August 8, 2026

Peak gold scarcity represents one of the most significant structural challenges facing precious metals markets today. As global demand consistently outpaces mine production, the industry confronts fundamental limitations that distinguish gold from conventional commodities. The convergence of declining ore grades, exhausted reserve bases, and accelerating demand from institutional buyers creates conditions rarely observed in commodity markets.

Unlike conventional commodities where higher prices typically stimulate increased production, gold faces inherent limitations that challenge standard economic assumptions. The convergence of declining ore grades, exhausted reserve bases, and accelerating demand from institutional buyers creates conditions rarely observed in commodity markets. These forces operate simultaneously across multiple timeframes, from immediate operational challenges to multi-decade resource depletion cycles.

What Is Peak Gold Scarcity and Why Does It Matter?

Defining Peak Gold in Economic Terms

Peak gold scarcity differs fundamentally from traditional peak resource theories that focus solely on production decline. The contemporary definition centres on whether annual mined gold supply can satisfy global demand without dependence on recycled material. This metric reveals structural imbalances that production figures alone cannot capture.

In 2024, global gold demand reached 4,974.5 tonnes while mine production delivered 3,661.2 tonnes, creating a 1,312.8-tonne deficit that required jewellery recycling to meet market requirements. This gap persists despite record-high production levels, indicating that peak gold scarcity represents a demand-supply imbalance rather than production decline.

The scarcity framework examines whether mining output can independently satisfy consumption without relying on secondary supply sources. When recycled jewellery becomes essential for market equilibrium, it signals that primary production has reached capacity constraints relative to demand growth.

The Mathematics of Depletion vs. Discovery

Historical discovery patterns reveal alarming trends in new deposit identification. During the 1970s, 1980s, and 1990s, the gold industry discovered at least one deposit containing over 50 million ounces and approximately ten deposits exceeding 30 million ounces each decade.

Since 2000, no deposits of comparable size have been identified, with very few discoveries reaching even 15 million ounces. This discovery drought occurs alongside accelerating reserve depletion at existing operations.

High-grading practices, where mining companies extract the highest-grade accessible areas while leaving lower-grade material, have masked immediate supply problems but accelerated long-term reserve exhaustion.

Discovery Timeline Comparison:

- 1970s-1990s: Multiple 50+ million ounce discoveries per decade

- 2000-2024: Zero discoveries exceeding 50 million ounces

- Current pipeline: Insufficient major deposits to maintain production growth

Why Traditional Supply Models Are Failing

Conventional commodity supply models assume that higher prices incentivise increased exploration and production investment, eventually rebalancing markets. Gold markets demonstrate why these models prove inadequate for resources with long development timelines and geological constraints.

