June 11, 2026

The Invisible Arbitrage Machine Running India's Cement Sector

Every large industrial market contains a hidden switching mechanism, one that activates not through policy announcements or executive strategy sessions, but through the quiet mathematics of delivered cost per unit of energy. In India's cement industry, that mechanism governs the continuous oscillation between two seaborne fuels: petroleum coke and Northern Appalachian thermal coal. When the numbers shift by even a few dollars per tonne, hundreds of thousands of tonnes of cargo orders change direction. Indian cement firms return to petroleum coke market dynamics, as played out across the first half of 2026, offer a textbook illustration of this dynamic, carrying lessons well beyond the Indian subcontinent.

When big ASX news breaks, our subscribers know first

How Petroleum Coke Functions in Cement Kiln Economics

The Combustion Requirements That Make Petcoke Attractive

Cement production is an energy-intensive process by nature. Rotary kilns must sustain temperatures exceeding 1,400 degrees Celsius to produce clinker, the intermediate product that forms the basis of finished cement. Fuels used in this process must deliver consistent, high-intensity heat over sustained periods.

Petroleum coke, a carbon-rich byproduct of crude oil refining, fits this requirement precisely. Its calorific value typically exceeds that of most thermal coals, and its combustion characteristics suit the continuous operation demands of large rotary kilns. The dominant specification purchased by Indian cement manufacturers is high-sulphur fuel-grade coke at 6.5% sulphur content, sourced primarily from US Gulf Coast refineries and, secondarily, from major Middle Eastern refining complexes.

Critically, fuel costs represent approximately 30% of total input costs for Indian cement producers, according to industry data. This makes the fuel procurement decision one of the single most consequential cost variables these companies manage, second only to raw material sourcing. In a market where producers have struggled to raise cement prices due to aggressive capacity expansion and intensifying competition for market share, any deterioration in fuel economics flows almost directly to the bottom line.

The Structural Substitution Dynamic: Petcoke vs. NAPP Coal

What makes India's fuel procurement market particularly interesting is the near-perfect substitutability between two very different fuels. High-sulphur petcoke and Northern Appalachian thermal coal graded at approximately NAR 6,900 kcal/kg compete for the same kiln burners, and their relative competitiveness is determined by a single offsetting mechanism built into India's import tax structure.

| Fuel | Import Duty | Typical Sulphur | Primary Source | Calorific Value |

|---|---|---|---|---|

| High-sulphur petcoke (6.5% S) | 11% | ~6.5% | US Gulf, Middle East | Higher (~8,000 kcal/kg) |

| NAPP thermal coal (NAR 6,900) | 2.75% | Low | US Appalachia | Lower (~6,900 kcal/kg) |

The 8.25 percentage point duty gap between the two fuels broadly offsets petcoke's calorific value advantage on a delivered, duty-paid basis. This means that when pre-duty prices for both commodities are similar, their landed cost per unit of energy is roughly equivalent, creating a highly sensitive switching threshold. A price movement of just $10 to $15 per tonne in either direction can tip the economics decisively toward one fuel or the other.

Key Market Dynamic: This is not a story about one fuel replacing another permanently. It is a story about a continuous, price-responsive rebalancing between two viable options, where structural loyalty is irrelevant and landed cost is everything.

What Caused Indian Cement Buyers to Exit the Petcoke Market Earlier in 2026

The Price Escalation That Broke the Economics

The seaborne petcoke market entered 2026 under pressure, but what followed was an unusually rapid and severe escalation. Delivered India prices for 6.5% sulphur coke rose for twelve consecutive weeks from the start of the year, eventually reaching a three-year high of $160 per tonne on 1 April 2026, representing a 24% increase over that period, according to Argus Media price assessments.

The escalation was driven by a convergence of supply disruptions. Regional conflict created logistical constraints affecting coke flows from the Aramco/TotalEnergies Satorp refinery located in Jubail, Saudi Arabia, a facility processing approximately 460,000 barrels per day of crude. Vessels accessing this refinery, situated on the Mideast Gulf coast, require passage through the Strait of Hormuz, and conflict in the region complicated that routing.

