June 30, 2026

When Supply Disruption and Price Signals Point in Opposite Directions

In commodity markets, the conventional wisdom is straightforward: disrupt supply, and prices rise. Block a critical shipping lane, and buyers scramble for alternatives, bidding up premiums on whatever barrels remain accessible. This logic has held through every major oil supply crisis of the past half-century, from the 1973 Arab oil embargo to the 2011 Libyan disruption. Understanding oil price volatility trends is therefore essential context before analysing what is unfolding now.

The 2026 Hormuz crisis is rewriting that rulebook in real time. Iran's blockade of the Strait of Hormuz — one of the world's most critical energy chokepoints through which approximately 20% of global oil supply traditionally passes — triggered an initial explosion in physical crude premiums that briefly pushed North Sea Forties crude toward levels unseen since the 2008 commodity supercycle peak. Then, almost as suddenly as they spiked, those premiums collapsed.

The Hormuz blockade remains in effect. The supply disruption has not resolved. Yet physical oil premiums collapse despite the Hormuz crisis has become the defining paradox of global energy markets in 2026, with cargo premiums declining by as much as 90% from their April highs.

Understanding why this is happening — and more critically, whether it will last — requires going beyond headline price data and into the structural mechanics of how physical crude markets actually function under stress.

When big ASX news breaks, our subscribers know first

What Physical Oil Premiums Actually Measure

Before dissecting the paradox, it is worth establishing precisely what physical crude premiums represent and why traders and analysts watch them so closely.

The oil market operates across two distinct pricing layers that most casual observers treat as interchangeable but are fundamentally different instruments:

- Futures contracts (such as front-month ICE Brent) are financial instruments. They represent an obligation or option to take delivery of crude at a future date. They are highly liquid, trade electronically around the clock, and are dominated by institutional investors, hedge funds, and algorithmic traders with varying degrees of physical market exposure.

- Physical cargo premiums (benchmarked against Dated Brent) represent what an actual refiner is willing to pay today for a real barrel of crude with near-term delivery. These transactions involve genuine commercial buyers with genuine processing needs. There is no financial abstraction here — only operational necessity.

Dated Brent itself serves as the primary reference price for physical North Sea crude cargoes, and by extension, influences pricing across Mediterranean and European markets. When Dated Brent trades at a significant premium to front-month futures, it signals that buyers are urgently competing for immediate supply. When that premium collapses toward zero, it signals that urgency has evaporated, regardless of what futures markets are pricing in.

Furthermore, the crude market dynamics underpinning these benchmarks have become increasingly complex as Atlantic Basin supply has grown.

"The physical premium is arguably the most honest signal in the oil market. It cannot be moved by algorithmic positioning or speculative flows. It reflects what refiners are actually willing to pay to keep their plants running today."

The April 2026 Spike: Record Territory Across Every Benchmark

To appreciate the scale of the subsequent collapse, the peak must first be understood in its proper context.

As Iran's Hormuz restrictions tightened through March and into April 2026, physical crude markets experienced stress rarely seen in modern energy history. Buyers who relied on Persian Gulf barrels found their traditional supply routes constrained and began aggressively bidding for alternative cargoes. The results were extraordinary:

| Benchmark | April 2026 Peak | Reference Point | Significance |

|---|---|---|---|

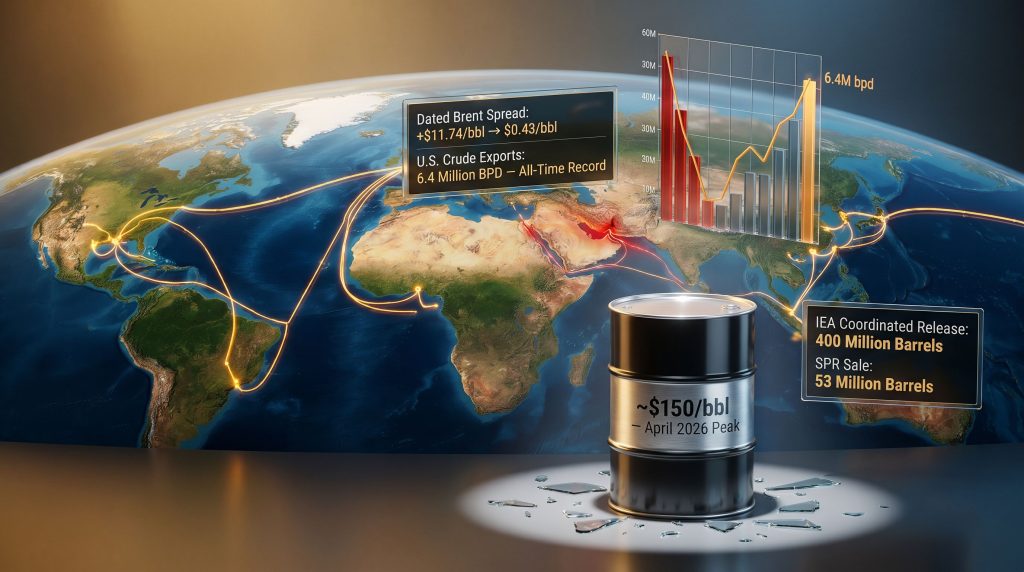

| North Sea Forties Crude | ~$150/bbl | 2008 price peak | First time 2008 record exceeded |

