June 4, 2026

Why Oil Has Stopped Behaving Like a Cyclical Commodity

For most of modern financial history, energy markets operated on a predictable psychological rhythm. Geopolitical shocks would arrive, traders would panic, prices would spike, and within weeks or months, markets would exhale and crude benchmarks would drift back toward their equilibrium. That model shaped decades of portfolio construction, corporate hedging strategies, and central bank forecasting frameworks. It may no longer be valid.

The relationship between oil prices and Middle East conflict has fundamentally changed. What analysts are observing today is not a temporary disruption layered onto an otherwise stable market. It is the emergence of a new pricing architecture, one in which supply security itself commands a persistent premium that does not evaporate when ceasefire announcements cross the wire.

Understanding why this shift has occurred, and what it means for inflation, portfolio positioning, and the global economy, requires moving beyond headline-driven analysis into the structural mechanics of how modern energy markets are actually priced.

When big ASX news breaks, our subscribers know first

The Architecture of a New Pricing Regime

From Temporary Shocks to Embedded Risk Premiums

Traditional commodity theory categorised geopolitical events as exogenous shocks, temporary deviations from a mean that markets would quickly correct. That framework depended on several conditions: abundant spare production capacity, relatively modest baseline demand, diversified supply chains, and a diplomatic architecture capable of containing regional conflicts before they threatened physical oil flows.

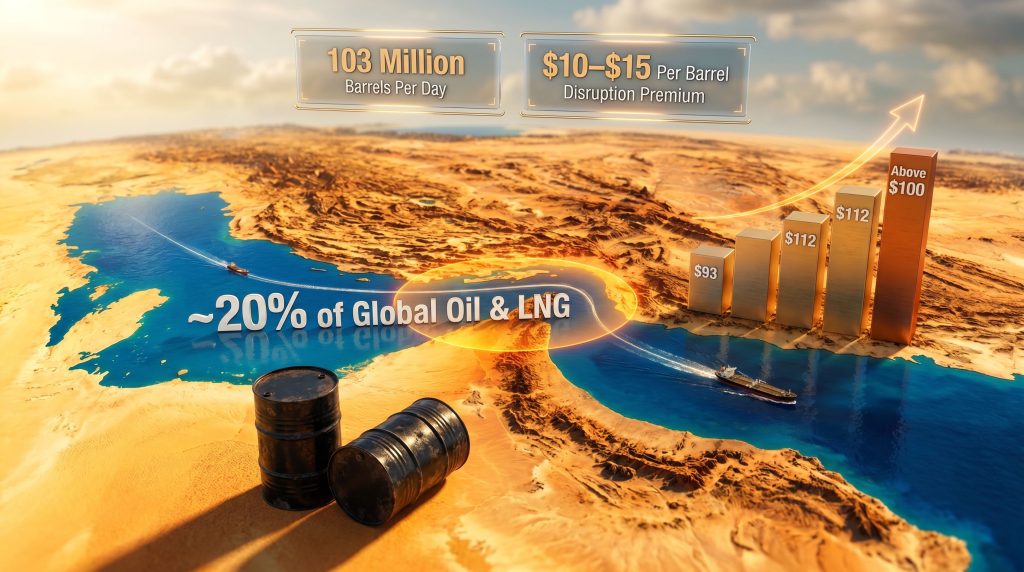

Each of those conditions has deteriorated meaningfully over the past several years. Global oil consumption now exceeds 103 million barrels per day, operating near all-time highs. Spare production capacity across OPEC+ nations sits at historically constrained levels, meaning the market's shock-absorbing buffer is considerably thinner than it was during previous conflict cycles such as the 1990 Gulf War or the 2008 price surge.

The result is a market that reacts to geopolitical risk not merely through short-term spot price movements, but through sustained adjustments across the entire forward curve. When medium-term contracts price in elevated risk alongside near-term contracts, that is not panic. That is a structural repricing, and it carries fundamentally different implications for how investors, businesses, and policymakers should respond.

Military Escalation in Lebanon and the Iran Factor

Israeli military operations pushing deeper into Lebanon have repeatedly reignited fears of a broader regional confrontation involving Iran-aligned forces. The concern is not simply about the immediate conflict itself. It is about the escalatory pathways that such confrontations can activate, particularly given Iran's documented capacity to threaten maritime transit through the Strait of Hormuz and its influence over Houthi operations in the Red Sea corridor.

