May 22, 2026

The Battery Material Hidden in Plain Sight

The global conversation around electric vehicle batteries has long centred on lithium, cobalt, and nickel. Investment theses, government policy frameworks, and media narratives have been built around these materials for years. Yet one material consistently underrepresented in that discourse quietly constitutes the single largest component by weight in every lithium-ion cell ever manufactured. Graphite, the workhorse of the battery anode, makes up roughly 30% of a lithium-ion battery's total weight and serves as the physical medium through which energy is stored and released with every charge cycle. The Orbia graphite recycling plant in the UK is now emerging as a pivotal response to this long-overlooked challenge.

Understanding why graphite has been overlooked requires understanding how battery economics have historically been framed. Lithium commands headlines because it is the namesake element. Cobalt attracts scrutiny due to its ethical sourcing complexity. Nickel draws attention because of its density and cost volatility. Graphite, by contrast, has a relatively low per-unit market price, which has made it commercially invisible within the recycling value chain, despite being the most voluminous material in the cell. This asymmetry between physical volume and economic recovery attention is precisely what makes the current moment in graphite recycling so significant.

When big ASX news breaks, our subscribers know first

Why the Graphite Supply Problem Demands Urgent Attention

The Scale of China's Dominance

The structural vulnerability underlying the graphite supply shortage is not subtle. Approximately 95% of both natural and synthetic graphite processed for battery applications originates from China. This concentration is not a recent development — it reflects decades of industrial investment in extraction, processing, and purification infrastructure that Western economies did not prioritise during the same period.

The consequences of this concentration are now becoming concrete. China's export restrictions on graphite, introduced in late 2023, sent immediate shockwaves through battery supply chains in Europe, Japan, South Korea, and the United States, forcing manufacturers to accelerate contingency planning. Unlike disruptions to lithium or cobalt supply, where multiple geographies offer viable alternatives, there is currently no established second-tier supplier capable of absorbing meaningful volume at battery-grade specifications.

A 2035 Deficit That Changes the Strategic Calculus

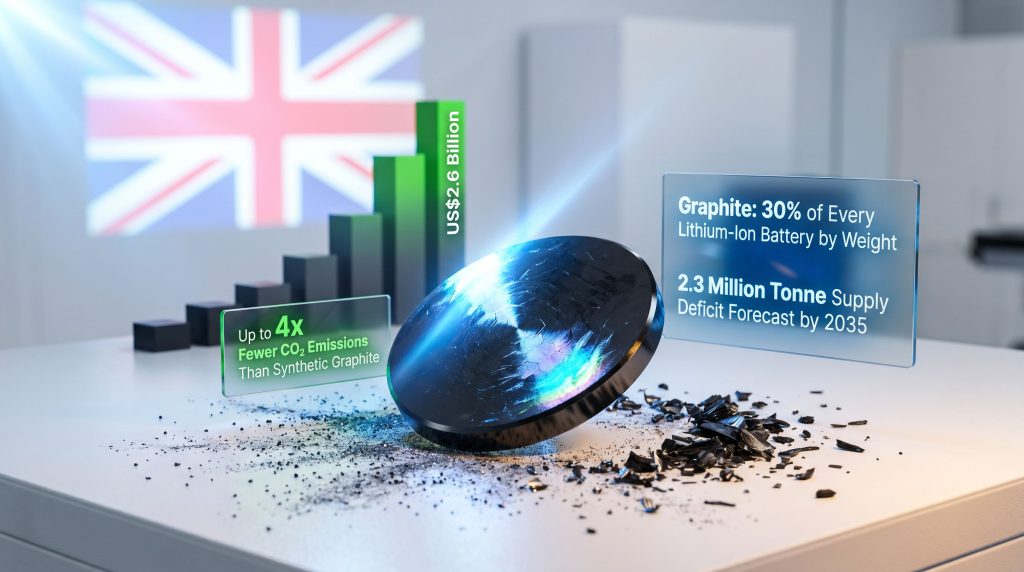

Demand projections make the supply picture considerably more urgent. Global graphite demand is forecast to exceed available supply by approximately 2.3 million tonnes annually by 2035. To contextualise that figure: global graphite production for battery applications was roughly 350,000 tonnes in 2023. A deficit nearly seven times current annual output, compounding across the decade, represents a structural supply failure rather than a temporary market imbalance.

