August 3, 2026

When the World's Most Important Oil Corridor Goes Dark

Global energy infrastructure has always contained a single, irreplaceable vulnerability that planners and policymakers have long acknowledged but never fully solved. The concentration of petroleum export capacity through a narrow maritime passage in the Persian Gulf represents the most consequential single point of failure in the modern global economy. When that passage closes, the ripple effects extend far beyond oil markets, touching food systems, aviation networks, manufacturing supply chains, and consumer price levels across dozens of nations simultaneously.

The OPEC+ oil output hike after Hormuz closure that has now occurred three consecutive months in a row presents a study in institutional messaging under conditions where the institution's core tool has been rendered temporarily inoperable. Understanding why the group continues approving quota increases when its largest members physically cannot export more oil requires looking beyond the barrel count and into the strategic logic of managing market expectations during geopolitical crises.

When big ASX news breaks, our subscribers know first

What the 188,000 bpd Quota Increase Actually Represents

There is a fundamental distinction in energy markets that retail investors and general audiences rarely encounter but which underpins the entire OPEC+ decision-making architecture. A production quota is an authorised ceiling, not a physical delivery commitment. When a member nation receives a quota of, say, 10 million barrels per day, that figure represents the maximum the cartel's framework permits that country to produce. It says nothing about what can be exported, refined, or delivered to buyers.

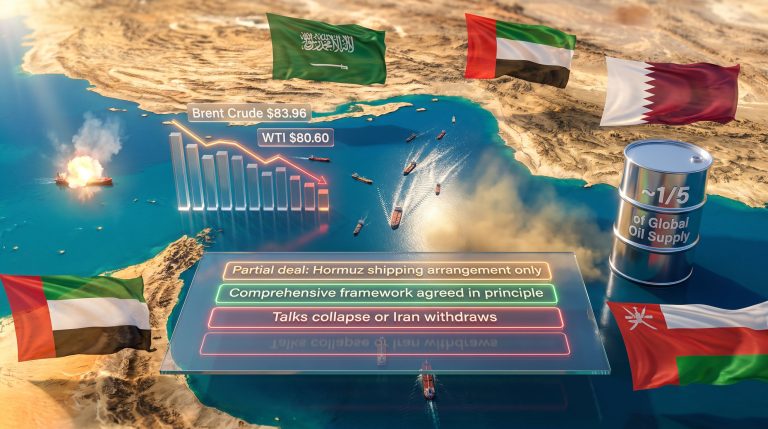

This distinction becomes decisive under the current conditions created by the U.S.-Iran conflict that began on February 28, 2026. Seven OPEC+ member nations reached an in-principle agreement to raise collective output targets by approximately 188,000 barrels per day for June 2026, according to reporting by Reuters. This follows the same pattern established over the preceding two months, with a slightly larger adjustment of approximately 206,000 bpd having been approved for May.

The June quota adjustment is the third consecutive monthly increase approved since the Strait of Hormuz was effectively closed to Gulf oil exports. Each of these decisions has been approved under conditions where the producers holding the bulk of surplus capacity cannot physically deliver additional barrels to international markets.

The core issue is straightforward: Saudi Arabia, Iraq, and Kuwait collectively hold the largest reserves of spare production capacity within OPEC+. Before the conflict erupted, these three nations were also identified as the only members within the group realistically positioned to increase actual output. With Hormuz closed, their export terminals are cut off from the global tanker network. A quota increase approved in Vienna or Riyadh does not change the physical reality in the Persian Gulf.

Furthermore, OPEC's influence on oil markets extends well beyond simple barrel counts, encompassing strategic signalling, geopolitical positioning, and long-term market architecture — all of which remain operative even when physical export capacity is constrained.

