This provides domestic supply security during critical deployment periods. Norwegian rare earth output supports both domestic wind development and export opportunities to other European markets.

Defence and Electronics Sectors – Strategic Technology Applications

Defence applications represent the most strategic rare earth demand category. These require secure supply chains and technical performance standards that prioritise capability over cost considerations. European defence contractors increasingly specify domestic or allied sources for critical materials.

Defence Rare Earth Applications:

• Radar Systems: Permanent magnets in phased array antennas and rotating mechanisms

• Guidance Systems: Precision actuators and sensor components requiring stable magnetic fields

• Communication Equipment: Miniaturised speakers and microphone assemblies

• Surveillance Technology: Gyroscopes and stabilisation systems for platforms and sensors

• Electronic Warfare: Signal processing equipment and countermeasure systems

Military specifications often require 20-30 year service life with minimal maintenance. This favours NdPr permanent magnets over electromagnetic alternatives that consume power and require active cooling. These performance requirements create inelastic demand regardless of price fluctuations.

Electronics Industry Demand Categories:

| Application | Annual EU Demand (tonnes) | Growth Rate | Substitution Risk |

|---|---|---|---|

| Smartphones/Tablets | 2,500 | 5% | Low – miniaturisation requires |

| Audio Systems | 1,800 | 3% | Medium – performance trade-offs |

| Industrial Automation | 3,200 | 8% | Low – precision requirements |

| Medical Devices | 800 | 12% | Very Low – safety critical |

Consumer electronics demand growth stems from device proliferation and performance enhancement rather than simple replacement demand. Each smartphone contains approximately 10-15 small permanent magnets for speakers, cameras, and haptic feedback systems.

The electronics sector's rare earth demand exhibits high price elasticity compared to automotive and defence applications. However, substitution timeline constraints create medium-term inelastic demand during supply disruptions. This market segment often benefits from insights shared in Modern Diplomacy analysis of European strategic materials policy.

What Challenges Could Impact Development Success?

Environmental Assessment Requirements – Balancing Conservation with Extraction

Norwegian environmental regulations require comprehensive impact assessments for large-scale mining projects. This creates potential timeline and cost pressures for the Fen development. Environmental challenges extend beyond compliance to encompass biodiversity protection, water resource management, and long-term landscape restoration.

Critical Environmental Assessment Areas:

• Biodiversity Impact: Flora and fauna population studies, habitat connectivity analysis

• Water Resource Protection: Groundwater contamination prevention, surface water quality maintenance

• Air Quality Management: Dust control, processing emissions, transportation impacts

• Waste Management: Tailings facility design, long-term stability, closure planning

• Landscape Integration: Visual impact mitigation, tourism industry considerations

The Telemark region where Fen is located contains sensitive ecological areas that require careful impact mitigation. Environmental groups have historically opposed infrastructure development in Norway. Consequently, this creates organised stakeholder opposition to large industrial projects.

Environmental Timeline Risks:

- Extended Assessment Periods: Seasonal wildlife studies may require 2-3 year observation cycles

- Regulatory Appeals: Environmental organisations possess legal standing to challenge permit decisions

- Mitigation Requirements: Biodiversity offset programmes and habitat restoration mandates

- Monitoring Obligations: Long-term environmental performance tracking and reporting

Water resource protection presents particular technical challenges for rare earth processing. This requires substantial freshwater input and generates liquid waste streams requiring treatment. The processing target of 800 tonnes NdPr annually suggests water usage of 2-4 million cubic metres annually.

Climate change adaptation requirements add complexity to environmental planning. Processing facilities and tailings management systems must account for changing precipitation patterns. Furthermore, they must consider extreme weather events over multi-decade operational periods.

Infrastructure Investment Needs – Transportation and Processing Facilities

The Fen project requires substantial infrastructure investment beyond mine development. This includes specialised processing facilities, transportation upgrades, electrical supply enhancement, and workforce accommodation. Infrastructure gaps could delay production timelines or increase capital requirements significantly.

Infrastructure Investment Categories:

| Category | Investment Requirement | Technical Specifications | Timeline Criticality |

|---|---|---|---|

| Processing Plant | $200-300 million | Flotation, leaching, separation | Critical path – 3 years |

| Transportation | $50-100 million | Heavy-haul rail/road upgrade | Pre-production essential |

| Electrical Supply | $30-50 million | High-voltage transmission | Processing plant dependency |

| Water Infrastructure | $20-40 million | Supply, treatment, tailings | Environmental compliance |

Processing Technology Selection Challenges:

• Proven vs. Advanced: Established technology offers reliability; new processes promise efficiency

• Environmental Performance: Closed-loop systems require higher capital but reduce permit risk

• Scalability Design: Phase 1 facilities must accommodate future expansion requirements

• Automation Level: Higher automation reduces labour but increases technical complexity

Southern Norway's existing infrastructure provides advantages compared to greenfield locations. However, rare earth processing requires specialised capabilities not present in conventional mining regions. Processing plant design must integrate multiple complex chemical operations. These include beneficiation, acid leaching, solvent extraction, and final product purification.

Critical Infrastructure Timeline Dependencies:

- Electrical Grid Connection: 18-24 months for high-voltage transmission construction

- Transportation Upgrades: 12-18 months for road/rail capacity improvements

- Processing Plant Construction: 30-36 months for complex chemical facilities

- Environmental Systems: 24-30 months for tailings and water treatment infrastructure

The government's planning authority assumption potentially accelerates infrastructure permitting. However, physical construction timelines remain constrained by technical complexity and specialised equipment procurement.

Market Price Volatility – Rare Earth Commodity Cycle Risks

Rare earth markets exhibit extreme price volatility due to supply concentration, demand fluctuations, and geopolitical factors. The Fen project's economic viability depends on sustained pricing levels that justify substantial infrastructure investment and operational costs.

Price Volatility Drivers:

• Supply Concentration: Chinese production dominance enables price manipulation

• Demand Cyclicality: Technology sector downturns reduce rare earth consumption

• Geopolitical Events: Trade disputes and export restrictions cause price spikes

• Speculative Activity: Financial markets amplify price movements beyond fundamentals

• Inventory Cycles: Industrial stockpiling and destocking create demand volatility

Historical rare earth price analysis demonstrates extreme volatility patterns. NdPr prices ranged from $40-180 per kilogram between 2010-2022. This represents 350% price variation that challenges project economics and financing decisions.

Risk Mitigation Strategies:

- **

Looking to Capitalise on Strategic European Rare Earth Opportunities?

Norway's massive rare earth discovery demonstrates how government intervention can accelerate critical mineral development, whilst the 15.9 million tonne Fen deposit positions Europe for greater supply independence from Chinese dominance. Discover why major mineral discoveries like this can generate substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional investment outcomes powered by our proprietary Discovery IQ model.