July 16, 2026

The Architecture of a Global Energy Crisis: What the Strait of Hormuz Breakdown Reveals

Every decade or so, global energy markets are forced to confront a structural truth they would prefer to ignore: the entire edifice of modern industrial civilisation rests on a handful of geographic bottlenecks. The current oil prices Strait of Hormuz Iran strikes crisis is a stark illustration of this vulnerability. No single point in that system carries more weight than a narrow stretch of water between the Omani coast and the Iranian shoreline. When that corridor becomes a contested war zone, the consequences ripple outward with extraordinary speed, touching fuel prices, shipping insurance, LNG contracts, and the economic planning of governments across four continents.

The events of July 2026 are not an anomaly. They are the logical endpoint of a geopolitical fault line that energy planners have quietly acknowledged for decades while hoping it would never fully activate. It has now activated.

When big ASX news breaks, our subscribers know first

The Geographic Reality That Makes Hormuz Irreplaceable

The Strait of Hormuz is, at its narrowest point, approximately 33 kilometres wide, with usable shipping lanes considerably more constrained than that figure implies. The waterway connects the Persian Gulf to the Gulf of Oman and ultimately to the Arabian Sea, functioning as the only practical maritime exit point for the oil and gas output of Saudi Arabia, the United Arab Emirates, Kuwait, Iraq, and Qatar.

What makes this corridor uniquely consequential is the absence of any realistic alternative at equivalent scale. While the East-West Pipeline across Saudi Arabia and the Habshan-Fujairah pipeline in the UAE provide partial bypass capacity, neither can absorb the full volume of Gulf exports. Combined bypass capacity across all existing pipeline infrastructure falls well short of the approximately 17 to 18 million barrels of crude oil that move through the strait on a daily basis. The geopolitical oil price drivers at play here have been building for years.

The table below captures the scale of what is at stake:

| Commodity | Estimated Daily Volume Through Hormuz |

|---|---|

| Crude Oil | ~17–18 million barrels per day |

| LNG (Qatar) | Significant share of total Qatari export volume |

| Share of Global Oil Supply | ~20% of worldwide daily consumption |

To place this in historical context, the 1973 Arab oil embargo removed roughly 5 million barrels per day from global markets and triggered the most disruptive energy price shock of the twentieth century. A complete Hormuz closure at current throughput volumes would dwarf that figure by a factor of three or more, making it the most significant single-point supply disruption in the history of the petroleum industry.

How the Conflict Reached Its Current Intensity

The current crisis did not emerge overnight. A month-long interim ceasefire between Washington and Tehran began deteriorating as negotiations over sovereign navigation rights in the Strait of Hormuz reached an impasse. The fundamental disagreement centred on whether Iran retained the right to restrict or condition passage through what it regards as a strategically sovereign waterway.

That disagreement turned kinetic in early July 2026, when Iranian forces struck at least three commercial tankers within a 48-hour window. The targets included a Qatari LNG carrier and a Saudi crude tanker. The United States treated these strikes as a material breach of the ceasefire, formally terminating the agreement and authorising military operations.

The escalation sequence since that point has been rapid:

- U.S. forces conducted strikes on missile storage and launch facilities located on Greater Tunb Island, a strategically positioned Iranian-controlled island near the entrance to the Strait.

- Operations continued for five consecutive days, with U.S. Central Command confirming additional strike packages each day.

- Iran responded with counterstrikes against U.S. military installations in Kuwait and Bahrain.

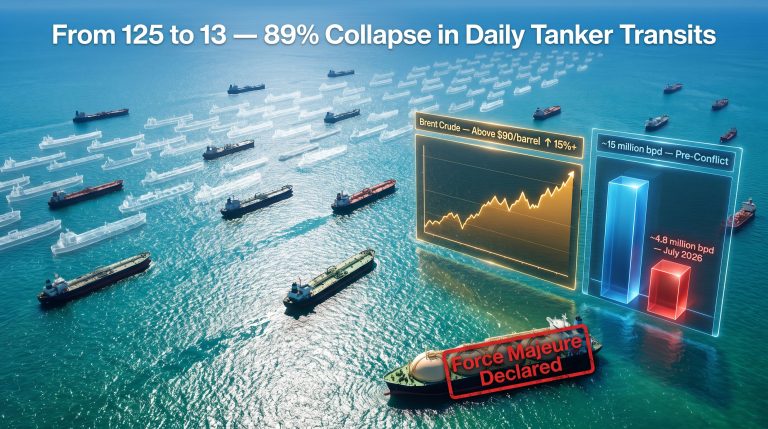

- The International Maritime Organization formally declared conditions in the Strait too hazardous for normal commercial navigation.

- Major shipping operators including Maersk suspended Hormuz transits entirely.