Separately, output from the Saudi Aramco/Sinopec Yasref refinery in Yanbu was reported to have run below normal levels during recent months. Together, these two facilities typically export approximately 1.8 million tonnes per year each of petroleum coke, meaning the effective supply removal from these two assets alone represented a meaningful share of the seaborne market. Furthermore, tighter fob coke availability from the US Gulf and elevated freight rates compounded upward price pressure across the entire delivered cost chain.

The Scale of the Demand Response

Indian cement manufacturers responded swiftly and decisively. Seaborne petcoke imports into the cement sector fell to approximately 707,000 tonnes in the first quarter of 2026, compared with 2.47 million tonnes during the same period of 2025, representing a year-on-year decline of roughly 71%, according to shipping agency Interocean data cited by Argus Media.

Across the January to April period, cement-sector petcoke imports totalled approximately 1.03 million tonnes, barely one-third of the 3.27 million tonnes received during the same months in 2025.

| Period | Petcoke Imports | Year-on-Year Change |

|---|---|---|

| Jan-Apr 2025 | 3.27 million tonnes | Reference period |

| Jan-Apr 2026 | 1.03 million tonnes | -68% |

| Q1 2026 | 707,000 tonnes | -71% vs Q1 2025 |

| Full-year 2026 (projected) | ~6 million tonnes | -44% vs 2025 |

To fill the gap, Indian buyers turned heavily to NAPP thermal coal. India's imports of this grade rose approximately 30% year-on-year across January to April 2026, reaching 3.65 million tonnes, with cement kilns and brick kilns representing the primary demand centres, according to trade analytics data from Kpler.

UltraTech Cement, India's largest cement producer, reported that petroleum coke's share of its fuel mix fell to 41% in the January-March 2026 quarter, down from 54% in the equivalent quarter of 2025, as the company disclosed in an April filing with the Bombay Stock Exchange. Consequently, the broader implications for commodity market volatility were significant, with seaborne cargo flows between India and major exporting nations shifting measurably.

Why Indian Cement Firms Return to Petroleum Coke in Mid-2026

The Price Convergence That Reignited Buying Interest

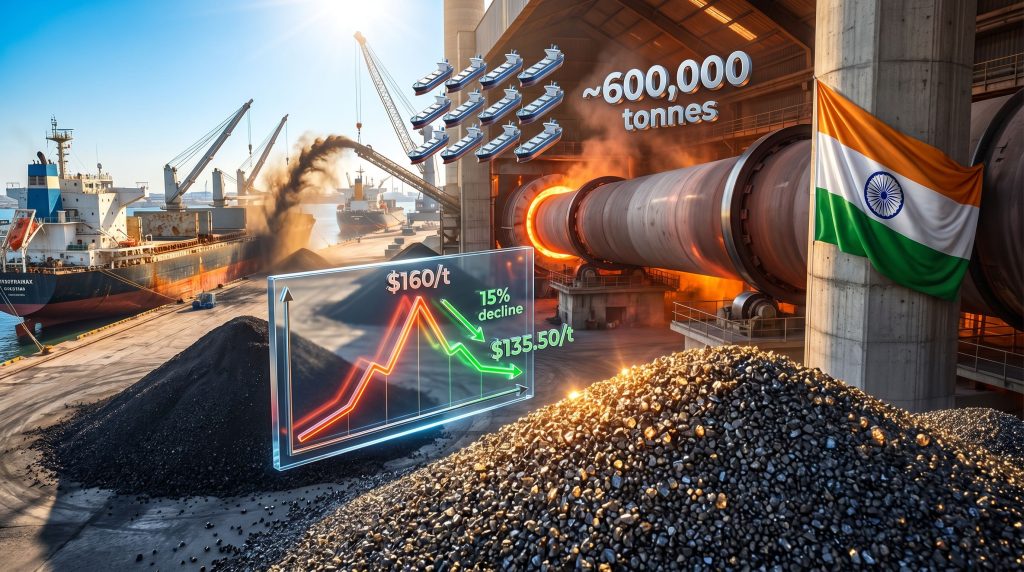

After reaching its April peak of $160 per tonne cfr India, delivered 6.5% sulphur petcoke pricing began a sustained retreat. By early June 2026, delivered India prices had fallen to $135.50 per tonne, reflecting a decline of approximately 15% from the recent peak, according to Argus Media assessments dated 3 June 2026.

