June 13, 2026

The global nuclear sector faces unprecedented challenges in securing reliable fuel supply chains amid shifting geopolitical dynamics and accelerating demand for advanced reactor technologies. Traditional enrichment dependencies have exposed critical vulnerabilities in national energy security frameworks, particularly as emerging reactor designs require specialised fuel compositions unavailable through conventional supply networks. Furthermore, the recent Russian uranium ban impact has intensified the need for domestic capability development, reflecting broader strategic imperatives beyond immediate energy needs.

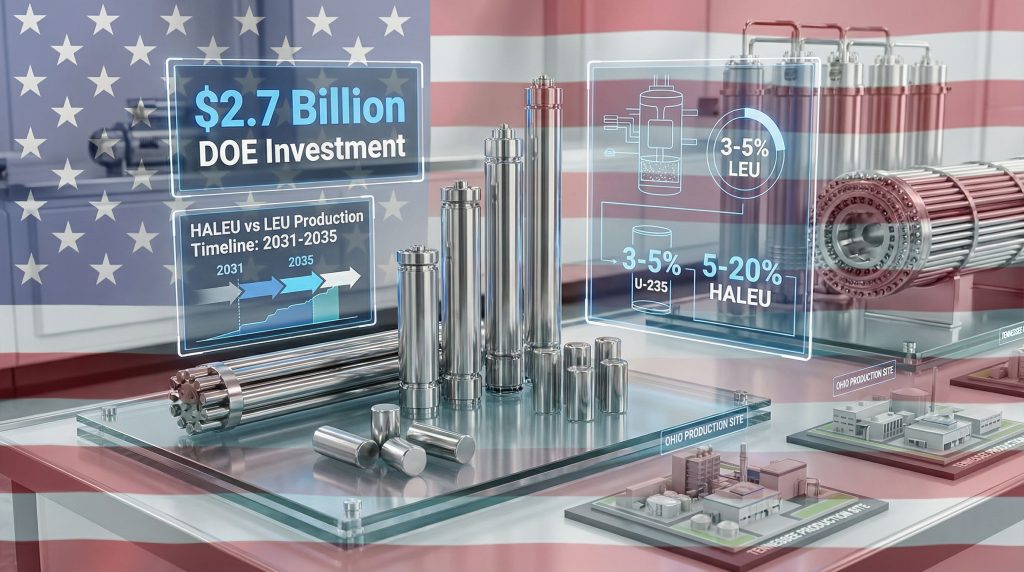

Strategic Investment Framework Transforms Nuclear Fuel Independence

The Department of Energy's comprehensive $2.7 billion allocation across multiple enrichment contractors represents a fundamental restructuring of America's nuclear fuel production capacity. The DOE awards $2.7B for HALEU and LEU enrichment initiative distributes funding across four primary recipients, each targeting different technological approaches and geographic footprints to establish redundant domestic supply chains.

Investment Distribution Analysis:

- American Centrifuge Operating: $900 million for expanding existing Ohio operations

- General Matter: $900 million for greenfield Kentucky facility development

- Orano Federal Services: $900 million for Tennessee LEU production expansion

- Global Laser Enrichment: $28 million for advanced laser-based enrichment technology

The strategic timing of these awards, announced January 6, 2026, follows initial contract selections from October 2024 where four companies were selected to split up to $2.7 billion in future high-assay low-enriched uranium enrichment contracts. This phased approach allows the DOE to validate contractor capabilities whilst maintaining competitive dynamics across different technological pathways.

Technological Diversification Strategy

Each recipient operates under distinct enrichment methodologies, creating technological redundancy that reduces single-point-of-failure risks across the domestic fuel supply ecosystem. Centrifuge-based approaches leverage mature international technology standards, while laser-based separation systems offer potential efficiency improvements and reduced energy consumption profiles.

The investment structure deliberately avoids concentration risk by distributing awards across established operators like Centrus Energy alongside emerging companies such as General Matter. This portfolio approach enables the DOE to balance immediate production requirements with longer-term technological advancement objectives, addressing critical US uranium production insights requirements.

When big ASX news breaks, our subscribers know first

HALEU Production Addresses Advanced Reactor Bottlenecks

High-assay low-enriched uranium serves as the critical enabling fuel for next-generation reactor technologies, yet the United States currently maintains zero commercial HALEU production capacity. This supply gap has constrained advanced reactor deployment timelines and created dependencies on foreign enrichment services for emerging nuclear technologies.