The UK faces a particularly acute version of this exposure. Without domestic mining capacity for graphite and without established recycling infrastructure, the nation's battery manufacturing ambitions rest almost entirely on uninterrupted access to Chinese-processed material. Consequently, closing that gap requires building recovery infrastructure that can transform end-of-life battery material into usable feedstock at industrial scale.

What Orbia's UK Graphite Recycling Plant Actually Does

The Pilot Facility and Its Strategic Purpose

The Orbia graphite recycling plant in the UK represents the country's first dedicated facility targeting graphite recovery from spent lithium-ion batteries. Funded through a £1.4 million (approximately US$1.87 million) UK Government grant via the DRIVE35 programme, the facility is being developed by Orbia's Fluor and Energy Materials (FEM) division and is expected to begin operations in early 2026, with initial outputs later in the year.

The facility will initially operate at kilogram-scale output, functioning as a proof-of-concept installation rather than an industrial production site. This staged approach is deliberate. Demonstrating technical robustness and commercial feasibility at pilot scale creates the evidence base required to attract the larger capital commitments needed for industrial-scale infrastructure. Orbia has been explicit that this pilot is the groundwork for a future full-scale plant.

| Funding Detail | Value |

|---|---|

| UK Government Grant | £1.4m (approx. US$1.87m) |

| Parent Programme | DRIVE35 |

| Total DRIVE35 Programme Budget | £4bn (approx. US$5.4bn) |

| Delivery Partners | Department for Business and Trade, Advanced Propulsion Centre UK, Innovate UK |

| Initial Facility Scale | Kilogram-scale pilot |

| Operations Commencement | Early 2026 |

Orbia FEM and Its UK Research Base

Orbia FEM is a specialised division of the broader Orbia group, focused on advanced battery materials including electrolytes, solvent systems, and lithium-ion cell component development. The company operates an existing research and development hub in Chester, England, where battery technologies are advanced across multiple chemistries. This established UK presence provides the scientific and engineering infrastructure that underpins the graphite recycling initiative, giving the programme access to decades of accumulated expertise in industrial-scale fluorine-based chemistry — a capability that proves directly relevant to the purification process at the heart of this technology.

How Graphite Recycling Works: The Technical Process

From Spent Battery to Black Mass

The recycling pathway begins with the mechanical processing of end-of-life lithium-ion batteries. When spent cells are fed into industrial shredders, the output is a heterogeneous mixture known as black mass — a dark powder containing all the active materials from both the cathode and anode components of the cell. Black mass typically includes lithium, cobalt, nickel, manganese, and graphite, alongside aluminium, copper, and various binders and electrolyte residues.

The critical challenge is that graphite in black mass is not battery-grade. It has been physically degraded through cycling, contaminated with impurities from adjacent materials, and mixed with substances that must be removed before the graphite can re-enter the battery supply chain. Conventional battery recycling operations focus primarily on recovering the cathode metals, meaning the graphite fraction has historically been treated as a residual waste stream rather than a valuable recovered material.

Purification Through Fluorine Chemistry

Orbia's proprietary process specifically targets the graphite fraction within black mass, using a multi-step purification approach based on hydrofluoric acid chemistry. This is where the company's industrial heritage becomes a genuine differentiator. Orbia has operated at the frontier of complex fluorine-based industrial chemistry for decades, and the expertise required to handle, control, and optimise hydrofluoric acid processes at scale represents a significant technical barrier to entry.

