July 7, 2026

When Quotas Become Theoretical: The Real Story Behind Five Consecutive OPEC+ Output Hikes

Global oil markets have always operated on a fundamental tension between announced policy and physical reality. Production quotas, compliance targets, and supply agreements are instruments of intent, not guarantees of delivery. That gap between stated ambition and actual barrel flows has rarely been wider than it is today, and understanding why requires examining the structural mechanics of how OPEC+ manages supply — and what happens when a geopolitical shock makes those mechanisms almost entirely irrelevant to near-term market conditions.

The fifth consecutive OPEC+ output hike, approved for August 2026, is best understood not as a reaction to current market conditions but as the continuation of a pre-programmed unwinding sequence. The decision follows an identical formula applied in March, April, May, June, and July, each adding 188,000 barrels per day (bpd) to the collective quota ceiling of seven core member nations. Yet for much of this period, the physical barrels those quotas represent have had nowhere to go.

When big ASX news breaks, our subscribers know first

The Mechanics of the Unwinding: What the Hike Cycle Actually Represents

To interpret the OPEC+ output hike cycle correctly, it helps to understand that OPEC+ production restraint exists in two distinct layers. The first layer — the deeper and older of the two — consists of the official cuts of approximately 2 million bpd agreed in October 2022 in response to deteriorating demand expectations. The second layer consists of voluntary cuts totalling roughly 1.65 million bpd introduced in 2023 by a subset of members seeking additional price support.

The current monthly hike sequence targets exclusively the second layer. At 188,000 bpd per cycle, the voluntary cut tranche is being methodically reversed across a multi-month schedule. If this pace is maintained, the full 1.65 million bpd of voluntary reductions will be unwound by late September 2026, at which point the group faces a far more consequential decision: whether to begin dismantling the October 2022 official cuts as well.

The monthly allocation breakdown across the seven active producers reveals the structured, formulaic nature of this process:

| Member Country | Monthly Output Increase (Aug 2026) |

|---|---|

| Saudi Arabia | +62,000 bpd |

| Russia | +62,000 bpd |

| Iraq | +26,000 bpd |

| Kuwait | +16,000 bpd |

| Kazakhstan | +10,000 bpd |

| Algeria | +6,000 bpd |

| Oman | +5,000 bpd |

| Total | +188,000 bpd |

Crucially, these country-level allocations have remained identical across five consecutive monthly decisions, from March through July 2026. This is not adaptive policymaking. It is the mechanical execution of a pre-committed schedule, which carries significant implications for how the market should interpret each announcement.

The cumulative build across the April through August 2026 window is substantial on paper:

| Month | Incremental Increase | Cumulative Increase (Apr–Aug) |

|---|---|---|

| April 2026 | +188,000 bpd | +188,000 bpd |

| May 2026 | +188,000 bpd | +376,000 bpd |

| June 2026 | +188,000 bpd | +564,000 bpd |

| July 2026 | +188,000 bpd | +752,000 bpd |

| August 2026 | +188,000 bpd | ~800,000 bpd |

The ~800,000 bpd cumulative increase across this window is a meaningful volume in ordinary conditions. In current conditions, however, it is largely theoretical.

Why Does This Schedule Keep Running?

OPEC's market influence extends well beyond any single monthly decision. The repetitive nature of the hike cycle reflects a deliberate internal consensus-building strategy. By locking members into a fixed formula, the group avoids reopening politically difficult negotiations every thirty days, consequently preserving coalition cohesion under stress. Furthermore, OPEC demand forecasts have played a central role in justifying the pace of this unwinding, with the group consistently projecting sufficient demand recovery to absorb returning barrels.

