May 15, 2026

The Race to Lock In Africa's Copper Future Before the Window Closes

When financial investors begin targeting assets that won't produce a single tonne of output for years, it signals something fundamental has shifted in how markets are pricing future supply. That is precisely what is unfolding across Africa's undeveloped copper landscape. Appian secures majority stake in Omitiomire Copper project, and this move reflects how the scramble for long-duration copper exposure is no longer the domain of major mining houses alone. Private capital is moving earlier in the project lifecycle, accepting more development risk in exchange for a position ahead of what many analysts view as a structural supply shortfall.

The logic is straightforward even if the risk profile is not: copper sits at the centre of every meaningful decarbonisation pathway, from utility-scale solar and wind installations to electric vehicle drivetrains and high-voltage transmission corridors. According to the International Energy Agency's Critical Minerals in Clean Energy Transitions report, the critical minerals demand for copper across clean energy applications alone is projected to grow significantly through 2040, with grid infrastructure upgrades representing one of the largest incremental consumption categories globally.

Against that backdrop, undeveloped but technically advanced copper projects in politically stable African jurisdictions have become some of the most contested assets in the global critical minerals race. Appian Capital Advisory's move to secure a 95% controlling equity interest in the Omitiomire Copper project in Namibia is a case study in this accelerating dynamic, one that deserves examination well beyond the headline transaction details.

When big ASX news breaks, our subscribers know first

Why Namibia Stands Apart in Africa's Copper Investment Landscape

Not all African jurisdictions compete equally for long-duration mining capital. The factors that differentiate Namibia from peer copper-prospective countries in the region are less about geology and more about institutional architecture. Namibia consistently ranks among the most transparent and well-governed mining jurisdictions on the continent, a distinction that translates directly into lower political risk premiums for investors deploying hundreds of millions of dollars over multi-decade project horizons.

The country's mining governance framework, administered through the Ministry of Mines and Energy, operates under a well-established legislative structure that provides clarity on licensing, royalties, environmental obligations, and capital repatriation. For a project requiring more than US$400 million in development capital, that regulatory predictability is not a minor consideration. It is often the factor that separates a project that attracts institutional financing from one that does not.

Infrastructure access reinforces Namibia's investment appeal. The country's road and rail networks connect inland mining operations to the port of Walvis Bay, one of the most capable export gateways on Africa's Atlantic coastline. For a future copper cathode producer, direct access to bulk export infrastructure reduces one of the most significant cost variables in project economics.

Namibia's Broader Critical Minerals Pipeline

Namibia is not a single-project mining story. The country hosts a diverse and active mineral production base that has built a skilled workforce, established regulatory precedent, and attracted sustained foreign investment across multiple commodity cycles. Operations including the Rosh Pinah zinc mine, the Husab uranium mine, and the Navachab gold operation have collectively deepened Namibia's mining sector capability in ways that directly benefit new entrants planning large-scale development projects.

Compared to peer jurisdictions competing for the same private capital, Namibia's combination of governance quality, infrastructure maturity, and technical workforce depth presents a compelling risk-adjusted proposition, particularly for investors with a five to fifteen year development horizon. Furthermore, the broader copper supply crunch unfolding globally only strengthens the strategic case for locking in well-governed African assets at the pre-production stage.

What Is the Omitiomire Copper Project? Technical Profile and Resource Characteristics

Located approximately 140 kilometres northeast of Windhoek in the Otjozondjupa Region, Omitiomire is widely regarded as one of Namibia's most technically advanced undeveloped copper assets. Its exploration pedigree stretches back to the 1970s, meaning decades of drilling campaigns, metallurgical test work, and technical studies have progressively reduced geological uncertainty and refined the resource model underpinning current development planning.

