May 14, 2026

The Economics of Decarbonisation: Why Nations With Fossil Fuel Wealth Face the Most Complex Transition Decisions

The conventional framing of net-zero commitments treats them as regulatory obligations imposed on energy-producing nations from the outside. This framing misses something fundamental. For hydrocarbon-dependent economies, the more consequential question is not whether to transition, but how to sequence it so that the revenue engine funding the transition does not stall before the replacement industries are capable of sustaining economic momentum. Oman's updated Oman net zero emissions roadmap 2050, unveiled by the Ministry of Energy and Minerals in May 2026, is a direct product of this more sophisticated logic.

Rather than treating decarbonisation as an environmental compliance exercise, Oman's planners have constructed a pathway explicitly designed to generate economic co-benefits, attract international capital, and diversify the national revenue base. The roadmap does not ask Oman to abandon what it produces. It asks Oman to build what it will need to produce next.

When big ASX news breaks, our subscribers know first

A National Emissions Baseline Built on Science, Not Assumption

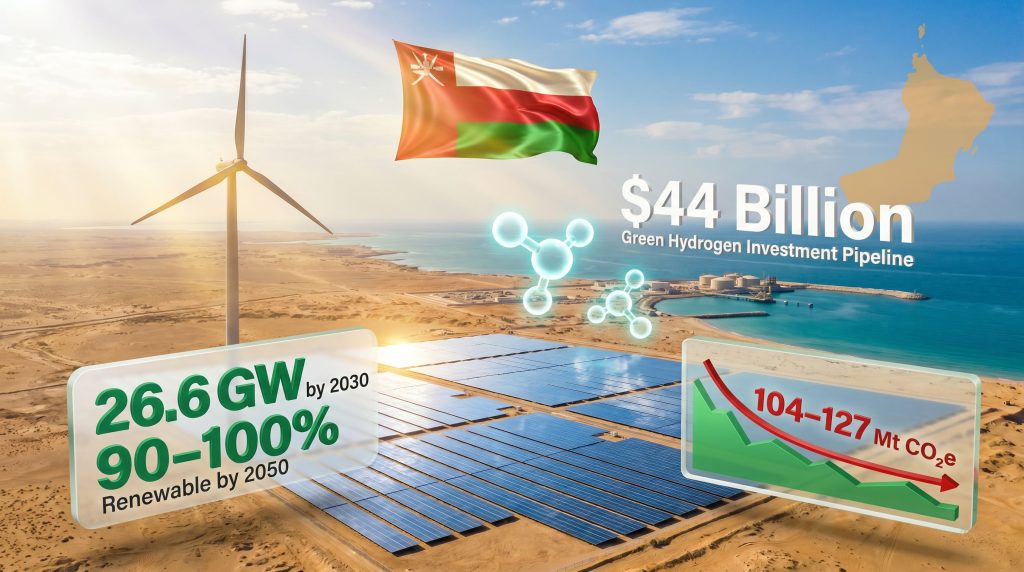

Before any reduction target can be credible, an accurate accounting of current emissions is required. Oman's updated roadmap establishes that total national greenhouse gas emissions reached approximately 94 million tonnes of carbon dioxide equivalent in 2024. Without meaningful policy intervention, that figure is modelled to rise to somewhere between 104 and 127 million tonnes of CO₂e by 2050, a range that reflects different assumptions about economic growth rates, population expansion, and industrial output.

What makes this baseline particularly rigorous is the methodological choice underpinning it. Rather than using a top-down national accounting approach, which allocates emissions by economic sector using macro-level energy consumption data, Oman's planners adopted a bottom-up emissions accounting methodology. This approach calculates emissions at the source level, individually accounting for specific facilities, transport modes, and industrial processes before aggregating them into national totals. The result is a more granular, defensible baseline that strengthens the scientific credibility of every reduction target built upon it.

