May 16, 2026

When Chokepoints Become Crisis Points: The Hormuz Oil Price Shock Explained

Few mechanisms in global energy markets are as poorly understood by the general public as the relationship between maritime chokepoints and crude oil pricing. Most observers assume that prices rise only when physical supply is cut off. In reality, the financial markets that underpin crude oil pricing are forward-looking instruments that respond to probability shifts, not just confirmed events. The Strait of Hormuz sits at the intersection of this dynamic more acutely than any other geographic feature on the planet, and the escalating breakdown in US-Iran relations during May 2025 has placed this reality into sharp focus.

Understanding why oil prices on US-Iran tensions and Strait of Hormuz closure fears have surged requires moving beyond headlines and into the mechanics of how energy markets actually process geopolitical risk. Furthermore, the role of crude oil geopolitics in shaping futures pricing has rarely been more visible than it is today.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Carries Irreplaceable Strategic Weight

The physical geography of the Strait of Hormuz is deceptively simple: a narrow passage roughly 33 kilometres wide at its tightest navigable point, separating Iran from the Omani exclave of Musandam. Yet this narrow corridor carries a disproportionate share of the world's most critical commodity.

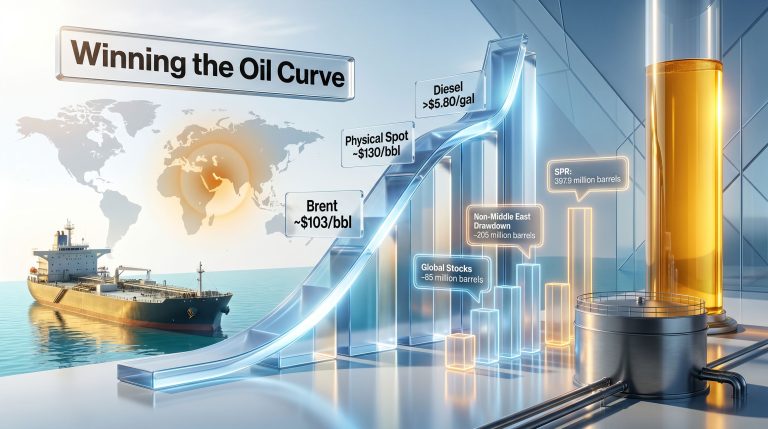

Under normal operating conditions, approximately 20% of the world's combined oil and liquefied natural gas supply moves through this passage. The primary exporters routing through the strait include Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar, the latter being one of the world's largest LNG producers. Before the current conflict disrupted traffic, an estimated 140 vessels per day transited the strait, a figure that captures tankers, LNG carriers, and support vessels collectively.

No viable alternative exists at equivalent scale. The Abqaiq-Yanbu pipeline in Saudi Arabia and the Iraq-Turkey pipeline provide partial bypass capacity, but their combined throughput falls well short of replacing full Hormuz volume. A confirmed closure does not merely redirect trade flows; it eliminates them for the economies most dependent on Gulf supply.

The Volume Gap Between Normal and Disrupted Conditions

The scale of the current disruption becomes stark when placed in direct comparison:

| Metric | Pre-Crisis Baseline | Current Disrupted State |

|---|---|---|

| Daily vessel transits | ~140 ships/day | 10–30 ships/day (estimated) |

| Global oil and LNG share at risk | ~20% | Partially constrained |

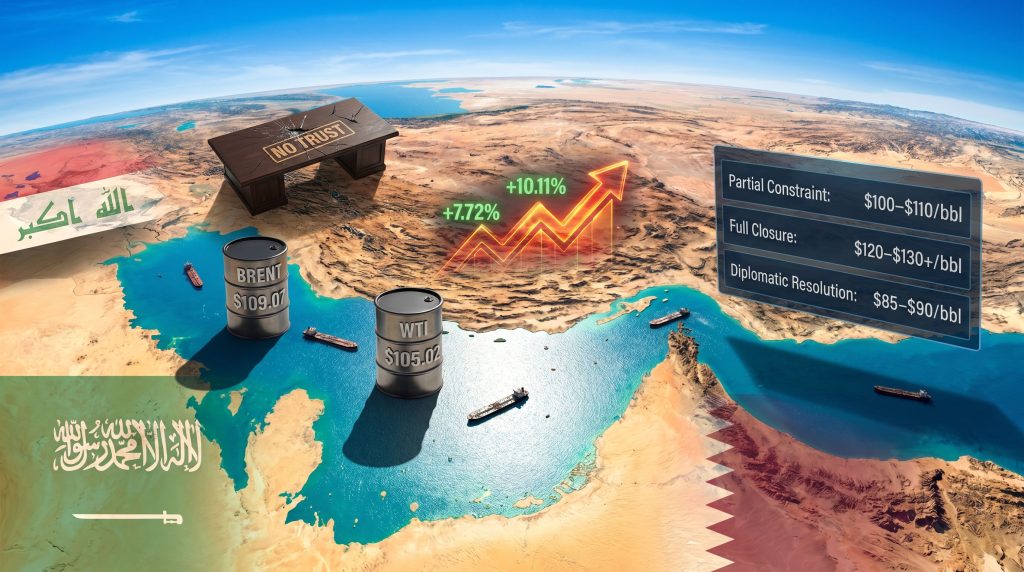

| Brent crude price range | ~$80–85/bbl | $109.07/bbl (recent high) |

| WTI crude price range | ~$75–80/bbl | $105.02/bbl (recent high) |

| Weekly Brent price increase | Baseline | +7.72% |

| Weekly WTI price increase | Baseline | +10.11% |

Shipping analytics firm Kpler reported that 10 vessels transited the strait within a single 24-hour period, compared with the five to seven daily crossings recorded in the preceding weeks. Iran's Revolutionary Guard separately reported that 30 vessels crossed between Wednesday evening and Thursday, a figure that, if accurate, represents a meaningful but still dramatically reduced throughput relative to the pre-war norm.

Key Market Insight: Even a partial reduction in Strait of Hormuz vessel traffic is sufficient to generate substantial upward pressure on global crude benchmarks. The psychological risk premium embedded in futures pricing can move markets well before any confirmed physical supply shortage materialises. This distinction between sentiment-driven pricing and balance-sheet disruption is critical for understanding current crude price behaviour.

The Diplomatic Collapse Driving Crude Price Escalation

The oil market's reaction to the current crisis is not primarily a response to physical events. It is a response to the collapse of confidence in a diplomatic resolution pathway. Indeed, oil prices jumped sharply when US-Iran talks broke down, underlining how quickly sentiment can shift when diplomatic channels close.

Commerzbank analysts characterised the situation by noting that the tone between the US and Iran had become significantly more confrontational, and that while the ceasefire remained technically in place, expectations for a rapid reopening of the strait had effectively evaporated. This framing captures the core market dynamic: traders are not pricing in a confirmed closure; they are pricing in the disappearing probability of a managed reopening.

Iran's Foreign Minister Abbas Araqchi stated publicly that Tehran holds no trust in the United States as a negotiating partner, and that engagement would only be considered if Washington demonstrated genuine seriousness. Simultaneously, President Trump indicated his patience with the pace of talks was running thin, a rhetorical signal that commodity markets interpreted as raising the probability of renewed military engagement.

The US-China Dimension: Limited Relief, Reshaped Trade Flows

The Trump-Xi summit introduced a variable that briefly tempered market anxiety before proving insufficient to shift the fundamental price trajectory. Both leaders reportedly aligned on the position that Iran cannot be permitted to acquire nuclear weapons and that the Hormuz passage must be reopened. China's foreign ministry characterised the conflict as one that has no reason to continue, language that signals Beijing's preference for de-escalation without committing to any enforcement mechanism.

Trump also indicated that China had expressed interest in purchasing US oil directly, a development that could meaningfully reshape Atlantic Basin energy trade flows if sustained. However, markets assessed the summit outcome as falling well short of any concrete mechanism to accelerate a Hormuz reopening, limiting any downside correction in current crude prices.

Vandana Hari, founder of oil market analysis provider Vanda Insights, described the market's attention as firmly fixed on the strategic deadlock, with traders now incorporating a tail risk of renewed military escalation into their pricing rather than treating diplomacy as a credible near-term resolution mechanism.

How the Risk Premium Actually Works in Practice

One of the least understood aspects of geopolitical oil price spikes is the mechanics of the risk premium itself. Unlike physical supply shortfalls, which affect the actual barrel-by-barrel balance of the oil market, a geopolitical risk premium is a forward-looking probability adjustment embedded into futures prices.

