July 10, 2026

When Supply Disruptions Lose the Battle Against Macro Gravity

The history of oil market crises offers a consistent pattern: geopolitical shocks spike prices sharply, but the gravitational pull of macroeconomic fundamentals ultimately wins. The 1973 Arab oil embargo, the 1990 Gulf War, and the 2019 Abqaiq drone strikes all followed the same arc. A supply disruption triggers fear-based buying, prices surge, and then reality reasserts itself as demand signals, central bank policy, and inventory data gradually reclaim control of price direction.

That same pattern is playing out today, this time with considerably more complexity. Oil prices slide as US-Iran conflict clouds Hormuz reopening has become one of the defining market narratives of mid-2026, capturing a moment where multiple conflict theatres, monetary policy tightening, and structural demand shifts are colliding simultaneously. Understanding why prices are falling in the middle of an active war requires looking beyond the headlines and into the layered mechanics of how modern energy markets actually price risk.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz: Why This Waterway Defies Easy Substitution

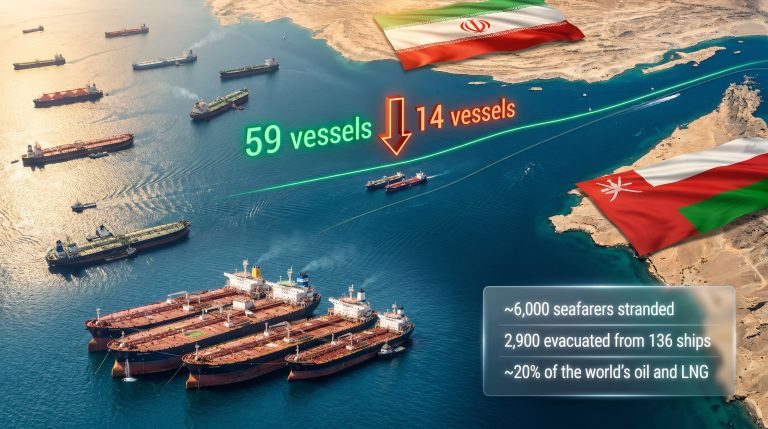

Before dissecting the current price dynamics, it is worth understanding precisely why the Strait of Hormuz commands such outsized attention from energy traders, policymakers, and military planners alike. The strait is a narrow maritime passage approximately 33 kilometres wide at its narrowest navigable point, separating Iran from the Arabian Peninsula. It is the only sea route connecting the Persian Gulf to the wider global ocean network.

Prior to the outbreak of the US-Iran conflict, roughly 20% of all globally traded oil passed through this single chokepoint every day. This includes crude exports from Saudi Arabia, Iraq, Kuwait, the UAE, and Iran itself, along with substantial volumes of liquefied natural gas from Qatar. There is no realistic alternative route that could absorb this volume at scale. The East-West Pipeline in Saudi Arabia and the Abu Dhabi Crude Oil Pipeline together offer partial bypass capacity, but neither can substitute for the strait's full throughput.

This structural irreplaceability is why even partial disruptions send shockwaves through energy markets. Furthermore, it explains why markets react so violently to tanker attacks, even when physical supply disruption is limited, because each incident raises the probability of a worse scenario. The broader picture of oil trade and geopolitics makes clear that these dynamics are not new, but the current convergence of pressures is unusually acute.

Hormuz Flow Recovery: What the Data Actually Shows

Goldman Sachs analysts tracking Persian Gulf shipping data reported that oil flows through the region recovered to above 80% of pre-war volumes during the first ten days following the strait's partial reopening, as vessels that had been trapped inside the Gulf rushed to exit. However, renewed attacks on tankers in the region caused that recovery to retreat to the low-70% range of normal throughput.

| Strait of Hormuz Flow Status | Volume as % of Pre-War Normal |

|---|---|

| Pre-conflict baseline | 100% |

| First 10 days post-reopening | 80%+ |

| Post-tanker attack retreat | ~70–72% |

| Market-implied ongoing range | 65–80% intermittent |

The partial recovery has not translated into price relief for a simple reason: physical security risks continue to deter full commercial shipping resumption. Tanker operators, insurers, and cargo owners are making voyage decisions based on war risk premiums that have become prohibitively expensive for some routes. Insurance war risk surcharges for Gulf transits have reportedly reached levels not seen since the 1980s Tanker War, adding material cost friction to every barrel that does flow through the strait.

Brent and WTI: Reading the Price Action Correctly

The current price levels require context to interpret properly. Brent crude futures fell approximately $1.12, or 1.4%, to $76.90 per barrel in Thursday trading, while WTI crude declined $1.20, or 1.6%, to $72.32 per barrel. These moves followed a sharp single-session surge of roughly 3% on Wednesday, when the breakdown of the temporary ceasefire was first confirmed by the US administration.

