June 11, 2026

When Headlines Move Markets: The Mechanics of Oil Price Volatility in a War Economy

Energy markets have always been uniquely sensitive to political instability, but the architecture of modern crude pricing has created a system where words alone can shift billions of dollars in value within minutes. The psychological infrastructure underpinning oil futures trading means that a single sentence from a head of state carries the capacity to reverse entire sessions of price movement, override fundamental supply-demand signals, and trigger cascading reactions across correlated asset classes.

Understanding this mechanism is essential context for interpreting why oil climbs above $91 as Trump warns of new strikes against Iran, a development that encapsulates how geopolitical communication and physical market realities interact in ways that are rarely straightforward. For a broader perspective, current crude market overview data provides essential grounding for what follows.

When big ASX news breaks, our subscribers know first

The Geopolitical Pressure Valve: Understanding What Drives Oil Above $91

The crude oil market operates as a forward-looking pricing mechanism, meaning it does not merely reflect current supply and demand conditions but attempts to price in anticipated future states. This characteristic makes it extraordinarily sensitive to geopolitical developments that carry the potential to alter supply availability weeks or months ahead.

When military escalation accelerates between two parties with significant influence over critical shipping infrastructure, market participants adjust their risk premium calculations rapidly, often before any physical disruption has occurred. Furthermore, understanding the geopolitical oil pricing factors at play helps contextualise why these adjustments can be so swift and severe.

On June 10, 2026, West Texas Intermediate crude reversed an earlier session decline to settle above $91 a barrel, registering a 2.1% intraday surge driven directly by fresh statements from President Trump indicating the United States would conduct additional strikes against Iran. The significance of this reversal lies not just in the magnitude of the move, but in what it reveals about market psychology: traders had already begun pricing in the possibility of diplomatic progress, only to have that expectation dismantled within hours by escalatory communication from Washington.

How Military Escalation Between the U.S. and Iran Translates Into Crude Price Movements

The transmission mechanism between military action and oil pricing operates through several interconnected channels. The most immediate is the supply disruption channel, where actual or anticipated interference with production facilities, export terminals, or transit corridors removes barrels from accessible global supply.

Closely linked is the logistics premium channel, where the cost of routing tankers away from disrupted waterways, combined with surging war-risk insurance rates, embeds additional expense into delivered crude prices. Finally, there is the sentiment channel, where uncertainty about conflict duration and resolution translates into elevated option premiums and forward curve steepening as hedgers compete for price protection.

The June 10 session illustrated all three channels activating simultaneously. U.S. forces had attacked sites near the Strait of Hormuz, Iran responded with drone strikes against the U.S. Fifth Fleet stationed in Bahrain, and U.S. Central Command confirmed the disabling of the Palau-flagged tanker M/T Settebello in the Gulf of Oman. Each of these developments compounded the other, creating a layered supply anxiety that simple headline price movements fail to fully capture.

The Relationship Between Presidential Rhetoric and Energy Market Volatility

What makes the current conflict particularly unusual from a market dynamics perspective is the degree to which presidential communication has become an independent price-moving variable. Historically, oil markets responded primarily to verified physical events: pipeline outages, port closures, military strikes on infrastructure.

The current environment has evolved such that anticipated actions, signalled through public statements, carry comparable market weight to confirmed events. Consequently, crude oil price trends have become increasingly difficult to forecast using conventional supply-demand models alone.

Trump's June 10 statement represented a notable departure from his established rhetorical pattern. During earlier phases of the conflict, his public commentary tended to emphasise the possibility of negotiated resolution and frequently sought to cap upward price pressure by framing diplomatic progress as achievable. The shift toward language explicitly promising imminent military action against Iran disrupted the conditional pricing framework traders had built around the assumption that political incentives to lower energy costs would moderate escalation.

StoneX market analyst Fawad Razaqzada noted that crude price risks remain oriented toward the upside for as long as U.S.-Iran negotiations remain unresolved, with each fresh escalation effectively resetting the floor for near-term pricing expectations.