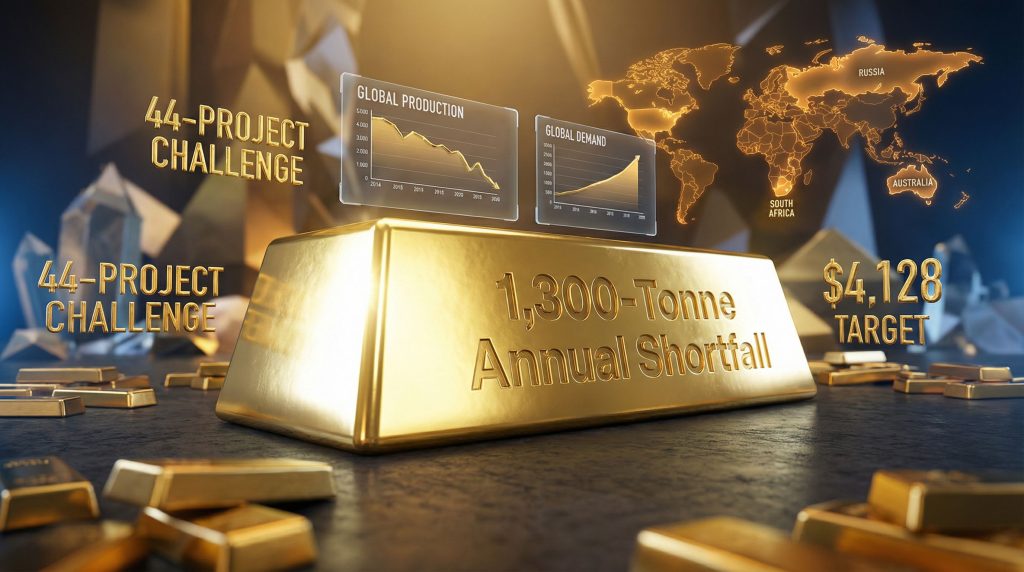

Wood Mackenzie analysis indicates that maintaining current production levels requires 44 gold projects currently in development to advance successfully to production. The consultancy acknowledges that achieving this target appears virtually impossible due to permitting delays, capital allocation priorities, and project scope changes.

Mining capital increasingly favours brownfield expansions over greenfield developments, seeking 50% to 70% faster production timelines. While this strategy provides near-term supply additions, it inherently limits production growth to existing reserve bases rather than expanding the industry's resource foundation.

When big ASX news breaks, our subscribers know first

How Severe Is the Current Gold Production Deficit?

Breaking Down the 1,300-Tonne Annual Shortfall

The magnitude of gold market imbalances becomes apparent when examining annual deficit patterns spanning nearly a decade. Production shortfalls persist consistently, requiring jewellery recycling to bridge supply gaps:

| Year | Demand (tonnes) | Production (tonnes) | Deficit (tonnes) | Recycling (tonnes) |

|---|---|---|---|---|

| 2024 | 4,974.5 | 3,661.2 | 1,312.8 | 1,370 |

| 2023 | 4,898.8 | 3,644.4 | 1,254.4 | 1,237.3 |

| 2022 | 4,741.0 | 3,611.9 | 1,129.1 | 1,144.1 |

| 2021 | 4,021.0 | 3,560.7 | 460.3 | 1,149.9 |

| 2020 | 3,759.6 | 3,400.8 | 358.8 | 1,297.4 |

These figures demonstrate that deficits range from 358.8 to 1,312.8 tonnes annually, with an average shortfall exceeding 1,000 tonnes per year. Even during 2021, when demand decreased relative to other years, production remained insufficient to satisfy consumption independently.

The Recycling Dependency Problem

Recycled jewellery volumes increased from 1,144.1 tonnes in 2022 to 1,370 tonnes in 2024, representing a 19.7% increase. This acceleration suggests recycling rates respond to price movements rather than providing stable supply security.

As record-high gold prices rise, recycling increases, but this creates an inherently unstable supply foundation dependent on consumer behaviour and economic conditions.

High-Grading: Mining's Short-Term Fix with Long-Term Consequences

High-grading practices have become widespread across the gold mining industry as companies respond to margin pressures and production targets. This strategy involves deliberately mining areas of ore bodies containing the highest-grade material while leaving lower-grade resources in place.

During periods of low metal prices, high-grading provided operational flexibility by maintaining profit margins through selective extraction. However, this approach creates significant long-term consequences by depleting premium reserves at accelerated rates compared to natural ore body extraction patterns.

The practice essentially borrows future production capacity to meet current targets, reducing the productive life of deposits and requiring more aggressive extraction methods to maintain output levels. Industry analysts identify rising operational complexity as the primary risk facing mining companies through 2026, driven by increasingly complex ore bodies, deeper mining requirements, and substantially declined ore grades.

Reserve Quality Deterioration Across Major Producers

Global gold mining faces simultaneous challenges across multiple operational dimensions. Reserves experience ongoing depletion while mines encounter production problems including lower grades, labour disruptions, protests, and regulatory complications.

Key Production Challenges:

- Ore grade decline: Average grades decrease as high-grade zones become exhausted

- Operational depth increases: Deeper mining raises costs and technical complexity

- Labour market disruptions: Workforce issues affect production continuity

- Regulatory pressures: Environmental and social requirements create development delays

- Infrastructure constraints: Remote locations require substantial capital investment

These factors compound to create production environments where maintaining output requires progressively higher capital investment and operational sophistication. The combination of declining resource quality and increasing operational challenges suggests that production growth will face persistent headwinds regardless of metal price levels.