The three largest emitting segments, namely oil and gas operations, transport, and electricity generation, together account for approximately 70% of Oman's total national emissions. This concentration is both a challenge and an opportunity: targeting these three areas with precision creates the leverage needed to achieve outsized emissions reductions without requiring comprehensive transformation of every sector simultaneously.

Disclaimer: Emissions projections and forecasts referenced in this article represent modelled scenarios based on stated planning assumptions. Actual future emissions will depend on policy implementation, economic conditions, and global technology cost trajectories. This article does not constitute financial or investment advice.

How Oman Built Its Roadmap: A Three-Phase Methodology

The updated national net-zero plan was developed through a structured participatory process coordinated by the Oman Centre for Net Zero, drawing on the expertise of more than 300 subject matter experts across 14 dedicated workshops involving government ministries, private sector entities, and technical specialists. This breadth of engagement is not cosmetic. Effective national transition plans require buy-in from entities that will actually implement them, and the inclusion of private sector participants ensures that investment constraints and market realities are baked into the plan from the outset.

The planning methodology moved through three integrated phases:

| Phase | Core Focus | Primary Output |

|---|---|---|

| Phase 1 | Business-as-usual trajectory assessment | Sectoral emissions growth projections to 2050 using bottom-up accounting |

| Phase 2 | Mitigation cost curve analysis | Classification of available technical solutions across three cost tiers |

| Phase 3 | Enabler identification | Legislative, regulatory, and financing framework requirements |

Understanding the Mitigation Cost Curve Approach

The use of a mitigation cost curve as the Phase 2 analytical tool is worth unpacking, as it is a methodology not widely understood outside energy planning circles. A mitigation cost curve plots emissions reduction options on two axes: the cost per tonne of CO₂e reduced on the vertical axis and the total emissions reduction potential in tonnes on the horizontal axis. This creates a visual and analytical ranking of interventions from cheapest to most expensive, allowing policymakers to sequence investments in order of economic efficiency.

Under this framework, Oman's available technologies were sorted into three tiers:

-

Low-cost tier: Renewable energy solutions, energy efficiency upgrades across buildings and industry, and public transport network expansion. These are mature, commercially available technologies where the cost of emissions abatement is relatively modest.

-

Medium-cost tier: Carbon capture and storage (CCS) infrastructure and green hydrogen integration into industrial processes. These solutions are technically proven but remain more capital-intensive and require supportive policy environments to become commercially viable.

-

Ambitious and frontier tier: Full electrification of the national electricity grid, hydrogen-powered commercial vehicle fleets, and other technologies that remain expensive and, in some cases, not yet at commercial scale. These represent the last phase of the transition, enabled by anticipated technology cost reductions over the coming decades.

This sequencing logic is significant from an investment perspective. It signals that Oman intends to deploy capital where it generates the greatest emissions reduction per dollar in the near term, preserving fiscal capacity for higher-cost interventions as those technologies mature and their costs decline.

Oman Net Zero Targets 2050: The Full Milestone Framework

The roadmap establishes a graduated timeline of specific, measurable targets across the energy transition. These milestones form the backbone of the Oman net zero emissions roadmap 2050 and provide investors, project developers, and international partners with a clear planning horizon.

| Target Year | Key Milestone | Notes |

|---|---|---|

| End of 2026 | Minimum 10% of electricity from renewables | Near-term proof-of-concept milestone |

| 2030 | 26.6 GW of renewable energy capacity installed | Alongside 1 million tonnes/year of green hydrogen production |

| 2035 | 33% reduction in emissions from 2024 baseline | Split into mandatory 7% and conditional 26% components |

| 2040 | 60-70% of total power production from renewables | Major structural shift in electricity mix |

| 2050 | 90-100% renewable energy share; net-zero achieved | Completion of the orderly transition pathway |

The Conditional Architecture of the 2035 Target

One of the more technically sophisticated aspects of the Oman net zero emissions roadmap 2050 is how the 2035 emissions reduction target is structured. The overall 33% reduction from the 2024 baseline is not a single uniform commitment. It is divided into two distinct components with different funding and conditionality structures:

-

A mandatory 7% unconditional reduction, representing domestic commitments that Oman will deliver regardless of external support, funded through national budget allocation and existing domestic policy mechanisms.