Why Trader Sentiment Shifts Faster Than Physical Supply Disruptions

A critical nuance in understanding oil market volatility is the asymmetry between sentiment speed and physical reality speed. Physical supply disruptions take time to manifest in inventory data, refinery throughput figures, and delivered product availability. Trader sentiment, by contrast, adjusts within seconds.

This gap creates conditions where markets can overshoot in both directions, pricing in catastrophic disruption scenarios before ground conditions warrant them, and then correcting sharply when physical supply proves more resilient than feared. According to Reuters reporting on the June 10 session, oil rose nearly 1% as U.S. strikes against Iran were launched and supply tightened simultaneously.

This dynamic helps explain a paradox central to the current conflict: despite analysts characterising the situation as the largest oil supply disruption in recorded history, crude futures were still trading more than 25% below their late-April peak by early June. Sentiment had raced ahead of reality in April, pricing in worst-case Hormuz closure scenarios. The subsequent months brought partial resilience in physical supply chains, forcing markets to unwind excessive risk premiums even as the underlying conflict remained unresolved.

What Is the Strait of Hormuz and Why Does It Hold the Global Oil Market Hostage?

No single piece of maritime geography exerts greater influence over global energy security than the Strait of Hormuz. This narrow waterway, measuring approximately 33 kilometres at its narrowest navigable point, connects the Persian Gulf to the Gulf of Oman and represents the only sea route out of the world's most hydrocarbon-dense region.

Understanding its physical characteristics and strategic significance is essential for contextualising why any credible threat to its operation triggers immediate price responses in crude markets worldwide.

A Strategic Chokepoint: The Geography That Makes the Strait Irreplaceable

The strait's irreplaceability stems from a combination of geographic confinement and the absence of viable alternative routes for the volume of oil it typically carries. While pipeline infrastructure exists to route some Persian Gulf crude overland to Red Sea and Mediterranean terminals, the total capacity of these alternatives falls dramatically short of the volumes that pass through the strait under normal conditions.

This structural bottleneck means that even partial disruption to Hormuz throughput creates supply gaps that cannot be quickly filled through other pathways, providing the waterway with what energy security analysts describe as a chokepoint multiplier effect on global price volatility.

The navigable shipping lanes within the strait are themselves constrained, with inbound and outbound traffic separated into channels only a few kilometres wide. This physical confinement creates vulnerability to relatively low-cost interdiction tactics, including naval mines, drone attacks on vessels, and seizure of commercial tankers, all of which have featured in the current conflict at various stages.

Quantifying the Risk: How Much Global Oil Supply Flows Through This Corridor?

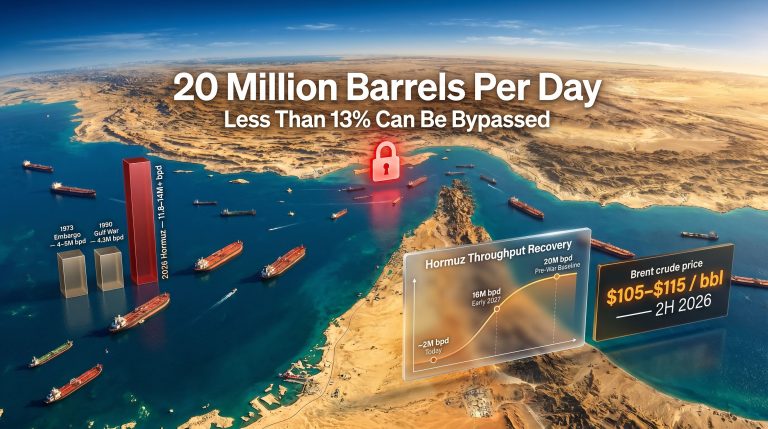

The Strait of Hormuz has historically served as a transit corridor for approximately 20% of global oil consumption and a substantial share of worldwide liquefied natural gas trade. The countries whose exports depend most heavily on the strait include Saudi Arabia, Iraq, the United Arab Emirates, Kuwait, and Iran itself, meaning that sustained closure would simultaneously affect multiple major OPEC producers.