What Economic Forces Are Driving Peak Gold Scarcity?

Central Bank Accumulation Patterns and Geopolitical Hedging

Central bank gold purchases represent a fundamental shift in global reserve management strategies, with institutions accumulating approximately 1,000 tonnes annually since 2022. This purchasing pattern reflects strategic diversification away from dollar-denominated assets rather than traditional monetary hedging.

Central Bank Purchase Drivers:

- Currency diversification: Reducing dependence on USD-denominated reserves

- Geopolitical risk management: Protecting against asset freezing or sanctions

- Monetary policy independence: Maintaining sovereign reserve control

- Inflation hedging: Preserving purchasing power during currency debasement

| Regional Focus | Purchase Motivation | Annual Volume |

|---|---|---|

| Emerging Markets | Dollar dependency reduction | 600-700 tonnes |

| Developed Nations | Portfolio diversification | 200-300 tonnes |

| Geopolitically Sensitive | Sanctions protection | 100-200 tonnes |

Why 1,000 Tonnes Annually Matters

Central bank purchases of 1,000 tonnes represent approximately 27% of total annual mine production, creating structural demand that competes directly with commercial and investment markets. Unlike traditional gold demand, central bank purchases demonstrate relative price insensitivity, continuing even as gold reaches historical highs.

Inflation Protection Demand vs. Mining Supply Constraints

Real yield compression drives institutional gold allocation as central banks implement rate cuts amid rising inflation. When nominal interest rates fall while inflation accelerates, real yields (nominal rates minus inflation) approach zero or turn negative, increasing demand for non-yielding assets that preserve purchasing power.

Société Générale exemplifies institutional response by increasing gold allocation from 7% to 10% while projecting average prices of $3,825 per ounce in 2025 and $4,128 per ounce in 2026. The bank's analysis focuses on USD dominance challenges rather than purely monetary factors.

Inflation-Driven Demand Mechanics:

- Real yield compression: Negative returns on fixed-income investments

- Currency debasement concerns: Fiat money purchasing power erosion

- Portfolio diversification requirements: Risk management across asset classes

- Alternative store of value demand: Non-yielding assets during inflationary periods

Currency Diversification Trends Away from Dollar Dominance

Global reserve managers increasingly question USD dominance as mounting government debt burdens strain major economies. Long-term government bond yields rise across developed markets as governments struggle to attract sufficient foreign investment for debt financing.

When governments cannot secure adequate foreign buyers for debt issuance, central banks face pressure to purchase treasury securities directly, similar to quantitative easing programmes implemented during the 2008 financial crisis and COVID-19 pandemic. These interventions typically prove highly inflationary, perpetuating demand for alternative stores of value.

The pattern creates self-reinforcing cycles where currency concerns drive gold demand, while increased gold purchases signal reduced confidence in fiat monetary systems, potentially accelerating diversification trends among other market participants.

Which Geological Factors Signal Imminent Supply Constraints?

The Discovery Drought: No Major Deposits Since 2000

Exploration success rates demonstrate the severity of geological constraints facing the gold industry. The complete absence of major deposit discoveries over the past two decades represents an unprecedented situation in modern mining history.

Historical Discovery Patterns

1970s-1990s Era: Consistent identification of world-class deposits exceeding 50 million ounces, with multiple discoveries per decade supporting production growth and reserve replacement.

2000s-Present: Zero discoveries exceeding 50 million ounces, minimal findings above 15 million ounces, indicating either geological exhaustion of accessible high-grade deposits or inadequate exploration techniques for remaining resources.

This discovery pattern suggests that easily accessible, high-grade gold deposits have been largely identified and developed. Remaining resources likely exist in more challenging geological environments, requiring advanced extraction technologies and substantially higher development costs.

The exploration industry faces a fundamental challenge: traditional geological models and search techniques may prove inadequate for identifying remaining world-class deposits, particularly if such resources exist in previously unexplored geological environments or at depths beyond conventional mining capabilities.

Ore Grade Decline and Operational Complexity Increases

Average ore grades across global gold mining operations continue declining as high-grade zones become exhausted. This trend forces mining companies to process larger volumes of material to maintain equivalent gold production, increasing operational costs and environmental impact.

