June 4, 2026

Malaysia's eastern state emerges as a strategic focal point for developing a comprehensive Pahang rare earth processing hub, capitalising on substantial mineral reserves and established infrastructure capabilities. The region's unique positioning combines non-radioactive ionic-clay deposits with existing processing facilities to create an integrated supply chain solution for global critical minerals energy security requirements.

Geographic Advantages and Infrastructure Positioning

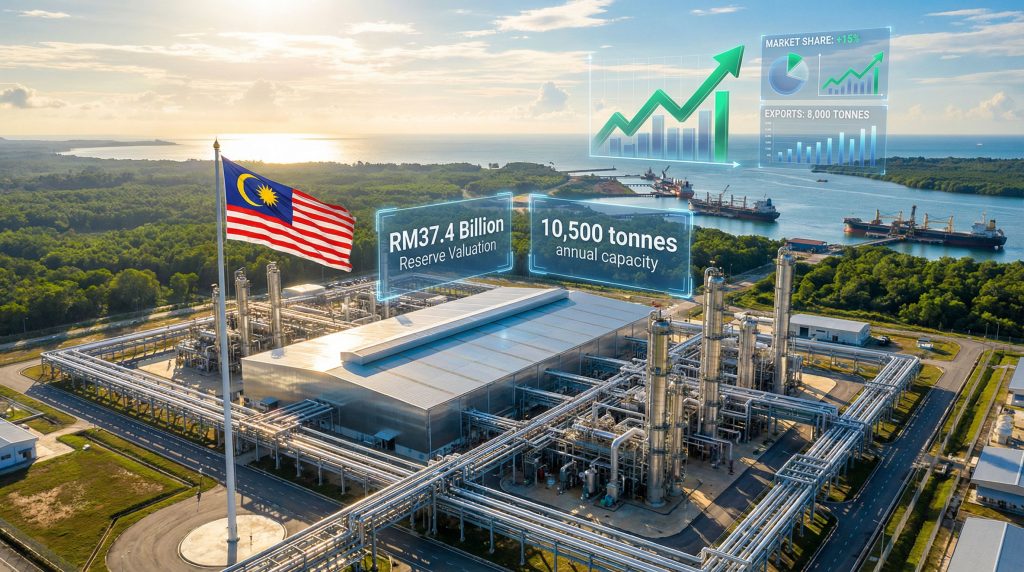

Malaysia's eastern peninsular coast offers distinctive logistical advantages for rare earth processing operations. The Port of Kuantan provides deep-water access with maximum draft capabilities reaching 14.5 metres, enabling direct Panamax-class vessel operations without transshipment requirements. This infrastructure supports efficient international shipping logistics for both rare earth concentrates and processed materials.

The facility's location within the Gebeng Industrial Zone provides established utility infrastructure including dedicated power supply averaging 85-90 MW capacity utilisation, fresh water sourcing from the Kuantan River through industrial treatment systems, and waste-water processing meeting Malaysian Environmental Quality Act standards. Strategic proximity to regional manufacturing hubs places operations within 400-500 kilometres of Singapore's petrochemical clusters and 1,200-1,400 kilometres from South Korean magnet manufacturing regions.

Existing Processing Capabilities and Technical Infrastructure

Since September 2012, the Gebeng facility has maintained operations as the world's largest rare earth processing installation outside China, with annual production capacity of approximately 10,500 tonnes of rare earth oxide equivalent. Furthermore, the facility employs sophisticated solvent extraction methodology specifically designed for lanthanide-bearing concentrates.

Processing technology encompasses multi-stage operations including:

- Cracking Stage: Conversion of rare earth carbonate precursors into soluble chlorides through hydrochloric acid treatment

- Separation Stage: Multi-stage solvent extraction using tributyl phosphate and kerosene carriers to fractionate light rare earths from heavy rare earths

- Purification: Counter-current extraction achieving >99% purity specifications for magnet manufacturers and industrial applications

The facility maintains on-site storage capacity for approximately 3-6 months of feedstock and 2-3 months of finished product inventory, providing operational flexibility and market response capabilities.