Fuel Specification Comparison:

| Parameter | LEU (Traditional) | HALEU (Advanced) |

|---|---|---|

| Enrichment Level | 3-5% U-235 | 5-20% U-235 |

| Primary Applications | Existing nuclear fleet | SMRs, Gen IV reactors |

| Current U.S. Production | Limited domestic capacity | Zero commercial production |

| Market Demand Growth | Stable replacement market | Exponential growth projected |

The absence of domestic HALEU production has historically required advanced reactor developers to rely on foreign suppliers or limited DOE research quantities for fuel supply. Companies developing small modular reactors, including NuScale, X-energy, and TerraPower's Natrium design, have identified HALEU availability as a critical path constraint affecting commercialisation schedules.

Advanced Reactor Market Dependencies

Small modular reactors and Generation IV designs require HALEU fuel to achieve enhanced thermal efficiency and extended operational cycles compared to traditional reactor technologies. The higher enrichment levels enable more compact reactor cores whilst maintaining proliferation-resistant fuel specifications below weapons-usable concentrations.

Advanced reactor developers have secured significant private and public funding commitments, yet fuel supply uncertainties have complicated deployment timelines and operational cost projections. Consequently, the DOE awards $2.7B for HALEU and LEU enrichment programme directly addresses this constraint by establishing multiple domestic production pathways capable of supporting large-scale advanced reactor deployment.

Geographic Distribution Creates Regional Manufacturing Hubs

Ohio Centrifuge Expansion Leverages Existing Infrastructure

Centrus Energy's American Centrifuge Plant in Piketon, Ohio, benefits from established uranium enrichment infrastructure and regulatory approvals, enabling rapid capacity expansion rather than comprehensive facility construction. The company announced plans to add 300 new jobs at the facility in advance of federal funding decisions, indicating confidence in contract award outcomes.

Operational Advantages:

- Pre-existing NRC licensing and regulatory compliance frameworks

- Established workforce with uranium enrichment operational experience

- Existing cascade infrastructure requiring expansion rather than replacement

- Supply chain relationships with uranium conversion and transportation providers

The Piketon facility's operational history provides immediate scaling capability for both LEU and HALEU production within existing facility boundaries. This approach reduces regulatory timeline uncertainty compared to greenfield developments whilst leveraging proven centrifuge technology deployed globally by established enrichment operators.

Kentucky Greenfield Development at Historic Nuclear Site

General Matter's selection of the former Paducah Gaseous Diffusion Plant site represents strategic reuse of historically significant uranium enrichment infrastructure. The DOE Office of Environmental Management signed a lease providing General Matter with a 100-acre parcel of federal land plus 7,600 cylinders of depleted uranium hexafluoride as feedstock.

Strategic Site Advantages:

- Access to existing nuclear infrastructure and security frameworks

- Federal land lease arrangements reducing initial capital requirements

- Feedstock provision eliminating upstream uranium conversion dependencies

- Historical workforce familiarity with uranium enrichment operations

The Paducah site operated as a major U.S. enrichment facility from 1952 until 2013 when gaseous diffusion operations ceased. Redeploying this location for modern enrichment technology demonstrates federal commitment to revitalising legacy nuclear sites whilst supporting private sector development of domestic fuel production capacity.

Tennessee LEU Focus Supports Existing Fleet Requirements

Orano Federal Services' Project IKE development in Oak Ridge focuses exclusively on low-enriched uranium production, targeting the substantial ongoing fuel requirements of the existing U.S. nuclear fleet. The $5 billion total project investment represents significant private sector commitment to domestic LEU production capacity.

Project Timeline:

- NRC licensing initiation: Early 2026

- Expected licence approval: 2026-2027

- Commercial operations start: 2031-2032

- Full capacity achievement: Mid-2030s

Oak Ridge's selection continues the site's historic role as a centre for U.S. nuclear technology development, providing symbolic continuity with Manhattan Project origins whilst addressing contemporary energy security requirements through private sector investment and operation.

Import Substitution Addresses Geopolitical Dependencies

The United States currently imports approximately two-thirds of its low-enriched uranium requirements, creating vulnerabilities to supply disruptions and price volatility from international sources. Russian uranium imports, historically representing 15-20% of total U.S. supply, face complete prohibition by 2028 under current federal legislation.

Current Import Structure Analysis:

- Total annual U.S. LEU demand: ~50 million pounds U3O8 equivalent

- Historical Russian supply: 15-20% of total consumption

- European consortium supply: 35-40% of imports

- Domestic production gap: 30-35 million pounds annually requiring substitution

The 2028 timeline for complete Russian uranium import prohibition creates urgent domestic capacity development requirements. European sources, whilst politically reliable, operate under their own capacity constraints and prioritise European utility customers, potentially limiting availability for expanded U.S. demand, contributing to ongoing uranium supply volatility.