The purification sequence progressively removes metallic contaminants, organic residues, and structural damage products from the graphite particles, restoring the material to a purity level comparable to virgin battery-grade specifications. Furthermore, the resulting product is described as ultra-high-purity graphite, functionally indistinguishable from freshly processed natural or synthetic graphite at the anode specifications required by cell manufacturers. These recycled graphite products are gaining increasing traction across the industry.

How Recycled Graphite Compares to Virgin Alternatives

One of the most commercially compelling aspects of the Orbia process is its carbon credentials. Early assessments indicate that the recovered graphite generates substantially fewer carbon emissions than both primary production routes.

| Graphite Type | Production Route | Relative CO₂ Emissions |

|---|---|---|

| Synthetic Graphite | Petroleum by-products, graphitisation at up to 3,000°C | Highest (baseline) |

| Mined Natural Graphite | Extraction, refinement, chemical processing | Up to 2x lower than synthetic |

| Orbia Recycled Graphite | Black mass extraction, fluorine-based purification | Up to 4x lower than synthetic |

The significance of this emissions reduction cannot be overstated for automotive OEM procurement teams. Net-zero manufacturing targets increasingly require material-level carbon accounting, and a battery anode material that reduces associated emissions by a factor of four compared to the synthetic alternative offers a compelling sustainability proposition alongside its supply chain resilience benefits.

The Commercial Opportunity: A Market Built From Waste

The 2030 Recovery Window

The scale of the commercial opportunity in graphite recycling is frequently underestimated because the feedstock is currently treated as waste. By 2030, projections suggest that more than 236,000 tonnes of graphite could be available annually for recovery from end-of-life batteries reaching the end of their useful service life. Translated into market value, this represents a potential US$2.6 billion addressable opportunity in recycled graphite supply alone, before accounting for value-added processing margins.

The timing reflects the deployment curve of first-generation EVs. Vehicles sold in the mid-2010s are now reaching end-of-life battery replacement cycles, and the volume of cells entering recycling streams will grow exponentially through the late 2020s as higher-volume model years from 2018 to 2022 mature. This creates a growing and increasingly predictable feedstock availability profile that industrial recyclers can plan around.

Why Graphite Has Been Left Behind Until Now

The economics of battery recycling have historically been constructed around cobalt and nickel — metals with high enough per-unit values to justify the cost of complex hydrometallurgical processing. Graphite's comparatively lower market price meant that recovery was rarely commercially viable when evaluated against the cost of processing black mass specifically for the graphite fraction.

Orbia's approach disrupts this calculus in two ways. First, it integrates graphite recovery into the broader black mass processing workflow rather than treating it as a standalone operation with independent cost justification. Second, it produces a material with verified environmental credentials that command a premium from manufacturers operating under carbon reduction commitments, effectively creating a new pricing layer on top of the commodity graphite value. The broader battery raw materials landscape is similarly shifting in response to these emerging recovery economics.

The DRIVE35 Framework and the UK's Industrial Strategy

What DRIVE35 Represents

The DRIVE35 programme is a £4 billion (approximately US$5.4 billion) UK government initiative designed to accelerate the development and commercialisation of zero-emission transport technologies. Administered through a partnership between the Department for Business and Trade, the Advanced Propulsion Centre UK, and Innovate UK, the programme provides structured grant funding to companies developing capabilities across the clean transport value chain.

Ian Constance, CEO of the Advanced Propulsion Centre UK, has articulated the programme's intent as converting world-class innovation into tangible industrial capability, with an explicit emphasis on building sovereign supply chain resilience rather than simply funding laboratory research. The framing positions DRIVE35 not as a research subsidy but as an industrial development instrument.

Supply Chain Sovereignty as a Strategic Objective

The graphite recycling initiative sits within a broader UK ambition to reduce import dependency for critical battery materials. The nation currently has no domestic graphite mining capacity and no established processing infrastructure for battery-grade graphite. Combined with the 95% Chinese market concentration, this creates a compounded vulnerability that affects not only automotive manufacturing but also energy storage deployment and grid-scale battery projects.