Grade Decline Implications:

- Processing volume increases: More rock required per ounce of gold production

- Energy consumption growth: Higher power requirements for material handling and processing

- Waste generation expansion: Increased tailings and overburden disposal needs

- Equipment capacity demands: Larger-scale machinery and infrastructure requirements

- Environmental footprint growth: Extended land use and ecosystem disruption

Operational complexity compounds as mines extend to greater depths, encounter more challenging geological conditions, and face increasingly stringent environmental regulations. The combination creates environments where maintaining production requires exponentially higher capital investment relative to output.

Brownfield vs. Greenfield Development Economics

Mining capital allocation increasingly favours brownfield expansions over greenfield developments, seeking to minimise development timelines and reduce exploration risk. Brownfield projects offer 50% to 70% faster production timelines compared to new greenfield developments, providing near-term supply additions while avoiding lengthy exploration and permitting processes.

However, this strategy inherently limits industry growth potential by constraining production expansion to existing reserve bases. Brownfield developments extend mine lives and increase production rates at established operations but cannot address the fundamental shortage of new world-class deposits.

Development Strategy Trade-offs:

| Approach | Timeline | Risk Level | Growth Potential | Capital Requirements |

|---|---|---|---|---|

| Brownfield | 2-4 years | Moderate | Limited to existing reserves | Lower |

| Greenfield | 7-15 years | High | Unlimited if successful | Very High |

The preference for brownfield development reflects industry recognition that greenfield exploration faces diminishing success rates and extended development timelines that may not align with production requirements or investment return expectations.

How Are Mining Companies Responding to Resource Depletion?

The 44-Project Challenge: Wood Mackenzie's Development Requirements

Maintaining current global gold production levels requires successful development of 44 projects currently in various stages of advancement. This requirement represents an unprecedented coordination challenge across the mining industry, involving multiple companies, jurisdictions, and regulatory frameworks.

Wood Mackenzie's head of gold research acknowledges the slim probability of achieving this target, noting that even if all probable projects advanced to production before 2025, the industry would only barely maintain 2019 production levels. The analysis assumes no delays or scope changes, conditions rarely achieved in complex mining developments.

Development Risk Factors:

- Permitting delays: Regulatory approval processes extending project timelines

- Capital allocation competition: Companies prioritising other projects or returning capital to shareholders

- Scope modifications: Technical challenges requiring design changes or capacity reductions

- Market condition changes: Metal price volatility affecting project economics

- Political risk: Jurisdiction changes impacting project viability

Capital Allocation Shifts Toward Brownfield Expansions

Mining companies demonstrate clear preference for brownfield expansions over greenfield exploration, reflecting risk management priorities and investor return expectations. This strategic shift provides operational advantages while creating long-term supply limitations.

Brownfield Expansion Advantages:

- Established infrastructure: Existing processing facilities, power systems, and transportation networks

- Known geology: Reduced geological risk through extensive historical data

- Regulatory familiarity: Existing relationships with local authorities and communities

- Operational expertise: Workforce experience with specific deposit characteristics

- Faster production timelines: Reduced development phases and permitting requirements

While brownfield expansions offer near-term production increases, they cannot address the industry's fundamental challenge: insufficient new world-class deposits to replace depleting reserves. This approach essentially optimises existing resources rather than expanding the industry's reserve base.

Exploration Budget Constraints vs. Discovery Success Rates

Exploration budgets face pressure from declining success rates and extended development timelines that challenge traditional investment return models. Companies must balance exploration investment against operational requirements and shareholder return expectations.

The combination of reduced success rates and higher exploration costs per discovery creates unfavourable risk-reward profiles for greenfield exploration programmes. Many companies redirect capital toward production optimisation, acquisitions, or shareholder returns rather than high-risk exploration initiatives.

Exploration Investment Challenges:

- Success rate decline: Fewer viable discoveries per dollar invested

- Technology requirements: Advanced techniques increasing exploration costs

- Remote location focus: Remaining prospective areas often lack infrastructure

- Long development timelines: Extended periods between discovery and production

- Regulatory complexity: Increasing environmental and social requirements

What Investment Implications Emerge from Peak Gold Scenarios?