The Strait of Hormuz Disruption: Why Paper Quotas Have Decoupled from Physical Supply

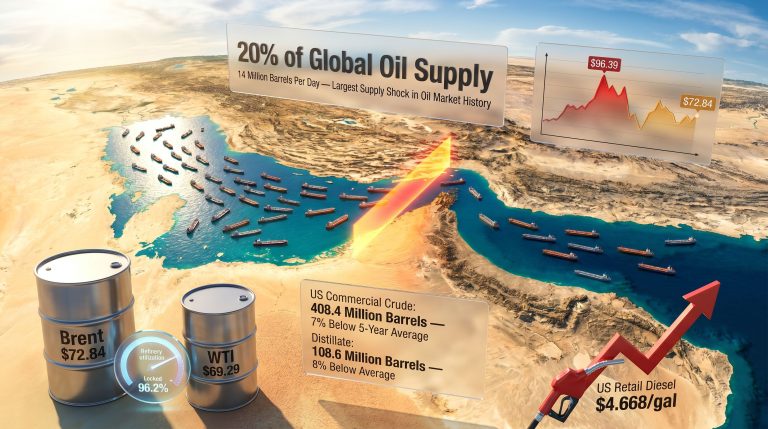

The Strait of Hormuz has historically served as the world's most critical oil and gas transit corridor, carrying approximately one-fifth of global oil and liquefied natural gas supplies before the onset of the US-Israeli conflict with Iran. When that artery closed to tanker traffic, the consequences for OPEC+ members with Persian Gulf export terminals were immediate and severe.

As unshipped barrels accumulated at export facilities with finite storage capacity, producers were forced to physically curtail output regardless of what their quota ceilings permitted. The result was a production collapse of historic proportions. Total OPEC+ output fell from 42.77 million bpd in February 2026 to 33.13 million bpd in May 2026, a reduction of nearly 9.64 million bpd according to OPEC's own figures.

Against that backdrop, the cumulative quota increase of approximately 800,000 bpd across the April-August period represents less than 9% of the volume lost to the Hormuz disruption. The announced hikes are therefore not adding barrels to the market. They are updating a theoretical ceiling that bears little relationship to current physical flows. Al Jazeera's reporting on OPEC's output decisions following the attacks underscores just how cautious the group's recovery language has remained throughout this period.

Neil Crosby, Oil Market Analyst at Sparta Commodities in Singapore, has characterised OPEC+ quota decisions as carrying essentially no short-term significance under current conditions, with their relevance only becoming material once a durable resolution to the Hormuz situation emerges, at which point the group's supply intentions will require fundamental reassessment against 2027 market balances.

This framing captures a dynamic that professional traders are already pricing. Brent crude futures for September delivery stood at approximately US$72/b in early July 2026, marginally below the pre-conflict settlement price of US$72.48/b recorded on February 27, 2026. The fact that Brent has not collapsed to reflect a 9.64 million bpd supply shock reflects the market's forward-looking nature: traders are discounting the eventual reopening of the strait and the supply surge that follows.

The UAE's Departure and the Governance Vacuum It Left Behind

Complicating the picture further is the structural change to OPEC+ membership that occurred in late April 2026, when the UAE formally exited the group to align its production more directly with its actual capacity. At the time of its departure, the UAE was the group's third-largest producer, and its voice within internal deliberations had served as a moderating force in debates over quota policy.

The practical consequences of that exit extend in two directions. First, a quota-free UAE is positioned to scale output aggressively in line with its own investment cycle, without coordinating those increases with the broader OPEC+ framework. This introduces a significant wildcard into 2027 supply projections. Second, the internal governance architecture of the group has weakened precisely at the moment when it faces its most complex supply management challenge in years.

Iraq's simultaneous push for higher quota allocations compounds this dynamic. Iraq receives the third-largest monthly allocation in the current hike structure at 26,000 bpd, yet Baghdad has historically produced above its assigned ceiling and continues to seek upward revisions. With a moderating UAE voice absent and Iraq pressing for quota expansion, the coalition's capacity to enforce internal discipline is under genuine stress.

Scenario Modelling: Three Paths Through the Post-Hormuz Transition

The most consequential variable for global oil markets through 2027 is not the incremental OPEC+ output hike schedule. It is the speed and completeness of the Strait of Hormuz reopening, and the supply dynamics that follow. Broader oil price geopolitics have consistently demonstrated that physical supply disruptions of this magnitude reshape market structures for years, not months.

