July 13, 2026

What the Third Consecutive Downgrade Actually Signals

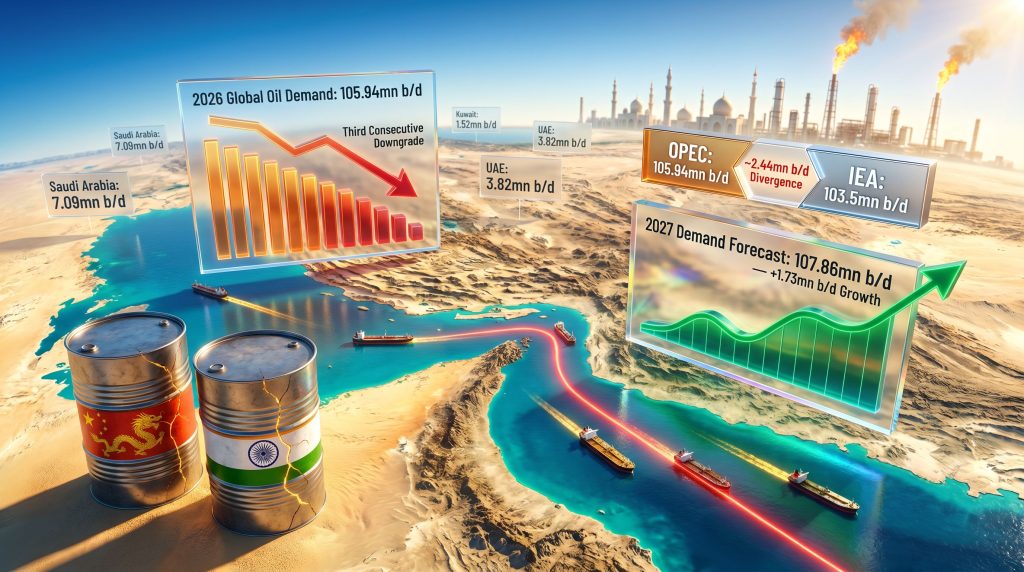

When an organisation revises the same metric in the same direction three months in succession, the pattern itself carries analytical weight beyond any single number. The OPEC downgrades oil demand forecast cycle of 2026 marks the third consecutive month in which the group has cut its global oil demand growth projection, this time by 190,000 barrels per day (b/d), bringing the full-year growth figure down to 780,000 b/d and total projected consumption to 105.94mn b/d.

The cumulative revision from earlier estimates exceeding 1.17mn b/d of growth represents a reduction of nearly one-third in expected demand expansion within just a few months. While OPEC did not provide an explicit rationale for the latest cut in its report, the underlying drivers are not difficult to identify. The US-China trade war and the US-Iran conflict, which began on 28 February 2026, have generated cascading economic disruptions that simultaneously weakened consumption in the world's two largest oil-importing nations and fractured Middle Eastern supply chains.

Furthermore, this has introduced a level of geopolitical risk premium into energy markets that has not been seen in modern history. According to Reuters reporting on the June 2026 MOMR, the organisation has been consistently lowering its demand outlook amid escalating uncertainty.

"The pattern of repeated revisions is analytically significant in its own right. Each successive cut signals that OPEC's initial assumptions about conflict duration, Hormuz recovery, and macroeconomic resilience have proven overly optimistic."

When big ASX news breaks, our subscribers know first

OPEC's 2026 and 2027 Demand Projections: The Full Picture

Revised Numbers at a Glance

| Metric | Previous Estimate | Revised Estimate | Change |

|---|---|---|---|

| 2026 Demand Growth Forecast | ~1.17mn b/d | 780,000 b/d | -190,000 b/d |

| Total 2026 Global Consumption | — | 105.94mn b/d | Third consecutive downgrade |

| China Demand Revision | — | -110,000 b/d | Largest single-country cut |

| India Demand Revision | — | -60,000 b/d | Second-largest contributor |

| 2027 Demand Growth Forecast | ~1.52mn b/d | 1.73mn b/d | +210,000 b/d upgrade |

| Total 2027 Global Consumption | — | 107.86mn b/d | Forward recovery signal |

The simultaneous downgrade for 2026 and upgrade for 2027 reveals the core thesis embedded in OPEC's current modelling: the demand destruction is viewed as transient rather than structural. The group appears to be treating the conflict-driven suppression as a temporary shock that will unwind once Hormuz shipping normalises and the broader economic fallout stabilises. Whether that assumption proves correct depends entirely on how the geopolitical situation evolves.