The Seven Nations Behind the Decision

The nations driving OPEC+ production decisions have recently shifted from an eight-nation coalition to seven following the UAE's departure from the group. The current decision-making core and their respective disruption exposure looks like this:

| Member Nation | Export Route Status | Capacity to Benefit From Quota Hike |

|---|---|---|

| Saudi Arabia | Severely constrained via Hormuz | Minimal, primary terminals inaccessible |

| Iraq | Heavily disrupted, southern terminals offline | Minimal, near-total Gulf dependence |

| Kuwait | Significantly constrained | Minimal, no viable alternative routing |

| Russia | Alternative routes via Black Sea/Baltic | Moderate, not directly Hormuz-exposed |

| Kazakhstan | Caspian pipeline and China routes | Moderate, limited disruption |

| Algeria | Mediterranean export access intact | Functional, largely unaffected |

| Oman | Gulf of Oman access, partially constrained | Partial, some routing flexibility |

This table reveals an asymmetry that shapes everything about the current OPEC+ dynamic. The three members facing the most severe disruption are precisely those holding the greatest surplus capacity. Meanwhile, the four members with viable export access hold less spare capacity. The quota hike, in practical terms, authorises producers who cannot export to produce more, while the producers who can export have less room to increase.

How the Hormuz Closure Restructured Global Supply Overnight

The Strait of Hormuz has long occupied a unique position in global energy security literature, described by analysts across institutions including the U.S. Energy Information Administration as the world's most strategically significant maritime oil chokepoint. Under normal operating conditions, an estimated 20 to 21 percent of global petroleum liquids transit through the strait on a daily basis. This is not a marginally important corridor. It is the primary artery through which the world's largest oil-exporting region connects to global demand centres in Asia, Europe, and beyond.

When the U.S.-Iran conflict escalated and effective closure of the strait followed, the simultaneous disruption of Saudi Arabia, Iraq, Kuwait, and the UAE's export pathways represented a category of supply shock with no directly comparable modern precedent. Previous Gulf disruptions typically involved a single nation's production. The Iran-Iraq War in the 1980s affected primarily Iranian and Iraqi output. What has not happened before at this scale is the simultaneous severing of export access for the four largest Persian Gulf producers in a single event.

The oil market disruption risks stemming from this conflict consequently extend well beyond conventional supply-side analysis, introducing cascading vulnerabilities that touch virtually every sector of the global economy. The production data released by OPEC itself confirmed the magnitude of the disruption. Collective OPEC+ crude output averaged 35.06 million barrels per day in March 2026, representing a decline of approximately 7.70 million bpd from February levels, according to OPEC's own monthly reporting.

To contextualise that 7.70 million bpd figure: it is roughly equivalent to simultaneously removing the entire combined production of Iraq and the UAE from global markets. In a single calendar month, the world lost access to a volume of oil that, under normal circumstances, would take years of coordinated production cuts to achieve deliberately.

This is not a supply reduction driven by geology, technological failure, or deliberate coordination. It is supply destruction driven entirely by export infrastructure access being severed at a chokepoint. The distinction matters because it means productive capacity still exists. The oil is in the ground or in storage. The problem is purely logistical, which is simultaneously reassuring and alarming, since the timeline for reopening is entirely contingent on geopolitical resolution, not engineering.

The Price Mechanics Behind $125 Oil

Energy market price theory distinguishes sharply between two types of bull markets in crude oil: those driven by demand growth, and those driven by supply destruction. Demand-led cycles tend to develop gradually as economic activity expands, industrial consumption increases, and transportation fuel demand rises. Supply destruction cycles are structurally different, typically producing faster, sharper price movements because the price signal is responding to a sudden gap between what buyers need and what is physically available.

The current environment reflects supply destruction mechanics. Crude oil price trends have followed precisely this pattern, with crude surging to a four-year high above $125 per barrel in the week following the conflict's full market impact being priced in, as reported by Reuters. Futures markets responded not by pricing in short-term volatility with a rapid mean reversion expectation, but by pricing in multi-month disruption scenarios. This is the signature of professional traders who have assessed that normalisation will not occur quickly even after active hostilities conclude.

The downstream consequences extend well beyond crude pricing:

| Downstream Sector | Nature of Impact | Projected Timeline |

|---|---|---|

| Aviation (jet fuel) | Shortage risk and acute price escalation | 1 to 2 months |

| Petrochemicals | Feedstock cost surge, margin compression | Near-term |

| Agricultural inputs | Fertiliser price inflation, food cost transmission | 1 to 3 months |

| Global freight | Fuel surcharge increases across shipping lanes | Immediate to near-term |

| Consumer inflation (CPI) | Broad-based price level pressure | 1 to 4 months |

The aviation sector faces particular structural vulnerability. Jet fuel is primarily refined from light crude grades, a significant share of which comes from Middle Eastern production. With those grades inaccessible to global refiners, alternative crude feedstocks produce different refinery yields. Refiners cannot simply substitute heavy North American crude and achieve equivalent jet fuel output without significant processing adjustments, and refinery configuration changes are neither fast nor cheap.