Supply Chain Resilience Through Diversification

The multi-recipient award structure establishes geographically and technologically diverse production capabilities, reducing concentration risks that could affect overall domestic supply security. Each facility operates under different ownership structures, regulatory pathways, and technological approaches.

Risk Mitigation Framework:

- Technology diversity: Centrifuge and laser-based enrichment methods

- Geographic distribution: Ohio, Kentucky, and Tennessee operational locations

- Ownership variety: Established operators and emerging companies

- Capacity redundancy: Multiple facilities capable of LEU and HALEU production

This diversified approach ensures that facility-specific operational disruptions, regulatory delays, or technical challenges at individual sites cannot compromise overall domestic enrichment capacity development objectives.

Market Dynamics and Economic Implications

Pricing and Long-Term Contract Structures

Domestic uranium enrichment typically commands premium pricing compared to international sources, reflecting higher labour costs, regulatory compliance requirements, and return on investment expectations for private facility development. Nuclear utilities must balance fuel cost considerations against supply security benefits when evaluating long-term procurement strategies.

Economic Impact Assessment:

- Domestic pricing premium: Estimated 10-25% above international spot markets

- Contract duration: Typically 10-20 year agreements for supply security

- Price volatility reduction: Domestic sources reduce exposure to international market fluctuations

- Supply security value: Risk mitigation benefits may justify premium pricing structures

Utility sector analysis suggests that fuel cost increases from domestic sourcing represent manageable impacts on overall electricity generation costs, particularly when balanced against supply security improvements and reduced exposure to geopolitical disruptions affecting international uranium markets. However, this must be considered alongside broader uranium investment strategies that utilities are adopting.

Technology Development Investment Returns

Global Laser Enrichment's $28 million allocation represents targeted investment in next-generation enrichment technology that could fundamentally improve production economics through reduced energy consumption and enhanced separation efficiency compared to traditional centrifuge methods.

Laser isotope separation technology offers theoretical advantages in power consumption per separative work unit and potential for more precise enrichment control. However, commercial-scale deployment remains technically challenging, requiring continued development investment to achieve competitive operational parameters.

Regulatory Pathways and Implementation Timelines

Each recipient faces different regulatory approval processes based on facility status, technology approach, and site characteristics. Existing facilities benefit from established licensing frameworks, whilst greenfield developments require comprehensive Nuclear Regulatory Commission review processes.

Regulatory Timeline Comparison:

| Company | Facility Type | Licence Timeline | Production Start |

|---|---|---|---|

| Centrus Energy | Existing expansion | 2026-2027 | 2028-2029 |

| General Matter | New construction | 2026-2028 | 2030-2031 |

| Orano Federal Services | New facility | 2026-2027 | 2031-2032 |

| Global Laser Enrichment | Technology development | 2027-2029 | 2032-2033 |

The staggered production timelines create sequential capacity additions that align with projected demand growth for both existing fleet fuel requirements and emerging advanced reactor deployment schedules. Early production from expanded existing facilities provides near-term import substitution whilst new facilities address longer-term capacity requirements.

Licensing Risk Factors

Nuclear Regulatory Commission licensing processes involve comprehensive safety, security, and environmental reviews that can extend beyond initial projections based on technical complexity, public comment periods, and regulatory staff availability. New facility licensing typically requires 2-4 years from initial application submission to final licence issuance.

Companies with existing NRC licences and operational experience benefit from streamlined expansion approval processes, whilst startup operators face more extensive regulatory scrutiny and potential timeline extensions based on technical review outcomes and stakeholder input processes. Furthermore, the broader national security order priorities may influence regulatory processing timelines.

The next major ASX story will hit our subscribers first

Long-Term Strategic Scenarios and Capacity Planning

Nuclear Capacity Expansion Requirements

The administration's goal of quadrupling U.S. nuclear capacity by 2050 requires corresponding expansion of domestic fuel production capabilities. Current nuclear capacity of approximately 95 gigawatts would expand to nearly 380 gigawatts under maximum deployment scenarios, necessitating 300-400% increases in annual fuel supply.

Capacity Growth Projections:

- Current U.S. nuclear capacity: ~95 GW across 93 operating reactors

- 2050 deployment target: ~380 GW including existing and new capacity

- Required fuel supply expansion: 300-400% increase in annual separative work units

- Advanced reactor contribution: Estimated 100-150 GW from SMRs and Gen IV designs

Large-scale nuclear deployment scenarios, particularly for data centre and industrial applications, require assured fuel supply availability throughout multi-decade reactor operational lifetimes. Domestic production capacity becomes essential for supporting utility investment decisions and reactor deployment commitments.