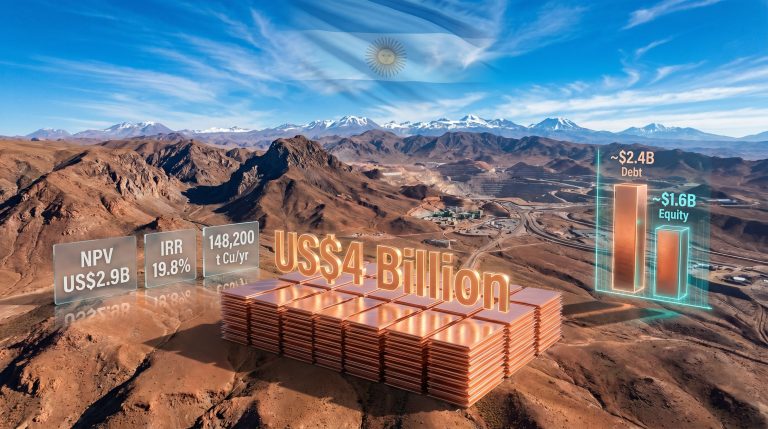

The deposit's resource base is significant in both scale and grade. Previous estimates have placed the mineral resource at more than 100 million tonnes of ore grading approximately 0.51% copper, which translates to a substantial quantity of contained copper metal before any processing losses are factored in. For context within the global copper development pipeline, a defined resource of this size with multiple completed feasibility studies behind it occupies a relatively advanced position, particularly among African projects outside the established Zambian and Congolese copper belts.

Omitiomire Project: Key Parameters at a Glance

| Parameter | Estimated Figure |

|---|---|

| Mineral Resource (Ore Tonnes) | More than 100 million tonnes |

| Average Copper Grade | ~0.51% Cu |

| Projected Annual Output | ~26,800 tonnes copper cathode |

| Projected Mine Life | ~15 years |

| Planned Development Capital | More than US$400 million |

| Location | Otjozondjupa Region, Namibia |

| Distance from Windhoek | ~140 km northeast |

| Processing Method | Heap leach with SX-EW |

| End Product | Copper cathode |

| Exploration History | Dating to the 1970s |

How Heap Leach and SX-EW Processing Works at Omitiomire

Previous feasibility work on the project confirmed plans for an open-pit mining operation paired with heap leach and solvent extraction-electrowinning (SX-EW) processing technology. This combination is particularly well-suited to oxide-dominant copper deposits and offers meaningful cost advantages compared to conventional flotation and smelting routes. In addition, understanding the copper leaching process in detail helps contextualise why this method is increasingly favoured for deposits of this character.

The process follows a logical sequence:

-

Ore is extracted by open-pit methods and crushed to a controlled particle size to maximise acid penetration.

-

Crushed material is stacked onto engineered, geomembrane-lined heap leach pads, then irrigated with a dilute sulphuric acid solution that dissolves copper from the ore matrix over a defined leach cycle.

-

The resulting copper-bearing solution, known in the industry as pregnant leach solution (PLS), drains from the base of the pad and is collected in lined ponds.

-

PLS is pumped through a solvent extraction (SX) circuit, where an organic extractant selectively binds copper ions, removing impurities and concentrating the copper in a purified aqueous solution called the strip electrolyte.

-

The strip electrolyte is fed into an electrowinning (EW) circuit, where an applied electrical current causes pure copper to plate onto stainless steel cathode blanks. These cathode sheets are then stripped, stacked, and dispatched to market.

The SX-EW process route produces copper cathode with a purity typically exceeding 99.99%, meeting London Metal Exchange (LME) Grade A specifications and enabling direct sale into refined copper markets without further processing. This simplifies offtake negotiations considerably compared to concentrate-producing operations, which require smelter treatment.

One of the less-discussed advantages of heap leach processing for lower-grade oxide deposits is its comparatively lower operational carbon intensity relative to smelting-based routes. The absence of a pyrometallurgical stage reduces both energy consumption and direct emissions, an increasingly relevant consideration as downstream copper buyers face growing pressure to demonstrate supply chain carbon accountability.

Understanding Appian's Acquisition Structure

According to Bloomberg, when Appian Capital Advisory secured the Omitiomire asset, the transaction was executed through a purpose-built subsidiary, Appian Omega Bidco Limited, which assumed control of Craton Mining and Exploration, the entity established specifically to advance the Omitiomire project. Through this structure, Appian acquired 95% of Omico Copper, giving the investment group a dominant controlling interest in all future development decisions, financing arrangements, and operational outcomes.

