July 18, 2026

The Sovereign-Private Blueprint Reshaping Global Phosphate Supply Chains

Phosphate fertilizer markets operate under a structural asymmetry that few other commodity sectors can match. A single country, Morocco, sits atop an estimated 70% or more of the world's economically recoverable phosphate reserves, giving its state-owned producer OCP a degree of supply-side influence that is difficult to overstate. Yet controlling reserves is only one dimension of market power. The other dimension — distribution reach, commercial networks, and feedstock supply logistics — has historically required private-sector partnerships to unlock at scale. The deepening alliance between OCP Nutricrops and Koch Ag & Energy Solutions represents the most advanced expression of this sovereign-private synthesis currently operating in global fertilizer markets, making the OCP Koch phosphate joint venture a development of significant strategic importance.

Understanding this partnership requires looking beyond the transaction itself and examining the strategic architecture being constructed, the supply chain vulnerabilities being navigated, and the competitive pressures building from neighbouring North African producers. Furthermore, the broader context of global commodity tariffs and shifting trade dynamics makes this alliance all the more consequential.

When big ASX news breaks, our subscribers know first

How the OCP Koch Phosphate Joint Venture Is Structured

A 50:50 Framework Built Around Jorf Lasfar's Industrial Core

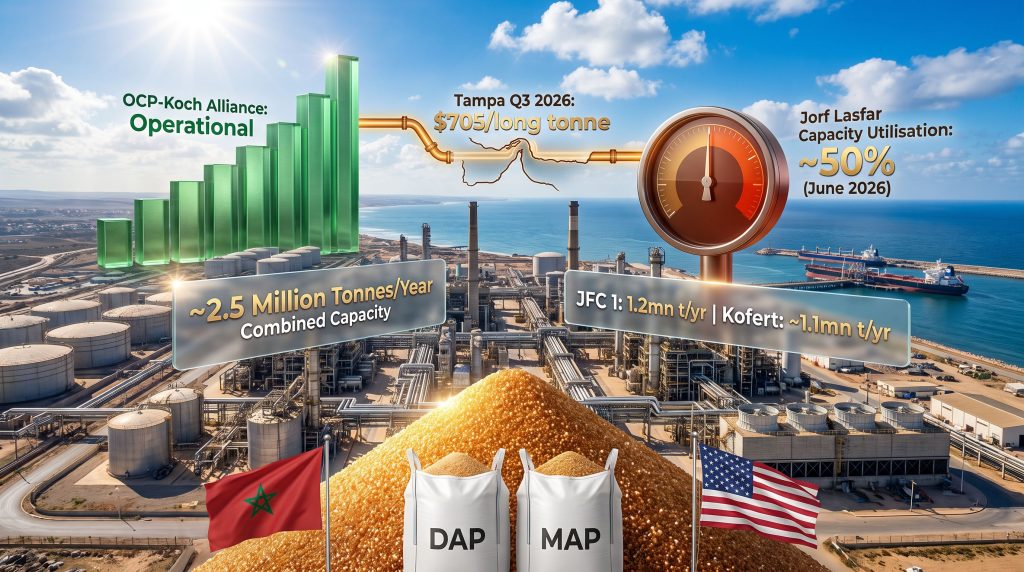

The OCP Koch phosphate joint venture operates through an equal-equity ownership model across two production facilities at Morocco's Jorf Lasfar industrial complex, one of the world's largest integrated phosphate fertilizer platforms. The latest agreement establishes a 50:50 joint venture over the Jorf Fertilizers Company 1 facility, known as JFC 1, which carries a nameplate production capacity of 1.2 million tonnes per year of phosphate-based fertilizers.