-

A conditional 26% reduction, explicitly contingent on securing international climate finance, technology transfer agreements, and national capacity building support from partner nations and multilateral institutions.

This split architecture mirrors the Nationally Determined Contribution (NDC) framework widely used under the Paris Agreement, where developing economies distinguish between what they can achieve alone and what they can achieve with international partnership. The practical implication is that the conditional 26% component creates a structured financing requirement that international climate finance mechanisms can address, converting what might otherwise appear as an aspirational target into a concrete investment opportunity.

Critically, the 2035 milestone has been designed to produce verifiable, tradable carbon credits that can be monetised through both voluntary and compliance carbon markets, creating a direct link between emissions reduction activity and investable financial instruments.

Carbon Markets as a Strategic Financial Architecture

A dedicated regulatory framework for carbon markets has been established alongside the net-zero roadmap, and its design reveals a sophisticated understanding of how international capital flows in the climate finance ecosystem. The framework sets transparent rules and streamlined procedures to enable both private sector entities and small and medium enterprises to participate in carbon market activity across seven identified economic sectors.

The strategic objectives embedded in this framework are threefold:

-

Position Oman as a high-integrity carbon credit supplier capable of competing in global voluntary carbon markets where credit quality and verification standards have become increasingly stringent following regulatory reforms in recent years.

-

Attract international capital to domestic decarbonisation projects by converting emissions reductions into standardised, investable instruments that meet international verification requirements.

-

Diversify national income streams by creating a carbon revenue channel that operates independently of hydrocarbon price cycles, reducing fiscal volatility over the long term.

This is a more nuanced financing architecture than many regional peers have implemented. Rather than relying exclusively on direct government investment or bilateral financing arrangements, Oman is constructing a market infrastructure that allows private capital to flow directly into emissions reduction projects at scale.

The carbon market regulatory framework represents a deliberate move to transform emissions reductions from a policy obligation into a financial asset class, with Oman positioned as both the supplier and the regulatory guarantor of credit integrity.

Green Hydrogen and Renewable Energy: The Industrial Spine of the Transition

The scale of Oman's clean energy investment ambition becomes clearest when examining the green hydrogen programme. Investment commitments across Oman's first two green hydrogen auction rounds exceeded $44 billion, establishing a project pipeline that ranks among the most significant per-capita clean energy investment commitments in the Gulf region. The production target of 1 million tonnes of green hydrogen per year by 2030 is paired with active development of export infrastructure, including a commercial liquefied hydrogen corridor being developed in partnership with the Kingdom of the Netherlands.

A green hydrogen investor guide is being prepared to reduce information asymmetry for international capital, while a second phase study on hydrogen storage in natural underground reservoirs is being completed. This geological storage research is particularly noteworthy from a technical standpoint: underground hydrogen storage in natural geological formations, such as salt caverns or depleted hydrocarbon reservoirs, represents a frontier technology with significant implications for critical minerals and energy security. Oman's existing oil and gas geology may offer natural advantages in this area, though commercial viability remains subject to ongoing technical assessment.

Supporting infrastructure being developed alongside the core hydrogen programme includes:

-

A unified permitting system to reduce procedural barriers and accelerate renewable project development timelines.

-

Completion of a national renewable energy database to improve resource planning and site identification for future project tenders.

-

Development of a renewable energy certificate system to support corporate green power procurement and international clean energy trade.

-

Tendering of a clean energy and battery storage project for Al Halaniyat Islands, serving as a pilot programme for decarbonising remote and off-grid communities dependent on diesel generation.

-

The launch of the Rashd Energy Efficiency Award during Sustainability Week 2026, designed to create competitive incentives for industrial efficiency improvements across sectors.

