June 5, 2026

Nuclear Expansion Strategies Reshape Global Uranium Markets

Accelerating nuclear power deployment across major economies creates profound shifts in uranium procurement strategies, as nations seek energy independence through diversified supply chains. The intersection of climate policy commitments and energy security concerns drives unprecedented demand for nuclear fuel supplies, fundamentally altering traditional supplier relationships established over decades.

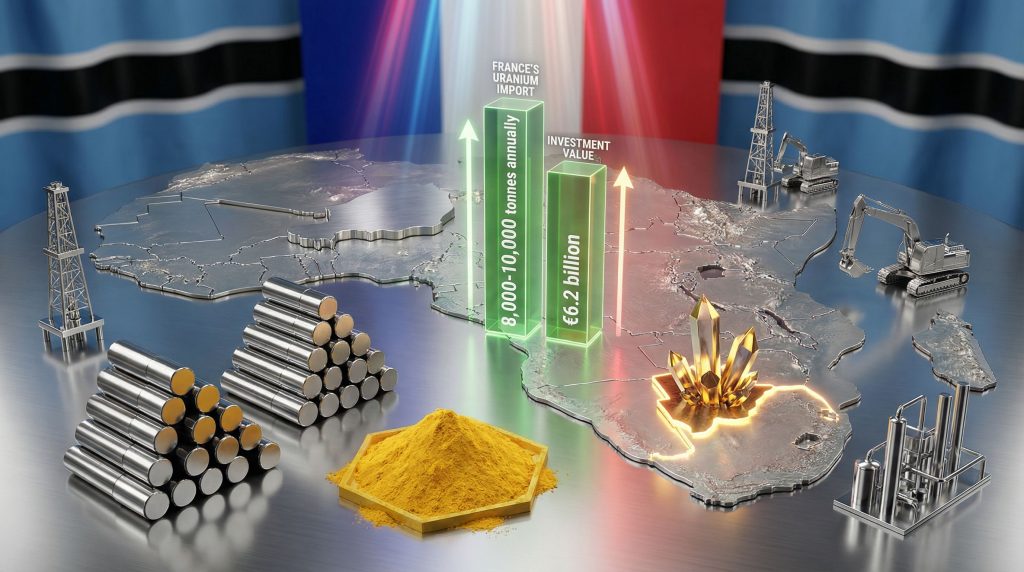

Critical minerals competition intensifies as geopolitical tensions fragment established trade networks, forcing industrial powers to reassess their resource dependencies. France Botswana uranium deals exemplify this strategic realignment, as European nations pursue alternative partnerships following supply chain disruptions across Africa's Sahel region.

When big ASX news breaks, our subscribers know first

Strategic Nuclear Fuel Diversification Accelerates

France operates 56 nuclear reactors generating approximately 70% of national electricity production, creating annual uranium requirements approaching 8,500 tonnes. This extraordinary nuclear dependency, the highest among major economies, transforms uranium procurement into a cornerstone of national energy security strategy.

The strategic imperative extends beyond immediate fuel requirements into economic sovereignty frameworks. Furthermore, French nuclear technology exports contribute over €6 billion annually to trade balances, while reactor construction expertise provides diplomatic leverage across emerging nuclear markets. Nuclear power's role in France's net-zero emissions pathway by 2050 amplifies the critical nature of secure uranium supply chains.

Reactor Fleet Characteristics:

- Generation II and III designs requiring specialised fuel assemblies

- Pressurised Water Reactor technology dominating the operational portfolio

- Multi-year fuel planning cycles demanding long-term supply agreements

- Advanced enrichment specifications for enhanced reactor efficiency

France's nuclear industry exemplifies how energy infrastructure creates structural dependencies on specific minerals, distinguishing uranium from other industrial commodities through its strategic security implications.

Sahelian Resource Nationalism Transforms Continental Mining

Niger's July 2023 military coup eliminated France's access to the SOMAIR uranium mine, where Orano held a 63.4% operational stake. This asset seizure removed approximately 1,800 tonnes from France's annual uranium supply, equivalent to 20% of total imports and sufficient to fuel 11-12 nuclear reactors.

The nationalisation reflects broader anti-colonial sentiment across Francophone Africa, where military governments increasingly challenge resource agreements negotiated under previous civilian administrations. Moreover, Niger's ruling junta framed the expropriation as correcting historical economic exploitation, stating that Orano exhibited irresponsible and illegal behaviour while France maintained hostile policies toward Niger following the coup.

| Supply Chain Disruption | Impact Assessment | Strategic Response |

|---|---|---|

| SOMAIR mine loss | 63.4% stake eliminated | Alternative sourcing required |

| Annual volume impact | 1,800 tonnes uranium | 11-12 reactor fuel supply |

| Logistics disruption | West African transport networks | Southern African route development |

| Preferential pricing loss | Decades-long agreements nullified | Market rate procurement necessary |

The military government accused foreign uranium operations of creating misery, pollution, and corruption while enriching France through below-market pricing mechanisms. This narrative gains traction across the Sahel region, where similar resource reassessment processes challenge European mining investments.

