July 24, 2026

The $63 Billion Crossroads: Peru's Mining Investment Future Hangs on a Single Vote

Few moments in Latin American resource history carry the weight of a presidential runoff in a country that sits atop some of the world's most significant copper and polymetallic deposits. Peru presidential candidates mining plans investment doubts have come sharply into focus as the June runoff approaches. Peru consistently ranks among the top three global producers of copper, silver, and zinc, and its mining sector contributes a substantial share of national export earnings and fiscal revenue. When electoral uncertainty intersects with a commodity supercycle, the decisions made in Lima's voting booths ripple through project boardrooms from Toronto to Tokyo.

The June 7 runoff between right-wing candidate Keiko Fujimori and left-wing candidate Roberto Sánchez has crystallised a fundamental tension that runs through every resource-dependent democracy: how a government divides the spoils of geological fortune between capital, communities, and the state. For investors, the stakes are not abstract. They are measured in discount rates, permit timelines, and the probability of stranded capital in the Andean highlands.

When big ASX news breaks, our subscribers know first

Understanding What Is Actually at Risk in Peru's Mining Sector

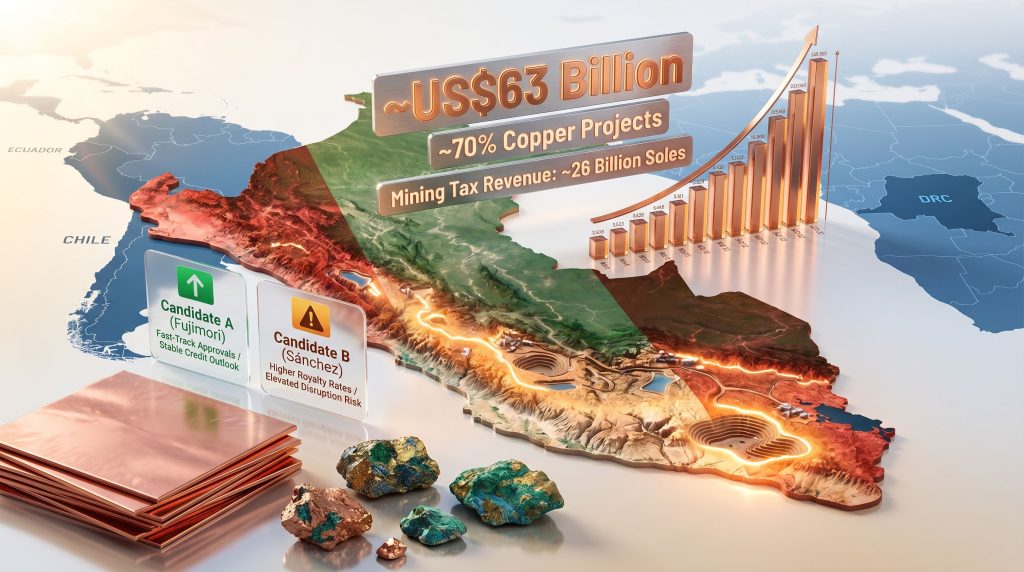

Peru's undeveloped mining pipeline is estimated at approximately US$63 billion, with roughly 70% of that total concentrated in copper projects located in the country's southern Andean corridor. This is not speculative prospecting capital. Much of this pipeline consists of advanced-stage projects with completed feasibility studies, environmental approvals in various stages, and committed development plans contingent on policy certainty.

The sector's fiscal contribution already represents a record-setting benchmark. In the most recent reporting year, total mining tax revenue reached approximately 26 billion soles, equivalent to roughly US$7.59 billion, driven by elevated copper and gold prices. Regional authorities in mining-affected areas received the equivalent of US$2.93 billion in transfers derived from income tax and royalty proceeds, funds earmarked for community development and infrastructure delivery.

| Metric | Value |

|---|---|

| Total mining investment pipeline | ~US$63 billion |

| Share in copper projects | ~70% |

| Mining tax revenue (record high, prior year) | |

| Regional transfers from mining revenue | ~US$2.93 billion |

| Exchange rate reference | US$1 = 3.426 soles |

These figures underline a critical reality: the existing framework is already generating substantial public benefit. The debate is not whether mining contributes to Peru, but whether changing the fiscal architecture would grow or shrink that contribution over time. Furthermore, these numbers sit within a broader context of critical minerals demand from global energy transition programmes that continue to place copper at the centre of long-range supply strategies.