The next major ASX story will hit our subscribers first

Sustaining Hydrocarbons While Building the Alternative Economy

A critical dimension of the Oman net zero emissions roadmap 2050 that distinguishes it from more aspirational transition plans is its frank acknowledgement of the continued role of hydrocarbon production during the transition period. The orderly transition pathway selected by Oman's planners explicitly accounts for the economic reality that oil and gas revenues fund the infrastructure investments required to move away from them. Furthermore, the energy transition in mining provides a useful parallel, demonstrating how resource-dependent industries can sustain output whilst simultaneously redirecting capital towards cleaner alternatives.

In 2025, Oman's oil and gas sector produced approximately 365.8 million barrels of crude oil and condensates, averaging close to 1 million barrels per day. Proven reserves stand at approximately 4.7 billion barrels of oil and condensates alongside 22.3 trillion cubic feet of natural gas, providing a substantial production runway over the transition period. LNG exports surpassed 11 million metric tonnes, reinforcing Oman's position as a reliable supplier to Asian and European markets.

Exploration activity remained robust in 2025, with 64 exploration and appraisal wells drilled across 47 oil targets and 17 gas targets. A new bidding round for five concession areas was announced in 2026, with 17 operating companies currently active across 34 concession areas, of which 12 have achieved commercial production across 18 areas. Proven reserves were approximately stable, reflecting the balance between production drawdown and exploration success.

The human dimension of this sector is substantial. Omanisation in oil and gas operating companies reached approximately 91.6%, supporting close to 20,000 direct jobs and thousands more in indirect employment. Local content spending across the sector exceeded RO 11 billion over the past decade, with the Majd programme launched specifically to support SME participation and localise supply chain activity.

Social investment linked to the sector totalled approximately 1,275 projects over ten years, with cumulative spending of around RO 74 million covering education, health services, youth empowerment, and community infrastructure. These numbers illustrate why a disorderly or premature transition would carry significant social risks, and why the orderly pathway was selected as the governing framework.

Mining as a Strategic Complement to the Energy Transition

Oman's mining sector is positioned not merely as a separate revenue stream but as a strategic complement to the clean energy transition. The sector reached total production of approximately 65 million tonnes in 2025, with sales of 60 million tonnes valued at around RO 159 million. Six new concession agreements were signed during the year, bringing active concession areas to 28 operated by 13 companies.

Copper concentrate exports rose notably to approximately 95,000 tonnes, with associated investments exceeding RO 105 million. Copper's centrality to electrical wiring, renewable energy infrastructure, and electric vehicle manufacturing makes this production directly relevant to global clean energy supply chains. The strategy is deliberately pivoting toward expanding exploration of strategic minerals that underpin those supply chains, including copper and chrome. In addition, critical minerals demand globally is accelerating as nations race to secure the raw materials essential for electrification and clean energy deployment.

Future mining strategy priorities include:

-

Expanding exploration into strategic and critical mineral categories with direct clean energy applications.

-

Developing local value-added manufacturing to process raw ore domestically rather than exporting unrefined material, capturing a greater share of the value chain.

-

Establishing the Minerals Trading Company as a national marketing entity to strengthen Oman's commercial position in global commodity markets.

-

Tendering additional concession areas and public investment sites to attract international mining capital, with three concession areas and three general sites planned for tender in 2026.

How Oman's Approach Compares Across the GCC

| Country | Net Zero Target | Key 2030 Renewable Target | Green Hydrogen Status |

|---|---|---|---|

| Oman | 2050 | 26.6 GW installed capacity | $44bn+ investment committed; 1 Mt/year by 2030 |

| Saudi Arabia | 2060 | 50% renewables in power mix | Major export ambitions |

| UAE | 2050 | 44% clean energy contribution | Significant export development |

| Qatar | 2050 | 20% renewables by 2030 | Emerging programme |

Note: All figures represent publicly stated national targets as of available reporting dates and are subject to revision. Comparisons are indicative.