The fragility of ceasefire arrangements between major regional and international powers has introduced a layer of diplomatic uncertainty that markets struggle to price with precision. Furthermore, when the downside risk scenario involves disruption to the world's most consequential energy chokepoint, the rational market response is to maintain a meaningful risk premium even during periods of apparent calm. The trade war impact on oil adds yet another layer of complexity to this already volatile environment.

The Strait of Hormuz: A Single Point of Failure for Global Energy

Why This Chokepoint Defines Global Energy Security

Approximately 20 percent of global oil consumption and a significant share of LNG supplies transit the Strait of Hormuz daily. The numbers alone do not fully capture the strategic vulnerability. Unlike pipeline infrastructure, which can sometimes be rerouted through alternative corridors, maritime chokepoints have no meaningful bypass options for large volumes of crude.

Critical Market Insight: Goldman Sachs Research has estimated that a severe disruption scenario at the Strait of Hormuz could add approximately $10 to $15 per barrel to global crude benchmarks. Given that Brent and WTI futures moved from roughly $93 per barrel before the latest escalation cycle to above $112 at peak crisis pricing, the market is already embedding a substantial portion of this risk into current valuations.

Iran has previously used the threat of Strait closure as an explicit geopolitical instrument. Naval incidents in the region have historically produced immediate and significant price responses. The fact that markets must continuously discount this tail risk, even during quieter periods, explains much of the structural premium currently embedded in crude prices. According to Al Jazeera's reporting on the Iran conflict, a prolonged military confrontation could have far-reaching consequences for energy markets well beyond the immediate region.

The Red Sea Dimension: A Dual Chokepoint Risk

Houthi attacks on commercial shipping in the Red Sea have compounded the Hormuz vulnerability by introducing a second layer of supply chain disruption. Major shipping carriers have been forced to reroute vessels around the Cape of Good Hope, adding approximately 10 to 14 days to voyage transit times and materially increasing fuel consumption per journey.

The combined effect creates what analysts are describing as a dual chokepoint risk environment: two critical maritime corridors simultaneously under threat, with limited hedging options available to importers at scale. This dynamic is without clear precedent in the post-Cold War era of globalised energy trade.

Brent Crude Pricing: Reading the Signals in the Data

The crude oil price trends across the current conflict cycle tell a story that goes beyond simple supply-and-demand mechanics.

| Price Stage | Brent Crude Level (USD/barrel) |

|---|---|

| Pre-escalation baseline | ~$93 |

| Crisis peak | ~$112 |

| Post-ceasefire partial retreat | Below $100 |

| Current level with renewed tensions | Above $100 |

The $19 per barrel swing between the pre-war baseline and the crisis peak represents the market's explicit valuation of supply disruption risk at its most acute. More significant analytically is what happened next: prices did not retrace fully to pre-conflict levels even as diplomatic activity produced temporary ceasefire arrangements.

Nigel Green, CEO of deVere Group, one of the world's largest independent financial advisory organisations, has argued that investors drawing comfort from the retreat from peak prices are misreading the signal. His position is that the assumption oil could quickly return toward pre-war levels is becoming increasingly difficult to justify analytically. Energy markets, in his assessment, are now pricing a new reality in which supply security carries a significant and durable premium.

Supply Fundamentals: Why the Market Has No Margin for Error

Demand at Record Levels With No Near-Term Ceiling

Global oil consumption above 103 million barrels per day reflects sustained demand growth driven by several structural forces:

- Continued industrialisation across major emerging market economies, particularly in South and Southeast Asia

- Strong aviation sector recovery following the pandemic-era collapse in air travel demand

- Petrochemical sector expansion, which uses oil not as fuel but as a feedstock for plastics, fertilisers, and synthetic materials

- The energy transition, while accelerating in specific sectors, has not yet produced a measurable reduction in aggregate global oil demand

This demand backdrop means the market has minimal slack to absorb supply disruptions without significant price consequences.

Constrained Spare Capacity: The Critical Vulnerability

Spare production capacity functions as the energy market's insurance policy. When it is abundant, as it was during earlier decades when Saudi Arabia could rapidly increase output by several million barrels per day, geopolitical shocks can be absorbed without triggering sustained price spikes.

Today's spare capacity environment is structurally different. OPEC's market influence has become increasingly constrained, and non-OPEC supply growth, particularly from U.S. shale producers, has moderated as operators have prioritised financial discipline over volume growth. The result is a market where even modest supply disruptions can produce outsized price responses.

The Inflation Transmission: How Oil Prices Reach Every Corner of the Economy

A Six-Month Lag With Compounding Effects

How the Mechanism Works: Crude price increases do not hit consumer prices instantaneously. The transmission process unfolds over a period of roughly three to six months, flowing through several distinct channels before appearing in headline CPI figures.