Three scenarios frame the realistic range of outcomes:

Scenario A: Gradual Reopening (Base Case)

- Hormuz traffic normalises incrementally over a 3-6 month window

- Strategic petroleum reserve (SPR) restocking and commercial inventory rebuilding absorbs the initial supply return

- Brent stabilises in the US$65-72/b range through the first half of 2027

- OPEC+ maintains the voluntary cut unwinding schedule and defers any decision on official cuts

Scenario B: Rapid Reopening and Quota Compliance Failure

- Multiple OPEC+ members simultaneously attempt to reach quota levels as physical access is restored

- A quota-free UAE independently accelerates output expansion

- The combination of returning OPEC+ barrels, UAE ramp-up, and stronger US shale output creates a surplus environment

- Rystad Energy projects a potential surplus of approximately 5 million bpd in the months immediately following a full reopening

- Brent faces downside pressure toward sub-US$60/b, threatening fiscal breakeven levels for members including Iraq and Algeria

Scenario C: Prolonged Closure and Structural Realignment

- Hormuz restrictions persist beyond the third quarter of 2026

- Global supply chains accelerate rerouting through alternative corridors

- The US shale slowdown dynamic reverses as producers capitalise on sustained elevated pricing to meaningfully expand output

- OPEC+ cohesion fractures under mounting fiscal pressure, particularly among lower-income members

Rystad Energy's Head of Geopolitical Analysis, Jorge Leon, has projected that once Hormuz flows normalise, OPEC+ could theoretically progress from unwinding voluntary cuts to dismantling the official 2-million-bpd framework agreed in October 2022. However, Leon has warned that the market may be structurally unable to absorb that volume, with the confluence of recovering OPEC+ supply, stronger US shale production, and demand destruction from an extended period of elevated prices potentially generating a surplus of historic proportions. Leon has also noted that SPR restocking could temporarily delay but not eliminate this surplus risk.

The SPR Buffer: A Delay Mechanism, Not a Structural Solution

One factor that will soften the initial impact of any Hormuz reopening is the strategic petroleum reserve restocking cycle. Nations that drew down government-held emergency reserves during the supply disruption will prioritise refilling those stockpiles before commercial market dynamics fully reassert themselves. This absorptive capacity could temporarily offset 1-2 million bpd of returning supply in the months immediately following normalisation.

However, SPR restocking is a time-limited buffer. Once reserves are rebuilt to target levels, that absorptive demand disappears. The surplus risk is consequently deferred rather than structurally resolved, and markets pricing a Hormuz reopening need to account for the distinction between the initial restocking period and the medium-term supply-demand balance that follows it.

The next major ASX story will hit our subscribers first

The Shale Dimension: OPEC+'s Self-Defeating Price War Risk

Embedded within the OPEC+ output hike cycle is a second strategic objective beyond internal quota discipline. Saudi Arabia and Russia, as the two largest quota holders in the current structure with 62,000 bpd each per monthly increment, have historically used production policy as a tool for applying competitive pressure on US shale producers.

The economics of this strategy rest on a critical threshold. Many US shale operators require Brent prices above approximately US$55-65/b to sustain drilling economics, depending on basin location and operator cost structure. Furthermore, the oil market trade war context adds an additional layer of complexity to how Saudi Arabia and Russia calibrate this competitive pressure against geopolitical considerations.

The self-defeating risk is that OPEC+ members with higher fiscal breakeven requirements — particularly Iraq — face budget shortfalls before US shale operators are forced to meaningfully curtail activity. Pushing prices below the level at which fiscal discipline becomes unsustainable internally, before external competitors are squeezed out, is the perennial trap in OPEC+ price war strategies. Reuters reporting on the fourth quota hike since the Hormuz closure highlighted precisely this tension, noting member nations' diverging fiscal pressures as a growing source of internal friction.