Qatar's enormous LNG export programme also routes through Hormuz, adding a natural gas dimension to the potential supply disruption. In addition, OPEC's market influence over spare capacity decisions becomes a critical wild card in this environment, as member nations weigh competing incentives.

Trump's June 10 statement confirmed that more than 200 commercial vessels and approximately 100 million barrels of oil had exited the waterway since the commencement of what he described as a covert maritime support operation directed by his administration. The revelation that some vessels were transiting at night with navigation lights extinguished underscores the degree to which normal commercial shipping operations have been transformed into quasi-military logistics exercises under the current threat environment.

Historical Precedents: When Hormuz Tensions Have Previously Spiked Oil Prices

The strategic sensitivity of the Strait of Hormuz is not a recent discovery. During the Tanker War phase of the Iran-Iraq conflict in the mid-1980s, deliberate targeting of commercial vessels transiting Persian Gulf waters created significant insurance market disruptions and forced the deployment of naval escorts under Operation Earnest Will.

The 2019 attacks on Saudi oil processing infrastructure at Abqaiq and Khurais, while not directly targeting the strait, demonstrated how quickly markets could price in Persian Gulf supply vulnerability, with crude surging approximately 15% in a single session before partially recovering as the scale of actual supply loss became clearer.

What distinguishes the current situation from these historical episodes is both its duration and the explicit military confrontation between the United States and Iran, rather than Iranian proxy activity against third-party commercial interests. This elevates the conflict to a categorically different risk tier in the assessment frameworks used by energy market participants.

How Are Oil Markets Pricing in the U.S.-Iran Conflict Right Now?

The precise calibration of risk premiums in a market navigating between active military conflict and partial supply resilience represents one of the more analytically complex pricing challenges crude markets have faced in decades. Understanding the current pricing structure requires examining both benchmark differentials and the intraday mechanics that created the June 10 price reversal.

WTI vs. Brent: Diverging Benchmarks Under Geopolitical Stress

| Benchmark | Price (June 10, 2026) | Daily Move | Key Driver |

|---|---|---|---|

| WTI Crude | ~$90.94 to $91.00+ | +2.1% | U.S. strike warnings, inventory draw |

| Brent Crude | ~$93.89 | Elevated | Hormuz closure risk, supply rerouting |

The spread between Brent and WTI under current conditions reflects differential exposure to Persian Gulf supply risk. Brent, which serves as the pricing benchmark for internationally traded crude and is more directly connected to Atlantic Basin and Middle Eastern supply flows, carries a larger geopolitical premium. WTI, priced against U.S. domestic production hubs, is more sensitive to inventory dynamics at Cushing, Oklahoma, and domestic refinery demand patterns.

Why Crude Prices Reversed an Earlier Session Decline

The intraday reversal on June 10 from negative to significantly positive territory illustrates a pattern that has repeated throughout the conflict period: intermittent ceasefire speculation creates temporary downward pressure, which is subsequently unwound when fresh escalation signals emerge. This pattern has produced extraordinary intraday volatility, with the implied volatility term structure for crude options reflecting elevated uncertainty across all forward tenors.

The mechanics of this reversal are instructive. As Asian trading sessions wound down on June 10, market participants had tentatively positioned for the possibility of diplomatic progress, partly based on broader geopolitical signalling that had been circulating. Trump's subsequent statement eliminated that conditional assumption, triggering position unwinding and fresh directional buying that drove the 2.1% recovery from session lows.

The Role of Ceasefire Speculation in Creating Intraday Volatility

One of the more underappreciated features of the current market environment is the extent to which ceasefire speculation functions as a systematic source of volatility rather than a stabilising force. In a conventional supply disruption, such as a pipeline outage or refinery fire, the market prices a known quantity of disrupted supply and adjusts as repair timelines become clearer.

