June 9, 2026

Global energy markets demonstrate remarkable sensitivity to macroeconomic forces, with monetary policy decisions and currency fluctuations creating cascading effects across commodity pricing structures. The interconnected nature of modern financial systems means that shifts in dollar strength, interest rate expectations, and institutional positioning can amplify fundamental supply-demand imbalances in ways that traditional market analysis often overlooks. Furthermore, understanding these economic policy & tariffs implications becomes essential for market participants.

Understanding the Economic Mechanics Behind Oil Price Corrections

Energy price volatility reflects complex interactions between geopolitical risk assessments and underlying market fundamentals. When oil prices fall on US-Iran de-escalation, the mechanism involves rapid repricing of supply disruption probabilities rather than actual physical supply changes.

The February 2, 2026 market session demonstrated this dynamic clearly, with Brent crude futures declining $3.63 per barrel (5.2%) to $65.69 and WTI crude falling $3.60 per barrel (5.5%) to $61.61. These price movements occurred within hours of diplomatic signals from Washington and Tehran, highlighting the speed at which geopolitical risk premiums can unwind.

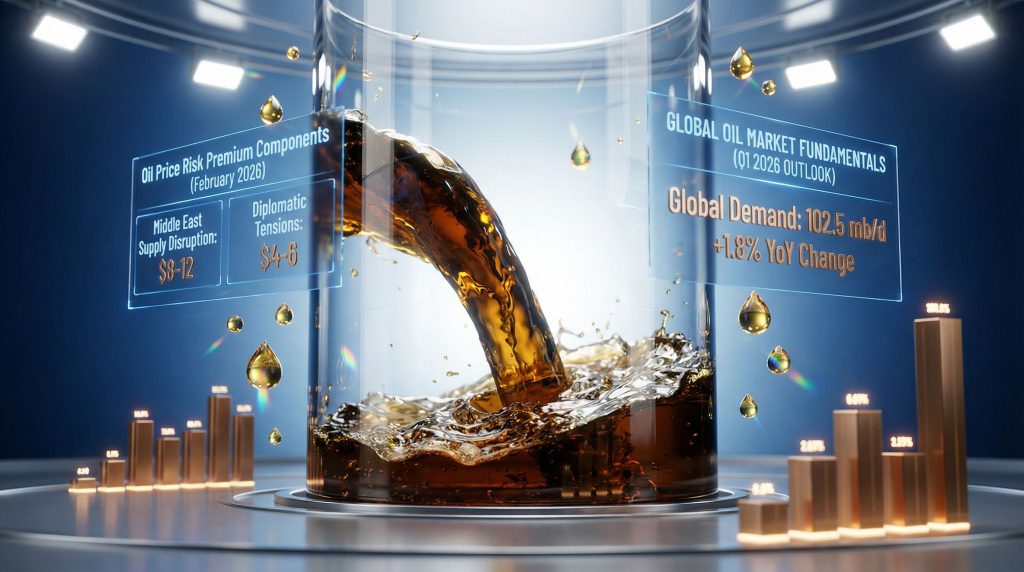

Table: Oil Price Risk Premium Components During Geopolitical Tensions

| Risk Factor | Price Impact Range | Market Response Speed | Duration |

|---|---|---|---|

| Middle East Supply Disruption | $8-12/barrel | Immediate | 3-6 months |

| Diplomatic Breakthrough | $3-5/barrel decline | 24-48 hours | 1-3 months |

| Production Capacity Concerns | $3-5/barrel | Weekly | 6-12 months |

| Strategic Reserve Actions | $2-4/barrel | Daily | 2-4 months |

Market analysis from UBS highlighted multiple concurrent factors driving the correction beyond diplomatic developments. The assessment noted declining supply disruptions in the United States and Kazakhstan, combined with the absence of further Middle East tension escalation, created systematic downward pressure on crude valuations.

This pattern validates the theoretical framework where markets distinguish between event risk and fundamental supply-side dynamics. The magnitude of January's price gains (Brent +16%, WTI +13%) had incorporated substantial geopolitical premiums that unwound rapidly when diplomatic signals reduced perceived escalation probabilities. Additionally, the OPEC meeting impact becomes crucial during such volatile periods.

