May 16, 2026

Global energy markets operate within a complex web of interconnected systems where supply disruptions cascade through multiple economic layers. The oil price rally analysis reveals that the fundamental mechanics of petroleum pricing extend far beyond simple supply-demand calculations, incorporating psychological risk assessments, geopolitical stability evaluations, and long-term strategic considerations. Furthermore, oil prices and Iran war dynamics shape investment flows and policy decisions worldwide.

Understanding Energy Security Through Economic Transmission Mechanisms

Energy price volatility represents one of the most significant challenges facing modern economies, with disruptions capable of triggering widespread economic adjustments across multiple sectors. The relationship between regional conflicts and petroleum pricing operates through sophisticated transmission channels that amplify initial shocks through interconnected global systems.

Current Market Dynamics and Historical Context

Recent market developments illustrate the complexity of energy pricing mechanisms. However, when examining oil movements amid trade wars, Brent crude futures have experienced substantial volatility, with prices reaching $111.01 per barrel amid ongoing regional tensions. This represents a 53% increase since late February 2026, while WTI crude has risen 45% to $97.07 per barrel during the same period.

The International Energy Agency has characterized the current situation as more severe than the two 1970s oil shocks combined. Consequently, approximately 11 million barrels per day have been removed from global circulation. This supply disruption affects roughly 11% of global crude oil supply, creating daily economic value disruption exceeding $1.2 billion.

| Market Indicator | Current Level | Change from Baseline |

|---|---|---|

| Brent Crude | $111.01/barrel | +53% YTD |

| WTI Crude | $97.07/barrel | +45% YTD |

| Daily Supply Loss | 11 million barrels | -11% global supply |

| Economic Impact | $1.2 billion/day | Sustained disruption |

When big ASX news breaks, our subscribers know first

Maritime Chokepoints and Global Energy Infrastructure

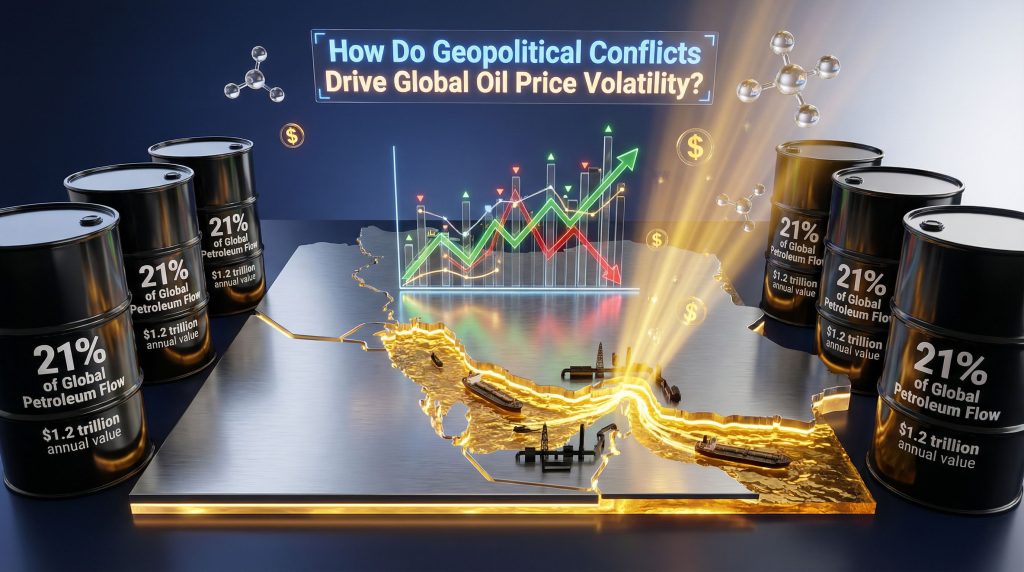

The Strait of Hormuz functions as the world's most critical energy transit corridor, facilitating approximately 21% of global petroleum liquids movement. This narrow waterway's strategic importance stems from its role as the primary export route for Gulf region petroleum production, handling crude oil flows valued at approximately $1.2 trillion annually.

Infrastructure Vulnerability Analysis

The strait's 21-mile width at its narrowest point creates asymmetric economic leverage, where relatively small disruptions generate disproportionate market responses. Moreover, maritime chokepoints demonstrate how geographic constraints can create systematic vulnerabilities in global energy distribution networks.