Geopolitical Risk Recalibration:

- Military governments controlling uranium-rich territories

- Anti-French sentiment spreading across former colonies

- Chinese and Russian mining companies expanding African presence

- Security deterioration constraining Sahelian operations

Consequently, understanding uranium market volatility becomes essential for investors navigating these geopolitical shifts.

Botswana Emerges as Strategic Alternative

Botswana's constitutional democracy, maintained continuously since 1966 independence, contrasts sharply with Sahelian political instability. Recent leadership transitions, including Duma Boko's election as president in late 2024, demonstrate institutional resilience attractive to long-term mining investments requiring decades-long operational commitments.

The country's mining sector expertise, developed through diamond industry leadership, provides technical foundations for uranium extraction. In addition, Botswana's economy currently depends on diamond revenues for approximately 80% of export earnings, creating strong incentives for mining diversification as global diamond markets face structural challenges.

Botswana's Strategic Advantages:

- Political stability: 58 years of constitutional governance

- Mining infrastructure: Established diamond sector capabilities

- Regulatory transparency: Clear licensing and permitting processes

- Geographic positioning: Southern African transport networks

- Economic incentives: Diversification beyond diamond dependency

Letlhakane Deposit Resource Potential

Botswana's uranium reserves, concentrated in the Letlhakane deposit within Ghanzi district, represent one of Africa's largest undeveloped uranium resources. Geological surveys estimate approximately 800,000 tonnes of uranium oxide equivalent, sufficient for multiple decades of large-scale production.

Technical Specifications:

- Shallow open-pit mining potential reducing extraction costs

- Acid heap leach processing suitable for local ore mineralogy

- Projected annual production: 1,150 tonnes uranium at full capacity

- Mine life expectancy: 18+ years under current reserve estimates

- Water management requirements in semi-arid environment

The deposit's shallow depth eliminates expensive underground mining infrastructure, while acid heap leach processing technology offers cost advantages over conventional milling operations. These characteristics position Botswana competitively against established uranium producers in Kazakhstan, Australia, and Canada.

However, uranium development timelines require substantial patience. Plans for Botswana's first commercial uranium mine have circulated since 2009, reflecting the complex regulatory, environmental, and financial requirements for nuclear fuel production facilities.

France Botswana Uranium Deals Gain Momentum

French nuclear group Orano has secured exploration licences covering approximately 15,000 square kilometres in western Botswana, signalling systematic commitment to developing alternative African uranium supplies. Senior executives, including Mining business unit head Xavier Saint Martin Tillet and Strategy Vice President Pierre Fourrier, conducted diplomatic engagement with President Duma Boko during his April 2026 Paris visit.

These meetings, organised alongside MEDEF business federation activities, demonstrate coordinated public-private partnership approaches characterising modern resource diplomacy. Furthermore, France's efforts to secure Botswana uranium represent mutual benefit frameworks addressing both French energy security requirements and Botswana's economic diversification objectives.

Exploration Licence Portfolio:

- 15,000 square kilometres licenced territory in Ghanzi district

- Multiple geological formations under systematic evaluation

- Technology transfer opportunities with local mining partners

- Environmental baseline studies supporting regulatory compliance

Botswana has actively positioned itself as a potential uranium supplier since 2021, engaging with the International Atomic Energy Agency in Vienna to develop nuclear sector capabilities. This institutional approach reflects deliberate strategy to capture value from uranium resources while building domestic technical expertise.

Implementation Timeline Challenges

Uranium mine development requires 7-10 year lead times from exploration through production, assuming favourable regulatory and environmental assessments. Botswana's uranium ambitions face several implementation hurdles despite favourable geological conditions.

Development Requirements:

- Comprehensive environmental impact assessments

- Water resource management in semi-arid regions

- Processing facility construction and waste disposal systems

- Skilled workforce development for nuclear fuel production

- Transportation infrastructure for remote mining locations

Capital investment requirements approach $1-2 billion for full-scale uranium operations, with payback periods extending 10-15 years under current market conditions. Therefore, these financial commitments require long-term supply contracts providing price stability for both producers and consumers.

Global Nuclear Renaissance Drives Uranium Demand

Nuclear power capacity must expand significantly to support climate commitments and energy security objectives across major economies. The International Energy Agency projects nuclear generation must double by 2050 to achieve net-zero emissions targets, creating structural uranium demand growth exceeding current production capacity.

Demand Growth Projections:

- Conservative scenario: 30% uranium demand increase through 2035

- Accelerated transition: 45-50% demand surge above current levels

- New reactor construction: 60+ units globally in development pipeline

- Small modular reactors: Additional deployment acceleration potential

Current global uranium production approximates 55,000 tonnes annually, insufficient to meet projected demand under most growth scenarios. Supply-demand imbalances emerge between 2028-2032 without substantial new production capacity additions, creating strategic opportunities for emerging producers like Botswana.