In a geopolitical conflict, however, the range of possible outcomes spans from rapid diplomatic resolution to prolonged military engagement, creating a pricing distribution with extremely fat tails in both directions. Each cycle of escalation followed by negotiation rumour and renewed escalation extends the period over which this wide distribution must be priced, keeping options markets elevated and making directional positioning increasingly costly for both producers and consumers.

How Market Participants Are Balancing Escalation Risk Against Demand Weakness

Shell Chief Executive Wael Sawan, speaking at the Wall Street Journal CEO Council in London, characterised the market as one searching for equilibrium, with pricing behaviour driven more by short-term headline events than by underlying supply and demand fundamentals, while inventories continue to be drawn down at an accelerating pace.

This observation captures a fundamental tension in current crude pricing: the physical market is tightening, as evidenced by the 7.2 million barrel weekly inventory draw and stockpiles sitting at four-month lows, but headline price levels remain substantially below where pure supply disruption analysis would place them due to demand-side headwinds. The market is simultaneously experiencing supply disruption and demand compression, creating an unusual pricing environment where conventional models perform poorly.

What Do the U.S. Crude Inventory Numbers Tell Us About the Broader Supply Picture?

Weekly crude inventory reports published by the U.S. Energy Information Administration function as one of the most closely watched barometers of physical market tightness. These reports measure actual stockpiles of crude oil held at commercial storage facilities across the United States, providing a concrete signal of whether physical supply is adequate to meet refinery demand or whether the market is structurally short of available barrels.

A 7.2 MMbbl Weekly Draw: What This Signals for the Physical Market

The 7.2 million barrel drawdown reported in the most recent weekly data represents a notably large single-week depletion, significantly above seasonal norms for the early June period. This magnitude of draw indicates that refineries were running at elevated throughput rates relative to the volume of crude being delivered to storage, either because domestic production was insufficient to replenish consumed barrels, or import flows were reduced due to Hormuz disruption, or both dynamics were operating simultaneously.

A draw of this scale carries additional significance because it compounds the cumulative inventory depletion that has occurred since the Persian Gulf conflict intensified. The multi-week trend of above-average draws has pushed total U.S. crude stockpiles to their lowest level in four months, a trajectory that, if sustained, would eventually force refineries to either reduce operating rates or pay premium prices to secure alternative supply sources.

Cushing, Oklahoma Storage Levels and Their Role as a Market Barometer

The storage hub at Cushing, Oklahoma occupies a unique position in crude oil market mechanics because it serves as the physical delivery point for WTI futures contracts. Inventory levels at Cushing therefore carry direct implications for futures pricing dynamics, particularly the relationship between spot and forward prices.

When Cushing stocks decline toward operational minimums, the structure of the WTI forward curve tends to steepen into backwardation, where near-term prices exceed forward prices, reflecting the premium placed on immediately available physical supply. The June 10 inventory data confirmed that Cushing stockpiles declined over the reporting week while remaining above operational minimum thresholds.

Why Inventories at Four-Month Lows Amplify the Impact of Geopolitical Shocks

Inventory levels function as a buffer against supply disruptions in physical commodity markets. When stocks are abundant, market participants can absorb temporary supply interruptions by drawing on stored reserves without experiencing immediate shortages or acute price spikes. Conversely, when inventories are already lean, the same supply disruption creates proportionally greater price pressure because the buffer capacity to absorb it is reduced.

The current four-month low in U.S. crude inventories therefore represents a structural amplifier for geopolitical shocks. Each fresh escalation signal from the U.S.-Iran conflict carries greater immediate price significance than it would in an environment of ample stocks, because traders understand that the physical market has less capacity to absorb incremental supply disruption without meaningful price consequences. Furthermore, the trade war impact on oil demand adds another layer of complexity to these already strained inventory dynamics.