Price Trajectory Modelling Under Supply Constraints

Institutional price forecasts reflect recognition of structural supply constraints combined with persistent demand growth. Société Générale's projections of $3,825 per ounce in 2025 and $4,128 per ounce in 2026 represent substantial increases from historical levels, indicating expectations of sustained scarcity premiums.

Bank Forecast Analysis:

| Institution | 2025 Target | 2026 Target | Allocation Change | Key Driver |

|---|---|---|---|---|

| Société Générale | $3,825/oz | $4,128/oz | 7% → 10% | USD dominance challenges |

| Central Banks | N/A | N/A | +1,000 tonnes annually | Reserve diversification |

Price modelling under supply constraint scenarios suggests that traditional price elasticity assumptions may not apply to gold markets. Unlike typical commodities, higher gold prices may not stimulate sufficient supply response due to geological limitations and long development timelines.

Société Générale's $4,128 Target Analysis

The French bank's gold price forecast 2025 projections assume continued central bank purchases despite elevated prices, indicating institutional demand driven by strategic positioning rather than price sensitivity. Their analysis emphasises USD dominance challenges and real yield compression as primary drivers supporting sustained price appreciation.

Portfolio Allocation Strategies for Scarcity-Driven Markets

Institutional investors recognise gold's evolving role from portfolio diversifier to strategic asset during periods of currency instability and supply constraints. Allocation strategies increasingly focus on long-term positioning rather than tactical trading approaches.

Strategic Allocation Considerations:

- Maximum allocation limits: Increasing from traditional 5-7% to 10%+ in institutional portfolios

- Duration positioning: Long-term holdings rather than cyclical trading strategies

- Physical vs. financial exposure: Preference for physical gold or allocated storage options

- Geographic diversification: Storage across multiple jurisdictions to mitigate political risk

Scarcity-driven markets require different allocation approaches compared to typical commodity investments. The combination of supply constraints and monetary demand suggests gold may function more like currency or sovereign assets rather than traditional commodities.

Junior Explorer Risk-Reward Dynamics in Tight Supply Environments

Peak gold scarcity creates significant opportunities for exploration companies with viable projects, as major mining companies seek acquisition targets to replace depleting reserves. The scarcity of new discoveries may drive substantial valuation premiums for successful exploration programmes.

Junior Explorer Investment Characteristics:

- High-risk, high-reward profiles: Potential for exceptional returns but significant failure rates

- Acquisition premium potential: Major miners competing for viable development projects

- Geological location importance: Projects in stable jurisdictions commanding valuation premiums

- Scale requirements: Deposits must achieve economic thresholds to attract major company interest

The limited pipeline of new projects may create exceptional opportunities for exploration companies that successfully identify and advance viable deposits through development stages. Furthermore, gold investment strategies must account for these structural changes in the industry landscape.

The next major ASX story will hit our subscribers first

Which Regions Face the Most Critical Reserve Exhaustion?

South Africa's 40-Year Reserve Cliff

South African gold mining faces particular challenges due to deep underground operations, aging infrastructure, and declining ore grades. The region's historically dominant position in global gold production has diminished significantly as easily accessible high-grade deposits become exhausted.

South African Mining Challenges:

- Extreme mining depths: Operations extending beyond 3,000 metres underground

- Infrastructure aging: Decades-old equipment requiring substantial capital investment

- Regulatory complexity: Evolving mining laws and social responsibility requirements

- Operational risks: Safety concerns in deep underground environments

- Economic pressures: High operational costs challenging project economics

The region's reserve base faces particular pressure due to geological characteristics requiring deep underground extraction methods that increase costs and technical complexity compared to open-pit or shallow underground operations common in other regions.

Nevada's Carlin Trend Depletion Timeline

Nevada's Carlin Trend has provided substantial gold production over several decades but faces geological constraints as high-grade zones become exhausted. The region's unique geological characteristics supported extensive development but may limit future expansion potential.