Why Fertiliser and Food Are Directly Exposed

A less commonly understood transmission mechanism connects crude oil disruptions to agricultural inflation. Natural gas, which is often co-priced with oil in certain regional markets, feeds directly into ammonia and urea fertiliser production. When energy costs surge and supply chains destabilise, fertiliser manufacturing costs rise. That cost increase transmits to farmers, then to food producers, and ultimately to consumer prices. The lag between an oil supply shock and a grocery store price change is typically measured in months, meaning the full inflationary impact of the Hormuz closure may not be visible in CPI data until mid-to-late 2026.

The UAE's Exit and What It Reveals About OPEC+'s Internal Tensions

The UAE's formal departure from OPEC+, finalised in the days immediately before the June quota decision, did not occur in a vacuum. It reflects a structural tension that has been building within the group's allocation framework for years. In addition, it signals a broader set of grievances about how the quota system handles members whose productive capacity has grown substantially since baselines were originally established.

OPEC+ production quotas are assigned based on baseline capacity assessments calibrated at the time each member joined the production management framework. For rapidly developing producers whose capacity has grown substantially since those baselines were set, the quota system creates a structural disadvantage. A country constrained by a quota assigned to its earlier self effectively subsidises other members' market share at its own expense.

The UAE argued precisely this case, maintaining that its actual production capacity had grown considerably beyond the baseline reflected in its quota allocation. The group's response was apparently insufficient to address these concerns, consequently leading to formalised departure.

Critically, OPEC+ is proceeding with production decisions without UAE participation. The group now comprises 21 members including Iran, though Iran's own production is directly affected by the conflict. This raises longer-term questions about whether other high-capacity members harbouring similar quota grievances might pursue comparable exits as the conflict reshapes the group's internal dynamics.

Reading OPEC+'s Signal: Three Distinct Strategic Functions

It would be analytically insufficient to characterise the OPEC+ oil output hike after Hormuz closure as purely symbolic without examining what these decisions are actually designed to accomplish. The June quota increase serves at least three distinct strategic functions operating in parallel.

-

Market Confidence Signalling: By maintaining the institutional process of regular quota adjustments, OPEC+ communicates readiness to restore supply once conditions permit. This messaging suppresses the risk of panic-driven price escalation that might otherwise emerge if the group appeared paralysed or rudderless.

-

Post-Conflict Positioning: Establishing a formal restoration schedule before hostilities conclude means that when Hormuz reopens, production ramp-up can proceed under a pre-agreed framework. Without this advance work, post-conflict supply restoration would require emergency negotiations among fractious members under time pressure.

-

Institutional Continuity: Maintaining the quota adjustment cycle preserves the decision-making architecture and member relationships during a period of both geopolitical disruption and membership change. Suspension of the process could introduce uncertainty about whether the framework itself remains viable.

Gulf oil executives and global commodity traders have consistently communicated that even after the strait reopens, flow normalisation will take several weeks, and potentially several months, to fully materialise. This reflects the layered technical requirements of recommissioning export infrastructure after an extended shutdown.

For the quota hike to transition from symbolic to operational, four distinct sequential prerequisites must be satisfied: active conflict must cease; maritime safety certification and mine-clearing operations through Hormuz must be completed; loading terminal operations at Saudi, Iraqi, and Kuwaiti export facilities must recommission; and tanker fleets must reposition to service restored routes. Each step carries an independent timeline, meaning the aggregate normalisation window could extend well beyond any individual ceasefire announcement.

The next major ASX story will hit our subscribers first

How Investors and Energy Market Participants Should Interpret Symbolic Quota Decisions

There is a useful analogy in monetary policy for understanding how quota decisions function under current conditions. When central banks engage in forward guidance during financial crises, they communicate future intentions to shape present-day expectations even when immediate policy tools have limited direct effect. The Federal Reserve's verbal commitment to accommodative policy during periods of financial stress can stabilise markets even before a single dollar of asset purchase occurs.