| Dated Brent vs. Front-Month | +$11.74/bbl (weekly peak) | Historical normal ~$0.20–$0.50/bbl | Extreme scarcity signal |

| Saudi Aramco OSP (May 2026) | Largest-ever month-on-month increase | Any prior OSP period | Record pricing by Saudi Arabia |

| Front-Month Brent Intraday Range | $35/bbl in a single session (March 9) | Typical daily range $1–3/bbl | Unprecedented volatility |

Saudi Aramco's Official Selling Price recorded its largest ever month-on-month increase for May 2026 deliveries. This was not a minor adjustment. It was a formal acknowledgment from the world's largest crude exporter that the physical market had entered genuinely unprecedented territory (Kimani, OilPrice.com, May 13, 2026).

The Four Mechanisms Behind the Physical Premium Collapse

Standard Chartered's commodity research team has identified the subsequent premium collapse as demand-driven rather than supply-driven — a distinction with profound implications for where prices go next. The bank's analysts attribute the compression to four distinct buyer-side mechanisms operating simultaneously.

Strategic Buyer Restraint

When North Sea Forties surged toward $150 per barrel, many commercial buyers made a calculated decision: wait. The logic was straightforward. If the Hormuz conflict resolved quickly, those elevated premiums would evaporate and buyers who had locked in at peak levels would suffer significant losses. Purchasing at historically extreme premiums exposed buyers to enormous downside risk with limited upside protection.

This was not irrational panic selling or demand destruction. It was disciplined commercial risk management. Refiners with sufficient inventory runway chose to defer spot market purchases and monitor diplomatic developments rather than chase premiums toward all-time records.

Inventory Drawdowns as a Buffer

Buyers who deferred spot purchases did not simply stop processing crude. Instead, they drew down on existing inventories — both commercial storage and strategic reserves — to keep their refineries running without re-entering the spot market at elevated premiums. This inventory buffer effectively insulated physical demand from the supply shock for a meaningful period.

In the United States alone, the U.S. crude inventory impact was dramatic: combined drawdowns from commercial storage and the Strategic Petroleum Reserve exceeded 2 million barrels per day at peak, according to data reported by Kimani (OilPrice.com, May 13, 2026). This is an extraordinary rate of inventory depletion that cannot be sustained indefinitely.

Reduced Refinery Run Rates and Maintenance Rescheduling

European refiners in particular responded to extreme crude price volatility by reducing throughput and accelerating or rescheduling planned maintenance outages. Lower run rates mechanically reduce crude purchasing requirements, removing demand from the spot market. Japan, meanwhile, saw refinery utilisation settle at 73%, partially sustained by strategic reserve deliveries rather than fresh spot cargo purchases.

Alternative Supply Sourcing

The most structurally significant response has been the rapid diversification of crude sourcing away from Persian Gulf origins. Atlantic Basin producers — particularly U.S. shale operators, Brazilian deepwater producers, and North Sea operators — have dramatically increased output volumes available to Asian and European buyers as substitutes for unavailable Middle Eastern grades.

The VaR Shock: Why Risk Management Is Suppressing Physical Demand

One of the least-discussed mechanisms behind the physical premium collapse operates not at the refinery level but inside the risk management departments of major trading houses and financial institutions.

When front-month Brent trades in a single-session intraday range of $35 per barrel, as occurred on March 9, 2026, the mathematical consequence for institutional risk managers is severe. Value-at-Risk (VaR) models — which quantify the maximum expected loss within a given confidence interval over a defined period — are calibrated around historical volatility assumptions. A $35 intraday range represents a volatility level that would breach VaR thresholds at virtually every major trading institution simultaneously.

"When VaR limits are breached, risk managers are not given the option to exercise judgement. Position sizes must be mechanically reduced. In a crude market context, that means cutting physical exposure regardless of whether the underlying supply situation justifies it."

This creates a self-reinforcing dynamic. Extreme volatility forces institutional buyers to reduce crude exposure. Reduced institutional demand pulls physical premiums lower. Lower physical premiums then suggest the market has normalised, encouraging further position reduction. The feedback loop compresses premiums well below what pure supply-demand fundamentals would dictate.

