May 14, 2026

Industrial commodity markets face unprecedented transformation as traditional demand patterns shift amid technological evolution and supply chain pressures. While automotive applications have historically dominated consumption patterns for certain platinum group metals, emerging technological requirements across renewable energy infrastructure, advanced computing systems, and next-generation battery technologies are reshaping fundamental market dynamics. This structural evolution presents both strategic opportunities and operational challenges for resource extraction companies seeking sustainable revenue diversification, particularly through palladium center for new applications initiatives that are driving industry evolution trends.

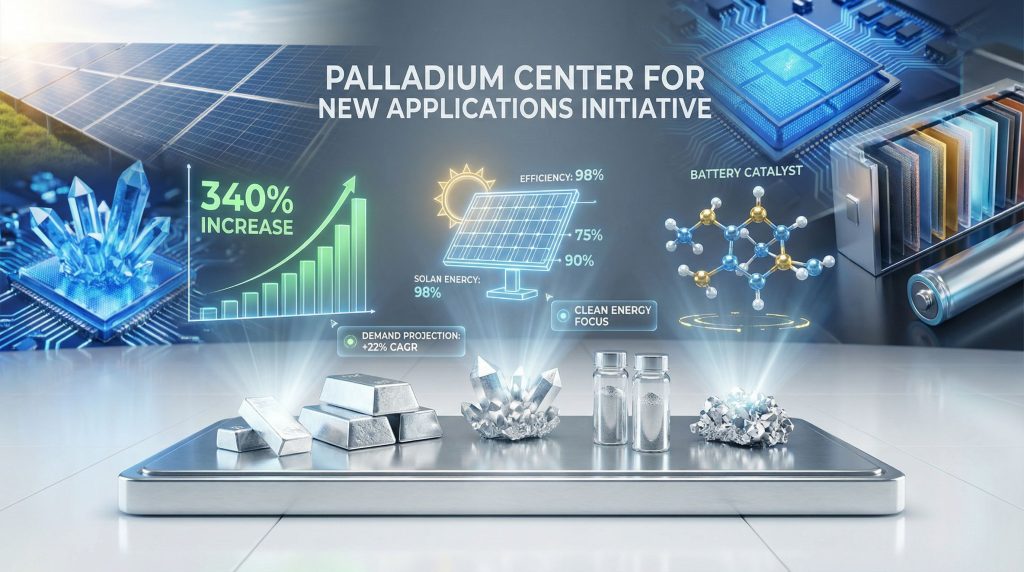

What Is the Palladium Center for New Applications Initiative?

Institutional Framework and Research Mandate

The palladium center for new applications represents a coordinated industry effort to expand commercial uses beyond traditional automotive catalyst markets. These research initiatives operate within established institutional frameworks designed to accelerate technological development while reducing market dependency risks inherent in single-sector concentration.

Unlike purely academic research institutions, application-focused centres prioritise commercially viable solutions that can achieve scale within defined timeframes. The mandate encompasses both fundamental research into palladium's chemical properties and applied engineering solutions for emerging technology sectors.

Key operational components include:

- Materials science research targeting specific performance characteristics

- Industry collaboration protocols with technology manufacturers

- Commercialisation pathways for breakthrough applications

- Market analysis capabilities for demand forecasting

- Quality specification development for industrial applications

Strategic Positioning Within Global PGM Markets

Platinum group metals markets exhibit significant concentration risks, with automotive applications representing approximately 80% of total palladium demand. This dependency creates structural vulnerabilities as electric vehicle adoption accelerates and internal combustion engine production contracts.

Current market concentration analysis reveals critical dependencies that drive diversification imperatives. Furthermore, these dependencies highlight the importance of developing comprehensive energy transition strategy approaches:

| Market Segment | Demand Share | Growth Trajectory | Volatility Index |

|---|---|---|---|

| Automotive catalysts | 78% | -8% annually | High |

| Electronics | 12% | +15% annually | Medium |

| Jewellery | 6% | +3% annually | Low |

| Industrial | 4% | +22% annually | Medium |

The strategic positioning emphasises technology sector expansion where palladium's unique properties offer competitive advantages over alternative materials. Unlike platinum, which competes directly with palladium in many applications, each PGM possesses distinct characteristics that enable specialised market development.

