May 12, 2026

The Coming Rutile Famine: Why the Titanium Feedstock Market Is Heading Toward a Supply Crisis

Most commodity markets experience price cycles driven by shifts in demand, currency fluctuations, or policy changes. Natural rutile is different. The forces building beneath the surface of the global titanium feedstock market are geological in nature, which means they operate on timescales that cannot be reversed by a policy announcement or a capital expenditure decision made today. Understanding that distinction is the starting point for understanding why the Fortuna Metals rutile discovery in Malawi matters far beyond its current stage of development.

The mineral sands sector rarely captures mainstream investment attention. It lacks the narrative excitement of lithium or the geopolitical weight of rare earths. Yet the case for natural rutile as a structurally constrained critical material may be stronger than almost any other feedstock in the current market environment. Supply is measurably contracting, critical minerals demand is expanding across multiple industrial verticals, and the pipeline of replacement projects capable of filling the widening gap is, by most credible assessments, dangerously thin.

When big ASX news breaks, our subscribers know first

What Natural Rutile Actually Is, and Why It Commands a Premium

Rutile is a naturally occurring titanium dioxide mineral, typically containing between 93% and 96% TiO₂ by weight. That compositional richness is what separates it commercially from ilmenite, the far more abundant titanium-bearing mineral that dominates global supply. Ilmenite typically contains between 45% and 65% TiO₂ and requires substantial downstream processing, including upgrading into synthetic rutile or titanium slag, before it becomes suitable for high-specification applications.

Natural rutile bypasses most of that processing burden. It feeds directly into the chloride-route pigment manufacturing process, which produces the highest-purity titanium dioxide for use in coatings, plastics, and paper. It is also the preferred feedstock for producing aerospace-grade titanium metal via the Kroll process, where impurity thresholds are stringent and feedstock quality directly determines final metal quality.

The paradox of the rutile market is that despite these clear advantages, approximately 95% of global titanium feedstock supply still originates from ilmenite rather than natural rutile. This is not because ilmenite is preferred. It is because large-scale, high-grade natural rutile deposits are geologically uncommon. The mineralogical conditions required to concentrate rutile into economically exploitable deposits at meaningful scale are rare enough that the global inventory of known, developable resources is measured in a handful of projects rather than dozens.

The Deteriorating Supply Picture: By the Numbers

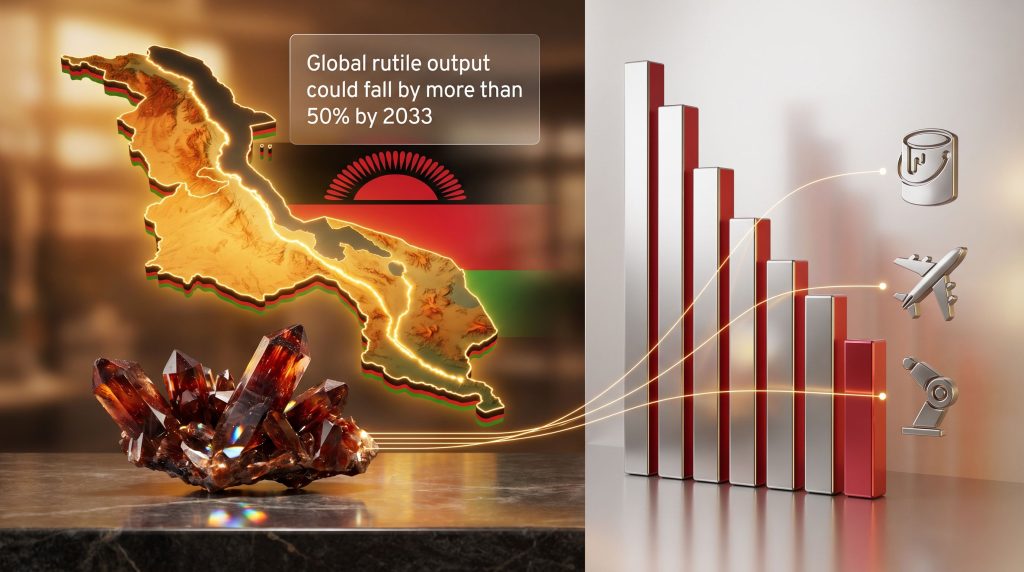

The two most significant natural rutile producing operations currently active are Sierra Rutile in Sierra Leone and Base Resources' Kwale project in Kenya. Both are approaching the end of their productive mine lives. The absence of credible, construction-ready replacement projects at comparable scale has led independent modelling to project that global rutile output could decline by more than 50% by 2033 absent the entry of new large-scale production.

| Supply Factor | Detail |

|---|---|

| Current major producers | Sierra Rutile (Sierra Leone), Kwale (Kenya, Base Resources) |

| Mine life status | Both operations approaching end-of-life depletion |

| Projected supply contraction | More than 50% potential decline by 2033 |

| Nature of the deficit | Structural, not cyclical |

| Replacement pipeline | No comparable projects in late-stage development |

The projected 50%-plus decline in global rutile supply by 2033 is not a demand-side phenomenon. It reflects geological scarcity and the absence of credible replacement projects in the development pipeline. For investors, this distinction matters enormously: structural deficits are sustained, not self-correcting.

