May 14, 2026

When Central Banks and Geopolitics Collide: Decoding the Forces Pulling Oil Lower

Few market conditions are more disorienting for energy traders than the one unfolding across global crude benchmarks in mid-2026. For much of the past decade, oil price direction could be reasonably tracked by monitoring a single dominant variable, whether that was OPEC supply discipline, US shale output, or Chinese import volumes. What the current environment presents is something structurally different: a collision between two powerful and opposing forces, monetary policy tightening on one side and geopolitical supply risk on the other.

When these forces operate simultaneously and in opposite directions, the result is not a clear price trend but a volatile, range-bound market prone to sharp reversals within the same trading session. Understanding why oil settles lower on US rate hike fears and Trump-Xi meeting uncertainty requires looking beyond the daily headline and into the architecture of the pressures underneath. For a broader view of where markets have been heading, the crude oil price trends of recent months provide essential context.

When big ASX news breaks, our subscribers know first

The Two Forces Compressing Crude Oil in 2026

Monetary Tightening and Its Slow Demolition of Demand Forecasts

Boston Federal Reserve President Susan Collins signalled on May 14, 2026 that further interest rate increases could be necessary if inflation pressures fail to moderate, a statement that landed with particular weight given the inflation data surrounding it. US producer prices in April 2026 recorded their steepest monthly rise in four years, driven by sharply higher costs across goods and services categories. That followed a second consecutive monthly surge in US consumer prices, producing the largest annual inflation increase in nearly three years.

For oil markets, the Fed's messaging operates through a distinct transmission chain that traders price in real time, well before the underlying economic effects materialise:

- Rate hike signals raise borrowing costs across business and consumer credit

- Industrial capex contracts, slowing energy-intensive manufacturing output

- Consumer discretionary spending compresses, including vehicle fuel consumption

- A stronger US dollar makes dollar-denominated commodities more expensive for international buyers, softening import demand

- Growth forecasts are revised downward, pulling forward oil demand projections with them

The critical dynamic here is that oil markets do not wait for rate hikes to take effect. Expectations alone reprice futures curves, meaning the demand destruction is priced in months before it actually arrives.

There is also a structural paradox embedded in this cycle. Elevated crude prices feed directly into transport costs, manufacturing inputs, and food production logistics, all of which accelerate broader consumer price inflation. That inflation, in turn, intensifies pressure on the Federal Reserve to tighten further. The result is a self-limiting mechanism: oil-driven inflation eventually generates the monetary conditions that suppress the very demand underpinning high prices.

| Monetary Condition | Impact on Oil Demand | Market Effect |

|---|---|---|

| Rate hike signals | Slower economic growth anticipated | Demand-side futures sell-off |

| Elevated consumer inflation | Reduced household purchasing power | Fuel consumption contraction |

| USD strengthening | Oil more expensive for non-US buyers | Import demand softens globally |

| Higher business borrowing costs | Industrial output slows | Energy-intensive activity contracts |

Geopolitical Risk Premium: The Supply-Side Floor That Won't Collapse

While monetary tightening is building a ceiling on oil price rallies, the geopolitical environment is simultaneously constructing a structural floor. The ongoing conflict between the United States and Iran has produced a supply disruption scenario centred on one of the most consequential maritime chokepoints on earth.

The Strait of Hormuz, the narrow passage between Iran and Oman, carries an estimated 20 to 21 million barrels of oil per day, representing approximately one-fifth of all global seaborne petroleum trade. Iran has progressively tightened its operational grip over Hormuz-adjacent maritime zones as the conflict has escalated, and US-Iran ceasefire negotiations have stalled after the Trump administration rejected Tehran's most recent proposal as unacceptable.

On May 14, 2026, a further layer of regional tension emerged when Iran's Foreign Minister Abbas Araqchi stated publicly that Kuwait had unlawfully attacked an Iranian vessel and detained four Iranian citizens in the Gulf, with Tehran formally reserving the right to respond. US Vice President JD Vance, separately, indicated that some progress was being made in negotiations with Iran, though no agreement had been reached. Oil prices slipping amid these Iran tensions have become a recurring theme throughout this period.