China and India: The Demand Growth Engines Stalling Under Pressure

The two economies responsible for the largest share of OPEC's downward revision are also the markets that matter most to the organisation's long-term pricing power.

China absorbed the largest single-country cut of 110,000 b/d. Beyond the direct logistical disruption caused by Hormuz-dependent crude flow rerouting, China is simultaneously navigating a slowing property sector, persistent trade tensions, and softening industrial output. These structural headwinds have compounded what began as a supply-chain shock into a broader demand softness across energy-intensive industries.

India, whose demand growth forecast was trimmed by 60,000 b/d, carries acute vulnerability to Middle Eastern supply disruptions given its heavy reliance on crude from Iran, Iraq, and Saudi Arabia. The rerouting of tankers away from Hormuz adds both cost and time to India's import logistics, creating friction that reduces effective demand even when underlying consumption intent remains stable.

Middle Eastern demand itself fell by approximately 40,000 b/d in the revised forecast, with March 2026 regional consumption running roughly 500,000 b/d below year-prior levels as the direct economic consequences of the conflict suppressed activity across the Gulf states.

"India and China together account for more than 60% of projected global oil demand growth over the next decade. Any sustained suppression of their near-term consumption trajectories carries long-term implications for OPEC's pricing power and production strategy."

The OPEC vs. IEA Divergence: A 2.44mn b/d Gap That Matters

Comparing the Two Dominant Forecasting Frameworks

| Forecasting Body | 2026 Global Oil Demand Projection | Year-on-Year Change |

|---|---|---|

| OPEC | 105.94mn b/d | +780,000 b/d growth |

| IEA | 103.5mn b/d | -1mn b/d decline |

| Divergence | ~2.44mn b/d gap | Structural disagreement |

The gap between OPEC and the International Energy Agency (IEA) has expanded into one of the most consequential analytical splits in contemporary energy markets. The IEA's position implies that the US-Iran war has not only interrupted demand growth but actively caused a year-on-year decline in global oil consumption, a view that reflects a considerably more pessimistic assessment of the conflict's economic reach.

OPEC's more constructive baseline likely incorporates an assumption of partial conflict resolution and a demand recovery weighted toward the latter half of 2026. The 2027 upgrade reinforces this interpretation, suggesting the organisation views the current trajectory as a trough rather than a trend.

For commodity traders, energy policymakers, and portfolio managers, a 2.44mn b/d divergence between the two most influential forecasting bodies creates significant pricing uncertainty. The oil market trade war dynamics compound this uncertainty further, as hedging strategies built on one set of assumptions become materially wrong if the other framework proves more accurate.

The Strait of Hormuz: A Chokepoint Under Active Threat

Why Hormuz Is the Central Variable in Every Scenario

Approximately 20% of global seaborne oil trade transits the Strait of Hormuz. When that corridor is disrupted, its effects are not confined to one producing nation or one trade route. They propagate across the entire global energy system through price adjustments, cargo rerouting, insurance premium spikes, and freight cost escalation.

In July 2026, Iran's Islamic Revolution Guards Corps (IRGC) declared the strait closed until further notice following a fresh round of US strikes on Iranian military targets. US Central Command disputed the declaration and asserted that traffic was continuing to flow, though visible vessel tracking data through MarineTraffic showed minimal transits, with many vessels apparently operating with their AIS tracking systems disabled to reduce targeting risk.

The operational reality sits somewhere between these competing claims. Some shipping is moving, but under significantly elevated security risk, with documented attacks on commercial vessels including the Cyprus-flagged containership GFS Galaxy, which was struck nine nautical miles east of the Omani coast and abandoned by its crew.