Scenario Modelling: Three Paths Forward for Oil Prices

Constructing a credible forward price outlook in the current environment requires explicitly acknowledging the range of geopolitical outcomes that could plausibly materialise, rather than anchoring to a single base case. The following scenario framework maps distinct conflict trajectories to their most likely crude price implications, drawing on current market data and the physical supply dynamics documented above.

Scenario 1: Escalation Deepens

Under the most adverse scenario, military operations expand in scope and intensity, further disrupting commercial traffic through the Strait of Hormuz and escalating damage to energy infrastructure in the broader Persian Gulf region. Key characteristics of this pathway include:

- Hormuz access remains partially or fully restricted for an extended period

- WTI prices sustain above $90 per barrel with potential to test the $95 to $100 range

- Coordinated emergency strategic petroleum reserve releases accelerate across OECD economies

- War-risk insurance premiums for Persian Gulf tanker routes reach levels that make alternative supply sources economically necessary regardless of price

- Shipping rerouting costs around the Cape of Good Hope become embedded in refined product prices globally

Scenario 2: Negotiated Pause

A diplomatic circuit breaker, whether through direct bilateral negotiation or third-party mediation, produces a verified ceasefire and the reopening of normal commercial traffic through Hormuz. Under this pathway:

- Crude futures shed the geopolitical risk premium rapidly, with WTI potentially retreating toward $80 to $85 as traders unwind conflict positioning

- Chinese import demand recovery becomes the dominant near-term price driver as buyers who deferred purchases during the disruption return to the market

- Physical market tightness eases as Hormuz traffic normalises and Persian Gulf export flows resume at pre-conflict volumes

- Strategic reserve inventory rebuilding programmes create sustained buying support but at moderate levels

Scenario 3: Prolonged Stalemate With Managed Leakage

The most analytically interesting scenario involves a continuation of the current ambiguous state in which active conflict coexists with partial supply transit. Trump's confirmation of a covert maritime support operation, through which more than 200 commercial vessels carrying approximately 100 million barrels of oil have exited the waterway, suggests this pathway is already partially operational. Under a sustained stalemate:

- Markets oscillate in a $85 to $92 range, driven primarily by headline-to-headline sentiment swings rather than fundamental reappraisal

- The physical supply picture remains complex, with some crude volumes reaching global markets through covert logistics while visible trade data understates actual throughput

- OPEC spare capacity becomes a critical wild card, with member nations facing competing incentives between maintaining market share and capitalising on elevated prices

- Shipping intelligence services and satellite tracking data become increasingly important inputs for market participants attempting to quantify actual versus reported throughput

Disclaimer: Scenario projections involve inherent uncertainty and should not be interpreted as price forecasts. Actual crude price outcomes will depend on geopolitical, economic, and logistical variables that cannot be reliably predicted.

The next major ASX story will hit our subscribers first

Why Have Oil Prices Fallen More Than 25% From Their April Peak Despite Ongoing Conflict?

The apparent paradox of crude futures trading more than a quarter below their April highs despite an ongoing conflict described as the largest oil supply disruption in history requires careful disentanglement of the forces simultaneously pushing prices in opposite directions.

The Demand-Side Counterweight: Chinese Import Volumes at Multi-Year Lows

China represents the world's largest crude importer and the most consequential marginal demand variable in global oil markets. The reported collapse of Chinese crude imports to multi-year lows during the conflict period has provided a structural ceiling on crude price appreciation that the supply disruption alone could not overcome.

When the world's largest buyer reduces its purchasing activity dramatically, the volume of crude competing for alternative destinations increases, moderating the price impact of supply disruptions elsewhere in the system. The drivers of reduced Chinese demand are multifaceted, incorporating slower-than-anticipated economic recovery, growth in domestic electric vehicle penetration, strategic decisions to draw down previously accumulated strategic reserves, and trade flow disruptions affecting export-oriented manufacturing.