These developments illustrate a broader pattern: every diplomatic signal, whether positive or negative, is capable of moving oil prices by several dollars in either direction within a single session.

What Actually Happened to Brent and WTI on May 14, 2026

The settlement data for Wednesday, May 14, 2026 tells a story of macro forces overwhelming fundamental supply signals:

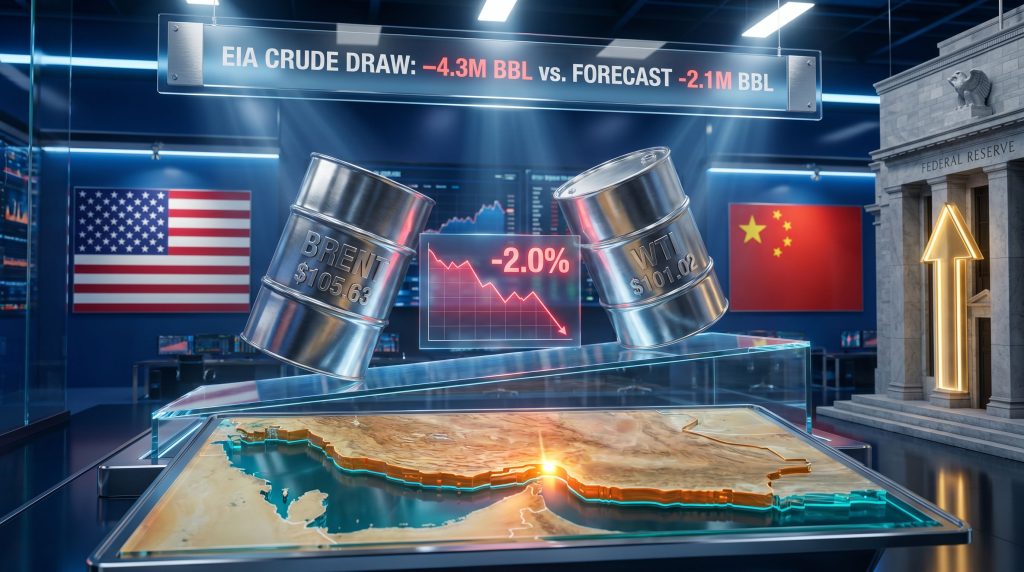

- Brent crude futures closed down $2.14 per barrel, a decline of 2.0%, settling at $105.63 per barrel

- US West Texas Intermediate (WTI) fell $1.16 per barrel, or 1.14%, closing at $101.02 per barrel

This came just one session after both benchmarks had surged more than 3% as hopes for a durable US-Iran ceasefire faded and Hormuz closure risk intensified. The speed of the reversal underscores a pattern that has defined oil trading throughout the 2026 conflict period: sentiment can shift entirely within 24 hours when competing variables are this evenly matched. Furthermore, the current crude market overview illustrates just how compressed these trading ranges have become.

Why a Larger-Than-Expected Inventory Draw Failed to Sustain Prices

The US Energy Information Administration released its weekly petroleum status data on the same day, and on the surface, the figures were unambiguously bullish:

| Product | Actual Weekly Change | Analyst Consensus | Variance |

|---|---|---|---|

| Crude Oil | -4.3 million barrels | -2.1 million barrels | -2.2M bbl (bullish surprise) |

| Gasoline | -4.1 million barrels | -2.9 million barrels | -1.2M bbl (bullish surprise) |

| Distillates | +0.2 million barrels | -2.7 million barrels | +2.9M bbl (bearish surprise) |

Crude stocks fell more than double the anticipated drawdown. Gasoline inventories also declined well beyond expectations. The data briefly lifted futures, but the recovery could not be sustained. Distillate inventories, covering diesel and heating oil, rose against expectations of a significant draw, introducing a bearish counterweight. More importantly, the macro narrative surrounding Federal Reserve hawkishness and slowing demand growth proved more durable as a price driver than a single week of supply-side tightness.

This is a recurring dynamic in commodity markets under monetary tightening conditions: even genuinely bullish physical data struggles to anchor prices when forward demand expectations are deteriorating in real time.