This builds directly on the earlier Kofert partnership, formerly known as Jorf Fertilizers III, in which Koch acquired a 50% stake from OCP in March 2022. Together, the two joint ventures create a combined bilateral production alliance with a capacity footprint of approximately 2.5 million tonnes per year.

| Joint Venture Entity | Established | OCP Stake | Koch Stake | Annual Capacity |

|---|---|---|---|---|

| Kofert (JFC III) | March 2022 | 50% | 50% | ~1.1 million t/yr |

| JFC 1 | 2025/2026 | 50% | 50% | ~1.2 million t/yr |

| Combined Alliance Total | ~2.5 million t/yr |

Scale Context: A 2.5 million tonne per year production capacity across two facilities positions the OCP-Koch alliance at a scale comparable to the total annual phosphate fertilizer output of multiple mid-tier producing nations combined. This is not a niche arrangement; it is a structurally significant force in global fertilizer supply.

The 50:50 ownership structure carries specific operational logic. Koch's contribution extends beyond capital. The company supplies ammonia and sulphur inputs that are essential feedstocks in the phosphate-to-fertilizer conversion process, effectively integrating upstream raw material access with downstream distribution capability. This transforms Koch from a passive investor into an active production partner whose supply chain relationships directly determine JFC throughput economics.

What the OCP Koch Alliance Produces and Why It Matters for Global Agriculture

DAP, MAP, and the Phosphoric Acid Chain

The primary outputs of the JFC 1 and Kofert facilities are Diammonium Phosphate (DAP) and Monoammonium Phosphate (MAP), the two dominant phosphate-based fertilizer grades in global agricultural markets. Both products are manufactured through a reaction chain that begins with phosphate rock, proceeds through sulphuric acid treatment to produce phosphoric acid (the critical intermediate), and then combines with ammonia to produce the final granular product.

The feedstock intensity of this process is a point that casual observers frequently underestimate. Producing a single tonne of phosphoric acid requires approximately 0.6 tonnes of sulphur, making sulphur not a secondary input but a primary production constraint. This ratio has enormous implications for understanding OCP's operational difficulties in mid-2026, discussed in detail below.

DAP and MAP hold a unique position in global agricultural supply chains for one fundamental reason: there is no viable substitute for phosphorus in crop nutrition. Unlike nitrogen, which biological fixation can theoretically supplement, phosphorus must be mined, processed, and applied. This makes phosphate fertilizers a non-discretionary input for food production at scale, underpinning consistent long-run demand across:

- Brazil, the world's largest agricultural commodity exporter and a major DAP/MAP importer

- India, which imports nearly all of its phosphate fertilizer requirements due to limited domestic reserves — a pattern well illustrated by the country's India import dynamics across multiple commodity sectors

- Southeast Asia, where intensifying palm oil and rice cultivation drives structural import demand

- North America, a historically significant DAP/MAP consumption market with shifting import supplier dynamics

The US Market Re-Entry: Countervailing Duties and the Koch Advantage

How an Eight-Month Trade Window Changes the Commercial Calculus

For a significant period, US countervailing duties on imports of Moroccan phosphate fertilizers effectively closed the North American market to OCP product flows. These trade remedy measures, imposed in response to findings of subsidised production, created a tariff barrier that made Moroccan product commercially uncompetitive against alternative suppliers in the US market.

The suspension of these duties for an eight-month period reopens a high-value market corridor at precisely the moment OCP's JFC 1 joint venture with Koch is being formalised. This timing is unlikely to be coincidental. Koch Fertilizer LLC operates one of the most extensive private fertilizer distribution networks in North America, with logistics infrastructure, blending capacity, and customer relationships that give it the commercial reach to absorb large volumes of imported DAP and MAP efficiently.

The critical risk embedded in this opportunity is binary: if countervailing duties are reinstated at the end of the suspension period, the North American market access rationale for the joint venture's near-term commercial strategy requires significant recalibration. Buyers and analysts monitoring the OCP Koch phosphate joint venture should track the progression of US trade remedy proceedings closely, as reinstatement would divert product flows back toward traditional OCP export markets in South Asia, Latin America, and Sub-Saharan Africa.