Nuclear Expansion Economics

Small modular reactor deployment accelerates nuclear adoption in markets previously unsuitable for large reactor installations. SMR technology requires comparable uranium enrichment specifications to conventional reactors, expanding total fuel demand without reducing per-unit consumption requirements.

Market Dynamics:

- Production capacity lags: 5-10 year mine development timelines

- Geopolitical concentration: Kazakhstan supplies 40% of global uranium

- Supply chain diversification: African production expansion necessity

- Climate policy drivers: Nuclear power essential for decarbonisation

France's uranium procurement strategy exemplifies broader European recognition that energy security requires diversified supply relationships with politically stable partners. For instance, developing effective uranium investment strategies becomes crucial as supply constraints tighten globally.

The next major ASX story will hit our subscribers first

Strategic Mining Partnership Implications

France's pivot toward Botswana uranium resources reflects systematic risk management across multiple operational dimensions. European nuclear programmes increasingly emphasise supply chain resilience over cost optimisation alone, recognising that energy security justifies premium pricing for reliable sources.

Risk Distribution Framework:

- Political risk diversification across multiple African jurisdictions

- Operational risk reduction through democratic governance partnerships

- Supply chain resilience via Southern African transport networks

- Technology transfer benefits supporting mutual development objectives

Continental Resource Realignment

France Botswana uranium deals could trigger competitive responses across African mining markets, as other European nations seek similar strategic partnerships. Chinese and Russian companies simultaneously expand African uranium investments, creating multilateral competition for mining rights and government partnerships.

Competitive Landscape Evolution:

- European nations pursuing bilateral uranium agreements

- Asian powers increasing African mining investments

- Regional cooperation frameworks for uranium development

- Technology transfer requirements for foreign investors

African governments increasingly demand higher revenue shares and local processing capabilities from international mining partnerships. This trend toward resource sovereignty creates opportunities for mutually beneficial arrangements while challenging traditional extraction-based models.

Market Psychology and Investment Dynamics

Uranium markets exhibit unique psychological characteristics distinguishing nuclear fuel from other industrial commodities. Long reactor fuel cycles create demand stability, while security considerations drive premium pricing for reliable suppliers from stable jurisdictions.

Investor Considerations:

- Strategic reserve accumulation by nuclear-dependent nations

- Long-term contract preferences reducing price volatility

- Geopolitical risk premiums in supplier evaluation

- Environmental compliance costs in mine development

France Botswana uranium deals demonstrate how resource partnerships can address both immediate supply requirements and longer-term strategic positioning. However, advances in US uranium production tech could also influence global market dynamics and competitive positioning.

Financial Structuring Considerations

Uranium mine financing requires sophisticated risk management given long development timelines and commodity price volatility. Joint venture structures between French companies and Botswana partners could distribute financial exposure while ensuring operational expertise transfer.

Capital Requirements:

- $1-2 billion full-scale mine development investment

- 10-15 year typical payback periods

- Price hedging mechanisms managing commodity volatility

- Infrastructure investment in remote mining regions

Future Market Structure Evolution

The emergence of Botswana as a significant uranium supplier could reshape global nuclear fuel markets by reducing concentration risk in traditional producing regions. Enhanced supplier diversification benefits both energy security objectives and market price stability through increased competition.

France Botswana uranium deals exemplify how resource partnerships can simultaneously serve energy security, economic development, and environmental objectives. Moreover, the Russian uranium import ban creates additional urgency for developing alternative supply sources like those emerging in Botswana.

Strategic Implications:

- Reduced geopolitical risk premiums in uranium pricing

- Enhanced investment confidence in African mining projects

- Integrated nuclear fuel supply chain development

- Templates for sustainable resource partnership models

This transformation in uranium sourcing strategies reflects broader recognition that critical mineral security requires diverse, politically stable supplier relationships. As nuclear power expansion accelerates globally, partnerships like those between France and Botswana may become essential components of energy security architecture for nuclear-dependent economies.

Consequently, monitoring the uranium mining status across various jurisdictions becomes increasingly important for understanding global supply dynamics and investment opportunities.

Investment decisions should consider the long-term nature of mining projects, regulatory risks, and commodity price volatility. This analysis provides educational content and should not be considered financial advice.

Could Uranium Supply Chain Disruptions Create New Investment Opportunities?

France's strategic shift from Niger to Botswana for uranium supplies highlights the growing importance of geopolitically stable mining jurisdictions in critical mineral markets. Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries across uranium and other strategic commodities, ensuring subscribers stay ahead of market-moving announcements as global supply chains reshape. Begin your 14-day free trial today to capture emerging opportunities in Australia's dynamic resources sector.