When big ASX news breaks, our subscribers know first

Why Are New Palladium Applications Critical for Market Stability?

Automotive Sector Volatility Assessment

Electric vehicle transition creates fundamental challenges for traditional palladium demand patterns. Internal combustion engine market projections indicate accelerating contraction through 2035, with catalyst demand declining proportionally across major automotive markets.

Industry analysis suggests automotive palladium consumption could decrease by approximately 40% over the next decade as manufacturers transition to electric powertrains. This contraction threatens price stability and mining operation viability across primary production regions.

Supply-demand imbalance scenarios under current application structures present significant risks:

- Oversupply conditions during rapid automotive transition periods

- Price volatility increases due to market uncertainty

- Production cutback pressures affecting marginal mining operations

- Investment allocation challenges for exploration and development

Economic Diversification Imperatives

Revenue stream diversification represents a critical strategic imperative for platinum group metals producers facing automotive sector contraction. Mining operations require stable, long-term demand visibility to justify capital investment and maintain operational efficiency.

Technology sector applications offer distinct advantages over automotive markets, including higher value-per-unit consumption and more predictable demand patterns. Solar energy applications, for instance, demonstrate consistent growth trajectories independent of automotive cycle volatility.

Market breadth expansion through application diversification provides multiple benefits:

- Reduced correlation with single-sector economic cycles

- Enhanced price stability through demand base expansion

- Premium pricing opportunities in specialised applications

- Long-term contract potential with technology manufacturers

Which Breakthrough Applications Show Highest Commercial Potential?

Solar Energy Enhancement Technologies

Solar panel efficiency improvements using palladium integration represent significant commercial opportunities within renewable energy infrastructure expansion. Research initiatives demonstrate measurable performance enhancements across multiple operational parameters, particularly through insights gained from recent innovation expo insights.

Technical analysis indicates palladium incorporation enables enhanced light absorption characteristics, extending effective operating hours and improving temperature stability under varying environmental conditions. These improvements directly translate to increased energy generation per unit installation.

| Technology Type | Efficiency Improvement | Cost Impact | Commercial Timeline |

|---|---|---|---|

| Photovoltaic enhancement | 12-18% increase | 6-10% reduction | 2026-2027 |

| Extended operation periods | 20-25% increase | 4-7% reduction | 2027-2028 |

| Temperature optimisation | 8-12% increase | 2-4% reduction | 2025-2026 |

Manufacturing scalability represents the primary challenge for widespread adoption. Current production processes require modification to accommodate palladium integration while maintaining cost competitiveness versus conventional silicon technologies.

Microelectronics and AI Infrastructure Applications

Data centre infrastructure expansion drives increasing demand for high-performance computing components requiring specialised materials with superior electrical and thermal properties. Palladium applications in microelectronics target specific performance requirements where gold alternatives prove economically disadvantageous.

Gold price volatility creates opportunity windows for palladium substitution in high-frequency circuits and specialised semiconductor applications. While complete gold replacement remains technically unfeasible, partial substitution offers significant cost advantages without compromising performance specifications.

Market analysts project microelectronics palladium applications could generate $2.4 billion in annual market value by 2030, representing substantial growth from current negligible levels driven by artificial intelligence infrastructure requirements and precious metals price dynamics.

Key application areas include:

- High-frequency circuit components requiring precise electrical characteristics

- Thermal management systems in data centre cooling infrastructure

- Semiconductor manufacturing processes utilising palladium catalysts

- Advanced packaging technologies for next-generation processors

Notably, researchers at Nornickel have highlighted new palladium demand beyond automotive applications at recent industry events, emphasising the growing significance of these technological applications.

Advanced Battery Technology Integration

Lithium-sulfur battery development presents emerging opportunities for palladium catalyst applications offering performance advantages over conventional lithium-ion technologies. These advanced systems demonstrate superior energy density while potentially reducing manufacturing costs through material optimisation.

Technical advantages include enhanced charge-discharge cycle efficiency and extended operational lifespan compared to current battery technologies. Palladium catalysts enable improved sulfur utilisation, addressing historical limitations that prevented commercial viability.