The negotiating positions of both parties remain deeply incompatible. Washington has stated that military operations will continue until Iran ceases attacks on commercial vessels and commits to freedom of navigation. Tehran, through the Islamic Revolutionary Guard Corps, has signalled that the Strait will remain inaccessible until U.S. strikes end and port blockades are lifted.

The IRGC's publicly stated position, relayed through Iran's Press TV, framed the regional energy corridor as a collective asset subject to collective consequences: either all parties benefit from its access, or none do. These oil market disruption risks were, furthermore, entirely foreseeable given the geopolitical trade disruptions reshaping international commerce throughout 2025 and into 2026.

The Price Response: What the Numbers Actually Show

Oil markets have responded to each escalation phase with swift repricing. Brent crude has climbed more than 13% within a single week, crossing the $85 per barrel threshold. WTI crude surged over 7.4% in a single session, reaching $72.01 per barrel. Since the conflict's origins in February 2026, cumulative price appreciation across both benchmarks has reached approximately 40%.

Both WTI and Brent futures have consequently repriced sharply, reflecting the severity of the supply disruption threat. The progression of Brent crude pricing across the conflict's key phases illustrates how each escalation has translated almost immediately into a market premium:

| Period | Brent Crude (Approx.) | Primary Trigger |

|---|---|---|

| Pre-conflict baseline (Feb 2026) | ~$60–62/bbl | Stable conditions |

| Post-ceasefire period (Jun 2026) | ~$75–78/bbl | Temporary de-escalation |

| Tanker strikes (Jul 8, 2026) | ~$80/bbl | Ceasefire collapse |

| Fifth consecutive airstrike day (Jul 15, 2026) | $85+/bbl | Sustained military operations |

The conflict has generated an estimated daily production and shipping deficit of 14.5 million barrels, a figure that reflects not only direct supply interruption but the broader chilling effect on commercial navigation across the entire Gulf region. Insurance-driven suspension of transits, even by vessels not directly threatened, compounds the volumetric disruption well beyond what military activity alone would produce.

"Brent crude has surged more than 13% in one week and approximately 40% since the U.S.-Iran conflict escalated in February 2026, driven by concerns over a sustained Strait of Hormuz closure that could effectively remove up to 20% of global oil supply from accessible markets."

Understanding the War Risk Premium in Shipping Insurance

Why Insurance Premiums Are Amplifying the Crisis

One dimension of this crisis that receives less public attention than crude price movements is the parallel collapse of commercial insurance viability for Gulf transits. War-risk insurance premiums for tankers operating in or near the Strait of Hormuz have surged to levels not recorded since the 2019 tanker incidents, which themselves represented a significant market disruption.

The mechanics of this dynamic are worth understanding clearly. War-risk insurance is a separate policy layer from standard marine insurance, applied when vessels operate in designated conflict zones. Underwriters at Lloyd's of London and other specialist markets assess these premiums based on proximity to active military operations, flag state, cargo type, and transit routing.

When the IMO issues a formal navigation advisory, as it has done for Hormuz, this is not merely a precautionary recommendation. It constitutes an institutional trigger that activates suspension clauses in commercial contracts, effectively making most Hormuz transits commercially uninsurable at economically viable premium levels. Shipowners face a binary choice: absorb catastrophic insurance costs, or suspend operations. Most have chosen the latter.

This insurance dynamic helps explain why the daily shipping deficit of 14.5 million barrels extends beyond the direct impact of military activity. The market has effectively pre-priced continued disruption into every aspect of Gulf maritime commerce.

Three Scenarios for the Strait: From Resolution to Full Escalation

Market analysts and energy strategists are currently working across three broad scenario frameworks when modelling the Hormuz crisis trajectory:

Scenario 1: Rapid Diplomatic Resolution

Probability assessments place this as the least likely near-term outcome. Under this pathway, transit resumes within weeks, Brent stabilises near the $80 level, and the geopolitical risk premium partially unwinds. Historical precedent for rapid resolution in Gulf conflicts of this nature is limited, and the current gap between U.S. and Iranian preconditions is unusually wide.

Scenario 2: Prolonged Standoff (Base Case)

The most analytically grounded scenario anticipates the Strait remaining effectively closed to commercial traffic for one to three months. Brent sustains above $85 per barrel, LNG and crude supply chains reroute at significant cost, and refinery margins in Asia and Europe compress sharply as feedstock access becomes both more expensive and less reliable.

Scenario 3: Full Escalation and Extended Blockade (Tail Risk)

This scenario, while representing the lower-probability tail, carries the most severe market implications. Analyst warnings centre on Brent potentially exceeding $100 per barrel under sustained closure conditions. Strategic petroleum reserve releases from IEA member nations would likely be triggered, but historical SPR deployments have generally served to moderate rather than eliminate price spikes. In price-sensitive emerging markets, demand destruction would begin to counteract the supply shock at some threshold below $100.