When big ASX news breaks, our subscribers know first

The Role of Risk Premium Unwinding in Energy Markets

Geopolitical risk premiums in oil markets operate through asymmetric pricing mechanisms where accumulation occurs gradually while unwinding happens rapidly. The January 2026 period exemplified this pattern, with persistent diplomatic tensions building premiums over weeks that dissipated within a single trading session.

OPEC+ production decisions during this period reflected sophisticated market psychology understanding. The organization's February meeting resulted in maintaining output levels unchanged for March, continuing the November 2025 freeze on planned increases through Q1 2026. This production discipline during elevated geopolitical tensions allowed OPEC+ to benefit from risk premiums without triggering demand destruction through excessive pricing.

Strategic Production Considerations:

- Seasonal demand patterns justify Q1 production restraint historically

- Geopolitical risk premiums provide temporary price support above fundamental levels

- Member fiscal requirements necessitate sustained pricing above $60/barrel for Brent

- Market share preservation versus revenue optimization creates complex trade-offs

The speed of risk premium unwinding demonstrates institutional positioning dynamics. When diplomatic breakthroughs occur, leveraged funds and commodity trading advisors often reduce exposure simultaneously, amplifying price movements beyond what fundamental supply-demand changes would suggest.

Capital Economics characterized the market structure as fundamentally bearish, with geopolitical risks providing temporary masking of underlying supply-demand imbalances. This assessment proved prescient as markets refocused on surplus supply concerns following the diplomatic de-escalation. According to recent reports on oil price volatility, these market dynamics continue to evolve rapidly.

Cross-Asset Correlation Patterns During Geopolitical Transitions

The February 2, 2026 market session revealed synchronized declines across multiple commodity sectors, with oil, precious metals, and agricultural products falling simultaneously. This pattern reflects institutional portfolio rebalancing rather than sector-specific fundamental changes.

Contagion Transmission Mechanisms:

- Currency strength dynamics making dollar-denominated commodities more expensive internationally

- Risk-off positioning triggering systematic commodity exposure reduction

- Margin requirement adjustments forcing leveraged position liquidation

- Correlation trading strategies amplifying initial price movements

Analysis from Phillip Nova identified the specific currency transmission channel operating during this period. Renewed U.S. dollar strength increased the cost of dollar-denominated oil for international purchasers, creating demand elasticity reduction independent of fundamental supply-demand shifts.

This currency effect operates through multiple pathways. Non-U.S. buyers require more local currency units to purchase the same quantity of oil when the dollar strengthens, effectively reducing their purchasing power. Simultaneously, U.S. exporters of other goods become less competitive internationally, creating feedback loops through trade balance adjustments.

The coordination between Federal Reserve policy expectations and commodity pricing creates additional complexity. Interest rate differentials drive capital flows that strengthen the dollar, while quantitative tightening cycles reduce global liquidity available for commodity speculation. However, the central bank impact extends beyond domestic considerations.

Federal Reserve Policy Transmission Through Commodity Channels

Dollar strength amplifies commodity price volatility by creating feedback loops between monetary policy expectations and global demand patterns. The February 2, 2026 session demonstrated this mechanism, where currency appreciation contributed to oil price declines beyond the direct impact of geopolitical de-escalation.

Policy Transmission Sequence:

- Interest rate expectations influence dollar exchange rates against major currencies

- Currency strength affects international commodity purchasing power

- Demand elasticity changes create secondary price pressures

- Institutional positioning adjusts to currency-commodity correlation shifts

Central bank policy coordination effects extend beyond direct monetary policy announcements. When the Federal Reserve signals hawkish intentions, other central banks often respond with their own policy adjustments, creating competitive currency dynamics that amplify commodity price movements.

"Energy transition investments gain relative attractiveness when traditional oil markets demonstrate extreme volatility, as institutional capital seeks more predictable return profiles in renewable energy infrastructure."