How the Two Candidates Approach Mining Policy Differently

Fujimori's Investment-Oriented Framework

Fujimori's platform centres on three pillars designed to accelerate project development and community buy-in simultaneously. Her proposals include:

- Directing 40% of mining royalties to host communities located near active mining operations

- Creating a fast-track approval mechanism specifically for projects classified as strategically significant

- Introducing tax incentives structured around profit reinvestment within Peru rather than capital repatriation

On paper, the community royalty redistribution concept attempts to bridge the persistent social licence gap that has historically stalled Peruvian projects. The fast-track mechanism, if implemented effectively, could materially reduce the permitting timelines that currently extend project development cycles by years and inflate pre-production financing costs.

Moody's Ratings has assessed that a Fujimori victory would more likely preserve Peru's existing macroeconomic framework and credit stability, a signal that international capital markets would interpret as a continuity scenario rather than a recalibration of investment risk. According to industry analysis, Fujimori currently holds a narrow lead heading into the runoff, though polling margins remain within the range of uncertainty.

Sánchez's State-Expansion Model

Sánchez's platform moves in a structurally different direction. His key proposals include:

- Raising mining royalty rates and corporate tax obligations across the sector

- Conducting formal reviews of existing contracts held by large-scale mining companies

- Pursuing a constitutional referendum to expand the state's role in economic activity

Each of these measures, taken individually, would introduce meaningful uncertainty into project-level financial models. Collectively, they represent a potential redesign of the operating environment for mining capital in Peru. Moody's has signalled that a Sánchez victory would carry an elevated probability of policy changes capable of weakening investor confidence and eroding fiscal credibility.

Side-by-Side Policy Comparison

| Policy Dimension | Fujimori | Sánchez |

|---|---|---|

| Royalty structure | 40% to host communities | Increase royalty rates |

| Tax settings | Reinvestment incentives | Higher corporate tax burden |

| Contract treatment | Preserve existing agreements | Formal contract reviews |

| Constitutional framework | Maintain current structure | Referendum for new constitution |

| Fast-track approvals | Yes, for strategic projects | Not proposed |

| Credit rating outlook | Stable / investment-preserving | Elevated disruption risk |

What Peru's Mining Industry Actually Thinks

The National Society of Mining, Petroleum and Energy (SNMPE) has taken the rare step of publicly assessing both platforms and concluding that neither offers a genuinely sustainable long-term framework for the sector. The organisation's central argument focuses on the structural consequences of increasing fiscal pressure on a capital-intensive industry that operates on decade-long investment horizons.

The SNMPE's position deserves careful reading. Rather than defending the status quo, the industry body has argued that the most productive policy intervention would be strengthening institutional capacity to deploy existing mining revenues efficiently. The evidence they cite is striking: more than 2,000 public works projects in mining-affected regions currently sit stalled, not because funding is unavailable, but because government execution capacity is inadequate.

The central challenge is not how much revenue the mining sector generates. It is whether the institutions responsible for spending that revenue can convert it into functional infrastructure and services. Increasing the tax burden without first resolving the execution deficit risks compressing investment while delivering no improvement in community outcomes.

This framing recentres the policy debate. If the existing transfer of US$2.93 billion to regional authorities is already failing to produce finished public works at scale, then the argument for extracting more revenue from the sector becomes harder to sustain on community benefit grounds alone. Peru's presidential candidates' mining plans have consequently drawn sharp scrutiny from industry leaders who question whether either approach adequately addresses this execution deficit.

How Political Risk Translates Into Capital Allocation Decisions

The Mechanics of Investment Deterrence

Mining projects are evaluated using discounted cash flow models that are extremely sensitive to long-duration risk. When policy uncertainty increases, the discount rate applied to future cash flows rises, which mechanically reduces a project's net present value. A project that clears a capital allocation hurdle under one policy scenario may fail to clear it under another, even if the underlying geology and commodity price assumptions remain identical.

For copper-heavy portfolios, this sensitivity is amplified by project lead times. A typical large-scale copper mine in the Andes requires seven to fifteen years from discovery to first production. Policy changes proposed today affect investment decisions being made right now for production that will not arrive until the mid-2030s. This is why electoral outcomes in Peru carry disproportionate weight in global mining capital allocation cycles. Understanding these dynamics is essential for anyone developing sound copper investment strategies for the decade ahead.

The Congressional Deadlock Variable

One factor that moderates the risk analysis in both directions is the structural fragmentation of Peru's Congress. Regardless of which candidate wins the presidency, neither will enter office commanding a majority legislative coalition. This is not a temporary political condition but a persistent feature of Peru's multi-party parliamentary environment.