Sulphur: The Feedstock Chokepoint That Caps the Alliance's Upside

Strait of Hormuz Closure and the Cascading Supply Chain Crisis

The most operationally significant constraint facing the OCP Koch phosphate joint venture in mid-2026 is not market access or competitive positioning. It is sulphur availability.

Sulphur for Moroccan fertilizer production flows primarily from Middle Eastern refinery and gas processing operations, with supplementary volumes historically sourced from Kazakhstan. Both supply corridors experienced severe disruption simultaneously in 2026. The re-escalation of US-Iran military confrontation led to Iran declaring the Strait of Hormuz closed again over the weekend of 11-12 July 2026, following a brief reopening period governed by a memorandum of understanding signed on 18 June. Kazakh sulphur export volumes remained independently constrained, compounding the supply stress.

The consequences for OCP's operations were direct and measurable. Jorf Lasfar capacity utilisation fell to approximately 50% of total output capacity during June 2026, driven primarily by sulphur feedstock shortages rather than demand weakness or mechanical issues. While sulphur inventory replenishment is understood to have theoretically enabled a return toward full capacity operation in July-August 2026, the structural vulnerability of relying on geopolitically exposed supply corridors for an irreplaceable feedstock represents a systemic risk that cannot be solved through short-term stock management.

Sulphur Price Stress in Numbers

The pricing data from 2026 illustrates the scale of market dislocation:

| Metric | Data Point |

|---|---|

| Tampa Q3 2026 liquid sulphur contract price | $705/long tonne (record high) |

| Tampa Q2 2026 contract price | $655/long tonne |

| Quarter-on-quarter price increase | +$50/lt (+8%) |

| US Gulf spot sulphur export price (9 July 2026) | $1,100-1,150/t fob |

| OCP Jorf Lasfar capacity utilisation (June 2026) | ~50% |

The Q3 2026 Tampa contract price of $705/long tonne not only set a new record but surpassed the prior peak established during the second quarter, which had itself already broken the previous record from 2008. The divergence between the contract price and the US Gulf spot price of $1,100-1,150/t fob signals the severity of the physical market tightness. That gap of roughly $400/t between contract and spot reflects a market where buyers willing to pay any price for prompt physical sulphur were competing against a structurally constrained supply base.

Less Commonly Known Dynamic: The moderate Tampa contract settlement relative to spot prices is thought to reflect deliberate affordability management. Downstream phosphate fertilizer demand had already weakened due to elevated input costs. Some US Gulf sulphur producers also lack export infrastructure for solid sulphur, making them dependent on domestic liquid sulphur consumers and acutely sensitive to any demand collapse that could fill their storage tanks.

Competitive Landscape: Morocco Under Pressure as Algeria Accelerates

The North African Phosphate Race Intensifies by 2027

The OCP Koch phosphate joint venture does not operate in a static competitive environment. Algeria is advancing an ambitious state-directed phosphate industry buildout that, if delivered on schedule, will add substantial new export capacity to regional and global markets by 2027.

Algeria's Integrated Phosphate Project (IPP), a partnership between state-owned energy company Sonatrach and state mining firm Sonarem, includes a phosphoric acid, sulphuric acid, and ammonia facility at Oued Keberit in Souk Ahras province. The IPP Souk Ahras facility is designed to produce 900,000 tonnes per year of P₂O₅ equivalent phosphoric acid, implying a potential phosphate rock feedstock demand of approximately 3 million tonnes per year. The project is targeting a Q1 2027 production start.

Supporting this production buildout, Algeria is simultaneously expanding its Annaba port to handle vessels of up to 80,000 tonnes cargo capacity, compared with the current 55,000-tonne maximum loading capability. The workforce and equipment deployment at Annaba has been accelerated, with completion also targeted for Q1 2027, timed to coincide with the IPP's first export shipments.