Appian's Dual-Asset Namibia Platform

The Omitiomire acquisition establishes Appian as a two-commodity operator in Namibia, combining an existing position in the country's zinc sector with a new controlling stake in its most advanced undeveloped copper asset.

| Asset | Commodity | Appian Equity | Status |

|---|---|---|---|

| Rosh Pinah Mine | Zinc | ~89.96% | Operating |

| Omitiomire Project | Copper | 95% | Pre-production / Development |

This dual-commodity structure carries strategic logic that extends beyond simple diversification. Zinc and copper have distinct demand drivers: zinc remains heavily tied to construction and industrial galvanisation, while copper's demand trajectory is increasingly shaped by electrification and energy transition spending. By holding significant positions in both metals within a single jurisdiction, Appian deepens its operational and regulatory expertise in Namibia while reducing single-commodity exposure without the complexity of operating across multiple countries.

Development Scenarios: How Omitiomire Could Reach Production

The path from controlled asset to producing mine involves navigating capital markets, permitting processes, and commodity price cycles simultaneously. Several plausible development scenarios exist for Omitiomire, each reflecting different assumptions about copper market conditions, financing availability, and project execution timelines.

Scenario 1: Accelerated Development

Under favourable copper price conditions, Appian deploys the full capital envelope on a compressed timeline, using strong commodity fundamentals to attract project finance lenders and progress through construction without staged interruptions. Projected steady-state output of approximately 26,800 tonnes of copper cathode per year over a 15-year mine life would be the target outcome.

Scenario 2: Phased Capital Deployment

A more conservative approach stages construction capital across multiple tranches, potentially using early production from higher-grade ore zones to fund subsequent development phases. This reduces upfront financing risk but extends the overall timeline to full production capacity.

Scenario 3: Offtake-Backed Financing

Appian secures a long-term offtake agreement with a downstream copper buyer, such as a European copper refiner, an Asian battery materials processor, or a utility-scale renewable energy developer seeking supply chain security. Offtake-backed project financing is an increasingly common structure in African copper development, as it reduces equity dilution by enabling higher debt capacity underpinned by contracted revenue.

Because Omitiomire produces copper cathode rather than concentrate, it bypasses the smelter treatment step entirely. This means any offtake agreement is negotiated directly at the refined copper level, without the treatment charge and refining charge (TC/RC) deductions that can significantly erode the net realised price for concentrate producers. That distinction matters considerably for project economics and financing conversations.

The Copper Supply Picture and Why Pre-Production Assets Are Gaining Value

The investment case for acquiring undeveloped copper projects ahead of the development curve rests on a straightforward thesis: the gap between where copper supply is heading and where demand is going is widening, and the pipeline of technically advanced, shovel-ready projects available to close that gap is thinner than most market participants appreciate. Monitoring the copper price outlook is consequently becoming a more central activity for institutional investors than it was even five years ago.

Electric vehicles provide a useful illustration of the demand intensity question. According to data published by the International Copper Association, a battery electric vehicle contains roughly three to four times the copper of a conventional internal combustion engine vehicle, primarily in the motor windings, power electronics, and charging infrastructure. Offshore wind installations are similarly copper-intensive, requiring several tonnes of copper per megawatt of installed capacity across cables, transformers, and generators.

Grid infrastructure may represent the single largest underappreciated copper demand category. As electricity networks in major economies are upgraded and expanded to handle bidirectional power flows from distributed renewable generation, the copper intensity per kilometre of upgraded transmission line is substantially higher than for older grid assets. This demand category is largely invisible in EV-focused coverage but is growing rapidly in infrastructure spending programmes across Europe, North America, and Asia.

Against this demand picture, the copper development pipeline faces structural constraints. The average time from discovery to first production for a major copper mine has historically exceeded fifteen years, according to research published by industry bodies tracking project development timelines. Environmental permitting, community engagement, and capital market cycles all contribute to this extended lead time. Projects with long exploration histories, completed feasibility studies, and defined resource bases therefore command a genuine scarcity premium in the current acquisition environment.

Omitiomire's exploration history extending back to the 1970s, combined with multiple rounds of completed technical studies, places it in a select category of African copper assets where geological risk has been substantially reduced relative to earlier-stage exploration projects.

The next major ASX story will hit our subscribers first

What Copper Cathode Production Means for Offtake and Market Access

A point that deserves more attention than it typically receives in project-level reporting is the commercial significance of producing copper cathode rather than copper concentrate. The distinction is not merely technical. It has direct implications for who buys the product, at what price, and under what terms.