What makes this particularly significant from an investment perspective is the long lead time between exploration discovery and production. Furthermore, even a mineral sands project with exceptional grade continuity and favourable logistics typically requires five to ten years from first discovery through feasibility, permitting, construction, and commissioning. Projects entering resource definition today are not realistically bringing supply to market before the mid-2030s at the earliest.

Malawi's Geological Position as an Emerging Rutile Province

Central Malawi has emerged as one of the few geological settings globally where large-scale, shallow, laterite-hosted rutile mineralisation is present at meaningful grade. The Lilongwe Plain is a mineralised corridor extending approximately 70 kilometres across southern Malawi, characterised by a rutile-graphite bearing geological unit that has been mapped by Malawi's Geological Department extending southward from established deposit boundaries.

The laterite-hosted style of mineralisation found here is particularly significant from a development economics perspective. Unlike hard-rock deposits, laterite-hosted mineral sands systems can be drilled rapidly using aircore and hand-auger methods, assessed at comparatively low cost per hole, and ultimately mined using straightforward open-cut techniques. This avoids the blasting requirements that elevate capital and operating costs in harder geology, making the low-cost extraction profile a structural development advantage that is rarely emphasised in mainstream mining coverage.

The Kasiya Benchmark and What It Reveals About the Region

Sovereign Metals' Kasiya deposit sits at the northern end of this mineralised corridor and is currently classified as the world's largest undeveloped natural rutile resource. Kasiya's economic profile is defined by high-grade core zones with surface-only mineralisation of two to four metres flanking the central system, and critically, by the presence of graphite as a co-product that substantially amplifies the project's revenue per tonne mined.

In the context of Kasiya's financial modelling, graphite co-product credits effectively double the project's rutile-equivalent grade. This is not a trivial observation. It transforms what might otherwise be a single-commodity rutile project into a dual-revenue system where each tonne of ore processed generates income from two separately marketable products. Sovereign Metals' project currently trades at approximately 14.5% of its project NPV following Pre-Feasibility Study completion, a data point that establishes a market-derived benchmark for how advanced mineral sands projects in this jurisdiction are valued.

What the Fortuna Metals Rutile Discovery at Mkanda Has Found

The Fortuna Metals rutile discovery in Malawi is centred on the Mkanda and Kampini tenements, a combined land position of 658 km² spanning the Lilongwe Plain directly south of Kasiya. The geological unit hosting Kasiya's mineralisation has been mapped extending into Fortuna's ground by Malawi's Geological Department, providing the interpretive framework for exploration targeting. The mineral exploration importance of this regional geological context cannot be overstated when evaluating the project's potential scale.

The reconnaissance drilling program completed to date has covered approximately 180 km² using 544 drill holes, a wide-spaced methodology designed to establish the lateral extent and grade character of the mineralised system before committing to the tighter spacing required for JORC Resource estimation.

Decoding the Grade Results

The headline grade outcomes from initial programs include:

- Peak aircore drilling result of 2.32% rutile

- Peak in-situ surface sampling result of 2.21% rutile

- Continuous mineralisation intercepts of 1.66% rutile over 10 metres and 1.32% rutile over a separate 10-metre interval

- Average QEMSCAN-confirmed grade of 1.11% rutile across soil sampling

- Rutile comprising approximately 80% of the total titanium mineral assemblage

- 9 out of 10 drill holes returning rutile grades above the 0.5% threshold

- Mineralisation persisting beyond the base of drilling in the majority of holes tested

That final point carries particular weight in mineral sands evaluation. End-of-hole mineralisation means the system has not been closed at depth. In this geological setting, it signals that the economically important saprock zone, which represents the deepest practical limit of low-cost open-cut extraction, has not yet been fully characterised. The saprock boundary is where the weathered laterite and saprolite profile transitions into harder, less-altered rock. Reaching it defines the vertical extent of a mining operation and is critical to calculating contained resource volume.