Emergency Strategic Reserve Releases and Their Price-Suppression Effect

Coordinated releases from strategic petroleum reserves held by OECD member nations represent a supply-side policy tool specifically designed to moderate the price impact of major supply disruptions. The large-scale reserve deployments referenced have injected additional supply into global markets that partially offsets the barrels removed from circulation by the Hormuz disruption.

The price-suppression effect of these releases depends on their scale relative to the supply gap, their duration, and the degree to which they are accompanied by credible signals of additional release capacity if needed.

The Paradox of a Well-Supplied Market During the Largest Supply Disruption in History

The combination of demand weakness and strategic reserve deployment has created a counterintuitive market configuration where physical crude availability appears adequate even as the structural disruption to normal supply routes is described in superlative terms. This situation reflects the market economy's capacity to route around disruptions given sufficient price signals and policy coordination, though it also creates a fragile equilibrium.

This equilibrium could be disrupted quickly if either the demand recovery accelerates or reserve release programmes are wound back prematurely. As Yahoo Finance reported during the session, oil climbed on fresh U.S. strikes, illustrating precisely how rapidly this fragile balance can shift on a single headline.

How Is the U.S. Military Involvement Reshaping Persian Gulf Energy Security?

The direct involvement of U.S. military forces in Persian Gulf operations represents a significant structural shift from the proxy-mediated conflicts and sanctions-based pressure campaigns that characterised previous phases of U.S.-Iran tension. The current direct military engagement creates a different risk calculus for market participants assessing the potential for rapid escalation or de-escalation.

U.S. Strikes on Sites Near the Strait: Tactical Goals vs. Energy Market Consequences

U.S. military strikes on facilities near the Strait of Hormuz carry dual implications that sometimes operate in opposite directions on crude prices. Tactically, strikes intended to degrade Iran's capacity to interdict commercial shipping could, if successful, reduce the probability of future supply disruptions, providing a medium-term bearish signal to crude markets.

Simultaneously, the immediate escalatory response they provoke, such as the Iranian drone strike against the U.S. Fifth Fleet in Bahrain documented in the June 10 reporting, raises the probability of near-term disruption, creating short-term bullish pressure.

The Fifth Fleet in Bahrain: Iran's Drone Response and Its Market Implications

The deployment of drone attacks against U.S. naval assets stationed in Bahrain represents a qualitative escalation from attacks against commercial shipping to direct engagement with American military infrastructure. This threshold crossing carries significant implications for conflict duration and resolution probability, as it elevates the political stakes for both parties and reduces the space for face-saving de-escalation frameworks.

From an energy market perspective, attacks on the Fifth Fleet's operational capacity carry secondary implications for the U.S. maritime support operation that has been facilitating the movement of commercial vessels through restricted waterways. Any degradation of that escort capability would directly affect the volume of crude reaching global markets through the covert transit programme confirmed by Trump on June 10.

The M/T Settebello Incident: How Tanker Interdictions Affect Oil Shipping Risk Premiums

The U.S. Central Command's disabling of the M/T Settebello, a Palau-flagged oil tanker, in the Gulf of Oman introduced a new dimension of complexity to Persian Gulf shipping risk assessments. When a vessel operating under the flag of a neutral third country becomes subject to military interdiction, it signals that the geographic scope of conflict-related maritime risk extends beyond the strait itself to the broader Gulf of Oman approaches.

This geographic expansion of risk directly affects the insurance market's pricing of war-risk coverage for tankers operating anywhere in the region. War-risk premiums, which are typically quoted as a percentage of vessel value per voyage, escalate rapidly when new incidents demonstrate that previously assumed safe transit corridors are subject to military action. These premium increases translate into higher delivered crude costs, effectively functioning as an additional price layer on top of commodity price movements visible in futures markets.

What Does Trump's Escalatory Rhetoric Mean for Oil Price Forecasting?

Presidential communication has always influenced energy markets, but the current conflict has elevated the market-moving significance of executive rhetoric to an unprecedented degree. Understanding how to interpret Trump's statements within the context of oil price forecasting requires distinguishing between communication patterns, policy signals, and the gap between stated intent and operational reality.