The Trump-Xi Summit: An Indirect Lever on Global Oil Supply Chains

US President Donald Trump arrived in Beijing on Wednesday, May 14, 2026, with meetings with Chinese President Xi Jinping scheduled for Thursday and Friday. The summit carried direct relevance for global oil markets across three interconnected dimensions. Indeed, the US-China oil tensions running beneath the surface of these diplomatic events have been reshaping market expectations throughout 2026.

1. Chinese Purchases of Iranian Crude

China is the world's largest importer of crude oil and remains the primary destination for sanctioned Iranian barrels despite sustained pressure from the Trump administration to reduce these purchases. Any shift in Beijing's procurement posture, whether negotiated or coerced, would materially alter the effective supply available to global markets.

2. US Energy Export Commitments

The Trump administration has pursued expanded Chinese purchases of American LNG and crude as a trade-balancing mechanism. Commitments in this area would have measurable consequences for US export volumes and domestic energy market dynamics.

3. Hormuz and Iranian Sanctions Enforcement

Washington's ability to apply meaningful pressure on Tehran through export restrictions is structurally limited by China's continued absorption of Iranian oil. The summit represents a critical diplomatic venue for aligning enforcement postures, though no confirmed agreements had been reached as of the session's close.

Trump notably stated the day before landing in Beijing that he did not believe Chinese assistance would be necessary to resolve the Iran conflict, a signal that complicated the diplomatic atmosphere ahead of the formal bilateral meetings.

Why China's Oil Market Role Creates Structural Complexity for US Foreign Policy

China's position as the dominant consumer of sanctioned Iranian crude is not simply a bilateral trade issue. It fundamentally limits the coercive reach of US energy sanctions as a geopolitical instrument. When the primary intended market for restricted oil barrels remains fully accessible through a major competing power, the economic pressure intended to modify behaviour is significantly diluted.

This dynamic places the Trump-Xi summit at the intersection of trade diplomacy, sanctions enforcement, and energy market architecture, making it consequential for oil traders regardless of whether any formal energy-specific commitments are announced. Consequently, the broader trade war impact on oil extends well beyond tariff headlines into the structural mechanics of global energy flows.

Structural Tightness: The Underlying Architecture Holding Prices Above $100

Despite the day's decline, energy market analysts note that the physical supply environment remains fundamentally constrained. Rystad Energy analyst Janiv Shah indicated that meaningful structural tightness in global oil markets is likely to persist for at least the remainder of 2026, driven by ongoing Middle East supply disruptions and limited capacity expansion elsewhere.

Several reinforcing supply-side constraints are operating simultaneously:

- Hormuz disruption risk maintains a persistent geopolitical premium on Brent pricing, with an estimated $8 to $12 per barrel embedded in current valuations

- OPEC revised its 2026 global oil demand growth forecast downward on May 14, reflecting the combined headwinds of rate-driven demand softening and war-related economic disruption

- The International Energy Agency assessed that global oil supply would be insufficient to meet total demand in 2026, with Middle East production losses as the primary constraint

- The Iran-Kuwait maritime incident introduced a new bilateral tension into an already fragile Gulf security environment

| Risk Factor | Estimated Price Premium | Outlook Duration |

|---|---|---|

| Strait of Hormuz disruption risk | $8-$12/bbl | Ongoing, conflict-dependent |

| Iranian sanctions enforcement gap | $4-$6/bbl | Medium-term (6-12 months) |

| OPEC production discipline | $3-$5/bbl | Maintained through 2026 |

| US-China diplomatic uncertainty | $2-$4/bbl | Summit-outcome dependent |

Note: Premium estimates are analytical approximations based on geopolitical risk modelling frameworks and do not represent institutional forecasts.

OPEC and the IEA: Two Institutions, One Uncomfortable Conclusion

Why Slower Demand Growth and a Supply Deficit Are Not Contradictory

OPEC's decision to lower its 2026 global oil demand growth forecast on May 14 might appear to contradict the IEA's simultaneous warning about a global supply deficit. In fact, these positions are compatible within a single analytical framework. OPEC's market influence has consistently demonstrated this ability to coexist with deteriorating demand outlooks without triggering price collapse.