Critically, both benchmarks remain significantly below the near-$120 per barrel peak recorded at the height of the conflict earlier in 2026. The gap between that crisis peak and current trading levels is itself the most important data point in this story. It tells us that markets have progressively repriced downward as:

- The Hormuz closure proved partial rather than total

- Iranian export volumes did not collapse to zero due to sanctions workarounds

- Global demand signals softened across multiple major economies

- Central banks signalled rate caution, suppressing the industrial growth outlook

For a broader perspective on how these forces interact, the crude oil market overview for 2025 provides useful context on the structural factors that continue to shape price behaviour into 2026.

The Gravitational Forces Pulling Prices Down

| Market Driver | Price Direction | Relative Weight |

|---|---|---|

| US-Iran military escalation | Upward pressure | High but episodic |

| Hormuz transit disruption | Upward pressure | Moderate (partial restoration) |

| Federal Reserve inflation caution | Downward pressure | Persistent |

| US labor market in slow-hire mode | Downward pressure | Moderate |

| China producer price inflation surge | Downward pressure | Significant |

| July 17 sanctions waiver expiry | Upward pressure | Near-term binary catalyst |

The July 17 Sanctions Deadline: The Market's Most Immediate Binary Risk

One factor receiving insufficient attention in mainstream commentary is the July 17, 2026 sanctions waiver expiry. Following the ceasefire breakdown, the US administration revoked the temporary sanctions waiver that had permitted transactions involving Iranian crude oil. Under the current framework, those transactions remain permissible only until July 17. After that date, full sanctions enforcement resumes.

The practical implications of this deadline are significant:

- Buyers of Iranian crude, particularly in Asia, must either complete transactions before the deadline or face secondary sanctions exposure

- Iranian export volumes will likely tighten materially post-July 17 absent a diplomatic resolution

- Forward oil curves are beginning to reflect this near-term supply tightening risk

- Any diplomatic breakthrough before the deadline could trigger a sharp downward price correction as the supply risk premium deflates

The July 17 sanctions deadline is the most immediate binary price catalyst in the oil market. A resolution removes upward pressure; a hard enforcement triggers supply tightening that could push Brent back toward the $85–$90 range in the near term.

There is also a lesser-known dimension to the sanctions architecture worth understanding. Iranian crude has been flowing into Asian markets through a network of ship-to-ship transfers, flag-of-convenience vessels, and falsified cargo documentation, collectively known in the industry as the shadow fleet. These vessels operate outside normal insurance and regulatory frameworks, making them largely immune to conventional sanctions enforcement. Full reinstatement of sanctions will increase the cost and risk of these operations, but it will not eliminate them entirely, meaning the supply reduction from sanctions may be smaller than the headline suggests.

Ukraine's Oil Market Footprint: The Secondary Shock

The US-China trade war is not the only macroeconomic force reshaping energy markets. The US-Iran conflict is also not the only supply disruption story active in global energy markets. Simultaneously, Ukrainian military forces have been conducting systematic drone strikes against Russian tanker vessels in the Sea of Azov, targeting fuel logistics supporting Russian military operations and attempting to economically isolate Moscow-controlled Crimea.

The downstream consequences of this campaign have been substantial. Following Russia's announcement of a ban on industrial diesel exports, US diesel futures recorded their largest single-day percentage gain in four years. This refined products shock adds a second layer of supply stress to a market already navigating crude flow disruptions from the Persian Gulf.

Why Diesel Matters More Than Most Investors Realise

Diesel is the fuel of economic activity in a way that gasoline is not. It powers freight trucks, agricultural machinery, construction equipment, and marine vessels. A diesel supply shock therefore has direct pass-through effects on goods prices across virtually every supply chain.

For energy market analysts, elevated diesel crack spreads — the premium of diesel over crude oil — serve as a leading indicator of industrial demand stress and inflationary pressure in the real economy. Russia's diesel export ban signals a significant policy shift: Moscow is now prioritising domestic fuel supply for military and civilian needs over export revenue, a characteristic behaviour of an economy under sustained wartime resource pressure.

Russia remained the world's third-largest crude oil producer in 2025, behind the United States and Saudi Arabia. A potential Ukraine war settlement could theoretically unlock Russian crude supply back into global markets, providing meaningful price relief. However, Moscow has made clear that deep Ukrainian strikes into Russian territory will not accelerate peace negotiations, reducing the probability of near-term Russian supply normalisation.

Federal Reserve Policy and the Demand Destruction Mechanism

Minutes from the Federal Reserve's June 16–17 policy meeting reveal the core tension facing US monetary policymakers. Inflationary concerns intensified through June, while labor market conditions remained stable but not robust. US unemployment benefit claims fell in the most recent reporting week, consistent with a labor market characterised as operating in a deliberate, low-velocity mode rather than actively expanding.