When big ASX news breaks, our subscribers know first

Vertical Integration Model Analysis

Malaysia's strategic positioning reflects broader regional industrial consolidation trends observed across Southeast Asia. Indonesia's state-owned nickel industrial parks demonstrate vertical integration from mining through smelting to downstream refining within single jurisdictions. Similarly, Vietnam's government-coordinated rare earth separation represents national supply chain consolidation efforts since 2011.

The proposed Pahang rare earth processing hub model would theoretically encompass upstream ionic-clay mining producing rare earth carbonate concentrates, midstream cracking and solvent extraction for fractionation into high-purity oxides, and downstream manufacturing converting materials to rare earth salts, metals, alloys, or permanent magnets.

Processing margin economics demonstrate significant value-addition potential:

| Processing Stage | Input Value | Output Value | Value Addition |

|---|---|---|---|

| Raw Carbonate | US$6,456/tonne | Base material | – |

| Separated Oxides | US$6,456/tonne | US$9,684/tonne | 50% margin |

| Magnet-grade Material | US$9,684/tonne | US$32,280/tonne | 400% premium |

Regulatory Framework and Permitting Structure

Malaysia's June 2025 approval of Non-Radioactive Rare Earth Elements mining Standard Operating Procedures establishes the first formalised regulatory framework specifically addressing ionic-clay extraction outside radioactive thorium-bearing ore systems. This regulatory advancement provides operational clarity for companies seeking to develop non-radioactive rare earth projects, offering valuable mining permitting insights for industry stakeholders.

The multi-layered approval structure requires coordination between Pahang State Executive Council for land releases, Forestry Department Peninsular Malaysia for forest reserve permits, and Malaysian Department of Environment for environmental impact assessments. This framework reflects lessons learned from earlier public opposition to thorium-bearing rare earth operations.

Market Pricing Analysis and Valuation Methodology

Pahang's disclosed reserves encompass approximately 1.4 million tonnes of ionic-clay rare earth bearing material valued at RM37.4 billion (US$7.9 billion at December 2025 exchange rates). Current mixed rare earth carbonate pricing of US$6,456 per tonne aligns with late-2025 market conditions following price stabilisation from 2022-2023 volatility.

Historical pricing context reveals significant market cyclicality:

- 2020-2021: REE carbonate prices ranged US$4,000-$5,500/tonne

- 2022-2023: Prices spiked to US$7,000-$9,000/tonne due to supply concerns

- 2024-2025: Stabilised around US$6,000-$7,000/tonne as supply chains normalised

Reserve distribution presents both opportunities and challenges, with approximately 70% located within federally protected forest reserves and 30% on state land or private concessions. Consequently, this geographic distribution necessitates comprehensive environmental impact assessments and community engagement processes.

Investment Risk Assessment Framework

The RM37.4 billion valuation represents theoretical maximum value based on current spot market pricing with several critical assumptions requiring validation. These include 100% extraction success rates, stable market pricing, and minimal environmental remediation costs. However, industry experience suggests typical recovery rates range from 60-85% for ionic-clay rare earth extraction.

Reserve classification accuracy indicates the 1.4 million tonnes figure represents inferred resources under mineral resource terminology standards. This represents the lowest confidence category and may vary by ±30-50% pending detailed geological confirmation. In addition, conversion to measured resources or proven reserves typically requires extensive drilling, metallurgical testing, and economic feasibility studies.

Key risk factors include:

- Geological uncertainty in inferred reserves versus proven resources

- Environmental compliance costs for forest reserve operations estimated at 12-15% of operational expenses

- Technology transfer requirements and local content mandates affecting foreign investment structures

- Market volatility in rare earth pricing and demand cycles affecting project economics

Upstream Mining Potential Analysis

Pahang hosts geologically significant ionic-clay rare earth deposits concentrated in weathered granitic terrains across districts including Kuantan, Raub, Lipis, Jerantut, and Cameron Highlands. These deposits contain commercially relevant concentrations of light and medium rare earths including neodymium, praseodymium, dysprosium, and terbium essential for permanent magnet applications.

Non-radioactive classification provides distinct advantages over traditional rare earth sources containing thorium and uranium. This characteristic simplifies regulatory approval processes, reduces environmental monitoring requirements, and improves public acceptance compared to radioactive-bearing alternatives. Furthermore, understanding the broader context of mining industry evolution helps position this development within global technological advancement trends.