The next major ASX story will hit our subscribers first

The LNG Dimension: An Overlooked Vulnerability

How Qatari Exports Are Compounding the Crisis

Most public coverage of the Hormuz crisis focuses on crude oil flows; however, the LNG exposure deserves equal attention. Qatar is among the top three LNG exporters globally by volume, and a substantial portion of its output transits the Strait before reaching Asian and European markets. For further context, the global LNG supply outlook was already under pressure heading into 2026.

European energy buyers who pivoted toward Qatari LNG as a partial replacement for Russian pipeline gas following 2022 sanctions now face a compounded vulnerability. A geopolitical disruption has materialised in the supply chain they adopted specifically to reduce geopolitical risk. This structural irony is not lost on energy security planners across the EU.

Asian LNG spot markets are tracking upward alongside crude, with Japanese, South Korean, and Chinese buyers facing immediate supply security concerns. India, which has significantly increased Gulf crude imports in recent years, faces dual exposure across both crude and LNG procurement channels.

Downstream Consequences: What Reaches the Consumer

Refined product prices typically lag crude benchmarks by two to four weeks, meaning the full retail impact of Brent's surge above $85 has not yet fully materialised for consumers. The transmission mechanism operates as follows:

- Crude prices rise at the wellhead or loading terminal level.

- Refinery gate prices for diesel, jet fuel, and gasoline adjust within days to weeks.

- Retail fuel prices at the pump respond within two to four weeks in most markets.

- Petrochemical feedstock costs, including naphtha and LPG from Gulf producers, elevate manufacturer input expenses.

- Aviation fuel costs rise in parallel, directly compressing airline operating margins.

The petrochemical exposure is particularly relevant for Asian manufacturing economies, where naphtha-based cracking operations supply feedstock for plastics, synthetics, and intermediate chemical production across major export industries.

The Diplomacy Gap and Structural Obstacles to Resolution

Is a Ceasefire Still Possible?

President Trump publicly stated that Iran had expressed interest in renewed negotiations, a characterisation that Iranian officials had not confirmed through any official channel as of July 15, 2026. This asymmetry in diplomatic signalling is itself a structural feature of Gulf conflict resolution dynamics: back-channel interest and public posturing frequently diverge during active military phases.

Oman has historically served as a functional intermediary between Washington and Tehran, having facilitated the preliminary communications that preceded the 2015 nuclear framework discussions. Whether this channel is currently active has not been publicly confirmed, but its structural availability remains relevant to any de-escalation pathway.

Historical precedent for Gulf military conflicts of this intensity suggests resolution timelines of 30 to 60 days minimum once kinetic operations are underway. A viable de-escalation framework would logically require:

- A simultaneous ceasefire covering both military strikes and tanker attacks.

- A verifiable navigation rights agreement with defined enforcement mechanisms.

- Partial or phased modification of U.S. port blockade conditions affecting Iranian commercial shipping.

- Third-party maritime monitoring, potentially under IMO or UN mandate.

- A phased commercial shipping resumption protocol with naval escort provisions during the transition period.

None of these elements appear close to agreement based on publicly available information as of mid-July 2026.

What the Hormuz Crisis Exposes About Long-Term Energy Security

Beyond the immediate market dynamics, the current oil prices Strait of Hormuz Iran strikes confrontation forces a longer and harder conversation about the structural brittleness of the global energy system. Decades of efficiency optimisation have produced supply chains that are extraordinarily lean but correspondingly fragile when single-point dependencies are disrupted.

The Hormuz crisis is not an argument against fossil fuel use per se, but it is consequently a compelling argument for supply chain diversification, strategic reserve adequacy, and a reassessment of how much concentration risk energy-importing economies are prepared to carry. The 40% cumulative price increase since February 2026, the 14.5 million barrel daily deficit, and the commercial paralysis of one of the world's most active shipping corridors collectively represent a live stress test of energy security planning across every major importing economy.

Disclaimer: This article presents analysis based on reported events and market data as of July 15, 2026. Oil price forecasts, scenario probabilities, and geopolitical outcome projections involve significant uncertainty. Nothing in this article constitutes financial or investment advice. Commodity markets are subject to rapid change, and readers should consult qualified financial professionals before making any investment decisions.

Want to Stay Ahead of Commodity Market Shifts Driven by Geopolitical Events?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly cutting through market complexity to surface actionable opportunities — even as global energy disruptions reshape commodity valuations. Explore historic examples of major discovery returns and start your 14-day free trial at Discovery Alert to position yourself ahead of the market.