Carlin Trend Characteristics:

- Geological uniqueness: Specific geological conditions rarely replicated elsewhere

- Extensive development: Multiple decades of intensive mining activity

- Grade decline patterns: Observable reduction in average ore grades over time

- Expansion limitations: Geological boundaries constraining further development

- Operational maturity: Established infrastructure but aging facilities

Australia's Kalgoorlie District Production Challenges

Australia's Kalgoorlie district represents one of the world's most significant gold mining regions but faces ongoing challenges maintaining production levels as easy-to-extract resources become depleted.

Kalgoorlie District Factors:

- Historical significance: Over 100 years of continuous mining activity

- Resource depletion: Progressive exhaustion of high-grade surface deposits

- Technical advancement requirements: Need for sophisticated extraction methods

- Economic pressures: Rising operational costs affecting project viability

- Environmental considerations: Increasing regulatory requirements for new developments

How Do Monetary Policy Shifts Amplify Gold Scarcity Effects?

Federal Reserve Rate Cuts and Real Yield Compression

Federal Reserve monetary policy creates conditions that amplify gold demand during periods of supply constraint. Rate cuts implemented alongside rising inflation compress real yields, making non-yielding assets like gold relatively attractive compared to fixed-income investments.

Real yield compression occurs when nominal interest rates fall while inflation remains elevated or accelerates. This combination reduces or eliminates the opportunity cost of holding non-yielding assets, supporting demand for gold as an alternative store of value.

Real Yield Impact Mechanisms:

- Negative real returns: Fixed-income investments losing purchasing power

- Opportunity cost reduction: Lower relative cost of holding non-yielding assets

- Currency debasement concerns: Monetary policy raising long-term inflation expectations

- Portfolio rebalancing drivers: Institutional allocation shifts toward real assets

Government Debt Crisis Impact on Precious Metal Demand

Rising government debt burdens across major economies create conditions requiring central bank intervention in treasury markets. When governments cannot attract sufficient foreign buyers for debt financing, central banks may implement quantitative easing programmes involving direct treasury purchases.

These interventions typically prove highly inflationary, as central bank money creation to purchase government debt increases monetary supply while potentially raising inflation expectations. The resulting currency debasement concerns drive demand for alternative stores of value including gold.

Debt Crisis Progression:

- Government borrowing increases: Rising fiscal deficits require additional debt issuance

- Foreign buyer reluctance: International investors reduce treasury purchases

- Yield pressure emerges: Interest rates rise to attract sufficient investment

- Central bank intervention: QE programmes to suppress yields and support debt markets

- Inflation acceleration: Monetary expansion drives price increases

- Currency concerns develop: Debasement fears encourage alternative asset demand

Quantitative Easing Cycles and Currency Debasement Risks

Historical quantitative easing programmes during the 2008 financial crisis and COVID-19 pandemic demonstrate how monetary expansion drives gold demand through currency debasement concerns. Similar programmes implemented to address government debt crises may create sustained inflationary pressures.

The cycle becomes self-reinforcing as currency debasement concerns drive gold demand, while persistent monetary expansion validates those concerns and supports continued allocation to alternative stores of value. Moreover, gold market performance increasingly reflects these monetary dynamics.

QE Impact on Gold Markets:

- Direct monetary expansion: Central bank balance sheet growth increasing money supply

- Inflation expectation changes: Market participants anticipating sustained price increases

- Currency confidence erosion: Reduced faith in fiat monetary systems

- International reserve diversification: Central banks reducing USD-denominated holdings

- Investment demand acceleration: Institutional and individual allocation increases

What Technology Solutions Could Address Peak Gold Challenges?

Advanced Extraction Technologies for Lower-Grade Deposits

Technological advancement offers potential solutions for extracting gold from previously uneconomic deposits, though implementation requires substantial capital investment and may not address fundamental geological constraints.

Emerging Extraction Technologies:

- Heap leaching improvements: Enhanced chemical processes for low-grade ores

- Bioleaching applications: Bacterial extraction methods for complex ores

- In-situ recovery: Underground chemical extraction without traditional mining

- Pressure oxidation: Advanced processing for refractory ores

- Sensor-based sorting: Automated ore grade identification and separation

While these technologies may improve extraction efficiency, they cannot create new deposits or fundamentally alter the geological reality of declining ore grades and exhausted high-grade resources.