2027 Market Balance: Key Risk Variables at a Glance

| Variable | Bullish Scenario | Bearish Scenario |

|---|---|---|

| Hormuz Reopening Speed | Gradual (6-12 months) | Rapid (1-3 months) |

| UAE Independent Output | Infrastructure-constrained | Aggressive ramp-up |

| US Shale Response | Flat at sub-US$65 Brent | Expansion above US$70 Brent |

| OPEC+ Quota Compliance | High (above 90%) | Low (below 75%) |

| Global Demand Recovery | Strong post-conflict rebound | Structural demand destruction |

| Estimated 2027 Surplus | 1-2 million bpd | 4-5 million bpd |

Frequently Asked Questions: OPEC+ Output Hike Explained

What is the OPEC+ output hike and why does it keep happening monthly?

The current OPEC+ output hike cycle is a pre-scheduled, formulaic unwinding of voluntary production cuts originally agreed in 2023. Seven core member nations — Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, and Oman — each receive fixed monthly quota increments totalling 188,000 bpd per cycle. The repetition reflects a pre-committed structural normalisation, not reactive policymaking.

How much has OPEC+ increased production in 2026?

Announced quota increases total approximately 800,000 bpd across the April-August 2026 window. Physical output reaching global markets remains far below pre-conflict levels due to the Strait of Hormuz disruption, which forced a production decline of nearly 9.64 million bpd between February and May 2026.

Why are oil prices relatively stable if OPEC+ is effectively offline?

Futures markets are forward-pricing the eventual Hormuz reopening and the anticipated supply surplus that follows, rather than pricing current physical scarcity at full premium. This is a classic example of futures markets discounting a known future event, consequently compressing the price response that the present physical shortage would otherwise generate.

What happens to OPEC+ if the Strait of Hormuz reopens rapidly?

A rapid reopening creates the conditions for a substantial surplus, potentially reaching approximately 5 million bpd in the months following normalisation, driven by returning OPEC+ supply, unconstrained UAE output growth, and stronger US shale production. SPR restocking will provide a temporary absorptive buffer, but this delays rather than eliminates the surplus pressure.

What is the difference between OPEC+ voluntary cuts and official cuts?

The voluntary cuts, totalling approximately 1.65 million bpd, were introduced in 2023 and are currently being reversed at 188,000 bpd per month. The official cuts of approximately 2 million bpd were agreed in October 2022 and have not yet entered the unwinding schedule. If both layers are reversed, the combined supply addition would be well beyond what current demand projections can absorb.

Key Metrics Summary

| Metric | Value |

|---|---|

| Monthly hike increment per cycle | 188,000 bpd |

| Cumulative increase (Apr-Aug 2026) | ~800,000 bpd |

| OPEC+ output drop (Feb-May 2026) | ~9.64 million bpd |

| Brent crude (early July 2026) | ~US$72/b |

| Pre-conflict Brent benchmark (Feb 27, 2026) | US$72.48/b |

| Projected post-Hormuz peak surplus risk | ~5 million bpd |

| Voluntary cuts being unwound | ~1.65 million bpd |

| Official cuts (Oct 2022, not yet unwinding) | ~2 million bpd |

| Active monthly production managers | 7 core members |

| Full OPEC+ membership | 21 nations |

Three structural conclusions define the analytical landscape. The OPEC+ output hike cycle is pre-committed, not reactive, and each monthly announcement carries little information content beyond confirming the schedule is on track. Physical supply and announced quotas are currently operating in separate realities, divided by the Strait of Hormuz closure in a way that makes standard supply-demand modelling almost entirely dependent on geopolitical assumptions. And the defining market event of the coming 12-18 months is not the hike schedule itself, but what materialises the moment Hormuz fully reopens — when accumulated surplus pressure is released into a market that has not yet priced its full magnitude.

This article contains forward-looking analysis, scenario projections, and market commentary that involve inherent uncertainty. Readers should not interpret any content herein as financial or investment advice. Oil market conditions, geopolitical developments, and OPEC+ policy decisions can change rapidly, and actual outcomes may differ materially from scenarios discussed.

Want to Stay Ahead of the Next Major Commodity Shift?

While oil markets navigate the complexities of OPEC+ quota mechanics and Hormuz disruption dynamics, significant mineral discovery opportunities continue to emerge on the ASX — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment they hit the market, turning complex data across 30+ commodities into clear, actionable insights. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.