The practical consequence cuts both ways:

- A Sánchez presidency would face significant legislative resistance to royalty increases, contract reviews, and constitutional reform timelines

- A Fujimori presidency would similarly struggle to pass fast-track permitting legislation or redesign royalty distribution frameworks without coalition building

For investors, this congressional constraint functions as a partial hedge against the most extreme policy scenarios under either administration. However, the probability of rapid, sweeping reform is lower than the headline platforms imply.

The Broader Risk Landscape Beyond Electoral Outcomes

Illegal Mining and the Governance Gap

Both candidates have largely avoided substantive engagement with one of Peru's most persistent structural problems: the scale and geographic spread of informal and illegal mining activity. Illegal gold mining in particular has expanded significantly across Amazonian and Andean regions, undermining formal sector economics, distorting regional production data, and creating environmental liabilities that eventually attach to the jurisdiction's overall investment reputation.

The absence of credible enforcement frameworks compounds formal sector risk in a way that neither royalty redistribution nor tax reform can address directly. In addition, these mining geopolitical risks extend well beyond Peru's borders, as competing jurisdictions actively monitor how Lima navigates its policy transition.

ESG Frameworks and Social Licence Pressures

International project financing has become increasingly conditional on ESG compliance metrics. For Peruvian copper projects specifically, community relations, water management, and indigenous consultation protocols have moved from reputational considerations to bankability requirements. The 2,000-plus stalled public works projects are not merely a governance statistic. They represent evidence of a broken social contract between the mining sector's fiscal contribution and visible community benefit delivery, a dynamic that international lenders and institutional investors now factor explicitly into project risk assessments.

Competing Jurisdictions and Capital Reallocation Risk

Peru does not compete for mining capital in a vacuum. Chile, Ecuador, and the Democratic Republic of Congo are all actively positioning for copper investment at a moment when the energy transition has elevated long-term copper demand forecasts significantly. Capital reallocation decisions by major mining companies are made at the portfolio level, weighing political risk premiums across multiple jurisdictions simultaneously.

A sustained period of policy uncertainty in Peru during a commodity upswing does not simply delay investment. It redirects capital to competing projects in more stable operating environments, often permanently, because exploration pipelines take years to rebuild once interrupted. For context, the copper supply crunch already unfolding globally makes Peru's political trajectory especially consequential for producers and investors alike.

The next major ASX story will hit our subscribers first

Strategic Variables Investors Should Monitor After the Vote

The election result is only the first data point in a multi-stage risk assessment. The following variables will shape the post-election investment environment more precisely than the vote count alone:

- Cabinet composition, particularly the appointment to the Ministry of Energy and Mines, which signals how literally either candidate intends to implement their platform

- Early legislative signals on royalty reform, contract review scope, or constitutional process timelines in the first 90 days of the new administration

- Sovereign credit rating actions from Moody's and S&P in the quarter following the runoff result

- Congressional coalition dynamics and whether either party can assemble the legislative partnerships needed to advance major reforms

- Chinese state-owned enterprise positioning, given that Chinese capital has historically provided Peruvian mining projects with an alternative financing pathway that reduces dependence on Western institutional debt markets

The Long-Term Structural Case for Peru

Electoral cycles create volatility, but they rarely alter geological endowments. Peru's copper and polymetallic reserves remain among the most significant on the planet, and the infrastructure investment already embedded in the southern Andean corridor represents a sunk cost advantage that competing jurisdictions cannot easily replicate. For instance, a major copper project of comparable scale elsewhere illustrates precisely how difficult and expensive it is to build equivalent geological and logistical foundations from scratch.

The highest-return policy lever available to either administration is institutional reform: improving the execution capacity of regional governments, clearing the backlog of stalled public works, and creating a functioning link between resource revenue and visible community outcomes. This would address the social licence deficit that has historically been the most common trigger for project disruption in Peru, more reliably than either tax increases or royalty redistribution models operating through broken delivery mechanisms.

For investors monitoring Peru presidential candidates mining plans investment doubts, the long-term thesis for the country's resource sector remains structurally intact. The near-term question is whether the political process will create conditions that allow that thesis to be acted upon.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking assessments involve inherent uncertainty, and readers should conduct independent due diligence before making any investment decisions. Commodity markets and political environments can change rapidly, and past performance or policy frameworks are not indicative of future outcomes.

Want To Stay Ahead of Major ASX Mineral Discoveries Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex mineral data into clear, actionable insights for investors at every level — explore the historic returns generated by major discoveries to understand what early positioning can mean, then begin a 14-day free trial at Discovery Alert to secure your market-leading advantage.