Several features of Oman's roadmap stand out when assessed against regional peers. The three-phase bottom-up emissions accounting methodology is more granular than approaches used in comparable national plans. The mandatory versus conditional split in the 2035 target introduces a financing conditionality mechanism that creates a structured incentive for international climate finance partners. The carbon market regulatory framework is among the more developed in the region in terms of enabling private sector and SME participation. And the $44 billion green hydrogen investment pipeline represents one of the most substantial per-capita clean energy commitments in the Gulf.

Key Enablers and Structural Risks

The credibility of any net-zero roadmap ultimately depends on identifying both what needs to go right and what could go wrong. Oman's roadmap addresses both dimensions. Consequently, mining electrification and decarbonisation trends offer instructive lessons for how capital-intensive industries can manage this dual challenge of operational continuity and structural change.

Critical enablers identified:

-

Securing international climate finance to fund the conditional 26% reduction component, without which the more ambitious 2035 target cannot be fully achieved.

-

Technology transfer agreements providing access to medium and frontier-tier solutions, particularly CCS and hydrogen vehicle fleets.

-

Regulatory clarity through the carbon market framework and unified permitting system, both of which reduce investor uncertainty and lower transaction costs.

-

Institutional continuity through the Oman Centre for Net Zero, which provides ongoing monitoring, stakeholder coordination, and plan updating capacity.

Structural risks to watch:

-

Hydrocarbon revenue dependency: The fiscal capacity to invest in the transition remains linked to oil price cycles, creating vulnerability if prices fall sharply during a critical investment window.

-

Technology cost trajectories: Medium and frontier-tier technologies remain expensive without continued global cost reductions driven by scale and R&D investment outside Oman.

-

Financing conditionality: The voluntary 26% reduction component is explicitly contingent on external support that is not guaranteed by any binding international commitment at this stage.

-

Demand-side behavioural shifts: Achieving targets in the transport sector requires significant changes in consumer and commercial behaviour that policy alone cannot fully engineer.

-

Residual emissions gap: Even under the modelled orderly transition scenario, a residual emissions gap is expected to remain in 2050, requiring breakthrough technologies that are not yet commercially available.

The Strategic Outlook for 2050

Under the orderly transition pathway selected by Oman's planners, modelled outcomes suggest emissions could decline by approximately 6% by 2030, 54% by 2040, and 92% by 2050 relative to baseline levels. The residual gap remaining by 2050 would need to be closed by frontier technologies currently in development phases globally. The IEA's national strategy framework for orderly transitions to net zero provides a useful benchmark against which Oman's milestone architecture can be evaluated by international partners and investors.

The economic co-benefits anticipated alongside these reductions include positive contributions to GDP growth through green industry development, new revenue streams from carbon credit markets, employment diversification across both established and emerging energy sectors, and stronger positioning in global clean energy supply chains through mining sector expansion into strategic minerals.

For international investors and project developers, the combination of a scientifically grounded net-zero roadmap, a functioning carbon market regulatory framework, a $44 billion hydrogen investment pipeline, and 26.6 GW of planned renewable capacity by 2030 constitutes a comprehensive and multi-dimensional market proposition. Oman's revised net-zero roadmap has attracted considerable regional commentary, reflecting how the plan's structure and ambition set it apart from comparable Gulf transition strategies.

Readers seeking additional context on Oman's energy transition and broader GCC sustainability developments can explore related coverage through Zawya's Green section at zawya.com, which tracks ongoing developments across regional climate policy and clean energy investment.

Want to Identify the Next Major Mineral Discovery Before the Market Does?

As Oman's transition strategy highlights the critical role of copper, chrome, and strategic minerals in clean energy supply chains, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly alerting subscribers to significant mineral discoveries across more than 30 commodities. Explore historic discoveries and their market returns, then start your 14-day free trial to position yourself ahead of the broader market.