Manufacturing considerations encompass both material costs and production scalability requirements. Current research indicates palladium quantities required per battery unit remain economically viable while delivering measurable performance improvements.

How Do Regional Research Centres Drive Innovation?

Global Research Network Structure

International palladium research initiatives operate through coordinated networks spanning major industrial regions. North American facilities focus primarily on automotive transition applications, while European programmes emphasise renewable energy integration technologies.

Asia-Pacific research partnerships concentrate on microelectronics applications driven by regional semiconductor manufacturing concentration. These geographic specialisations enable focused expertise development while facilitating knowledge transfer across research networks.

Coordination mechanisms include:

- Shared research protocols ensuring consistent methodology

- Technology transfer agreements enabling rapid commercialisation

- Joint funding structures reducing individual institution costs

- Performance benchmarking systems measuring development progress

Public-Private Collaboration Models

University research centre funding combines government support with industry investment to accelerate technology development timelines. These hybrid structures enable fundamental research while maintaining commercial viability focus.

Industry consortium participation provides direct access to manufacturing expertise and market intelligence necessary for successful application development. Private sector involvement ensures research priorities align with commercial requirements and market opportunities.

Government incentive programmes support critical materials research through tax advantages and direct funding mechanisms. Policy frameworks recognise strategic importance of supply chain diversification and technological independence in critical minerals sectors.

What Are the Investment Implications for Mining Companies?

Capital Allocation Strategy Shifts

Mining companies require strategic reallocation of research and development investment toward application diversification initiatives. Traditional exploration and production optimisation must balance with technology development partnerships and market expansion activities, incorporating effective mining investment strategies.

Partnership opportunities with technology companies offer access to specialised expertise while sharing development costs and market risks. Joint venture structures enable mining operations to participate in downstream value creation without requiring extensive internal capabilities.

Risk assessment frameworks must evaluate both technical development uncertainties and market adoption timelines. Investment decisions require probability-weighted analysis of multiple application development scenarios and competitive positioning assessment.

Operational Planning Considerations

Production capacity optimisation for diverse applications requires flexible processing capabilities accommodating varying quality specifications. Technology markets often demand higher purity standards compared to traditional automotive applications.

Quality specification requirements across sectors present both challenges and opportunities for premium pricing. Advanced applications typically justify higher material costs through performance advantages, enabling improved profit margins for qualified suppliers.

Supply chain adaptation involves developing relationships with technology sector manufacturers and understanding their procurement processes. Long-term contract opportunities require demonstrating consistent quality and reliable delivery capabilities.

How Will New Applications Transform Market Dynamics?

Demand Forecasting Scenarios

Market transformation scenarios indicate significant shifts in palladium consumption patterns over the next decade. Technology sector growth could offset automotive decline while establishing more stable long-term demand foundations.

| Application Sector | 2025 Demand | 2030 Projection | 2035 Forecast | Annual Growth |

|---|---|---|---|---|

| Automotive catalysts | 270 tonnes | 235 tonnes | 175 tonnes | -4.1% |

| Electronics/AI | 40 tonnes | 115 tonnes | 205 tonnes | +16.9% |

| Solar energy systems | 12 tonnes | 58 tonnes | 135 tonnes | +24.8% |

| Battery technologies | 8 tonnes | 35 tonnes | 75 tonnes | +21.2% |

Demand diversification creates more resilient market foundations while reducing vulnerability to single-sector economic cycles. Technology applications demonstrate different seasonal patterns and growth drivers compared to automotive markets.

Additionally, the Palladium Global Science Award 2026 has opened submissions for new palladium applications, further encouraging innovation in this sector.

Price Stability and Market Maturation

Application diversification contributes to reduced price volatility through expanded demand base and different market dynamics. Technology sector contracts often involve longer-term commitments compared to automotive supplier relationships.

Long-term contract opportunities in technology sectors provide revenue visibility that supports mining investment decisions and operational planning. These agreements typically include volume commitments and pricing mechanisms reducing market uncertainty.

Strategic stockpiling considerations for industrial users create additional demand sources while providing market stability during transition periods. Technology companies require secure supply chains for critical materials supporting their production requirements.