Key infrastructure elements at risk include:

- Kharg Island oil terminal (Iran's primary export facility)

- Tanker traffic volumes (300-400 monthly transits during normal conditions)

- Regional production access (30% of seaborne oil exports)

- Natural gas shipments (25% of global LNG trade)

Market participants recognise that even partial restrictions through this corridor can trigger significant risk premium adjustments. As reported by Morningstar, one Phillip Nova analyst noted, markets are currently pricing for conflict longevity rather than reacting solely to headline developments, with any direct damage to oil infrastructure potentially forcing rapid repricing scenarios.

Risk Premium Mechanisms in Energy Markets

Energy markets incorporate geopolitical uncertainty through sophisticated risk premium mechanisms that often exceed actual supply disruptions. These psychological components reflect collective market assessments of worst-case scenarios and probability-weighted outcome modelling.

Fear Premium Framework Analysis

Risk premium calculations typically incorporate multiple uncertainty factors:

- Immediate disruption risk: $8-12 per barrel

- Escalation probability: $5-8 per barrel

- Duration uncertainty: $3-7 per barrel

- Contagion potential: $2-5 per barrel

Current market pricing suggests risk premiums may account for 15-25% of oil prices during active conflicts. However, with Brent trading at $111.01 per barrel compared to pre-conflict levels around $72 per barrel, the embedded premium of approximately $39 per barrel represents roughly 35% of current pricing. This indicates heightened perceived risk levels regarding oil prices and Iran war developments.

Scenario-Based Pricing Models

Market participants utilise probabilistic outcome modelling to assess potential price trajectories:

Rapid De-escalation (25% probability)

- Oil prices normalise to $85-95/barrel within 60 days

- Risk premium contraction drives price relief

- Economic impact: Moderate inflation easing

Prolonged Standoff (45% probability)

- Oil sustains $110-130/barrel range for 6+ months

- Elevated risk premiums persist

- Economic impact: Sustained inflationary pressure

Infrastructure Damage Escalation (20% probability)

- Oil spikes to $150-200/barrel potential

- Catastrophic risk premium expansion

- Economic impact: Recession risk elevation

Regional Conflict Expansion (10% probability)

- Oil sustains $200+ barrel levels

- Systematic risk premium reaches crisis levels

- Economic impact: Global economic crisis potential

Critical Market Dynamic: Weekend risk factors create additional pricing complexity, as significant geopolitical events often occur during market closures, leading to gap openings and volatility spikes when trading resumes.

Economic Transmission Channel Analysis

Energy price shocks propagate through global economies via three distinct transmission channels, each creating cascading effects across different economic sectors and timeframes. In addition, tariff impact on markets further complicates these transmission mechanisms.

Primary Direct Cost Transmission

Direct cost impacts manifest immediately through:

- Transportation and logistics expenses (fuel surcharges, shipping costs)

- Manufacturing input costs (petrochemical feedstocks, energy-intensive production)

- Utility and heating expenditures (residential and commercial energy bills)

- Agricultural production costs (fertiliser prices, machinery operation)

Secondary Economic Effects

Secondary transmission occurs through behavioural adjustments:

- Consumer spending reallocation (reduced discretionary expenditure)

- Business investment delays (capital expenditure postponement)

- Currency fluctuation impacts (import cost adjustments)

- Trade balance adjustments (energy import-export dynamics)

Tertiary Systemic Impacts

Long-term structural effects include:

- Central bank policy responses (monetary tightening or accommodation)

- Government fiscal adjustments (subsidy programmes, strategic reserve releases)

- International capital flows (investment reallocation patterns)

- Energy transition acceleration (renewable energy investment increases)

Strategic Reserve Systems and Market Stabilisation

Strategic petroleum reserves serve as critical buffer mechanisms during supply disruptions. However, their effectiveness depends on coordinated release strategies and prevailing market conditions.

Global Reserve Capacity Structure

| Reserve System | Capacity (Million Barrels) | Import Coverage (Days) |

|---|---|---|

| United States SPR | 714 | 90-120 |

| China State Reserves | 500+ | 60-80 |

| IEA Member Collective | 1,500+ | 90+ |

| Private Commercial Storage | 2,800+ | Variable |

Release Strategy Economics

Optimal reserve deployment requires balancing immediate price relief against long-term strategic security considerations. Release timing must account for market psychology factors, production recovery timelines, and geopolitical negotiation dynamics.

The current crisis has highlighted coordination challenges among major reserve holders. Consequently, decisions require multilateral cooperation to maximise market impact while preserving strategic capabilities for extended disruption scenarios.