Ionic-clay extraction methodology typically involves in-situ leaching or heap leaching technologies producing rare earth carbonate or hydroxide concentrates with 40-60% rare earth oxide content. Malaysia's approach would likely employ centralised processing of pre-concentrated feeds rather than in-ground leaching methods used in Chinese operations.

Midstream Processing Dominance

Malaysia maintains the only fully permitted cracking and leaching facility outside China, providing established technical expertise in lanthanide separation processes. Quality control standards meet international specifications required by magnet manufacturers, defence contractors, and clean energy technology producers.

Processing capacity expansion potential exists within existing infrastructure constraints. The Gebeng facility operates with power, water, and waste treatment systems designed for current throughput levels. Consequently, significant capacity increases would require infrastructure upgrades and additional environmental permitting.

Comparative analysis with global processing capabilities reveals Malaysia's unique position:

- China: Produces 120,000-140,000 tonnes rare earth oxides annually through in-situ leaching and heap leaching

- Malaysia: Operates 10,500 tonnes annual capacity through centralised solvent extraction

- Other regions: Limited operational processing capacity outside pilot-scale facilities

RM600 Million Super Magnet Factory Development

The partnership between Malaysian entities and South Korean JS Link represents strategic downstream integration targeting 3,000 tonnes annual production of neodymium-iron-boron magnets. This initiative positions Malaysia to capture higher value-addition margins compared to raw material or intermediate product exports.

Technology transfer agreements typically include licensing of proprietary magnet manufacturing chemistry, training programmes for local technical workforce, and shared research and development agreements for process optimisation. Joint intellectual property ownership or technology-access clauses may limit re-export of manufacturing know-how.

Market positioning against Chinese magnet manufacturers requires competitive advantages in quality, delivery reliability, or cost structure. However, Malaysia's geographic proximity to Asian electronics and automotive manufacturing provides logistical benefits compared to Western magnet producers. The development of such facilities aligns with establishing a comprehensive critical raw materials facility framework for regional supply chain resilience.

Value Chain Integration Opportunities

Malaysia's unique configuration combines upstream non-radioactive rare earth potential with established midstream separation capacity and emerging downstream manufacturing capabilities. No other nation outside China currently maintains this integrated structure across the entire value chain.

"Strategic positioning enables Malaysia to serve as both supplier and processor, reducing dependency on single-source materials while capturing multiple margin layers throughout the production sequence."

Integration benefits include reduced transportation costs between processing stages, coordinated quality control throughout the value chain, and enhanced supply chain security for international customers seeking non-Chinese sources.

Forest Reserve Development Protocols

Environmental impact assessment requirements for forest reserve operations encompass biodiversity protection measures, water management systems for ionic-clay leaching, and indigenous community consultation processes. Malaysia's regulatory framework reflects heightened environmental awareness following historical mining controversies.

Biodiversity protection measures include offset programmes compensating for habitat disruption, wildlife corridor preservation, and endangered species monitoring protocols. These requirements increase project development timelines and capital costs but provide social licence for operations in environmentally sensitive areas.

Water management systems require careful design for ionic-clay leaching operations, which typically consume significant volumes of process water. Treatment and recycling systems must meet stringent discharge standards to protect local waterways and aquatic ecosystems.

Public Acceptance and Regulatory Compliance

Historical public opposition to thorium-bearing rare earth processing provides important lessons for non-radioactive project development. Transparent monitoring and reporting frameworks, community engagement programmes, and independent environmental oversight help build social acceptance.

Thorium-free processing advantages significantly improve community relations by eliminating radioactive waste concerns and reducing long-term environmental monitoring requirements. This distinction proves crucial for securing local government support and maintaining operational permits.

International environmental certification pathways through organisations like the International Finance Corporation or Equator Principles provide additional credibility for environmentally responsible operations. These certifications often facilitate access to international financing and customer acceptance.

The next major ASX story will hit our subscribers first

Government Partnership Models

State-controlled processing hub ownership structures reflect broader regional trends toward resource nationalism and strategic industry control. Indonesia's nickel industrial parks and Vietnam's rare earth consolidation provide precedents for government participation in critical mineral value chains.