A notable aspect of the conflict's geographic reach is the targeting of Duqm port in Oman, which sits well south of Hormuz. The IRGC claimed strikes on logistics and refuelling infrastructure there, extending the zone of active disruption beyond the strait itself and complicating alternative routing strategies that had treated Oman's southern ports as safer transit points.

OPEC+ Production Recovery: Progress Against a Fragile Backdrop

Country-by-Country Output Status in June 2026

| OPEC+ Member | June 2026 Output (mn b/d) | May 2026 Output (mn b/d) | Production Target (mn b/d) | Gap vs. Target |

|---|---|---|---|---|

| Saudi Arabia | 7.09 | 6.57 | 10.29 | -3.20 |

| Iraq | 2.15 | 1.55 | 4.35 | -2.20 |

| Kuwait | 1.52 | 0.58 | 2.63 | -1.11 |

| Iran | 2.75 | 2.65 | n/a | n/a |

| UAE | 3.82 | ~2.11 | ~3.46 | +0.36 |

| Russia | 9.00 | 9.00 | 9.76 | -0.76 |

| Kazakhstan | 1.86 | 1.86 | 1.60 | +0.26 |

| Nigeria | 1.65 | 1.59 | 1.50 | +0.15 |

| Algeria | 1.00 | 0.98 | 0.99 | +0.01 |

Total OPEC+ crude output including Mexico rose by approximately 2.999mn b/d in June to reach 36.278mn b/d, according to estimates from secondary sources including Argus. Despite this partial recovery, production remains roughly 6.5mn b/d below pre-war levels, illustrating how far the system still is from returning to its earlier baseline.

The June improvement was driven primarily by Mideast Gulf members that were able to ramp up exports following a US-Iran interim peace deal on 18 June 2026. Saudi Arabia, Iraq, Kuwait, Iran, and Bahrain collectively contributed the bulk of the monthly increase. However, Iran's sanctions waiver, which was issued as part of that interim arrangement, was subsequently revoked, creating fresh uncertainty about Tehran's ability to sustain or expand output in the weeks ahead.

The UAE's Post-OPEC Surge and Its Strategic Implications

Perhaps the most structurally significant development within the OPEC+ production landscape is the UAE's trajectory following its departure from the alliance. UAE output climbed to a record 3.82mn b/d in June, approximately 360,000 b/d above the quota the country would likely have held had it remained within OPEC's framework.

This creates a new competitive dynamic. If Hormuz fully reopens and multiple Gulf producers simultaneously accelerate output recovery, the risk of a rapid oversupply event rises materially. OPEC's market influence is consequently being tested at precisely the moment when the UAE continues producing at or above current record levels while Saudi Arabia, Iraq, and Kuwait push toward closing their respective gaps against target.

The tension between maintaining collective supply discipline and pursuing individual market share objectives is a defining strategic fault line that will shape OPEC+ cohesion through the remainder of 2026 and into 2027.

Three Scenarios for the Second Half of 2026

The path forward for global oil markets hinges on a small number of variables, primarily the durability of any ceasefire arrangement, the pace of Hormuz normalisation, and the response of non-OPEC+ producers.

-

Conflict Escalation: Hormuz remains effectively disrupted through Q3 2026. The supply deficit implied by OPEC's own demand figures deepens further. Brent crude faces sustained upward pressure despite weakening demand growth.

-

Managed De-escalation: A durable ceasefire enables phased Hormuz reopening by late Q3 2026. OPEC+ production recovery accelerates. The 2027 demand upgrade becomes the dominant market narrative and price momentum shifts lower.

-

Prolonged Stalemate: Intermittent conflict with periodic Hormuz disruptions creates a persistent geopolitical risk premium. Markets operate in a state of elevated uncertainty. Non-OPEC+ supply growth from the United States, Brazil, and Guyana becomes a critical buffer against a full-blown energy shortage.