The February 2026 event occurred without explicit Federal Reserve policy announcements, suggesting that dollar strength reflected market-driven positioning rather than direct policy communication. This distinction highlights the importance of market expectations versus official policy guidance in commodity price formation. In addition, the US–China trade impact adds another layer of complexity to these dynamics.

OPEC+ Production Strategy During Volatile Risk Environments

OPEC+ production decisions demonstrate strategic understanding of how geopolitical risk cycles interact with fundamental market conditions. The organization's ability to maintain production discipline while benefiting from elevated risk premiums represents sophisticated market timing.

February 2026 OPEC+ Decision Framework:

- Output maintenance for March 2026 continues November 2025 production freeze

- Seasonal justification based on Q1 demand weakness patterns

- Risk premium utilization allows revenue optimization without demand destruction

- Market stability considerations balance member country fiscal requirements

The strategic calculus involves multiple variables. OPEC+ members typically require Brent prices above $60/barrel for fiscal sustainability, with some countries needing higher thresholds. The February 2, 2026 price of $65.69/barrel provided adequate margins while remaining below levels that historically trigger significant demand destruction.

Production restraint during geopolitical volatility allows OPEC+ to benefit from temporary price support without structural market distortions. When risk premiums unwind, as occurred in February 2026, the organization can reassess production levels based on underlying fundamentals rather than geopolitical noise.

This approach contrasts with historical periods where OPEC+ increased production during price spikes, often contributing to subsequent price collapses when geopolitical tensions eased. The current strategy suggests evolved market sophistication within the producer alliance.

Fundamental Supply-Demand Imbalances Behind Geopolitical Noise

Market participants distinguished between temporary geopolitical risk factors and underlying structural conditions during the February 2026 correction. The rapid price decline occurred as attention returned to fundamental supply-demand dynamics that had been overshadowed by Iran-related tensions.

Structural Market Conditions (Q1 2026):

- Declining U.S. supply disruptions reduced non-OPEC+ production constraints

- Kazakhstan export normalization increased available supply in global markets

- Commercial inventory levels above historical averages in key consuming regions

- Demand growth moderation reflecting economic uncertainty and high energy costs

UBS analysis highlighted the return of focus to global oil supply exceeding demand concerns following geopolitical de-escalation. This assessment reflected underlying market conditions that existed throughout the January tension period but received minimal attention while risk premiums dominated pricing.

Table: Global Oil Market Fundamentals Assessment

| Metric | Current Estimate | Trend Direction | Market Impact |

|---|---|---|---|

| Global Demand Growth | +1.8% YoY | Moderating | Bearish pressure |

| Non-OPEC+ Supply | +3.4% YoY | Accelerating | Bearish pressure |

| OPEC+ Production | -2.1% YoY | Controlled restraint | Price supportive |

| Commercial Inventories | Above 5-year average | Building | Bearish pressure |

Capital Economics' characterization of geopolitical risks masking a fundamentally bearish oil market proved accurate as prices declined following diplomatic progress. The research firm's reference to well-supplied market conditions and comparison to previous Israel-Iran conflicts provided historical context for the risk premium unwinding. Consequently, comprehensive analysis of market fundamentals suggests continued volatility ahead.

Regional demand pattern shifts create additional complexity in fundamental analysis. Asian markets, particularly China's strategic petroleum reserve policies and India's expanding refining capacity, alter traditional demand elasticity assumptions and global oil flow patterns.

The next major ASX story will hit our subscribers first

Currency Dynamics Amplifying Commodity Price Movements

Dollar strength creates systematic pressure on dollar-denominated commodity prices through multiple transmission channels operating simultaneously. The February 2, 2026 session demonstrated how currency appreciation can amplify primary market movements beyond their fundamental significance.

Currency Transmission Mechanisms:

- Direct price effect: Stronger dollar increases commodity costs for international buyers

- Demand elasticity impact: Reduced purchasing power decreases consumption in non-U.S. markets

- Portfolio rebalancing: Currency appreciation triggers institutional position adjustments

- Margin dynamics: Leverage requirements adjust to currency volatility patterns

Analysis from Phillip Nova specifically identified the purchasing power transmission channel where renewed dollar strength makes oil more expensive for non-U.S. buyers. This mechanism operates independently of fundamental supply-demand conditions and can create false signals about underlying market balance.