Public-private partnership frameworks typically balance government strategic objectives with private sector operational expertise and capital investment. Foreign investment limits and local content requirements ensure domestic benefit capture while maintaining access to international technology and markets.

Technology transfer and skills development mandates create long-term capacity building within local communities. Training programmes for technical workforce, research and development partnerships with universities, and knowledge transfer protocols enhance national capabilities beyond immediate project operations.

Market Positioning Strategies

Competition with Chinese integrated producers requires differentiated value propositions including supply chain reliability, quality consistency, and geopolitical risk mitigation. Malaysia's democratic governance structure and legal framework provide stability compared to alternative supply sources.

Collaboration opportunities with Western supply chain initiatives include participation in critical minerals partnerships, technology sharing agreements, and coordinated stockpiling programmes. These relationships enhance market access while supporting broader strategic objectives.

ASEAN regional rare earth cooperation frameworks enable resource sharing, technology transfer, and coordinated development approaches. Regional coordination reduces individual country risk while building collective capabilities across Southeast Asia.

Development Phase Projections

Project development timelines reflect complex permitting requirements and infrastructure development needs. Environmental assessments and permitting processes typically require 18-24 months for forest reserve operations, followed by infrastructure development and facility construction phases.

Projected Timeline:

- 2025-2026: Environmental impact assessments, community consultations, and detailed permitting

- 2027-2028: Infrastructure development, facility construction, and equipment installation

- 2029-2030: Commissioning, ramp-up operations, and commercial production initiation

- 2031+: Full-scale integrated operations achieving design capacity

Capital investment requirements for integrated rare earth processing facilities typically range US$500 million to US$1.2 billion depending on capacity and processing complexity. Malaysia's existing infrastructure provides cost advantages compared to greenfield development in remote locations.

Furthermore, the development aligns with broader initiatives for establishing Australia critical minerals strategic reserve capabilities, creating complementary regional supply chain networks.

Key Performance Indicators for Success

Monitoring metrics include permitting approval timelines, processing capacity utilisation rates, international market share gains, and environmental compliance performance. Community acceptance ratings and workforce development indicators provide social sustainability measures.

Environmental compliance metrics encompass water quality monitoring, air emissions tracking, waste management efficiency, and biodiversity impact assessment. Regular third-party auditing ensures transparency and maintains operational permits.

Production performance indicators include processing recovery rates, product quality specifications, customer satisfaction scores, and operational cost benchmarking against international competitors. These metrics demonstrate operational excellence and market competitiveness.

Geopolitical Supply Chain Diversification

Western nations' China dependency reduction strategies create market opportunities for alternative rare earth suppliers. Malaysia's established processing capabilities and democratic governance structure align with diversification objectives of allied nations seeking reliable supply sources.

ASEAN critical minerals cooperation initiatives enable collective bargaining power and coordinated development strategies. Regional partnerships reduce individual project risks while building economies of scale across multiple countries and resource types.

Technology alliance partnerships through frameworks like AUKUS or Quad nations provide access to advanced processing technologies, research collaboration, and market development support. These relationships enhance competitiveness while supporting broader strategic alliance objectives.

Long-term Strategic Positioning

Malaysia's development as an Asia-Pacific Pahang rare earth processing hub depends on successful integration of upstream resources, midstream processing excellence, and downstream manufacturing capabilities. This positioning enables participation in global clean energy transition supply chains.

Competitive advantages in non-radioactive processing provide differentiation from traditional rare earth sources containing thorium and uranium. This distinction proves increasingly important as environmental regulations tighten and public awareness increases.

Regional supply chain resilience building through ASEAN coordination creates backup capabilities and alternative routing options during supply disruptions. However, Malaysia's strategic geographic position enables flexible supply arrangements serving both Eastern and Western markets.

Disclaimer: This analysis contains forward-looking statements based on current information and industry projections. Rare earth market conditions, regulatory environments, and technological developments may vary significantly from current expectations. Investment decisions should consider comprehensive due diligence and professional financial advice.

Looking to Capitalise on Asia's Rare Earth Revolution?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant critical minerals and rare earth discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, then begin your 30-day free trial today to position yourself ahead of the market.