Deep Mining Innovations and Cost Reduction Strategies

Deep mining presents significant technical challenges that require innovative solutions to maintain operational viability. As surface and shallow underground deposits become exhausted, the industry must develop technologies for accessing deeper resources economically.

Deep Mining Technology Development:

- Automated equipment: Remote-controlled machinery reducing human exposure to dangerous conditions

- Ventilation systems: Advanced air circulation for deep underground environments

- Rock mechanics: Engineering solutions for high-pressure underground conditions

- Transportation efficiency: Improved systems for moving material from extreme depths

- Energy management: Power distribution and cooling systems for deep operations

Exploration Technology Improvements and Discovery Rates

Advanced exploration technologies may improve discovery rates by identifying deposits in previously unexplored geological environments or at depths beyond conventional exploration capabilities.

Exploration Technology Advances:

- Geophysical surveying: Enhanced subsurface imaging and analysis techniques

- Geochemical analysis: Improved soil and rock sampling methods

- Satellite technology: Remote sensing for geological anomaly identification

- Artificial intelligence: Machine learning applications for geological data analysis

- Drilling technology: Advanced techniques for deeper and more precise exploration

However, technological improvements cannot overcome fundamental geological constraints if world-class deposits simply do not exist in accessible locations. Technology enhancement may improve discovery efficiency without guaranteeing discovery success.

When Will Peak Gold Scarcity Reach Critical Thresholds?

2027 Production Peak Projections and Plateau Scenarios

Industry analysis suggests global gold production may reach peak levels around 2027, followed by plateau conditions rather than immediate decline. This timeline reflects the completion of projects currently under development combined with limited new project pipelines.

Production Timeline Projections:

- 2025-2027: Final production increases from projects under development

- 2027-2030: Production plateau as new project additions balance natural decline

- Post-2030: Production decline unless major new discoveries advance to development

- 2035-2040: Significant production decreases absent technological breakthroughs or new deposit discoveries

These projections assume successful development of currently identified projects and continuation of current exploration success rates. Changes in either factor could accelerate or delay timeline progression. Additionally, the historic gold surge explanation demonstrates how supply constraints are already manifesting in price behaviour.

2040-2050 Reserve Depletion Timelines

Long-term reserve depletion modelling suggests significant production capacity loss by 2040-2050 unless substantial new discoveries replace depleting reserves. This timeline reflects natural mine life progression combined with limited replacement resource identification.

Reserve Depletion Factors:

- Natural mine life cycles: Established operations reaching end-of-life stages

- High-grading consequences: Accelerated depletion of premium reserves

- Limited replacement resources: Insufficient new deposit pipeline

- Technological limitations: Current extraction methods reaching geological boundaries

Market Response Mechanisms and Price Discovery

Gold markets may demonstrate different price behaviour during scarcity periods compared to typical commodity cycles. The combination of monetary demand drivers and supply constraints suggests price discovery mechanisms may become increasingly volatile.

Market Response Characteristics:

- Reduced price elasticity: Supply response limitations regardless of price levels

- Increased volatility: Scarcity premiums creating unstable price formation

- Monetary demand dominance: Central bank and institutional demand overwhelming commercial markets

- Regional price disparities: Physical delivery constraints creating geographic price differences

Frequently Asked Questions About Peak Gold Scarcity

Is Peak Gold Theory Supported by Current Data?

Current data demonstrates consistent annual deficits between mine production and total demand, requiring jewellery recycling to satisfy market requirements. These deficits have persisted for nine consecutive years despite record production levels, supporting the structural supply constraint thesis.

The key evidence includes production-demand gaps averaging over 1,000 tonnes annually, absence of major deposit discoveries since 2000, and increasing dependence on recycled gold to meet market demand. However, production has continued growing rather than declining, requiring clarification of peak gold scarcity definitions.

How Does Gold Scarcity Compare to Other Commodity Cycles?

Gold demonstrates unique characteristics compared to typical commodity cycles due to its monetary function and geological constraints. Unlike industrial metals where higher prices typically stimulate increased exploration and production, gold faces fundamental limitations in supply response.