Separately, Somiphos, a Sonarem subsidiary, is targeting a 1 million tonne per year capacity expansion at its Djebel Onk phosphate rock mine by mid-2027. A supply agreement of up to 1 million tonnes per year has already been signed with Indonesia's state-owned fertilizer group Pupuk Indonesia, pre-positioning Algerian rock exports into the strategically important Southeast Asian market before the expanded mine reaches full output.

Strategic Positioning Comparison

| Producer | Key Asset | Capacity Target | Primary Market Focus | Status |

|---|---|---|---|---|

| OCP-Koch Alliance | JFC 1 + Kofert, Jorf Lasfar | 2.5mn t/yr combined | Global (US re-entry focus) | Operational |

| Algeria IPP (Sonatrach/Sonarem) | Souk Ahras P₂O₅ facility | 900,000 t/yr P₂O₅ | Export markets | Q1 2027 target |

| Algeria Somiphos | Djebel Onk mine expansion | +1mn t/yr rock | Indonesia (Pupuk deal) | Mid-2027 target |

| Ma'aden (Saudi Arabia) | Wa'ad Al Shamal complex | ~3mn t/yr phosphates | Asia, global | Operational |

Morocco's competitive moat remains deep, anchored by reserve scale, established processing infrastructure, and now the integrated marketing capability that the Koch partnership provides. However, the window of unchallenged North African export dominance is narrowing as Algeria's state-directed phosphate industrialisation agenda moves from planning to physical execution. In addition, the Saudi Arabia minerals strategy continues to evolve in ways that could further reshape regional competitive dynamics.

The next major ASX story will hit our subscribers first

Three Strategic Scenarios for the OCP Koch Phosphate Joint Venture

Scenario 1: Accelerated US Market Penetration (Base Case)

If the countervailing duty suspension converts into durable tariff relief, Koch's North American logistics infrastructure becomes a permanent competitive advantage for OCP product. Ongoing US-China trade tensions are already incentivising US agricultural buyers to diversify away from Chinese phosphate fertilizer suppliers. Moroccan DAP and MAP, channelled through the Koch distribution network, are the most naturally positioned alternative. Under this scenario, the JFC 1 capacity addition translates directly into growing US market share, and the return profile on the joint venture supports further capital deployment.

Scenario 2: Sulphur Constraint Caps Production Upside (Downside Risk)

A prolonged Strait of Hormuz closure combined with sustained Kazakh export restrictions could keep sulphur prices structurally above $800/t for an extended period. Under these conditions, Jorf Lasfar capacity utilisation may remain below 80% even with the JFC 1 joint venture fully operational on paper. Elevated DAP and MAP prices resulting from constrained supply would suppress agricultural demand, particularly in price-sensitive markets in South and Southeast Asia. This scenario carries the most significant food security implications globally, as reduced Moroccan output would create a supply gap that no single alternative producer can rapidly fill.

Scenario 3: Alliance Expansion Into Additional Jorf Lasfar Units (Upside Case)

Successful US market re-entry generating strong returns could create the commercial justification for OCP and Koch to extend their 50:50 model to additional production units at Jorf Lasfar beyond JFC 1 and Kofert. A combined JV capacity exceeding 3.5 to 4 million tonnes per year would firmly establish the alliance as the dominant bilateral production partnership in global phosphate trade, materially exceeding the production scale of Ma'aden's Wa'ad Al Shamal complex in Saudi Arabia. This scenario also meaningfully diversifies Koch's commodity portfolio beyond its historically nitrogen-weighted asset base.

Furthermore, for context on the scale of phosphate resource bases that underpin these competitive dynamics, the Ammaroo phosphate project in Australia offers a useful reference point for understanding how emerging producers are attempting to position themselves relative to established North African supply chains.

Analytical Note: Of the three scenarios, Scenario 2 carries the most systemic significance for global food markets. The sulphur-phosphate feedstock chain is one of the least visible yet most consequential supply chain dependencies in the global food system. When sulphur flows from the Middle East are disrupted, the impact propagates within weeks through to phosphate fertilizer availability and ultimately to planting economics in agricultural nations with limited import diversification options.