International buyers face dual currency exposure when purchasing dollar-denominated commodities. Local currency depreciation against the dollar creates effective price increases that can reduce demand even when dollar-denominated prices remain stable. This dynamic contributed to the February 2026 oil price decline as currency effects reinforced geopolitical de-escalation impacts.

Central bank policy coordination creates additional currency volatility. When the Federal Reserve signals different policy trajectories than the European Central Bank, Bank of Japan, or Bank of England, competitive devaluations or strength cycles can emerge that systematically affect commodity pricing.

How Do Currency Fluctuations Impact Oil Purchasing Power?

Currency fluctuations create immediate cost implications for international oil buyers, as stronger dollar conditions reduce purchasing power for non-U.S. entities. This effect operates independently of underlying supply-demand fundamentals.

Furthermore, oil prices fall on US-Iran de-escalation events can be amplified when occurring simultaneously with dollar strength cycles, creating compound effects that exceed geopolitical risk premium adjustments alone.

Investment Implications from Oil Market Volatility Patterns

Energy sector rotation opportunities emerge when geopolitical risk premiums normalize, creating relative value propositions across different market segments. The February 2026 price correction illustrated how rapid premium unwinding can create tactical positioning opportunities for informed investors.

Portfolio Allocation Considerations:

- Energy sector positioning during risk premium normalization phases

- Currency hedge requirements for international commodity exposure

- Volatility strategies capitalizing on elevated implied volatility levels

- Supply chain investments in energy-intensive manufacturing sectors

Traditional energy investments face structural headwinds from transition pressures and regulatory changes, while renewable energy infrastructure demonstrates more predictable return profiles during volatile periods. The February 2026 correction reinforced this dynamic as institutional capital sought stability over volatility.

Volatility Trading Opportunities:

- Options strategies benefit from elevated implied volatility during geopolitical tensions

- Futures spreads capture premium normalization patterns

- Cross-commodity arbitrage exploits correlation breakdowns

- Currency-commodity pairs capitalize on transmission channel inefficiencies

Long-term structural investment themes include supply chain resilience in energy-intensive industries. Companies with diversified energy sourcing arrangements outperform during volatile periods, creating investment opportunities in industrials and materials sectors. Moreover, implementing appropriate volatility hedging strategies becomes essential for portfolio protection.

"Strategic Consideration: Energy transition investments gain relative attractiveness when traditional oil markets demonstrate extreme volatility, as institutional capital seeks more predictable return profiles in renewable energy infrastructure."

Oil Price Impact Transmission Through Economic Sectors

Energy price corrections create cascading effects through economic sectors with varying sensitivity levels and response timeframes. The February 2026 oil price decline demonstrated how rapid commodity adjustments influence different industries through distinct transmission mechanisms.

Table: Sectoral Sensitivity to Oil Price Changes

| Sector | Sensitivity Level | Response Lag | Regional Variation |

|---|---|---|---|

| Transportation | High (-0.3% per $10 change) | 1-2 quarters | Developed markets higher |

| Manufacturing | Medium (-0.15% per $10) | 2-3 quarters | Energy-intensive concentration |

| Consumer Discretionary | Low (-0.08% per $10) | 3-4 quarters | Income-level dependent |

| Energy Services | Very High (+0.5% per $10) | Immediate | Resource-rich regions |

Airlines and logistics companies typically benefit from rapid fuel cost reductions, while energy services firms face immediate revenue pressure from reduced exploration and production activity. Manufacturing sectors with high energy intensity, including chemicals, steel, and aluminum, experience delayed but sustained impacts as energy costs flow through production processes.

Consumer sectors demonstrate complex response patterns where lower energy costs can increase discretionary spending power, but this effect varies significantly by income demographics and regional economic conditions. Higher-income consumers often demonstrate lower sensitivity to energy price changes compared to lower-income segments.