How Mkanda's Characteristics Compare to Kasiya

| Geological Characteristic | Mkanda (Fortuna Metals) | Kasiya (Sovereign Metals) |

|---|---|---|

| Deposit style | Shallow laterite-hosted rutile-graphite | Shallow laterite-hosted rutile-graphite |

| Peak rutile grade | 2.32% | Comparable high-grade core zones |

| Flanking mineralisation thickness | 2-4 metres | Similar flanking profile |

| Depth continuity | Confirmed beyond drill base | Confirmed to saprock boundary |

| Graphite co-product potential | Under assessment, 115 holes submitted | Confirmed, doubles rutile-equivalent grade |

| Nacala rail corridor proximity | Yes | Yes |

The structural parallels between the two systems are not coincidental. They reflect shared geological origins within the same Lilongwe Plain mineralised unit. What remains to be quantified at Mkanda is whether the graphite content mirrors Kasiya's, and what the metallurgical recovery profile looks like under processing conditions. Those are the two key uncertainties that Phase 2 work is designed to address.

The Layered Rock Profile: Why the Saprock Zone Changes the Economics

Understanding why end-of-hole mineralisation matters requires a brief explanation of how laterite weathering profiles are structured. From the surface downward, the sequence is:

- Laterite cap — highly weathered, iron-rich surface zone

- Saprolite — intermediate weathering zone, soft and friable

- Saprock — transition zone between weathered and fresh rock, partially altered

- Fresh rock — unweathered parent material, significantly harder and more expensive to excavate

In mineral sands projects hosted within laterite profiles, the economically mineable material is almost entirely confined to the laterite through saprock sequence. Once excavation reaches fresh rock, the cost profile of extraction rises sharply due to the need for blasting and harder rock handling. Defining where the saprock boundary sits therefore defines the actual volume of material available for low-cost mining.

At Mkanda, mineralisation persisting to end-of-hole means Phase 2 drilling, targeting penetration to 20 metres and beyond, is needed to locate that boundary and confirm whether the grade persists through the saprolite into the saprock zone. If it does, the system's contained resource expands substantially.

The next major ASX story will hit our subscribers first

Malawi's Regulatory Landscape: Risk Resolved, Not Avoided

In late 2025, Malawi's government introduced an executive order restricting the export of unprocessed raw ore, a policy designed to encourage in-country beneficiation and value addition. The order created a period of uncertainty for early-stage explorers who were uncertain whether bulk sample shipments, metallurgical test parcels, or concentrate exports would fall within its scope.

In February 2026, formal clarification was received confirming that operations built around beneficiation and concentrate production fall outside the restriction. This distinction is technically important. Mineral sands operations do not export unprocessed ore. They process run-of-mine material through gravity and other separation circuits to produce heavy mineral concentrate, which is then shipped to downstream processors. That production model was explicitly confirmed as outside the order's scope.

The February 2026 regulatory clarification established a consistent policy framework for mineral sands concentrate producers in Malawi. Operations that incorporate in-country processing steps — which is standard practice for rutile and graphite projects at this scale — are not captured by the unprocessed ore export restriction. This removes a previously perceived sovereign risk overhang that had weighed on market sentiment toward Malawi-based explorers.

This outcome aligns with the framework already governing Sovereign Metals' Kasiya operation, meaning Malawi now has an established and internally consistent regulatory precedent for how mineral sands concentrate producers are treated under the 2025 executive order.

The Nacala Corridor: A Decisive Logistics Advantage

For any mineral sands project, transport to port is a primary determinant of operating cost. The Nacala Development Corridor is a multimodal infrastructure route connecting landlocked Malawi to the Mozambican port of Nacala on the Indian Ocean. Both Mkanda and Kasiya sit in proximity to this corridor, a geographic advantage that significantly reduces concentrate haulage costs relative to projects in more isolated African locations.

Nacala is a deep-water port capable of handling bulk export shipments at scale. For a future Mkanda operation, access to this infrastructure would allow concentrate to reach major global pigment and titanium metal producers in Asia, Europe, and North America via established shipping routes. In addition, this shared logistics advantage reinforces the broader investment case for the Lilongwe Plain as a coherent mineral province rather than a collection of isolated projects.

The Metallurgical Dimension: Why Processing Recovery Determines Project Value

One of the least-discussed but most consequential variables in mineral sands project evaluation is metallurgical recovery. A project with peak grades of 2.32% rutile is not necessarily more valuable than one grading 1.5% rutile if the higher-grade system delivers poor separation efficiency and significant rutile loss to tailings. Recovery rates from processing circuits directly determine the volume of saleable product per tonne mined, and therefore the revenue per unit of capital deployed.

