June 7, 2026

When Diplomatic Signals Move Oil Markets More Than Fundamentals

Energy markets have always been acutely sensitive to political risk, but the speed at which crude prices respond to diplomatic signalling reveals something deeper about how modern commodity markets are structured. Traders do not wait for signed agreements or verified supply restorations. They price probabilities, not certainties. When geopolitical tension builds a substantial risk premium into crude benchmarks, any credible signal of de-escalation triggers an immediate unwinding of that premium, regardless of whether a single barrel of oil has actually changed course.

That dynamic is precisely what drove oil prices fall on possible Iran peace deal signals in early May 2026, sending Brent crude tumbling for a second consecutive session even as the underlying supply disruption remained entirely intact. Furthermore, understanding crude oil price trends in recent years helps contextualise just how dramatic this reversal has been.

When big ASX news breaks, our subscribers know first

Understanding the Risk Premium That Built Oil to $126 Per Barrel

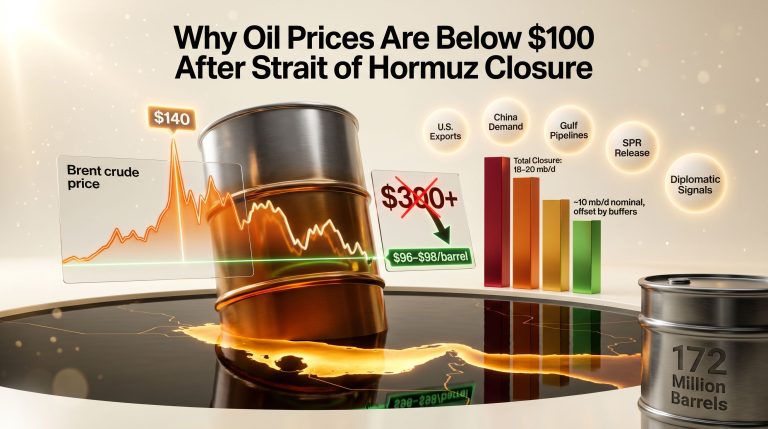

To understand why oil prices fell so sharply, it is necessary to first understand why they had climbed so high. Brent crude reached approximately $126 per barrel in early May 2026, its highest trading level since March 2022, according to Arab News. That elevated price did not reflect a permanent structural shift in global supply and demand fundamentals. It reflected a concentrated geopolitical risk premium attached to one critical piece of global energy infrastructure: the Strait of Hormuz.

The Strait is the world's most consequential maritime energy corridor. A significant share of global crude oil and liquefied natural gas transits through this narrow waterway daily, connecting Persian Gulf producers to markets across Asia, Europe, and beyond. Its closure or restriction creates a direct transmission mechanism between Middle Eastern conflict and global energy costs. When the Strait was closed as a consequence of the Iran war, the physical supply loss cascaded through to inventory drawdowns across the globe.

How Three Consecutive Weeks of US Inventory Declines Confirmed the Supply Crisis

The evidence of genuine supply stress was not merely theoretical. American Petroleum Institute data for the week ending May 1, 2026, confirmed three consecutive weeks of US crude inventory declines, with the following drawdowns recorded in the most recent reporting period:

| Inventory Category | Weekly Change (Week Ended May 1, 2026) |

|---|---|

| Crude Oil Stocks | -8.1 million barrels |

| Gasoline Inventories | -6.1 million barrels |

| Distillate Stocks | -4.6 million barrels |

Source: American Petroleum Institute figures, as cited by Arab News, May 6, 2026

These drawdowns are significant for a critical reason that often escapes casual observation: inventory declines during a price spike suggest that demand destruction has been insufficient to offset the supply loss. Under normal market conditions, prices rising to $126 per barrel would incentivise demand reduction substantial enough to rebalance the market. The fact that inventories kept falling indicates the supply disruption exceeded the market's ability to self-correct through price signals alone.

When crude inventories fall for three consecutive weeks despite prices at multi-year highs, the market is telling you that the supply disruption is structural, not cyclical. Price alone cannot fix a closed strait.

The Anatomy of Trump's "Project Freedom" Pause

On Tuesday, May 5, 2026, US President Donald Trump announced that the United States would temporarily suspend Operation Project Freedom, a naval initiative designed to escort stranded commercial tankers through the Strait of Hormuz. The announcement came only hours after Secretary of State Marco Rubio had briefed reporters on the programme, which had been publicly announced the previous Sunday.

The critical distinction embedded in Trump's announcement was that the military blockade of Iranian ports would remain in full force, while only the escort operation for third-party commercial vessels was being paused. This nuance matters enormously for understanding what markets were actually pricing. The physical supply constraint on Iranian oil exports remained unchanged. What changed was the diplomatic atmosphere surrounding potential negotiations.

The timing of the announcement also carried tactical significance. On Monday, the day before the pause declaration, US military forces had destroyed several Iranian small boats along with cruise missiles and drones while guiding two commercial vessels out of the Gulf through the Strait, according to Arab News. Active military engagement was ongoing at the operational level even as high-level diplomatic signals emerged, illustrating the layered complexity of the situation.