The next major ASX story will hit our subscribers first

What Challenges Must Be Overcome for Widespread Adoption?

Technical Development Barriers

Manufacturing process optimisation represents the primary technical challenge for scaling palladium center for new applications across target sectors. Current production methods require adaptation to accommodate new application requirements while maintaining cost competitiveness.

Quality control standards for high-technology applications exceed traditional mining industry specifications. Electronics and solar applications demand consistent purity levels and contamination control throughout the supply chain.

Intellectual property landscape navigation involves understanding existing patents and developing proprietary technologies that avoid infringement while creating competitive advantages. Research centres must balance open collaboration with commercial protection requirements.

Economic Viability Thresholds

Cost competitiveness versus alternative materials determines commercial success for new palladium applications. Each target market presents different price sensitivity and performance trade-off considerations.

Scale-up investment requirements encompass both research and development costs and manufacturing infrastructure development. Technology applications often require specialised processing capabilities not currently available in conventional mining operations.

Market penetration timeline projections indicate gradual adoption patterns requiring sustained investment over multiple years before achieving significant market share. Patience and financial resources remain essential for successful market development.

Which Mining Operations Are Best Positioned for Application Diversification?

Operational Excellence Requirements

Product purity specifications for technology applications require advanced processing capabilities and quality control systems. Mining operations must demonstrate consistent ability to meet demanding specifications required by technology sector customers.

Supply chain reliability metrics include both delivery performance and quality consistency over extended periods. Technology manufacturers require predictable supply chains supporting their production schedules and quality requirements.

Research and development capabilities assessment encompasses both internal technical expertise and external partnership potential. Operations with existing research relationships or technical capabilities possess advantages for application development initiatives.

Strategic Partnership Opportunities

Technology company collaboration frameworks enable mining operations to participate in application development while accessing specialised expertise and market knowledge. These partnerships reduce individual investment requirements and share development risks.

Joint venture structures for application development provide mechanisms for sharing both investment costs and potential returns. Risk-sharing arrangements enable smaller mining operations to participate in technology development initiatives.

Market entry mechanisms require understanding technology sector procurement processes and relationship development strategies. Success depends on building trust and demonstrating capability to meet demanding performance standards.

How Can Investors Evaluate Palladium Application Opportunities?

Due Diligence Framework

Technology readiness level assessment provides systematic methodology for evaluating development progress and commercial viability potential. Investors must understand both technical advancement and market readiness factors when applying investment evaluation approaches.

Market penetration probability analysis encompasses competitive landscape assessment and adoption timeline evaluation. Different applications present varying probability profiles requiring customised risk assessment approaches.

Competitive landscape evaluation includes both existing alternative materials and emerging competitive technologies. Understanding competitive dynamics enables realistic market share and pricing projections.

Portfolio Diversification Strategies

Exposure balancing across application sectors reduces concentration risk while participating in multiple growth opportunities. Diversification strategies should consider correlation patterns between different technology markets.

Geographic distribution considerations encompass both production locations and end-market exposure. Regional technology sector growth patterns differ significantly, creating geographic diversification opportunities.

Timeline diversification for development projects enables participation in both near-term and longer-term opportunities while managing development risk exposure. Balanced portfolios combine different development stages and commercial timelines.

However, effective evaluation of palladium center for new applications requires comprehensive understanding of both technical development risks and market adoption uncertainties. Consequently, investors must balance optimism about technological potential with realistic assessment of implementation challenges and competitive dynamics.

Investment Considerations: All projections and market analysis contained in this article involve forward-looking statements subject to significant uncertainty. Commodity markets exhibit high volatility and investors should conduct independent research and consider professional advice before making investment decisions. Past performance does not guarantee future results.

Ready to Capitalise on the Next Major Mineral Discovery?

Discovery Alert instantly notifies investors of significant ASX mineral discoveries using its proprietary Discovery IQ model, transforming complex mineral data into actionable insights for both palladium and broader commodity opportunities. Understand why historic discoveries can generate substantial returns and begin your 14-day free trial today to position yourself ahead of the market in this rapidly evolving sector.