On the US Gulf fob side, the correction was equally notable. High-sulphur petcoke fob prices dropped below $80 per tonne for the first time since early February 2026, touching $79 per tonne by 3 June. The catalyst was a combination of higher US refinery utilisation rates and increased coke output flowing into the export market, which steadily eroded the supply tightness that had underpinned earlier price strength.

Meanwhile, NAPP coal was being offered at approximately $133 to $134 per tonne cfr India's west coast during the same period. With Supramax petcoke cargoes for July and August loading being quoted in the low-to-mid $130s per tonne cfr, the price gap that had favoured coal by $15 to $20 per tonne in May had effectively evaporated by early June.

The Procurement Wave: Scale, Speed, and Origin

The market response was immediate. Indian cement buyers collectively booked approximately 10 to 12 Supramax vessels of high-sulphur petcoke over a concentrated period spanning late May and early June 2026. Given that a standard Supramax dry bulk vessel carries approximately 50,000 to 60,000 tonnes of cargo, this buying wave represents roughly 600,000 tonnes of new petcoke procurement — a significant volume relative to the depressed import rates seen earlier in the year.

The cargoes were predominantly of US origin, consistent with the established supply corridor for high-sulphur fuel-grade coke into the Indian market.

What makes this procurement episode particularly instructive is the arbitrage behaviour observed simultaneously at port inventory level. Several cement plants that had previously substituted petcoke with NAPP coal were observed selling coal from their existing port stocks into the domestic retail market at a profit of $5 to $6 per tonne, then reinvesting the proceeds into new petcoke cargo bookings. This dual transaction illustrates just how rapidly fuel economics had shifted, and underscores the financial sophistication of India's large industrial fuel buyers.

The Regulatory Architecture That Governs Fuel Competitiveness

Import Duties as the Structural Equilibrium Mechanism

India's import duty framework is not a passive backdrop to this story; it is an active determinant of fuel competitiveness. The 11% duty applied to petroleum coke versus the 2.75% duty on NAPP thermal coal represents a structurally embedded cost disadvantage for petcoke that must be overcome through pre-duty price differentials before the two fuels reach parity on a landed cost basis.

This duty architecture serves a dual purpose in the Indian policy context. Domestically, it offers indirect protection for coal consumption at a time when India continues to rely heavily on coal across its industrial and power sectors. From an emissions management perspective, it creates a financial disincentive for the higher-sulphur fuel, even if enforcement of sulphur-related emissions standards for cement kilns has historically been complex.

It is worth noting that India also maintains import quota and duty structures for calcined petroleum coke used in aluminium anode production and raw petcoke destined for calcining operations, representing a separate market segment with distinct pricing signals. These dynamics, alongside broader shifts in tariffs and supply chains, can occasionally influence sentiment in the fuel-grade coke market, even though the two segments serve fundamentally different industrial functions.

Any future revision to India's import duty framework — whether aimed at supporting domestic coal demand, managing industrial sulphur emissions, or responding to broader energy trade policy shifts — could materially and permanently alter the competitive equilibrium between petcoke and NAPP coal in the cement sector.

Forward Scenarios: Will the Return to Petcoke Hold?

Reading the Supply-Side Signals

The trajectory of fob petcoke prices from US Gulf refineries is arguably the most important single variable determining whether Indian cement buyers' renewed appetite for coke persists through the second half of 2026. Higher utilisation rates at US refineries translate directly into increased coke output, which exerts sustained downward pressure on fob prices and improves the economics of US-origin cargoes for Indian importers. This closely mirrors broader crude oil price drivers, given that petcoke supply is fundamentally a function of refinery throughput.

On the coal side, market observers note that significant downside for NAPP coal delivered prices is structurally limited. Rising domestic production and inland transportation costs in the US have elevated the cost floor for coal export economics, meaning that even if demand from competing buyers softens, delivered India NAPP prices are unlikely to collapse to levels that would recreate the wide price gap seen earlier in 2026.