Fortuna's bulk sampling and metallurgical testwork program is currently underway in Johannesburg, which serves as the primary hub for mineral sands processing expertise in the Southern African region. The programme is designed to establish representative recovery rates across the main mineralised zones, determine concentrate quality specifications, and provide the processing circuit design inputs needed for resource economic modelling.

In parallel, 115 drill holes have been submitted for graphite analysis. If the graphite content at Mkanda proves comparable to Kasiya's, the project's rutile-equivalent grade would effectively double, replicating the economic amplification that made Kasiya's Pre-Feasibility Study financials compelling to the market. Consequently, these results represent one of the most anticipated technical milestones in the current programme.

Team Appointments That Signal a Phase Transition

Two recent technical appointments reflect a deliberate organisational shift from reconnaissance-phase exploration toward resource definition:

- David Bougourd, a former processing specialist from Iluka Resources, one of the world's leading mineral sands producers. Processing expertise is the critical capability gap for projects transitioning from exploration to production planning, and Iluka's operational experience spans multiple commodity cycles.

- Richard Stockwell, a geologist with direct involvement in the Kasiya project. His geological interpretation of the Lilongwe Plain mineralised system is precisely the knowledge set needed to guide drill targeting, resource boundary definition, and deposit characterisation at Mkanda.

Together, these appointments signal that Fortuna is no longer operating as a pure exploration company. The institutional knowledge brought by these individuals positions the team to execute on resource definition with a level of regional and technical authority that would otherwise take years to accumulate.

Three Demand Vectors Reshaping the Rutile Outlook

The supply contraction story would be significant enough on its own. However, what amplifies it is the simultaneous expansion of demand across three distinct end-use markets, each operating on different growth trajectories and driven by different underlying forces.

| Demand Segment | Growth Driver | Rutile Requirement |

|---|---|---|

| TiO₂ pigment | Infrastructure expansion in China and India | High-grade chloride-route feedstock |

| Aerospace and defence | Next-generation aircraft platforms, defence procurement | Aerospace-grade titanium metal |

| Humanoid robotics | Adoption curve acceleration, Chinese manufacturing data | High-purity titanium alloy inputs |

Titanium dioxide pigment remains the dominant end-use market for rutile by volume. Chloride-route pigment producers specifically require high-grade feedstock because the chemistry of the process is intolerant of iron and other impurities that lower-grade ilmenite carries. Continued construction activity and infrastructure development across India and China sustains baseline demand for this application.

Aerospace and defence represent the highest unit-value demand channel. Modern commercial aircraft platforms incorporate significantly more titanium than their predecessors, driven by fuel efficiency mandates that reward the metal's strength-to-weight ratio. Defence procurement provides a demand floor that is largely non-cyclical, as it is driven by strategic capability requirements rather than commercial economic conditions.

Humanoid robotics is the emerging long-horizon demand vector that most conventional supply forecasts have not yet incorporated. Titanium's combination of fatigue resistance, biocompatibility, and weight efficiency makes it the material of choice for joints, actuators, and structural components in robotic systems. Furthermore, energy transition minerals and advanced material supply chains are increasingly interlinked as industrial policy globally shifts toward securing domestic or allied-nation feedstock sources.

How the Market Values Projects on the Path to Resource Definition

Mineral sands companies are not typically valued on earnings multiples during the exploration and resource definition phases. The relevant valuation framework is NPV-based, and the market's willingness to price a company at a meaningful fraction of project NPV is gated by the completion of key technical milestones. Understanding the feasibility study stages that lie ahead helps contextualise how valuation re-ratings occur as technical risk is progressively removed.

| Milestone | Risk Category Removed | Market Re-Rating Potential |

|---|---|---|

| Maiden JORC Resource | Geological uncertainty | Yes, quantifies the asset |

| Metallurgical testwork results | Processing recovery risk | Yes, confirms commercial viability |

| Graphite co-product confirmation | Revenue diversification | Potentially significant |

| Pre-Feasibility Study | Economic viability uncertainty | Major, enables NPV-based valuation |

| Regulatory clarity (achieved Feb 2026) | Sovereign and policy risk | Partial, removes overhang |

The sector benchmark provided by Sovereign Metals is instructive. Following completion of its Pre-Feasibility Study, the Kasiya project has traded at approximately 14.5% of its project NPV on the market. This is not a prediction of where Fortuna will trade; it is a reference point for understanding how the market prices risk reduction in this specific commodity and jurisdiction context. For a project to reach PFS-equivalent valuation, it first needs a maiden JORC Resource, which requires the Phase 2 drilling and testwork programme now underway.