Federal Reserve Bank of New York President John Williams communicated that despite the renewal of Middle East hostilities, he did not anticipate a sustained rise in energy prices for the remainder of 2026. This signal is significant for two reasons:

- It suggests the Fed will not loosen monetary policy in response to geopolitically-driven energy price spikes, as policymakers view these as transitory rather than structural

- It means higher interest rates will persist, maintaining pressure on consumer borrowing costs, business investment, and ultimately oil demand growth

The mechanism here is direct: higher rates increase the cost of credit-financed purchases, from vehicles to industrial equipment, reducing the rate of oil-consuming economic activity. In a market already dealing with supply disruptions, the demand side provides the counterweight that prevents a full price breakout.

China's Demand Signal: Inflation Without Strength

China's economic profile adds further complexity. Producer price inflation in China surged to its highest level in four years in June 2026, suggesting upstream cost pressures are intensifying. However, weak domestic consumer demand means manufacturers cannot pass these cost increases through to end markets, compressing profit margins and reducing incentives for additional industrial output.

Compounding this, Typhoon Bavi, carrying winds approaching 200 kilometres per hour, was bearing down on coastal regions while parts of China were still recovering from Typhoon Maysak. Severe weather events of this magnitude disrupt port operations, manufacturing activity, and energy consumption patterns in ways that add further near-term demand uncertainty.

The next major ASX story will hit our subscribers first

Europe's Long-Term Demand Erosion: The Structural Signal Hidden in the Headlines

While near-term market attention is focused on Hormuz transit data and ceasefire status, a structurally significant development is emerging from Brussels. The European Commission has been circulating a draft proposal outlining a comprehensive package of electrification policies and funding mechanisms designed to shift a larger portion of the EU economy away from oil and gas dependency.

This matters to long-term oil price analysis because Europe represents one of the world's largest crude import markets. A successful multi-year electrification transition would systematically reduce European oil demand, shrinking one of the key demand pools that currently supports price floors. The Russia-Ukraine conflict and the US-Iran disruption have both reinforced European policymakers' motivation to reduce geopolitical energy exposure, making implementation more politically viable than in previous cycles. Consequently, crude oil price trends may face structural headwinds from European demand erosion well beyond the current conflict cycle.

Scenario Analysis: Four Price Pathways for the Next 90 Days

| Scenario | Trigger Conditions | Brent Range Estimate |

|---|---|---|

| Diplomatic Resolution | Ceasefire restored; Hormuz fully reopened; sanctions extended | $68–$74/bbl |

| Status Quo Continuation | Intermittent conflict; partial Hormuz flow; no sanctions resolution | $74–$82/bbl |

| Escalation Without Closure | Attacks expand; tanker strikes intensify; sanctions fully reimposed | $85–$95/bbl |

| Full Strait Closure | Complete Hormuz blockade; Gulf-wide military escalation | $100–$120+/bbl |

Option markets are currently pricing the Status Quo Continuation scenario as the base case, with implied volatility elevated but not at levels consistent with a systemic supply crisis. Markets are serious, but not panicking.

Key Takeaways for Investors and Energy Market Participants

The current oil market environment is genuinely unusual in its complexity. Multiple conflict theatres, a central bank policy ceiling on upside momentum, and structural demand erosion forces are all operating simultaneously. For investors and analysts attempting to navigate this landscape — including through the lens of oil markets under trade war pressures — several principles stand out:

- Geopolitical risk premiums are episodic, not structural: each military escalation generates a spike that fades as markets reassess actual physical supply impacts

- The July 17 sanctions deadline is the single most actionable near-term catalyst: watch for diplomatic signalling in the days preceding it

- Diesel crack spreads serve as the clearest real-time signal of supply stress severity: a widening spread signals genuine physical market tightness beyond headline price noise

- Shadow fleet dynamics mean Iranian supply reduction from sanctions will be partial: full elimination of Iranian crude from global markets is not a realistic outcome even under maximum enforcement

- China's demand trajectory, not Middle East supply headlines, will likely determine where oil prices settle over a six-to-twelve month horizon

- The Fed's rate posture is a structural cap on oil's upside: rate cuts would need to arrive before a sustained price recovery above $90 becomes sustainable

The broader message from current price action is that oil markets have become significantly more sophisticated in how they process geopolitical risk. The era of automatic, sustained price surges in response to Middle East conflict has given way to a more nuanced calculus that weighs physical supply reality, demand-side fundamentals, and monetary policy constraints with considerably more discipline. Indeed, the oil prices slide as US-Iran conflict clouds Hormuz reopening narrative encapsulates precisely this evolution in market behaviour.

This article is intended for informational purposes only and does not constitute financial or investment advice. Oil price forecasts and scenario analyses reflect current market conditions and analyst estimates, which are subject to rapid change. Readers should conduct their own research and consult qualified financial advisers before making investment decisions.

Want to Stay Ahead of the Next Major Resource Discovery?

While macro forces dominate oil markets, significant mineral discoveries on the ASX can deliver extraordinary returns independent of commodity price cycles — and Discovery Alert's proprietary Discovery IQ model ensures subscribers receive real-time alerts the moment such opportunities emerge. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.