Risk Premium Explained: When a critical supply chokepoint faces a credible threat of disruption, futures traders adjust contract prices upward to reflect the probability-weighted cost of a supply shock occurring before the contract expires. Crucially, the actual disruption does not need to materialise. A deterioration in diplomatic signals, a hostile statement from a key political figure, or a reduction in ceasefire confidence is sufficient to expand this premium. As resolution prospects improve, the premium contracts. This is why crude prices can move 3–6% on a single day of geopolitical news without a single additional barrel being removed from the market.

PVM analyst Tamas Varga captured this distinction precisely, noting that the gradual increase in vessel transits through the strait was having a more tangible effect on market sentiment than on the actual physical oil balance. For now, the disruption remains primarily a sentiment story with physical supply implications growing on the margin.

The Depleted Safety Buffer: Why This Crisis Is Structurally Different

The current Hormuz disruption does not exist in isolation. It is unfolding against a backdrop of historically depleted oil safety reserves, a condition that amplifies the market's sensitivity to every diplomatic signal and vessel transit count. This dynamic, combined with the broader impact of trade war oil prices on global supply chains, is compressing the market's capacity to absorb further shocks.

Phil Flynn, senior analyst at Price Futures Group, assessed the situation by noting that the world had consumed its oil safety buffer at a historically unprecedented rate. Strategic petroleum reserve releases and demand-side adjustments had prevented immediate supply chaos, but the margin for absorbing a prolonged disruption was shrinking rapidly. A sustained Hormuz closure now points directly toward tighter physical markets, refined product shortages, and sustained upward price pressure across the coming months.

This structural depletion of reserve buffers distinguishes the current episode from prior Hormuz tension events:

- 2019 Gulf of Oman tanker attacks: Produced sharp but short-lived price spikes because SPR buffers were substantially intact and the escalation risk was assessed as contained.

- 1980–1988 Iran-Iraq Tanker War: Sustained elevated risk premiums without triggering a full closure, but global spare capacity was significantly higher relative to demand.

- 2025 conflict context: SPR reserves across IEA member nations have been drawn down substantially since 2022. OPEC+ spare capacity, while present on paper, cannot be rapidly deployed at the scale required to compensate for a Hormuz closure.

Saxo Bank analyst Ole Hansen added a second compounding factor to the current price environment: ongoing Ukrainian strikes on Russian refinery infrastructure are simultaneously constraining refined product output from a second major supply source. The convergence of Middle East maritime disruption with European refinery capacity reduction creates a multi-vector risk environment that amplifies price sensitivity to each incremental escalation event.

Scenario Analysis: Oil Price Pathways Under Different Hormuz Outcomes

The range of plausible outcomes from the current standoff spans a wide price band, depending on the diplomatic and military trajectory over the coming weeks.

| Scenario | Brent Crude Range | Near-Term Probability | Key Trigger |

|---|---|---|---|

| Partial Constraint Continues (Base Case) | $100–$110/bbl | Elevated | Diplomatic stalemate persists |

| Full Strait Closure (Tail Risk) | $120–$130+/bbl | Low-moderate | Military re-engagement |

| Diplomatic Breakthrough | $85–$90/bbl | Low (near-term) | Verified ceasefire plus strait reopening |

Scenario 1: Partial Constraint as the Base Case

Vessel traffic remains in the 10–30 ship per day range with intermittent fluctuations. Brent crude sustains levels above $100 per barrel. Refined product prices rise in import-dependent markets, particularly for gasoline and diesel in Asia and Europe. Global inflationary pressures intensify, creating secondary economic drag in energy-importing economies.

Scenario 2: Full Closure as the Tail Risk

A confirmed cessation of maritime traffic would represent a supply shock of historic proportions. Brent crude could breach $120–$130 per barrel within days of a confirmed full closure. Emergency SPR releases across IEA member nations would likely follow, but given current reserve depletion levels, their capacity to absorb the shock is more limited than in previous crises. Downstream shortages in refined products would compound the primary crude price impact within weeks. OPEC market influence in such a scenario would face its most significant test in decades.

Scenario 3: Diplomatic Breakthrough

A verifiable agreement on maritime security and nuclear programme constraints would trigger a meaningful risk premium unwind. Brent crude could correct toward $85–$90 per barrel as the probability-weighted disruption cost is removed from futures pricing. China's reported interest in purchasing US oil could further reshape Atlantic Basin trade flows as a secondary market development.

The next major ASX story will hit our subscribers first

Which Regions Face the Greatest Exposure

The geographic distribution of Hormuz dependency creates uneven vulnerability across global economies.