In mineral sands, the most significant valuation re-rating events typically occur between maiden resource announcement and PFS completion. At maiden resource, the project transitions from a geological concept to a quantified asset. At PFS, it becomes an economic model with definable cash flow assumptions. Each step removes a layer of technical and commercial uncertainty that the market had previously been discounting.

The cut-off grade economics applied during resource estimation will also play a critical role in determining what proportion of drilled material ultimately qualifies for inclusion. For laterite-hosted mineral sands systems, selecting an appropriate cut-off threshold is particularly consequential given the wide range of grade outcomes across different parts of the deposit footprint.

Frequently Asked Questions: Fortuna Metals Rutile Discovery in Malawi

What is the Mkanda project and where is it located?

Mkanda is a mineral sands exploration project in Mchinji district, Malawi, forming part of a 658 km² combined tenement package with the adjacent Kampini project. It sits within the same geological unit that hosts the Kasiya deposit on the Lilongwe Plain, a region that has emerged as a globally significant rutile-graphite province. For further background, Fortuna's Malawi project page provides additional detail on the tenement's scope and geological setting.

What grades has Mkanda returned so far?

Reconnaissance programmes have returned peak rutile grades of 2.32% from aircore drilling and 2.21% from in-situ surface sampling. Continuous mineralisation intervals of 1.66% and 1.32% rutile over 10-metre intercepts have also been confirmed. The average QEMSCAN-confirmed grade across soil sampling was 1.11%, with rutile comprising roughly 80% of the total titanium mineral assemblage.

Why does mineralisation persisting to end-of-hole matter?

When drill holes terminate in mineralised material rather than in barren rock, it indicates the system has not been closed at depth. In the context of laterite-hosted deposits, this typically means the saprock zone — which represents the practical lower limit of economic open-cut mining — has not yet been reached. Defining that boundary through deeper Phase 2 drilling is essential to calculating total resource volume.

What is the significance of graphite at Mkanda?

At Kasiya, graphite co-product credits effectively double the project's rutile-equivalent grade by generating a second revenue stream from the same mined material. If Mkanda's graphite analysis, currently underway across 115 submitted drill holes, returns comparable results, the project's economics would be similarly enhanced without any change to the rutile grades already confirmed.

Has Malawi's ore export policy affected the project?

No. Malawi's late-2025 executive order restricting unprocessed ore exports was formally clarified in February 2026 to exclude operations involving beneficiation and concentrate production. This is the intended development model for Mkanda and mirrors the framework under which Sovereign Metals' Kasiya project already operates.

What is the timeline for a maiden JORC Resource?

Phase 2 aircore drilling is scheduled to commence in May 2026, targeting infill of the highest-grade zones and deeper penetration to confirm saprock boundary grades. Metallurgical testwork and graphite assay results will feed into the resource model alongside expanded spatial drilling data. The company held approximately A$7.4 million in cash following a late-2025 capital placement, funding this phase of work. An independent analysis of Fortuna Metals' discovery has highlighted the significance of the drilling results in establishing the scale of this system.

The Broader Significance of the Lilongwe Plain

The Fortuna Metals rutile discovery in Malawi is best understood not as a single project story but as evidence of a mineral belt whose full dimensions have not yet been mapped. The Lilongwe Plain hosts Kasiya at its northern extent and Mkanda at its southern reach, across a combined geological footprint that exceeds anything represented by either project individually.

If Phase 2 results confirm grade continuity to saprock depths and graphite analysis replicates Kasiya's co-product profile, Malawi's position in the global critical minerals supply landscape would be materially different from its current characterisation as a single-deposit province. A geological belt capable of hosting two independently significant rutile-graphite resources in close proximity, both served by the same rail and port infrastructure, represents a fundamentally different category of mineral endowment.

That possibility remains speculative at this stage. What is not speculative is the direction of travel: an accelerating global supply deficit, an expanding demand base, and a team executing a disciplined technical programme at the threshold of resource definition. The Fortuna Metals rutile discovery in Malawi is a story still being written, but the chapters that matter most are now being drafted in real time.

This article is intended for informational purposes only and does not constitute financial advice. Readers should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions. Forward-looking statements, supply projections, and valuation references involve assumptions that may not be realised. Mineral exploration involves significant uncertainty, and past exploration results are not a guarantee of future resource outcomes.

Want to Be First When the Next Major Mineral Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex data across more than 30 commodities into clear, actionable insights for both short-term traders and long-term investors — explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the broader market.