OPEC+ quota increases during Hormuz closure function analogously. They shape market expectations and signal institutional intent without immediately altering the physical supply-demand balance. Markets typically process these signals in two phases: an initial sentiment-driven response where the promise of future supply generates mild price softening, followed by a reassessment phase where physical supply realities reassert upward price pressure. The sustained $125+ per barrel environment suggests markets have already moved through the initial response.

However, understanding oil's role in the global economy is essential for contextualising why these quota signals carry such outsized influence on consumer prices, industrial margins, and monetary policy decisions across dozens of nations simultaneously.

The risk scenarios facing global energy markets span a wide range of outcomes with materially different price implications:

| Scenario | Assessed Probability | Crude Price Implication |

|---|---|---|

| Hormuz reopens within 30 days | Low to moderate | Rapid correction of $20 to $30 per barrel possible |

| Conflict extends 3 to 6 months | Moderate to high | Sustained $120 to $140 per barrel range |

| Secondary supply disruptions emerge elsewhere | Low | Potential spike beyond $150 per barrel |

| Coordinated strategic reserve releases by IEA members | Moderate | Temporary suppression of $10 to $15 per barrel |

Disclaimer: Probability assessments and price range projections are speculative in nature and reflect analytical scenarios rather than confirmed forecasts. Energy market conditions are highly sensitive to geopolitical developments that are inherently unpredictable. This content does not constitute financial advice.

A Less-Discussed Risk: The Tanker Fleet Repositioning Problem

One element of the normalisation timeline that receives relatively little attention in mainstream energy coverage is the tanker fleet logistics dimension. The Very Large Crude Carrier (VLCC) fleet that services Persian Gulf export routes does not sit idle waiting for a reopening signal. During an extended Hormuz closure, these vessels redeploy to alternative routes, enter floating storage arrangements, or reposition to service Atlantic Basin or West African loading programmes.

When the strait reopens, the logistical process of returning sufficient tanker capacity to Gulf loading ports adds meaningful weeks to the normalisation timeline, independent of the geopolitical resolution itself. This means that even a sudden, clean ceasefire announcement would not immediately translate into normalised supply flows. The price response to a reopening announcement would likely precede the actual physical supply normalisation by weeks, creating a potential spread between market pricing and physical reality.

OPEC+'s Structural Limitation: When the Quota System Cannot Function

The Hormuz crisis has exposed a fundamental architectural constraint within OPEC+'s production management framework. The entire quota system rests on an implicit assumption that authorised production can be translated into delivered supply. When geopolitical events sever the export infrastructure of multiple core members simultaneously, that assumption breaks down entirely.

The geopolitical trade tensions surrounding this conflict have consequently accelerated conversations in energy ministries and policy circles about whether existing frameworks require substantial redesign to remain relevant during major geopolitical disruptions. Furthermore, for major oil-importing economies, the crisis accelerates long-running conversations about strategic petroleum reserve adequacy, geographic diversification of import sources, and the pace of energy transition investment as a supply security measure.

For producers outside the Gulf corridor, including those in North America, West Africa, the North Sea, and the Caspian region, the disruption has created a temporary but commercially significant window to capture market share that displaced Gulf volumes can no longer serve. The longer-term institutional question for OPEC+ is whether an organisation whose core production management tool becomes temporarily non-functional during major geopolitical events needs new frameworks for maintaining market relevance during those periods. That conversation is likely already underway in the corridors of member nation energy ministries, even if it has not yet surfaced in formal communiqués.

This article is based on reporting by Reuters as published by ET EnergyWorld on May 3, 2026, and supplementary analysis of publicly available energy market data. Forward-looking statements, scenario projections, and price range estimates are analytical in nature and do not constitute investment advice. Energy markets carry significant geopolitical and macroeconomic risks. Readers should conduct independent research and consult qualified financial advisors before making investment decisions.

Want To Stay Ahead of Market-Moving Commodity Discoveries Before the Broader Market Catches On?

While geopolitical shocks like the Hormuz closure reshape global energy supply chains, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across 30+ commodities and delivering actionable alerts directly to subscribers — start your 14-day free trial at Discovery Alert today, or explore how historic mineral discoveries have generated extraordinary returns to understand the full opportunity.