Departing From the Pattern: Why "Hit Iran Hard Again" Signals a Policy Shift

Trump's June 10 statement represented an explicit departure from his established pattern of balancing military pressure with rhetorical emphasis on the possibility of negotiated resolution. Throughout his previous tenure and the early phases of the current conflict, his public statements tended to emphasise deal-making possibilities, partly reflecting genuine interest in diplomatic resolution and partly reflecting awareness that prolonged conflict is inflationary for American consumers through elevated fuel costs.

The shift toward explicitly promising additional strikes, without specifying targets or diplomatic conditions for cessation, suggests either a strategic recalibration toward maximum pressure or a tactical communication choice designed to extract specific concessions from Tehran. Market participants, unable to determine which interpretation is correct, responded by pricing in the more adverse scenario: prolonged conflict with reduced probability of near-term resolution.

Presidential Communication as a Market-Moving Variable

The degree to which individual presidential statements move oil markets reflects both the structural significance of the conflict and the absence of credible independent information sources that might arbitrage away the information advantage implied by executive communication. In a conflict where covert maritime operations are underway and the true state of Hormuz throughput is obscured by lights-out shipping, presidential disclosure represents a primary information source for market participants seeking to assess actual physical supply conditions.

How Traders Are Interpreting the Gap Between Negotiation Rhetoric and Military Action

Experienced energy traders understand that the gap between negotiation rhetoric and military action is itself a market signal. When de-escalation language is followed quickly by escalatory operations, it reduces the credibility weight traders assign to subsequent de-escalation signals, effectively making each positive diplomatic statement worth less in market terms than the previous one.

This credibility erosion dynamic means that genuine diplomatic progress, when it occurs, may initially be discounted by markets that have adapted to treating positive signals as noise.

Comparing Oil Price Responses: Current U.S.-Iran Conflict vs. Historical Middle East Crises

Contextualising the current crude price response within the historical record of Middle Eastern supply disruptions reveals both the unprecedented nature of the current event and the equally unprecedented set of counterbalancing forces that have moderated its price impact.

| Event | Peak Price Impact | Duration of Spike | Key Supply Route Affected |

|---|---|---|---|

| 1973 Arab Oil Embargo | +400% over months | ~6 months | Global tanker routes |

| 1990 Gulf War | +100% spike | ~6 weeks | Persian Gulf |

| 2019 Abqaiq Attacks | +15% intraday | 2 to 3 days | Saudi export terminals |

| 2026 U.S.-Iran Conflict | -25% from April peak despite disruption | Ongoing | Strait of Hormuz |

Why the 2026 Disruption Has Produced a Counterintuitive Price Trajectory

The table above captures a striking anomaly: despite the current conflict being characterised as the most significant supply disruption in recorded history, its net price impact over the period from April to June 2026 has been negative. This outcome reflects the convergence of several demand-side and policy factors that have no historical precedent operating simultaneously at this scale.

The 1973 embargo occurred in an environment of tight global supply capacity with no meaningful strategic reserve infrastructure. The 1990 Gulf War disrupted supply from two large producers simultaneously but left the Hormuz corridor itself functional for other regional producers. The 2026 conflict is structurally different in that it simultaneously creates supply disruption through Hormuz interdiction while encountering demand weakness from China, coordinated reserve releases, and partial covert supply transit that prevents a complete supply cutoff.

The Role of Non-OPEC Supply Growth in Cushioning Geopolitical Shocks

A structural factor that distinguishes the current market from previous disruption episodes is the substantial growth in non-OPEC production, particularly from U.S. shale, over the intervening decades. The U.S. transformed from a significant net crude importer to a position of domestic production sufficiency during the shale revolution, reducing the direct vulnerability of American consumers to Persian Gulf supply disruptions.

This structural shift means that the global oil market now has a degree of supply diversification that did not exist during the 1973 or 1990 crises, providing a cushion against the most extreme price outcomes even in the context of significant Persian Gulf disruption.