Regional Economic Impact Distribution

Energy price shocks affect global regions differently based on their economic structures, energy dependencies, and trade relationships. This creates distinct winners and losers during crisis periods.

Net Energy Importing Economies

Countries heavily dependent on energy imports face multiple economic pressures:

- Current account deficit expansion (increased import costs)

- Inflationary pressure acceleration (cost-push inflation dynamics)

- Economic growth deceleration (reduced disposable income effects)

- Currency depreciation risks (balance of payments pressures)

Recent reporting indicates emerging economies are experiencing particular stress. Furthermore, record debt issuance programmes encounter disruption as the Iran conflict impacts market conditions.

Net Energy Exporting Economies

Oil-producing nations benefit from windfall revenues but face distinct challenges:

- Revenue windfall generation (approximately $39/barrel premium above baseline pricing)

- Economic overheating risks (excessive liquidity injection)

- Currency appreciation pressures (Dutch disease effects)

- Resource curse vulnerabilities (economic diversification delays)

For typical Gulf exporters producing 10 million barrels daily, current pricing represents approximately $390 million in daily incremental revenue compared to pre-conflict levels.

Transit and Service Economies

Countries providing energy infrastructure services experience mixed impacts:

- Infrastructure utilisation increases (pipeline, refining capacity premiums)

- Geopolitical leverage enhancement (strategic positioning value)

- Investment opportunity expansion (infrastructure development demand)

- Security responsibility burdens (protection cost increases)

The next major ASX story will hit our subscribers first

Investment Flow Reallocation During Energy Crises

Sustained geopolitical tensions reshape global energy investment patterns. This influences long-term supply capacity development and technological innovation acceleration.

Capital Allocation Transformation

Crisis periods accelerate several investment trends:

Traditional Energy Infrastructure:

- Increased exploration spending in geopolitically stable regions

- Enhanced pipeline and storage capacity development

- Strategic transportation route diversification

- Emergency response capability expansion

Alternative Energy Systems:

- Accelerated renewable energy project development

- Enhanced energy storage technology investment

- Grid modernisation and resilience upgrades

- Energy efficiency technology advancement

Economic Diversification Programmes:

- Supply chain resilience building initiatives

- Regional energy hub development projects

- Technology innovation ecosystem creation

- Policy framework adaptation investments

Market Psychology and Behavioural Finance Factors

Energy market volatility during geopolitical conflicts demonstrates classic behavioural finance principles. Psychological factors significantly influence pricing beyond fundamental supply-demand calculations.

Speculative Positioning Dynamics

Futures market positioning intensifies during crisis periods:

- Long position accumulation by institutional investors

- Volatility regime shifts (2-3x historical volatility increases)

- Bid-ask spread widening (liquidity provision costs)

- Risk premium persistence (extended uncertainty pricing)

According to Yahoo Finance, a Sparta Commodities analyst noted the market's awareness of military buildup dynamics and tendency toward weekend event clustering when markets remain closed. This creates additional uncertainty layers regarding oil prices and Iran war outcomes.

Inventory Build Anticipation

Market participants increase strategic holdings in anticipation of future disruptions:

- Commercial inventory accumulation (storage capacity constraints)

- Strategic purchasing acceleration (supply security priorities)

- Forward contract premium expansion (future delivery guarantees)

- Alternative sourcing cost acceptance (supply diversity premiums)

Policy Response Framework Development

Effective responses to energy-driven economic disruption require coordinated approaches across multiple policy domains. This balances immediate stabilisation with long-term structural adaptation.

Immediate Crisis Management

Short-term policy measures focus on market stabilisation:

- Strategic reserve coordination (multilateral release timing)

- Emergency fuel allocation systems (priority sector protection)

- Targeted consumer assistance programmes (vulnerable population support)

- Financial market stability mechanisms (credit facility provisions)

Medium-term Structural Adaptation

Intermediate-horizon policies address systemic vulnerabilities:

- Energy efficiency acceleration programmes (consumption reduction incentives)

- Alternative supply source development (import diversification strategies)

- Economic sector resilience building (adaptive capacity enhancement)

- International cooperation framework enhancement (crisis response coordination)

Long-term System Transformation

Strategic policy initiatives target fundamental energy security:

- Energy transition acceleration (renewable capacity expansion)

- Supply chain geographic diversification (single-point-of-failure reduction)

- Economic flexibility enhancement (adaptive capacity building)

- Geopolitical risk mitigation strategies (diplomatic engagement frameworks)

When examining energy transition challenges, energy security increasingly requires balancing traditional supply reliability with transition toward renewable sources. This creates complex optimisation challenges for policymakers worldwide.