Economists estimate that every sustained increase of $10 per barrel in crude prices adds between 0.2 and 0.4 percentage points to inflation in advanced economies. The transmission channels operate in sequence:

- Fuel and energy costs rise immediately, affecting household petrol bills and business energy expenses directly

- Transportation and logistics costs increase as fuel represents a major operating expense for freight carriers

- Agricultural production costs climb as fertiliser prices, machinery fuel costs, and distribution expenses all increase

- Manufacturing input costs rise for energy-intensive industries, compressing margins and eventually pushing through to product prices

- Retail and consumer goods prices reflect the accumulated downstream cost increases, completing the transmission cycle

Central Banks Caught Between Inflation and Growth

Financial markets had broadly anticipated a cycle of interest rate reductions across major economies through 2025 and 2026, premised on inflation returning durably toward central bank targets. Sustained crude prices above $100 per barrel introduce a complicating variable that monetary policy cannot easily address.

Energy-driven inflation is particularly challenging for central banks because it originates in supply constraints rather than excess demand. Raising interest rates can dampen demand-driven inflation effectively, but does little to address a price level that reflects physical supply scarcity and geopolitical risk. Tightening monetary policy aggressively into an energy shock risks causing economic contraction without resolving the underlying inflationary pressure.

Nigel Green has specifically flagged the risk that higher-for-longer borrowing costs, if forced upon central banks by persistent energy inflation, would carry material consequences for government bond valuations, growth-oriented equities, and mortgage markets. This is the stagflationary risk scenario that policymakers most fear: elevated prices combined with decelerating economic activity, leaving no clean monetary policy response available.

The next major ASX story will hit our subscribers first

Sector Winners and Losers: The Asymmetric Impact Map

Not all economic actors respond the same way to elevated oil prices. The distributional consequences are substantial and, for investors, actionable.

| Sector | Impact | Primary Driver |

|---|---|---|

| Energy producers and integrated majors | Strongly Positive | Revenue expansion and margin growth |

| Gulf state sovereign wealth funds | Positive | Improved fiscal revenues |

| Commodity-exporting economies (AUD, CAD, NOK) | Positive | Trade balance and currency appreciation |

| Airlines | Strongly Negative | Fuel at 25-35% of total operating costs |

| Logistics and freight operators | Negative | Direct fuel cost pass-through |

| Energy-intensive manufacturers | Negative | Input cost compression |

| Consumer discretionary retail | Negative | Household spending power erosion |

| Emerging market oil importers | Strongly Negative | Currency weakness and import bill inflation |

Aviation represents perhaps the most acute sectoral vulnerability. Jet fuel typically accounts for between 25 and 35 percent of total airline operating costs. Airlines cannot rapidly pass sustained fuel cost increases through to consumers without triggering demand destruction, and hedging programmes, while helpful, are typically structured only 6 to 18 months in advance, leaving carriers exposed to sustained price shifts of the kind currently underway.

How Oil-Exporting and Oil-Importing Economies Diverge

The Fundamental Asymmetry

The macroeconomic consequences of sustained high oil prices are not shared equally across nations. The International Monetary Fund has consistently noted that oil price shocks produce fundamentally asymmetric outcomes: exporting nations with uninterrupted production capacity are relatively insulated and may benefit materially, while importing nations face simultaneous deterioration across multiple economic indicators.

Oil-exporting economies typically experience:

- Strengthening fiscal revenues and improved sovereign balance sheets

- Current account surplus expansion and sovereign wealth fund inflows

- Increased appetite for upstream capital expenditure

- Currency appreciation pressure as commodity-linked exchange rates strengthen

Oil-importing economies typically experience:

- Widening trade deficits and current account deterioration

- Currency depreciation, which amplifies the cost of oil imports further

- Domestic inflation that is difficult to contain through monetary policy alone

- Erosion of consumer and business confidence

Currency markets often reflect this divergence before equity and bond markets fully reprice. Commodity-linked currencies such as the Australian dollar, Canadian dollar, and Norwegian krone tend to appreciate relative to import-dependent currencies during sustained oil rallies. This creates both risk management challenges and portfolio positioning opportunities for internationally diversified investors. For a broader understanding of how these dynamics develop, CommBank's energy market explainer provides useful context for Australian investors navigating this environment.