This is arguably the most under-appreciated dynamic in the 2026 physical crude market. The premium collapse is not primarily a supply story. It is a financial risk management story playing out in the physical trading arena. According to Reuters reporting on spot crude premiums, this easing from record highs has surprised many analysts who expected sustained tightness.

U.S. Crude Exports: The Market's Structural Pressure Release Valve

Among the most concrete expressions of the global supply rebalancing effort is the extraordinary surge in U.S. crude exports. Data from the U.S. Energy Information Administration (EIA), as reported by Kimani (OilPrice.com, May 13, 2026), shows American export volumes reached levels that were unthinkable just a few years ago.

| Export Metric | Week Ending April 24, 2026 | Previous Record (Late 2023) | Change |

|---|---|---|---|

| U.S. Crude Exports | 6.4 million bpd | 5.3 million bpd | +20.8% |

| Combined Crude + Petroleum Products | 12.9 million bpd | Prior peak | New all-time record |

The primary destinations driving this export surge are Asian refiners, particularly in Japan, South Korea, and Taiwan, who have sharply increased purchases of American light sweet shale oil. U.S. shale grades — predominantly Eagle Ford and Permian Basin production — carry API gravities typically in the 40–45 degree range, making them broadly suitable substitutes for the lighter Middle Eastern grades that have become difficult to source through disrupted channels.

The critical question for market participants is whether these export volumes are genuinely displacing Persian Gulf supply at sufficient scale to justify the physical premium compression, or whether they are simply papering over a deepening structural deficit that will eventually re-emerge with force.

The next major ASX story will hit our subscribers first

Strategic Reserve Releases: Finite Buffers in a Potentially Prolonged Crisis

The coordinated release of strategic petroleum reserves represents perhaps the most powerful short-term price suppression mechanism currently operating in physical crude markets.

The scale of the response is historically significant:

- The Trump administration authorised the sale of approximately 53 million barrels from the SPR to nine energy companies as part of an initial phase.

- The total U.S. SPR release programme targets approximately 172 million barrels in aggregate.

- The International Energy Agency (IEA) coordinated a broader global response totalling approximately 400 million barrels across member nations.

- Combined with commercial inventory drawdowns, U.S. market supply has been supplemented at a rate exceeding 2 million barrels per day beyond normal production levels.

This is a genuinely massive policy intervention. However, it operates on a finite timeline. Strategic petroleum reserves exist precisely for crises of this nature, but they cannot release indefinitely without depleting to levels that compromise national energy security.

Morgan Stanley analysts have separately flagged that oil market buffers could run out before Hormuz reopens — a concern that aligns directly with Standard Chartered's thesis that the current physical premium suppression is temporary. Once the 172-million-barrel U.S. release programme and the broader IEA coordinated response are exhausted, the physical market loses its most significant artificial price buffer. At that point, the underlying supply-demand balance — currently masked by reserve releases — becomes the dominant pricing mechanism.

The Jet Fuel Market: A Microcosm of the Broader Dynamic

The jet fuel market provides a uniquely instructive window into the broader story, illustrating how regulatory flexibility can expand effective supply and compress differentials across interconnected markets.

The European Union Aviation Safety Agency (EASA) recently authorised the broader use of U.S.-grade Jet A fuel across European aviation markets, where the standard specification is the slightly different Jet A-1 grade. By removing regulatory barriers to U.S. jet fuel imports, the effective supply pool available to European aviation was meaningfully enlarged, reducing the scarcity premium that had built up in regional jet fuel markets.

| Jet Fuel Metric | Status (May 2026) |

|---|---|

| U.S. Jet Fuel Inventories (May 1, 2026) | 43.57 million barrels, above 5-year seasonal range |

| ARA Region Jet Fuel Stocks | Declined from ~1.1 Mt (late 2025) to 0.56 Mt |

| Front-Month Jet Fuel Contracts | Now trading in contango |

However, the regulatory authorisation carries a meaningful technical caveat. Jet A has a higher freezing point than Jet A-1, which limits its utility to lower-altitude, short-to-medium haul routes. High-altitude long-haul operations — particularly polar routing across transpolar Asian routes — remain dependent on Jet A-1 specification fuel.

European jet fuel inventories in the Amsterdam-Rotterdam-Antwerp (ARA) hub region have tightened sharply, falling from approximately 1.1 million metric tonnes held through late 2025 to just 0.56 million metric tonnes in the most recent weekly data. This draws a clear map of the directional pressure building beneath the current surface calm in physical energy markets.

Global Crude Flow Realignment: Structural Winners and Losers

The Hormuz crisis is not merely disrupting existing trade routes. It is actively accelerating a long-term realignment of global crude flows that analysts expect to leave lasting marks on international supply chain geography. Furthermore, the oil market disruption impact from prior geopolitical tensions has already primed buyers to seek supply diversification more aggressively.