Export Market Development Potential

Domestic enrichment capacity exceeding immediate U.S. requirements could position the United States as a uranium fuel exporter, particularly for HALEU products where global supply remains extremely limited. International advanced reactor development creates potential export opportunities for specialised fuel products.

Countries developing small modular reactor programmes, including Canada, United Kingdom, Poland, and others, require HALEU fuel supplies that currently lack established commercial production sources. As highlighted by the Department of Energy's commitment to nuclear fuel supply chains, U.S. enrichment capacity could serve these markets whilst generating export revenue and extending geopolitical influence through nuclear fuel relationships.

Implementation Risks and Monitoring Requirements

Technology and Execution Risk Assessment

Each recipient faces distinct implementation challenges based on technology maturity, operational experience, and facility development complexity. Established operators like Centrus benefit from proven centrifuge technology and operational experience, whilst startup companies carry higher execution risk profiles.

Risk Factor Analysis:

- Technology maturity: Centrifuge technology proven globally; laser-based systems require commercial validation

- Operator experience: Centrus and Orano have enrichment operational history; General Matter represents startup risk

- Regulatory complexity: New facilities face more extensive licensing requirements than expansions

- Capital availability: Private sector investment requirements beyond DOE funding commitments

Market demand validation remains critical as actual uranium consumption patterns may vary from projections based on reactor deployment timelines, particularly for advanced reactor technologies requiring HALEU fuel. Utility long-term procurement commitments provide demand visibility but require ongoing validation against actual deployment schedules.

Market Demand Evolution Scenarios

While utility commitments indicate strong projected demand for domestic enrichment services, actual consumption patterns depend on reactor deployment success, advanced technology commercialisation timelines, and competitive dynamics between nuclear and alternative energy sources.

Economic recession scenarios, regulatory delays affecting reactor construction, or technological breakthroughs in competing energy technologies could affect nuclear capacity deployment rates and corresponding fuel demand projections. The diversified investment approach provides flexibility to adjust production levels based on market evolution.

Global Nuclear Leadership and Competitive Positioning

The DOE awards $2.7B for HALEU and LEU enrichment programme demonstrates American commitment to nuclear technology leadership and strategic independence from foreign fuel supply dependencies. Domestic production capabilities become increasingly important as global nuclear capacity expands and geopolitical tensions affect traditional supply chain relationships.

International Competitive Landscape:

- Russia (Rosatom): ~45% global enrichment market share with established international relationships

- European Consortium (Urenco): ~25% market share serving European and select international customers

- China (CNNC): ~15% market share with rapidly expanding domestic and export capacity

- United States (post-investment): Projected 20-25% coverage of domestic demand with potential export capability

Global nuclear capacity expansion, particularly in Asia and emerging markets, creates growing demand for enrichment services beyond current supplier capabilities. U.S. domestic capacity development positions American companies to compete for international contracts whilst ensuring domestic fuel security through established production infrastructure.

Strategic Alliance Development Opportunities

Domestic enrichment capability enables the United States to develop strategic nuclear fuel partnerships with allied nations developing nuclear power programmes. Countries seeking alternatives to Russian nuclear technology and fuel supply increasingly value partnerships with democratic suppliers committed to non-proliferation standards.

The AUKUS partnership, NATO energy security initiatives, and Indo-Pacific strategic frameworks could incorporate nuclear fuel cooperation agreements that leverage U.S. domestic enrichment capacity whilst supporting allied energy security objectives and reducing collective dependencies on authoritarian suppliers. Moreover, as detailed in recent nuclear fuel enrichment analyses, these partnerships could strengthen international nuclear supply chains.

The DOE awards $2.7B for HALEU and LEU enrichment initiative represents a pivotal moment in American energy independence and nuclear leadership. By establishing multiple domestic production pathways, the programme addresses critical vulnerabilities in nuclear fuel supply chains whilst positioning the United States to compete in expanding global nuclear markets. The strategic investment framework balances immediate operational requirements with long-term technological advancement objectives, creating a foundation for sustained nuclear energy growth and international influence.

Disclaimer: This analysis is based on publicly available information and industry projections as of January 2026. Actual implementation timelines, production capacities, and market outcomes may vary based on regulatory approvals, technical developments, and evolving market conditions. Investment and policy decisions should consider comprehensive due diligence beyond the scope of this analysis.

Want to Capitalise on Nuclear and Uranium Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX uranium and mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 30-day free trial today with Discovery Alert and secure your market-leading advantage in the expanding nuclear sector.