Demand growth can decelerate while a supply gap still emerges if production disruptions are severe enough to outpace even the revised, slower consumption trajectory. The Middle East conflict has removed meaningful volumes of oil from accessible global supply, and no alternative production source has been brought online at sufficient scale to compensate.

When the world's two leading oil market institutions are simultaneously trimming demand expectations and warning about supply shortfalls, the message is not price collapse. It is a prolonged period of compressed but structurally supported valuations, elevated volatility, and significant sensitivity to geopolitical news flow.

This environment creates a specific challenge for traders and portfolio managers. Long positions face persistent ceilings from monetary headwinds. Short positions face persistent floors from supply constraints and geopolitical risk premiums. The result is a market that rewards tactical range-trading over directional conviction.

The next major ASX story will hit our subscribers first

Scenario Pathways: Where Oil Prices Go From Here

Three Outcomes That Will Define Crude Direction Through the Rest of 2026

Scenario 1: Diplomatic Resolution

The Trump-Xi summit produces a framework reducing Chinese purchases of Iranian crude. A ceasefire structure enables unrestricted Hormuz transit. The Federal Reserve signals a pause in tightening as inflation moderates. Under this scenario, Brent crude would likely retreat toward the $90 to $95 per barrel range as geopolitical risk premiums unwind.

Scenario 2: Prolonged Stalemate

US-Iran negotiations remain deadlocked and Hormuz restrictions persist. The Fed maintains its hawkish posture through the third quarter of 2026. OPEC holds production discipline. This pathway points to Brent oscillating in the $100 to $110 per barrel range with elevated intraday volatility. Analysts tracking how oil settles lower on US rate hike fears and Trump-Xi meeting outcomes increasingly view this as the base-case scenario.

Scenario 3: Escalation and Supply Shock

Iran escalates Hormuz restrictions or initiates a broader Gulf confrontation. US-China relations deteriorate following the summit. The Federal Reserve faces a stagflationary dilemma between fighting inflation and supporting growth. Under this scenario, Brent could surge toward $130 to $150 per barrel, with demand destruction accelerating rapidly at those price levels.

Historical analogies from the 1973 Arab oil embargo and the 1990 Gulf War supply shock suggest that partial or sustained Hormuz blockages carry the potential to push Brent toward the upper bounds of that range within weeks rather than months.

Frequently Asked Questions

Why Did Oil Prices Fall on the Same Day US Crude Inventories Showed a Major Drawdown?

The bearish signal from Federal Reserve rate hike commentary outweighed the bullish inventory surprise. Forward demand destruction risk, driven by tightening monetary conditions, proved more powerful as a price driver than current physical supply tightness.

What Direct Relevance Does the Trump-Xi Summit Have for Oil Markets?

The summit carries implications for Iranian crude sanctions enforcement, US LNG export commitments to China, and broader trade relations that influence global supply and demand balances.

Does a Stronger US Dollar Always Push Oil Prices Lower?

Generally yes, since dollar-denominated oil becomes more expensive for international buyers as the dollar strengthens. However, severe supply disruptions can override this relationship, as seen during previous Middle East conflict periods.

What Does Structural Tightness in Oil Markets Mean for Everyday Consumers?

It means supply constraints are not temporary or easily resolved, reflecting deep-seated production limitations and geopolitical disruptions likely to keep fuel prices elevated for an extended period even as day-to-day price movements remain volatile.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Scenario projections and price premium estimates are analytical approximations and carry significant uncertainty. Readers should consult qualified financial advisers before making investment decisions based on energy market analysis.

Want to Stay Ahead of the Next Major Mineral Discovery Before the Market Catches On?

While geopolitical forces and monetary policy continue to reshape commodity markets, Discovery Alert's proprietary Discovery IQ model cuts through the noise by delivering real-time alerts on significant ASX mineral discoveries — explore the historic returns major discoveries have generated or start your 14-day free trial today to position yourself ahead of the broader market.