Copper concentrate, the output of most large-scale sulphide processing operations, requires further processing at a smelter before it becomes refined copper. The smelter charges treatment and refining fees that reduce the mine's net copper revenue. By contrast, copper cathode is a finished, market-ready product that trades directly on the LME and can be sold to rod mills, wire manufacturers, and fabricators without any intermediate processing step.

For a project like Omitiomire, where the end product will be LME-deliverable copper cathode, the commercial pathway is more direct and the revenue realisation is more predictable. This characteristic also expands the potential buyer universe beyond smelter operators to include downstream industrial consumers. Thoughtful copper investment strategies increasingly prioritise cathode-producing assets for precisely this reason, as supply chain transparency requirements tighten and ESG due diligence frameworks become more stringent.

Key Investment Considerations and Risk Factors

Investors and analysts evaluating the strategic logic of the Omitiomire acquisition should weigh several factors alongside the headline opportunity:

-

Development capital risk: At more than US$400 million, the capital requirement is substantial. Cost overruns and timeline extensions are common in large-scale mine construction, and the financing structure will significantly influence project returns.

-

Copper price dependency: Project economics are sensitive to the copper price at the time of production commencement. A sustained copper price decline between acquisition and first production would affect the return profile.

-

Permitting and environmental timeline: Even in well-governed jurisdictions, environmental impact assessments and community consultation processes can introduce delays. Water availability in the Otjozondjupa Region is a variable that will require careful management given the water-intensive nature of acid leach operations.

-

Offtake and financing structure: The terms under which project financing is secured, and whether offtake agreements are in place before construction begins, will shape both the risk profile and the equity return outcome.

-

Resource classification and recovery rates: The stated resource estimate of more than 100 million tonnes at approximately 0.51% copper requires consideration of the JORC classification breakdown (Measured, Indicated, Inferred), the cut-off grade assumptions, and the heap leach recovery rate applied in feasibility modelling. These parameters collectively determine the actual copper that reaches the market.

This article contains forward-looking analysis and scenario projections that are based on publicly available information and general industry knowledge. They do not constitute financial advice. Readers should conduct independent due diligence and consult qualified advisers before making investment decisions.

Frequently Asked Questions: Appian and the Omitiomire Copper Project

What is the Omitiomire Copper Project?

Omitiomire is a pre-production copper development asset situated approximately 140 kilometres northeast of Windhoek in Namibia's Otjozondjupa Region. The project holds a mineral resource estimated at more than 100 million tonnes of ore grading around 0.51% copper, with prior feasibility work outlining plans for an open-pit operation using heap leach and SX-EW technology to produce refined copper cathode.

Who owns Omitiomire and how was the stake acquired?

Appian Capital Advisory completed the acquisition of Omico Copper in May 2026, securing a 95% controlling equity interest through its subsidiary Appian Omega Bidco Limited, which assumed control of Craton Mining and Exploration, the development entity for the project. As reported by Mining.com, the deal deepens Appian's strategic commitment to Namibia as a priority jurisdiction for long-duration mineral investment.

How much capital is required to develop Omitiomire?

Development capital requirements have been estimated at more than US$400 million, covering mine construction, processing infrastructure, and associated site facilities.

What will Omitiomire produce and at what scale?

Project studies conducted before the acquisition estimated average annual output of approximately 26,800 tonnes of copper cathode over a projected mine life of around 15 years.

Is the project currently producing copper?

No. Omitiomire remains a pre-production development asset requiring significant capital investment and construction activity before any copper cathode output can be achieved. Appian secures majority stake in Omitiomire Copper project as a long-horizon investment with production timelines that reflect the inherent lead times of large-scale mine development.

How does this acquisition fit within Appian's broader Namibia strategy?

Appian already holds approximately 89.96% of the Rosh Pinah zinc mine, Namibia's only operating zinc mine. The Omitiomire acquisition adds copper exposure to the portfolio, creating a two-commodity critical minerals platform within a single jurisdiction where Appian has established operational and regulatory experience. Consequently, this positions the firm as one of the most significant private mining investors active in southern Africa today.

Want to Track the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and the returns they generated, then begin your 14-day free trial to position yourself ahead of the next major find.