Asia-Pacific: The Highest-Dependency Region

- China, India, Japan, and South Korea collectively represent the dominant share of Gulf crude imports transiting through the strait.

- India sources a substantial proportion of its crude requirements from Gulf producers, making it acutely exposed to both price increases and physical supply constraints.

- Japan and South Korea have virtually no domestic hydrocarbon production at scale, making their energy security almost entirely contingent on unobstructed maritime access through Hormuz.

Europe: Indirect but Compounding Exposure

- European refiners are simultaneously managing reduced Russian crude availability alongside elevated Hormuz risk premiums.

- Qatar's LNG exports, which transit through the strait, directly affect European gas markets that remain structurally tight following the post-2022 supply restructuring.

United States: Producer Beneficiary, Consumer Risk

The US occupies a paradoxical position. As a net crude exporter, elevated oil prices on US-Iran tensions and Strait of Hormuz closure dynamics benefit domestic producer economics. However, US gasoline prices remain sensitive to global crude benchmarks, creating consumer-side inflationary pressure that creates political risk for the administration. A prolonged crisis also accelerates the strategic case for US LNG and crude exports to Asian markets actively seeking Hormuz-independent supply alternatives.

The Long-Term Energy Security Lesson Taking Shape

Beyond the immediate price dynamics, the current crisis is generating a deeper strategic conversation about the structural fragility of chokepoint-dependent energy supply chains. Consequently, the Hormuz episode is already accelerating investment interest in several alternative supply security mechanisms:

- LNG import terminal diversification in Japan, South Korea, and India to reduce dependence on single-origin supply corridors.

- Pipeline infrastructure expansion providing partial bypass capacity for Gulf producers.

- Strategic petroleum reserve rebuilding programmes across IEA member nations following the drawdowns of 2022–2024.

- Renewable energy acceleration framed explicitly as a national security hedge against fossil fuel chokepoint dependency.

Broader Strategic Implication: The Hormuz crisis is providing a concrete, quantifiable illustration of the argument that energy transition investment is simultaneously a national security investment. Every percentage point of domestic renewable generation capacity that an importing nation develops reduces its exposure to the price volatility that geopolitical disruptions at maritime chokepoints generate. This framing is increasingly influencing policy conversations in Tokyo, Seoul, New Delhi, and Brussels.

Frequently Asked Questions: Hormuz, Oil Prices, and the US-Iran Standoff

What share of global oil supply transits the Strait of Hormuz?

Approximately 20% of the world's combined oil and LNG supply moves through the strait under normal conditions, making it the single most strategically significant energy corridor on the planet.

How much have crude prices risen during the current escalation?

Brent crude rose approximately 7.72% over the week of escalation, reaching $109.07 per barrel. WTI gained 10.11% over the same period, reaching $105.02 per barrel. Single-day moves of 3–6% were recorded on days of significant diplomatic deterioration. The oil prices on US-Iran tensions and Strait of Hormuz closure concerns have driven some of the sharpest weekly moves seen in crude markets in recent years.

Can the strait be bypassed if fully closed?

Partial bypass options exist through the Abqaiq-Yanbu pipeline in Saudi Arabia and the Iraq-Turkey pipeline, but combined capacity falls well short of replacing full Hormuz throughput. A complete closure would create unavoidable supply shortfalls, particularly for major Asian importers.

What do war risk insurance premiums indicate about market expectations?

War risk insurance premiums for tankers transiting the Gulf have risen sharply during the current crisis. Some operators are actively rerouting vessels via the Cape of Good Hope, which adds approximately 10–15 days to voyage times and significantly increases freight costs, effectively embedding a supply disruption premium into delivered crude prices even before any physical shortage occurs.

Disclaimer: This article contains forward-looking scenario analysis and market commentary intended for informational purposes only. Crude oil price forecasts and geopolitical risk assessments involve significant uncertainty. Nothing in this article constitutes financial or investment advice. Readers should conduct their own research and consult qualified financial professionals before making investment decisions.

Want to Stay Ahead of the Next Major Resource Discovery Driven by Global Commodity Shifts?

When geopolitical shocks like the Hormuz crisis send commodity markets into sharp relief, the biggest opportunities often emerge in the ASX exploration and mining sector — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment a significant mineral discovery hits the exchange, turning complex market signals into actionable investment insights. Explore how historic discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to ensure you're positioned ahead of the broader market.