OPEC has been preparing for scenario two by unwinding voluntary production cuts ahead of a hoped-for recovery. Seven core members, including Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, and Oman, agreed on 5 July 2026 to raise their collective ceiling by a further 188,000 b/d for August. This leaves just 188,000 b/d of voluntary cuts remaining, which could be fully eliminated as early as September if conditions permit.

Russia adds another layer of complexity to non-OPEC+ supply stability. Output held at approximately 9.00mn b/d in June, still 760,000 b/d below target due to sustained Ukrainian strikes on energy infrastructure. Furthermore, the oil geopolitics analysis surrounding Russia's position suggests further losses cannot be ruled out, and any material reduction in Russian supply would significantly tighten an already strained global balance.

The next major ASX story will hit our subscribers first

FAQ: OPEC Oil Demand Forecast Downgrade Explained

Why Has OPEC Downgraded Its Oil Demand Forecast Three Months in a Row?

The consecutive revisions reflect compounding disruption from the US-Iran war, which began in late February 2026. The conflict has suppressed regional consumption, interrupted Hormuz shipping, and weakened near-term growth expectations in China and India. Consequently, each successive OPEC downgrades oil demand forecast announcement has reflected deeper-than-anticipated economic contagion.

What Is OPEC's Current 2026 Global Oil Demand Forecast?

As of the July 2026 MOMR, OPEC projects total consumption of 105.94mn b/d in 2026, representing demand growth of approximately 780,000 b/d. However, oil price volatility remains a significant complicating factor in how these figures translate into actual market pricing.

How Does OPEC's Outlook Compare to the IEA's?

The two organisations are separated by approximately 2.44mn b/d. The IEA projects 2026 demand at 103.5mn b/d, implying a year-on-year decline of 1mn b/d, while OPEC still anticipates modest growth. Rigzone's analysis of prior consecutive monthly downgrades highlights how unusual this level of sustained revision is historically.

What Is OPEC's 2027 Demand Outlook?

OPEC has upgraded its 2027 growth forecast to 1.73mn b/d, projecting total consumption of 107.86mn b/d, signalling confidence in a post-conflict demand rebound.

What Happens If Hormuz Disruption Persists?

OPEC's demand figures imply a large supply deficit this year if Middle Eastern production remains constrained at current levels, which would sustain upward pressure on crude prices even against a backdrop of weaker demand growth.

Reading the Market Stress Test in Real Time

What the 2026 cycle in which OPEC downgrades oil demand forecast reveals, when examined as a sequence rather than a series of isolated events, is that the global energy system is undergoing a real-time stress test of its resilience to concentrated geopolitical shock. Three successive cuts in demand expectations, each driven by the same underlying conflict, indicate that the disruption has been deeper, more persistent, and more economically contagious than the initial modelling anticipated.

The demand destruction in the Middle East has proven more entrenched than early forecasts suggested. The China and India growth narrative has been materially interrupted, though not permanently derailed, a distinction that OPEC's 2027 upgrade reflects clearly. Non-OPEC+ supply stability, particularly from the United States, Brazil, and Guyana, has provided a partial buffer that has prevented the supply shock from translating into an even more severe price event.

What remains unresolved is whether the partial recovery in OPEC+ production observed in June will be sustained, reversed, or accelerated. In addition, each successive time OPEC downgrades oil demand forecast expectations, the question sharpens: is this a temporary trough, or the beginning of a longer structural reset? The answer depends not on market fundamentals in any conventional sense, but on geopolitical decisions being made in Washington and Tehran that no demand model can reliably anticipate.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts and projections referenced herein are subject to material uncertainty and should not be relied upon as the sole basis for any investment or trading decision. Independent financial advice should be sought where appropriate.

Want to Stay Ahead of the Commodity Discoveries Driving Market Moves?

While OPEC's demand revisions reshape global energy narratives, significant mineral discoveries on the ASX continue to create compelling opportunities for investors — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment those discoveries are announced, turning complex data across more than 30 commodities into clear, actionable insights. Explore Discovery Alert's dedicated discoveries page to understand how historic finds have generated substantial returns, and begin a 14-day free trial to position yourself ahead of the broader market.