Three Scenarios for Oil Prices Going Forward

Scenario 1: Diplomatic Resolution and Gradual De-escalation

Military activity in Lebanon and surrounding regions subsides; ceasefire arrangements hold. Brent crude gradually retreats toward the $85 to $90 per barrel range as supply risk premiums unwind. Central banks regain confidence to proceed with rate reduction cycles. However, structurally high demand and constrained spare capacity mean prices are unlikely to return to pre-2024 levels even under this optimistic pathway.

Scenario 2: Prolonged Conflict Without Infrastructure Disruption (Base Case)

Military operations continue but do not directly threaten Hormuz transit or major production facilities. Brent stabilises in the $95 to $105 range with elevated volatility. Inflation remains sticky, and central banks adopt a cautious, data-dependent stance. Most analysts currently consider this the most probable medium-term outcome.

Scenario 3: Escalation to Critical Infrastructure or Hormuz Disruption

Direct attacks on major production facilities or an effective closure of the Strait of Hormuz. Brent could spike toward $120 to $130 or higher in an acute disruption. Emergency strategic reserve releases by IEA member nations would be likely. Oil-importing economies face severe inflationary shocks and potential recession conditions.

Portfolio Recalibration: What Investors Need to Consider

Nigel Green of deVere Group has argued that a return to pre-war oil pricing appears increasingly unlikely in the foreseeable future, and that adapting to that reality could become one of the most consequential portfolio decisions investors face over the coming years. An oil price rally of this nature, sustained rather than fleeting, demands a fundamentally different strategic response from investors.

This perspective frames oil not as a cyclical variable to be managed tactically, but as a structural force reshaping multi-year market performance. Investors whose portfolio construction assumes a rapid reversion to $70 to $80 per barrel oil may be carrying significant mispricing risk across multiple asset classes simultaneously.

Practical portfolio considerations in a sustained high-oil environment include:

- Overweighting energy equities, particularly upstream producers and integrated majors that benefit directly from elevated crude benchmarks

- Reassessing exposure to long-duration growth stocks, whose valuations are compressed by higher-for-longer interest rate environments

- Reviewing bond duration positioning, as inflation persistence reduces the real return on long-dated fixed income

- Considering commodity-currency exposure through AUD, CAD, or NOK-denominated assets as natural portfolio hedges

- Underweighting aviation and consumer discretionary sectors most exposed to fuel cost and spending power headwinds

Frequently Asked Questions: Oil Prices and Middle East Conflict

Why do Middle East conflicts cause oil prices to rise?

The Middle East hosts a disproportionate share of global oil production and controls critical transit infrastructure. Markets respond to the risk of supply disruption even before any actual supply loss occurs, embedding a forward-looking risk premium into prices.

How much could a Hormuz disruption add to oil prices?

Goldman Sachs Research estimates a severe disruption scenario could add approximately $10 to $15 per barrel to global crude benchmarks, based on the roughly 20 percent of global oil and LNG that transits the strait daily.

Does every Middle East conflict cause sustained oil price increases?

Not necessarily. Historical analysis shows that conflicts which do not directly threaten production or transit routes often produce short-lived reactions. The critical determinant is whether physical supply flows face genuine disruption risk.

How does higher oil flow through to consumer prices?

Each sustained $10 per barrel increase adds an estimated 0.2 to 0.4 percentage points to inflation in advanced economies, with the full transmission typically taking three to six months to appear in headline CPI figures.

Which economies are most at risk?

Oil-importing nations, particularly across Asia, Europe, and emerging markets, face the greatest economic headwinds from sustained high crude prices. Oil-exporting nations with uninterrupted production capacity generally benefit from the same conditions.

Will oil prices return to pre-conflict levels?

Most analysts consider a full return to pre-conflict pricing levels increasingly unlikely in the near term, given structurally high demand, constrained spare production capacity, and a geopolitical risk premium that appears unlikely to fully unwind even with diplomatic progress.

Readers seeking ongoing coverage of global energy market dynamics and the evolving relationship between oil prices and Middle East conflict can access additional analysis and reporting at Petroleum Australia, covering energy sector developments across the Asia-Pacific region.

This article contains forward-looking analysis and scenario projections. These represent analytical frameworks rather than financial advice. Readers should seek independent financial counsel before making investment decisions based on commodity market forecasts.

Want To Catch The Next Major Mineral Discovery Before The Market Does?

While energy markets grapple with structural repricing and geopolitical uncertainty, significant mineral discoveries on the ASX can deliver equally transformative investment opportunities — and Discovery Alert's proprietary Discovery IQ model sends real-time alerts the moment those discoveries are announced, turning complex data across 30+ commodities into clear, actionable insights. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.