Inflation expectations and monetary policy responses create secondary effects on commodity markets through expectations channels. Central bank reactions to energy price volatility influence forward guidance on interest rates, affecting investor positioning across multiple asset classes.

What Sectors Benefit Most from Oil Price Corrections?

Transportation and logistics sectors typically experience the most immediate benefits from oil prices fall on US-Iran de-escalation scenarios, as fuel costs represent significant operational expense components. Airlines, shipping companies, and trucking firms often see margin expansion within quarterly reporting cycles.

However, consumer discretionary sectors show more complex patterns, with benefits appearing over 3-4 quarters as lower energy costs increase disposable income for non-essential purchases.

Long-term Structural Changes in Global Oil Markets

Repeated geopolitical volatility accelerates corporate energy sourcing diversification, reducing single-region dependency while potentially increasing supply chain costs. This structural evolution reflects risk management priorities outweighing pure cost optimization in energy procurement strategies.

Supply Chain Diversification Trends:

- Geographic distribution of energy suppliers reduces concentration risk

- Contract structures incorporate flexibility provisions for volatile periods

- Strategic reserves at corporate level supplement government stockpiles

- Alternative energy integration creates competitive pressure on traditional pricing

Technology adoption acceleration during volatile periods includes digital trading platforms that reduce transaction costs and increase market efficiency. Predictive analytics improve inventory management and reduce volatility impacts on operational planning.

Market Structure Evolution:

- Electronic trading increases market liquidity and price discovery efficiency

- Data analytics improve supply-demand forecasting accuracy

- Financial instruments provide better hedging capabilities for market participants

- Renewable integration creates long-term competitive pressure on fossil fuel pricing

Alternative energy integration creates systematic competitive pressure on traditional oil pricing mechanisms. As renewable energy costs continue declining and grid integration improves, substitution effects become more pronounced during periods of fossil fuel price volatility.

Risk Assessment Framework for Energy Market Participants

Geopolitical risk premiums typically persist for 3-6 months with intensity declining as diplomatic progress continues or alternative supply arrangements develop. Historical analysis shows premiums averaging 10-15% of total crude value during peak tension periods.

Risk Premium Duration Analysis:

- Initial escalation phase: Rapid premium accumulation over 2-4 weeks

- Sustained tension period: Premium maintenance for 2-4 months

- De-escalation phase: Rapid unwinding over 24-72 hours

- Normalization period: Gradual stabilization over 4-8 weeks

Speculative positioning amplifies fundamental price movements, with leveraged funds often representing 20-30% of futures market open interest during volatile periods. This concentration creates systemic risk when positions unwind simultaneously.

Market participants must distinguish between temporary risk factors and structural market changes. The February 2026 event demonstrated how quickly geopolitical premiums can dissipate, while underlying supply-demand imbalances require longer-term solutions.

Practical Risk Management Applications:

- Hedging strategies must account for premium volatility patterns

- Contract negotiations should incorporate geopolitical adjustment mechanisms

- Inventory management requires buffer stock calculations for supply disruption scenarios

- Financial planning must model scenario-based price ranges rather than point estimates

How Long Do Geopolitical Risk Premiums Typically Last?

Historical analysis indicates that geopolitical risk premiums in oil prices fall on US-Iran de-escalation scenarios typically unwind within 24-72 hours of diplomatic breakthrough announcements. However, complete normalization requires 4-8 weeks as market participants reassess fundamental supply-demand conditions.

The intensity of premium unwinding depends on the severity of initial escalation and the credibility of diplomatic progress signals from both parties involved.

Disclaimer: This analysis contains forward-looking assessments and market projections that involve inherent uncertainties. Oil price forecasting involves significant risks due to unpredictable geopolitical developments, regulatory changes, and macroeconomic factors. Readers should conduct independent research and consult qualified financial advisors before making investment decisions based on this analysis.

Ready to Capitalise on Volatile Energy Market Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities as energy markets shift investor focus toward resource exploration companies. Begin your 14-day free trial today at Discovery Alert and secure your market-leading advantage whilst energy sector volatility creates new investment landscapes.