Tehran did not issue an immediate official response to Trump's announcement, leaving the negotiation framework's viability unconfirmed from Iran's side at the time of market opening on May 6. Consequently, the intersection of oil and geopolitics remained as volatile as ever, with every statement from either party being parsed for its implications on supply flows.

A Two-Day Price Correction in Context

The market reaction to the peace deal signals unfolded across two trading sessions, with both major crude benchmarks experiencing meaningful declines:

| Benchmark | Previous Session Drop | May 6 Drop | Price Level (May 6) | Approximate Peak (Early May) |

|---|---|---|---|---|

| Brent Crude Futures | -4.0% | -1.5% ($1.69) | $108.18/barrel | ~$126/barrel |

| WTI Crude Futures | -3.9% | -1.6% ($1.67) | $100.60/barrel | ~$120/barrel |

Source: Arab News, citing Reuters data as of 09:40 a.m. Saudi time, May 6, 2026

The combined two-day decline of approximately 5.5 percent across both benchmarks is significant by commodity market standards. Crude oil, being one of the most liquid physical commodities in the world, typically requires a substantial volume of position unwinding to generate moves of this magnitude over such a short timeframe. A move driven entirely by a single diplomatic announcement, with no confirmed change in physical supply flows, underscores just how large the geopolitical risk premium had become.

From the $126 peak to $108.18, Brent shed roughly $17.82 per barrel, or approximately 14 percent. This contraction represents the partial unwinding of the conflict risk premium that had accumulated since the Strait of Hormuz closure began restricting global supply flows.

Why a $5.5 Percent Two-Session Move Matters in Energy Markets

For context, daily price swings of 1 to 2 percent in crude oil markets are considered elevated but not exceptional during periods of geopolitical tension. A sustained two-day correction of this magnitude driven by a single unverified diplomatic signal reflects an unusually high degree of market sensitivity, itself a function of how concentrated the risk premium had become. Brent and WTI futures traders, in particular, were quick to unwind long positions as the probability of de-escalation increased. When traders agree that a large portion of the prevailing price reflects a single risk factor, any credible diminishment of that risk triggers coordinated selling across futures, options, and related instruments simultaneously.

What Markets Are Actually Pricing: Probability, Not Certainty

A critical insight from Anh Pham, senior research specialist for oil at LSEG, clarifies the interpretive framework that informed market participants are applying to these developments. Pham noted that the announcement signals potential de-escalation and raises hopes for the release of stranded vessels inside the Gulf, which could gradually bring supply back to the market, while simultaneously cautioning that prospects for a peace deal remain uncertain and that restoring full trade flows will take time even if an agreement is reached, as reported by Arab News.

This expert framing highlights a systematic mispricing risk embedded in the current correction. Markets are behaving as if supply restoration is a near-term certainty, but the physical mechanics of unwinding a maritime blockade operate on a different timeline than diplomatic announcements. In addition, oil market volatility driven by geopolitical uncertainty compounds this mispricing risk further.

Markets are not pricing a confirmed peace deal. They are pricing the probability of one. Even a moderate increase in de-escalation probability is sufficient to trigger significant downward pressure when a substantial risk premium is already embedded in the price.

Three Scenarios for Oil Prices From Here

The trajectory of crude prices from this point depends heavily on which of three broadly defined scenarios materialises:

Scenario 1: Full Agreement Signed

A comprehensive and verified peace deal between the US and Iran would theoretically enable gradual supply restoration as stranded vessels are cleared to transit the Strait. However, the physical process involves insurance clearances, port logistics, crew rotations, and vessel inspections that require weeks to execute. Markets would likely price forward expectations of supply restoration aggressively, but the actual barrels would arrive later than the diplomatic timeline suggests. A modest risk premium reflecting implementation uncertainty would likely persist for weeks.

Scenario 2: Partial Ceasefire or Stalled Negotiations

A partial resolution, such as a humanitarian pause or limited vessel release, would sustain uncertainty about the durability of any arrangement. Under this scenario, a meaningful geopolitical risk premium remains embedded in crude prices, potentially preventing a full normalisation toward pre-conflict pricing levels. Market volatility would remain elevated as traders re-rate probabilities with each new diplomatic development.

Scenario 3: Talks Collapse

A breakdown in negotiations would likely trigger a rapid reversal of the risk premium contraction seen across the two-day correction. Prices would move sharply higher as the market reprices the supply disruption and conflict risk at their previous elevated levels. The speed of this reversal could exceed the speed of the initial decline, given that physical inventory drawdowns would have continued in the interim. According to reporting from Time Magazine, the broader oil and gas market remains acutely exposed to precisely this kind of rapid reversal.

The next major ASX story will hit our subscribers first

The Broader Economic Toll of Sustained High Oil Prices

The economic consequences of the sustained supply disruption extend well beyond the trading screens. Crude oil prices transmit through the economy via multiple channels:

- Consumer energy bills: Higher crude prices lift retail gasoline and diesel costs directly, reducing disposable income for households globally.