Gold Market Distinctions:

- Monetary demand component: Central bank purchases driven by strategic positioning rather than price sensitivity

- Long development timelines: 7-15 years from discovery to production limiting supply elasticity

- Geological constraints: Finite high-grade resources unlike renewable or synthetic alternatives

- Recycling limitations: Secondary supply dependent on consumer behaviour and economic conditions

What Role Does Recycling Play in Supply Security?

Recycled gold currently provides approximately 27.5% of total supply when combined with mine production, representing the critical component bridging annual supply-demand gaps. However, recycling rates depend on gold prices and economic conditions rather than providing stable supply foundations.

Recycling volumes increased 19.7% from 2022 to 2024, suggesting price sensitivity in secondary supply. This characteristic creates inherently unstable supply foundations, as recycling may decrease during economic growth periods or when gold prices decline, potentially exacerbating scarcity conditions.

Can Higher Prices Solve the Discovery Problem?

Higher gold prices improve project economics for marginal deposits but cannot overcome fundamental geological constraints. If world-class deposits do not exist in accessible locations, price increases alone cannot stimulate discovery of non-existent resources.

Price appreciation may enable development of lower-grade deposits previously considered uneconomic, but these typically require substantially higher capital investment and operational costs. The relationship between prices and discovery success rates remains limited by geological availability rather than economic incentives alone.

Strategic Investment Positioning for Gold Supply Constraints

Physical Gold vs. Mining Equity Exposure Strategies

Supply constraint environments may favour physical gold exposure over mining equity positions due to operational challenges facing mining companies. While scarcity drives gold prices higher, mining operations face increasing costs and complexity that may limit equity performance relative to commodity price appreciation.

Physical Gold Advantages:

- Direct commodity exposure: Pure play on gold price appreciation without operational risks

- No counterparty risk: Physical ownership eliminating financial institution dependencies

- Monetary demand participation: Benefiting from central bank and institutional accumulation trends

- Storage flexibility: Geographic diversification and allocation control

Mining Equity Considerations:

- Operational leverage: Potential for amplified returns during price appreciation

- Production challenges: Rising costs and complexity limiting profit margins

- Development risks: Project delays and cost overruns affecting returns

- Jurisdiction exposure: Political and regulatory risks varying by location

Geographic Diversification Considerations

Supply constraints create opportunities in different geographic regions based on resource quality, political stability, and development timelines. Investors may benefit from understanding regional production challenges and reserve depletion patterns.

Regional Investment Factors:

- Political stability: Jurisdiction risk affecting asset security and operational continuity

- Resource quality: Ore grades and deposit characteristics influencing production costs

- Infrastructure availability: Transportation and power access impacting development economics

- Regulatory environment: Mining laws and environmental requirements affecting project viability

Timing Market Entry Points in Scarcity-Driven Cycles

Peak gold scarcity may create sustained rather than cyclical price appreciation, requiring different timing strategies compared to traditional commodity investments. Supply constraints combined with persistent monetary demand suggest extended periods of price support.

Investment timing considerations should account for monetary policy cycles, central bank accumulation patterns, and production development timelines rather than focusing primarily on traditional supply-demand cyclical factors.

Entry Point Considerations:

- Monetary policy inflection points: Federal Reserve rate policy changes affecting real yields

- Central bank accumulation phases: Sustained institutional demand supporting price floors

- Production development gaps: Supply constraint periods creating scarcity premiums

- Currency stability periods: Dollar strength cycles affecting gold demand patterns

Disclaimer: This analysis contains forward-looking projections and speculative elements regarding commodity markets, monetary policy, and geological factors. Investment decisions should consider multiple factors and professional advice. Past performance does not guarantee future results, and precious metals investments carry inherent risks including price volatility and market liquidity considerations.

Want to Position Yourself Ahead of Gold's Supply Crunch?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market during this unprecedented period of gold scarcity. Understand why major mineral discoveries can lead to significant market returns by exploring historic examples of exceptional outcomes, then begin your 14-day free trial today to secure your market-leading advantage.