Building domestic recovery infrastructure addresses this exposure through a circular economy mechanism rather than a mining development pathway. Rather than attempting to develop greenfield graphite extraction in geologically challenging territories, the UK strategy routes investment through end-of-life material recovery, using domestically generated waste as the feedstock source. In addition, the growing critical minerals demand driven by the energy transition makes this domestic focus all the more strategically important.

From Pilot to Industrial Scale

The pathway from kilogram-scale pilot to industrial production is not merely a matter of building larger equipment. It requires:

- Demonstrating consistent product quality at scale sufficient to satisfy battery manufacturer qualification requirements

- Establishing contractual supply relationships with OEM partners willing to offtake recovered material

- Securing the capital investment required for full industrial infrastructure

- Building regulatory frameworks for the handling and processing of black mass at commercial volumes

- Developing workforce capabilities in a sector that did not previously exist in the UK

The DRIVE35 pilot grant accelerates the first of these steps by funding the technical demonstration that underpins everything downstream.

The next major ASX story will hit our subscribers first

Orbia's Global Graphite Recycling Ambitions

The North American Parallel Programme

The UK initiative does not exist in isolation. Orbia is simultaneously advancing graphite recycling infrastructure in North America through a separate programme involving a US$125 million Department of Energy cost-sharing grant in partnership with Ascend Elements, a battery materials specialist focused on closed-loop recovery systems. This parallel programme operates at a more advanced development stage than the UK pilot, reflecting the US DOE's earlier and larger-scale investment in battery recycling infrastructure.

| Dimension | UK Pilot (DRIVE35) | US Programme (DOE Grant) |

|---|---|---|

| Funding Source | UK Government via DRIVE35 | US Department of Energy |

| Grant Value | £1.4m (US$1.87m) | US$125m (cost-sharing) |

| Partner Organisation | Advanced Propulsion Centre UK | Ascend Elements |

| Development Stage | Pilot / kilogram-scale | Advanced development |

| Strategic Goal | UK domestic supply chain | North American battery supply chain |

Why Multi-Geography Infrastructure Matters

The parallel development of graphite recycling infrastructure across multiple jurisdictions reflects an emerging consensus that supply chain sovereignty for critical battery materials cannot be achieved through a single national programme. OEMs operating global production platforms require regional supply chain redundancy, meaning that a recycled graphite supplier capable of serving facilities in both Europe and North America commands structural commercial advantages over geographically constrained alternatives.

Orbia's multi-geography approach positions the company to serve this demand, with the UK pilot acting as the European proof-of-concept and the North American programme establishing the commercial template that the UK facility will ultimately scale toward. The broader battery recycling outlook reinforces the view that multi-regional recovery infrastructure will become a defining feature of future battery supply chains.

Building the Circular Battery Economy

The OEM Partnership Model

The commercial model Orbia is developing for recovered graphite centres on direct circular supply agreements with automotive manufacturers and cell producers. Rather than selling into commodity graphite markets where pricing is set by Chinese production costs, this model establishes bilateral relationships where recovered graphite is purchased specifically for its provenance, purity, and carbon credentials.

For automotive OEMs, these agreements serve multiple strategic functions:

- They provide a verified source of low-carbon anode material that supports Scope 3 emissions reduction targets

- They create geographic supply chain diversification that reduces dependence on Chinese-processed graphite

- They contribute to circular economy reporting metrics increasingly demanded by institutional investors and regulators

- They establish a closed-loop relationship between the OEM's end-of-life battery collection infrastructure and its new cell procurement

The Net-Zero Procurement Dimension

The intersection of carbon reduction commitments and critical materials supply is creating an entirely new procurement category in the automotive industry. Materials that can demonstrate verified lifecycle emissions reductions while meeting technical performance specifications are increasingly treated as strategic assets rather than commodity inputs.