### What are the Key Sectoral Impact Areas?

Energy price volatility creates distinct patterns of sectoral winners and losers, generating both challenges and opportunities across different economic segments during crisis periods.

Primary Beneficiary Sectors

Certain industries experience positive impacts from energy crisis conditions:

- Alternative energy technology companies (accelerated adoption demand)

- Energy-efficient transportation systems (comparative advantage enhancement)

- Strategic commodity storage facilities (storage premium capture)

- Regional energy infrastructure projects (bypass route development)

Vulnerable Economic Segments

Energy-intensive sectors face significant cost pressures:

- Manufacturing industries (input cost increases, margin compression)

- Transportation and logistics (fuel cost pass-through challenges)

- Consumer discretionary spending (disposable income reduction)

- Tourism and hospitality industries (travel cost increase impacts)

Adaptive Sector Responses

Some industries demonstrate crisis adaptation capabilities:

- Financial services (commodity trading opportunity expansion)

- Technology solutions (efficiency optimisation demand growth)

- Infrastructure development (alternative route construction)

- Defence and security services (risk management demand increases)

Historical Precedent Analysis and Learning Applications

Previous oil shock episodes provide valuable insights for understanding current crisis transmission mechanisms and potential economic outcomes.

1973 Oil Embargo Impact Assessment

The Arab Oil Embargo demonstrated classic transmission channel effects:

- Price escalation: Oil prices increased from $3 to $12 per barrel (300% increase)

- GDP impact: 1-2 percentage point global growth reduction

- Inflation acceleration: 2-3 percentage point increases across OECD nations

- Employment effects: Unemployment increases during 1974-1975 recession

1979 Iranian Revolution Precedent

The Iranian Revolution crisis showed supply disruption impacts:

- Production collapse: Iranian output dropped from 6 million to near-zero barrels daily

- Price trajectory: Global prices rose from $15 to nearly $40 per barrel by 1980

- Economic consequences: Stagflation dynamics across developed economies

- Policy responses: Central bank monetary tightening, government stimulus programmes

Contemporary Crisis Comparison

Current circumstances present both similarities and distinctions compared to historical precedents:

- Scale: 11 million barrels daily represents larger absolute disruption

- Duration: One-month timeline suggests extended impact potential

- Geographic scope: Strait of Hormuz closure affects broader regional production

- Economic context: Different underlying economic conditions and policy frameworks

The International Energy Agency assessment that current conditions exceed both 1970s shocks combined suggests potential for more severe economic transmission effects than historical precedents.

### How Can Strategic Planning Address Future Scenarios?

Understanding potential outcome pathways enables better preparation for various crisis evolution trajectories. This supports both public policy development and private sector strategic planning.

Scenario Planning Framework

Multiple scenarios exist for crisis resolution, each carrying distinct economic implications and requiring different response strategies. Furthermore, energy security strategies must account for these varied possibilities.

Each scenario pathway involves different probability assessments, economic impact magnitudes, and appropriate policy response frameworks. Market participants and policymakers benefit from maintaining flexibility across multiple potential outcomes while preparing specific contingency plans for high-probability scenarios.

Investment Strategy Adaptation

Crisis conditions require portfolio and strategic adjustments:

- Geographic diversification (supply source and market exposure)

- Technology investment acceleration (efficiency and alternative energy)

- Risk management enhancement (hedging strategy sophistication)

- Operational flexibility development (adaptive capacity building)

Energy price volatility during geopolitical conflicts represents a fundamental challenge requiring sophisticated understanding of transmission mechanisms. The analysis of oil prices and Iran war dynamics reveals the need for risk assessment capabilities and coordinated response strategies. The intersection of geopolitical risk and energy markets will likely remain a critical factor in global economic stability, demanding continuous analysis and adaptive policy frameworks from both public and private sector participants.

Disclaimer: This analysis contains forward-looking assessments and scenario projections that involve substantial uncertainty. Oil prices and Iran war developments create volatile market conditions subject to rapid change. Readers should conduct independent research and consider multiple perspectives when making investment or policy decisions based on geopolitical energy market analysis.

Looking to Navigate Volatile Energy Markets During Geopolitical Crises?

Discovery Alert's proprietary Discovery IQ model identifies ASX mineral discoveries across critical commodities, including energy transition metals, providing real-time alerts when market volatility creates exceptional opportunities. Understand why major mineral discoveries can lead to significant market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, or begin your 14-day free trial today to position yourself ahead of the market during these uncertain times.