- Transportation and logistics costs: Freight and aviation fuel costs rise proportionally, increasing the cost of moving goods across supply chains.

- Industrial input costs: Petrochemicals, plastics, and synthetic materials derived from crude oil become more expensive, affecting manufacturing margins.

- Inflation dynamics: Persistent oil price elevation feeds into headline inflation measures, complicating monetary policy decisions for central banks managing rate cycles.

The asymmetric impact across economies is also worth noting. Oil-importing economies in Asia and Europe bear the full cost burden of elevated crude prices without any offsetting revenue benefit. Gulf producers and other oil-exporting nations, by contrast, capture the windfall revenue from higher prices, which funds fiscal expenditure and sovereign investment programmes. This divergence reshapes global current account balances and capital flows during sustained supply shocks.

How OPEC+ Dynamics Shift If Iranian Supply Returns

A fully resolved conflict and the restoration of Iranian export capacity would introduce a significant new variable into OPEC+ supply management calculations. Iran holds substantial proven crude oil reserves and has historically been a major OPEC producer. Reintegrating Iranian barrels into global supply at scale would require OPEC+ members, particularly Saudi Arabia, to assess whether coordinated production adjustments are necessary to prevent a market oversupply condition.

Saudi Arabia's position is particularly complex. As both a leading OPEC+ member and a regional power with its own strategic interests in the Iran situation, the Kingdom would need to balance alliance obligations within the cartel against market share considerations. OPEC's market influence is already being tested by this evolving dynamic, and a scenario where Iranian barrels return at volume without corresponding cuts from other producers could push prices below levels that support Gulf states' fiscal breakeven requirements.

Frequently Asked Questions: Oil Prices and the Iran Peace Deal

Why did oil prices fall on possible Iran peace deal signals?

Brent crude had been trading at approximately $126 per barrel, a level that embedded a substantial geopolitical risk premium reflecting the Strait of Hormuz closure and associated supply disruptions. When signals emerged suggesting a potential diplomatic resolution, markets began unwinding that risk premium across two trading sessions, pushing prices lower even before any formal agreement was confirmed by either party.

What is the Strait of Hormuz and why does it matter for global oil prices?

The Strait of Hormuz is one of the world's most critical maritime energy corridors, through which a significant portion of global crude oil and liquefied natural gas transits daily. Any disruption to passage through the Strait directly restricts the volume of oil reaching international markets, creating sustained upward price pressure that manifests in global energy costs. As reported by 9News, shipping firms are also facing sanctions risks tied directly to this waterway.

What is "Project Freedom" and why was it paused?

Project Freedom was a US Navy-led operation to escort stranded commercial tankers through the Strait of Hormuz. The operation was temporarily paused by the US administration as a diplomatic gesture intended to create space for potential peace negotiations with Iran. Critically, the naval blockade of Iranian ports remained in effect throughout the pause.

Will oil prices immediately recover if a peace deal is signed?

According to LSEG's senior oil research specialist Anh Pham, as reported by Arab News, prices are expected to remain elevated in the near term even following a confirmed agreement. Restoring full trade flows through the Strait involves logistical lead time that extends well beyond diplomatic announcements, meaning physical supply relief arrives materially later than market pricing may anticipate.

What do the US inventory drawdowns indicate about actual supply stress?

Three consecutive weeks of US crude inventory declines, culminating in an 8.1 million barrel drawdown for the week ended May 1, confirm that the supply disruption is creating genuine and measurable tightness in physical commodity markets, not merely a trader sentiment effect. Oil prices fall on possible Iran peace deal news, however, suggests that markets remain forward-looking and highly sensitive to any probability-shifting developments.

Key Takeaways for Investors and Market Observers

- Diplomatic optionality is priced, not certainty: The correction reflects increased probability of de-escalation, not a confirmed outcome.

- Inventory stress is real and measurable: Three consecutive weeks of US crude drawdowns confirm genuine physical supply tightness beyond futures market sentiment.

- Physical supply restoration lags diplomatic timelines: Even a signed agreement would require weeks of logistical lead time before additional barrels reach markets.

- A partial risk premium remains intact: Uncertainty over Iran's domestic political response and deal durability sustains a floor under crude prices.

- OPEC+ faces a structural recalibration: If Iranian export capacity returns to global markets at scale, coordinated supply management decisions become significantly more complex for the cartel.

- Inflation and consumer cost implications persist: Until physical supply normalises, the broader economic transmission of elevated energy prices continues to affect households and businesses globally.

Disclaimer: This article contains forward-looking analysis, market scenario projections, and third-party data points that involve inherent uncertainty. Nothing in this article constitutes financial or investment advice. Commodity markets are subject to rapid change, and actual outcomes may differ materially from scenarios described. Readers should consult qualified financial professionals before making investment decisions.

Want To Stay Ahead Of The Next Major Commodity Market Shift?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly cutting through market noise to surface actionable investment opportunities — explore Discovery Alert's discoveries page to see the historic returns major discoveries have generated, then begin your 14-day free trial to position yourself ahead of the market.