Frequently Asked Questions: Oil Prices, Iran, and the Strait of Hormuz

Why did oil prices rise above $91 following Trump's Iran strike warning?

Crude markets registered a 2.1% intraday gain on June 10, 2026, after President Trump publicly stated that the U.S. would conduct additional military strikes against Iran. The statement signalled that diplomatic resolution remained distant, reducing the probability of a near-term Hormuz reopening. Combined with a large weekly U.S. crude inventory draw of 7.2 million barrels, the market interpreted the signal as pointing toward sustained or worsening supply constraints.

What is the Strait of Hormuz and why does it matter for oil prices?

The Strait of Hormuz is the world's most strategically significant maritime energy transit corridor, connecting the Persian Gulf to the Gulf of Oman and the broader global shipping network. Historically, it has carried approximately 20% of global oil consumption in tanker shipments. Any sustained restriction of traffic through this narrow waterway threatens to remove millions of barrels per day from accessible global supply, creating immediate and significant upward pressure on crude benchmarks.

How low are U.S. crude oil inventories right now?

As of the reporting week ending in early June 2026, U.S. crude inventories fell by 7.2 million barrels, bringing national stockpiles to their lowest point in four months. The storage hub at Cushing, Oklahoma also experienced a decline, though it remained above operational minimum levels. This tightening trend reflects the ongoing effort by global buyers to source replacement barrels for volumes displaced by Persian Gulf supply chain disruption.

Could oil prices reach $100 per barrel?

Under an escalation scenario where Hormuz access deteriorates materially from current conditions, upside risks to crude forecasts remain substantial. However, the combination of weakened Chinese import demand, coordinated strategic reserve deployments, and partial covert supply transit has so far acted as a structural ceiling preventing prices from sustaining above the $95 threshold. This does not constitute a price forecast and should not be relied upon for investment decisions.

Why are oil prices still below their April 2026 peak despite ongoing conflict?

Crude futures declined more than 25% from their late-April peak due to the simultaneous operation of several counterbalancing forces: a significant reduction in Chinese crude import volumes to multi-year lows, large-scale coordinated releases from strategic petroleum reserves across major consuming nations, and the continued movement of crude volumes through the strait via the covert maritime operation confirmed publicly by Trump on June 10, 2026.

Key Takeaways: What the Oil Market Is Really Telling Us

- The geopolitical risk premium is real but fragile: Crude prices respond sharply to escalation signals but are equally sensitive to any diplomatic opening, creating extraordinary intraday volatility that rewards neither directional traders nor long-term hedgers

- Physical supply is tighter than headline prices suggest: A 7.2 million barrel weekly draw and four-month inventory lows indicate structural tightening beneath the surface of a headline price that appears to have stabilised

- The Strait of Hormuz remains the single most critical variable for near-term crude price direction, and any verified change in its operational status would immediately reset the pricing framework markets are currently operating within

- Demand-side headwinds from China are providing a structural ceiling that limits how far geopolitical fear alone can push prices, creating a market that is simultaneously underpriced on supply disruption metrics and fairly priced when demand weakness is incorporated

- Covert maritime operations have partially offset supply disruption in ways that are difficult to track through conventional trade data, adding analytical complexity to oil market modelling that relies on visible flow statistics

- Presidential rhetoric functions as an independent price signal, with the credibility weighting assigned to de-escalation statements declining over time as the gap between diplomatic language and military action widens

This article is intended for informational purposes only and does not constitute financial advice. Crude oil markets involve significant risk and price volatility. Forward-looking statements and scenario analyses involve uncertainty and should not be relied upon as forecasts of actual market outcomes.

Want to Stay Ahead of the Next Major Resource Discovery Amid Market Volatility?

While geopolitical shocks continue to reshape energy and commodity markets, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and delivering actionable insights to subscribers before the broader market reacts — explore historic discovery returns to understand the opportunity, or begin your 14-day free trial today to position yourself ahead of the next major find.