Beneficiaries of the disruption:

- U.S. shale producers who are capturing premium pricing and record export volumes previously inaccessible due to cost competition from Gulf producers.

- Brazilian deepwater operators whose crude exports to China have reportedly doubled as Chinese refiners seek alternatives to disrupted Persian Gulf supply.

- North Sea producers of Forties, Brent, Oseberg, Ekofisk, and Troll grades, which have seen sustained demand from Atlantic Basin refiners diversifying supply chains.

Those bearing the greatest costs:

- China's independent teapot refiners, which historically relied heavily on discounted Iranian and other Middle Eastern crude, are slashing throughput as margin compression makes operations increasingly uneconomic.

- Emerging market importers without strategic reserve buffers or access to alternative credit lines face the full brunt of elevated spot market prices without the institutional mechanisms to defer purchasing.

- Persian Gulf-dependent term contract holders are finding their existing arrangements increasingly difficult to honour amid transit uncertainty.

The trade flow realignment toward Atlantic Basin suppliers may prove more durable than the crisis itself. Once Asian refiners establish operational relationships with U.S., Brazilian, and North Sea suppliers, supply chain inertia tends to preserve those relationships even after geopolitical disruptions resolve. This represents a potentially permanent market share shift rather than a purely cyclical disruption.

Consequently, OPEC's market influence over long-term pricing benchmarks may face structural erosion if Atlantic Basin producers consolidate these newly established buyer relationships.

Three Scenarios for Physical Oil Premium Trajectory

Standard Chartered's core thesis holds that the current physical premium suppression is a temporary equilibrium sustained by finite buffers and deliberate buyer restraint. The bank expects premiums to reassert themselves as those buffers are exhausted and seasonal refinery demand recovers. However, the trajectory depends critically on diplomatic and geopolitical developments that remain genuinely uncertain.

Three distinct scenarios frame the forward outlook:

Scenario A: Diplomatic Resolution Before Buffer Exhaustion

A negotiated end to the Hormuz blockade before strategic reserve releases are depleted would allow physical premiums to remain subdued. Futures markets would likely drift lower as geopolitical risk premiums unwind. This represents the most orderly outcome but requires diplomatic progress that has so far proven elusive, particularly following reports that the Trump administration rejected an Iranian peace proposal.

Scenario B: Hormuz Constraint Persists Into Q3 2026

If the blockade extends into the northern hemisphere summer refinery run season without diplomatic resolution, the buffer mechanisms currently suppressing physical premiums face simultaneous exhaustion. Strategic reserve releases approach their limits, commercial inventory drawdowns cannot continue indefinitely, and seasonal demand from refiners returning from maintenance creates a surge in spot market purchasing. In this scenario, physical premiums re-escalate sharply, potentially pulling futures prices significantly higher as financial markets re-anchor to physical benchmarks.

Scenario C: Partial Hormuz Reopening With Persistent Uncertainty

Iran's reported case-by-case approach to Hormuz transit permissions creates a middle path where access is neither fully blocked nor fully restored. Physical premiums stabilise at moderate levels, sustained backwardation persists in futures markets, and global trade flows continue their realignment toward Atlantic Basin suppliers. This scenario is explored in greater depth by energy analysts examining the Hormuz crisis outlook and represents the most likely near-term outcome based on available geopolitical reporting.

The Signal Hidden in the Numbers

The compression of the Dated Brent spread from +$11.74 per barrel to just $0.43 per barrel in a matter of weeks is not a sign that the physical oil market has normalised. It is a sign that buyers have collectively chosen to pause, deploying every available buffer mechanism to avoid transacting at historically elevated prices.

The paradox of physical oil premiums collapse despite the Hormuz crisis ultimately reveals more about the sophistication of modern market participants than it does about underlying supply conditions. When those buffers are exhausted — as Standard Chartered analysts expect they will be — the physical market's underlying supply-demand reality will reassert itself with considerable force.

The question is not whether physical premiums will recover, but how quickly the mechanisms currently masking that recovery will run out of room to operate.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. All figures and data points are sourced from publicly available reporting as cited. Forward-looking scenario analysis involves inherent uncertainty and should not be relied upon as a basis for investment decisions. Past market behaviour during geopolitical supply disruptions does not guarantee comparable outcomes in future events.

Want to Stay Ahead of the Next Major Commodity Discovery?

While oil market dynamics capture headlines, significant mineral discoveries on the ASX can deliver equally transformative returns — and Discovery Alert's proprietary Discovery IQ model ensures subscribers receive real-time alerts the moment those discoveries are announced, turning complex data across 30+ commodities into clear, actionable opportunities. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial to position yourself ahead of the broader market.