Recycled graphite that generates up to four times fewer carbon emissions than synthetic alternatives, and that can be sourced from domestic waste streams rather than Chinese processing facilities, satisfies both dimensions of this emerging procurement framework simultaneously. This dual value proposition may ultimately prove more commercially significant than the raw material cost economics alone. For further context on how this space is evolving, Battery Tech Online's coverage of Orbia's breakthrough offers useful additional detail.

Frequently Asked Questions

What is the Orbia graphite recycling plant in the UK?

It is the UK's first dedicated facility for recovering graphite from end-of-life lithium-ion batteries. Developed by Orbia's Fluor and Energy Materials division with £1.4 million in UK Government funding via the DRIVE35 programme, the facility will purify graphite extracted from battery black mass to battery-grade specifications. Initial operations are expected to begin in early 2026.

What is black mass and why does it matter for graphite recovery?

Black mass is the powdered residue produced when spent lithium-ion batteries are mechanically shredded. It contains all the active materials from the cell, including the graphite anode fraction. Historically, recycling operations focused on recovering cathode metals from black mass, leaving the graphite as a waste stream. Orbia's process specifically targets the graphite fraction within black mass for recovery and purification.

How does recycled graphite compare in quality to virgin graphite?

Orbia's purification process produces graphite described as ultra-high-purity and functionally equivalent to virgin battery-grade material. The recovered graphite meets the performance specifications required for battery anode applications and generates up to four times fewer carbon emissions than synthetic graphite produced through conventional high-temperature graphitisation processes.

Why does the UK need domestic graphite recycling capability?

Approximately 95% of global battery-grade graphite supply is processed in China. The UK has no domestic graphite mining capacity, meaning its battery manufacturing sector currently depends entirely on imported material. Building domestic recovery infrastructure through recycling creates a sovereign supply pathway using domestically generated end-of-life batteries as feedstock, reducing geopolitical supply risk.

What is the DRIVE35 programme?

DRIVE35 is a £4 billion UK Government initiative to develop and commercialise zero-emission transport technologies. It is delivered through a partnership between the Department for Business and Trade, the Advanced Propulsion Centre UK, and Innovate UK, providing structured grant funding to companies building capabilities across the clean transport supply chain.

Key Signals for Battery Materials Investors

The Orbia graphite recycling plant in the UK carries implications that extend well beyond a single pilot facility announcement. Taken in aggregate, several structural signals emerge:

- Graphite constitutes approximately 30% of a lithium-ion battery by weight, making it the largest single material component, yet it has been systematically excluded from battery recycling economics due to its lower per-unit market value relative to cathode metals

- A projected 2.3 million tonne supply deficit by 2035 creates structural demand urgency for domestic recovery infrastructure that cannot be resolved through mining development alone within the required timeframe

- The US$2.6 billion addressable market available from graphite recovery by 2030 represents a commercially significant opportunity that has been largely ignored by the recycling industry until now

- Orbia's fluorine-based purification process produces material with up to four times lower CO₂ emissions than synthetic graphite, creating a carbon premium that may exceed the commodity price differential over time

- The parallel development of graphite recycling programmes in the UK and North America simultaneously suggests that the industry is entering a period of accelerated infrastructure investment across multiple jurisdictions

- Supply chain sovereignty is emerging as a discrete valuation factor for battery materials investments, separate from commodity price fundamentals, as governments and OEMs assign strategic premiums to domestically processed critical materials

Disclaimer: This article contains forward-looking statements, market projections, and supply-demand forecasts from third-party sources. These represent estimates and analytical assessments rather than confirmed outcomes. Readers should conduct independent research before making investment or commercial decisions based on this content. Market conditions, technological developments, and policy frameworks are subject to change.

Want to Stay Ahead of the Next Major Battery Materials Discovery?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements across more than 30 commodities — including battery materials like graphite — delivering real-time alerts on significant mineral discoveries before the broader market reacts; explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.