The Broader Significance of the Sovereign-Private Joint Venture Model

Why Private Capital Is Moving Upstream in Phosphate

The sovereign-private joint venture model reflects a structural shift in how private trading and distribution companies approach commodity markets. Historically, firms like Koch Fertilizer LLC derived their commercial advantage from aggregating supply through offtake agreements and optimising logistics. The move toward upstream equity stakes signals a recognition that arm's-length offtake contracts provide insufficient supply security and margin stability in a market where sovereign producers hold dominant reserve positions.

By taking a production equity stake, Koch gains:

- Preferential access to product volumes without dependence on open-market procurement

- The ability to manage transfer pricing and marketing economics within the JV structure

- A hedge against third-party supply disruptions that could otherwise leave its distribution network undersupplied

For OCP, the benefits flow in the opposite direction: access to private capital that reduces sovereign balance sheet strain, guaranteed offtake through Koch's distribution channels, and feedstock supply contributions in the form of ammonia and sulphur that reduce OCP's own procurement exposure.

One underappreciated dimension of large-scale joint venture marketing arrangements is their effect on spot market liquidity. When a significant share of Moroccan phosphate export volumes becomes effectively captive to joint venture marketing structures, the volume of product available for price discovery through transparent spot market transactions shrinks. Consequently, this can increase price volatility for buyers operating outside the JV structure, particularly smaller import nations without the purchasing scale to negotiate long-term supply agreements directly with OCP or Koch.

Frequently Asked Questions: OCP Koch Phosphate Joint Venture

What is the OCP Koch phosphate joint venture?

A 50:50 operating joint venture between Morocco's OCP Nutricrops and US-based Koch Ag & Energy Solutions, covering two production facilities at the Jorf Lasfar industrial complex. Combined annual capacity across JFC 1 and Kofert is approximately 2.5 million tonnes of phosphate-based fertilizers, primarily DAP and MAP.

What products does the OCP Koch joint venture produce?

The primary outputs are Diammonium Phosphate (DAP) and Monoammonium Phosphate (MAP), both manufactured via phosphoric acid as the core intermediate. Product is marketed globally through OCP's distribution infrastructure combined with Koch Fertilizer LLC's North American commercial networks.

How does the US countervailing duty suspension affect the OCP Koch joint venture?

The eight-month suspension of US countervailing duties on Moroccan phosphate imports reopens the North American market to OCP-Koch product flows, a corridor previously closed by trade remedy measures. Koch's established US distribution infrastructure makes this market re-entry commercially executable at scale.

What is the sulphur supply risk for OCP's Jorf Lasfar operations?

Sulphur feedstock shortages, linked to the re-closure of the Strait of Hormuz and constrained Kazakh export flows, reduced OCP's Jorf Lasfar complex to approximately 50% of total capacity during June 2026. Given that roughly 0.6 tonnes of sulphur are required per tonne of phosphoric acid produced, even partial supply interruptions translate rapidly into significant output reductions.

Who are the emerging competitors to the OCP Koch alliance?

Algeria's state-directed Integrated Phosphate Project, targeting a Q1 2027 production start with 900,000 t/yr of P₂O₅ capacity at Souk Ahras, and the Somiphos Djebel Onk mine expansion targeting an additional 1 million t/yr of phosphate rock by mid-2027, represent the most proximate competitive development. Saudi Arabia's Ma'aden Wa'ad Al Shamal complex also operates at significant scale in overlapping export markets.

This article contains forward-looking statements, scenario projections, and market analysis based on publicly available information as of the time of writing. Commodity markets are subject to rapid change. Readers should not interpret any content herein as financial, investment, or trading advice. Independent professional guidance should be sought before making decisions based on commodity market analysis.

Want to Track the Next Major Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex commodity data into actionable investment insights for both new and experienced investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.