One seasonal factor worth monitoring is brick kiln demand. Brick kilns, alongside cement plants, are among the primary consumers of NAPP coal in the Indian industrial sector. During the monsoon months of July through September, brick kiln operations typically slow substantially, reducing competition for NAPP coal and potentially softening delivered prices modestly. However, this seasonal effect is unlikely to fundamentally alter the petcoke demand recovery trajectory unless it coincides with a simultaneous resurgence in petcoke supply disruptions.

Scenario Matrix: Key Variables and Their Impact

| Scenario | Most Likely Impact on Petcoke Demand |

|---|---|

| US refinery runs remain elevated | Sustained fob price pressure supports continued Indian cement buying |

| Middle East supply disruptions intensify | Petcoke tightens, prices rise, coal substitution resumes |

| NAPP coal weakens on monsoon brick kiln slowdown | Modest coal price softening, but unlikely to re-open $15-$20/t gap |

| India revises import duty structure | Could structurally rebalance the petcoke-coal competition |

| Indian cement capacity additions accelerate | Higher aggregate fuel demand benefits both petcoke and coal |

| Stricter sulphur emission regulations enforced | Structural long-term headwind for high-sulphur petcoke use |

Furthermore, global industrial demand trends suggest that energy-intensive sectors beyond cement are also navigating similar fuel-switching dynamics, adding a broader dimension to how these market movements are interpreted internationally.

The next major ASX story will hit our subscribers first

Frequently Asked Questions

Why do Indian cement companies use petroleum coke as a kiln fuel?

Petcoke delivers a high calorific value per tonne and burns with consistent intensity, making it well-suited to the sustained high-temperature requirements of rotary cement kilns. With fuel representing roughly 30% of total cement production costs, price competitiveness is critical, and petcoke has historically offered a cost advantage over many alternatives when import duty effects are accounted for.

What is the primary substitute fuel when petcoke becomes expensive?

Northern Appalachian thermal coal, graded at NAR 6,900 kcal/kg, is the dominant substitute. It carries a significantly lower import duty of 2.75% versus 11% for petcoke, which partially compensates for its lower calorific value and allows it to compete closely with petcoke whenever pre-duty price spreads narrow.

How large is India's cement sector petcoke import market?

In 2025, Indian cement manufacturers imported approximately 10.67 million tonnes of seaborne petcoke. Full-year 2026 imports are projected to reach only around 6 million tonnes, reflecting the extended coal substitution period during the first half of the year.

Is the current return to petcoke a structural or tactical shift?

It is tactical and price-driven. Market participants characterise it as conditional, with procurement managers indicating that petcoke would be selected over coal for near-term purchases at current price levels, but making clear this reflects cost arithmetic rather than any long-term strategic preference for the fuel.

Key Takeaways for Market Observers

-

The mid-2026 return to petcoke by Indian cement buyers reflects price normalisation after a severe supply-driven spike, not a structural realignment of fuel strategy

-

A procurement wave of approximately 600,000 tonnes across 10 to 12 Supramax vessels signals meaningful near-term demand recovery concentrated in a very short timeframe

-

The petcoke-coal price gap is highly sensitive to small movements, given the structural offset between the duty differential and the calorific value advantage, making this a market prone to rapid reversals

-

The simultaneous coal inventory arbitrage observed at Indian ports — selling coal at a profit to fund petcoke purchases — illustrates the financial sophistication of India's large industrial fuel buyers

-

Continued upward pressure on US refinery output and the resulting fob petcoke price softness could sustain Indian cement-sector buying interest well into the third quarter of 2026

-

Longer term, India's cement fuel mix will remain a dynamically managed blend of petcoke and coal, with import duties, emissions regulations, freight markets, and geopolitical supply disruptions serving as the primary swing variables

This article contains forward-looking projections, market estimates, and scenario analyses. These are based on available data and industry reporting and should not be construed as investment advice. Commodity markets are subject to significant volatility, and outcomes may differ materially from projections.

Want to Catch the Next Major Commodity Market Shift Before the Crowd?

The fuel-switching dynamics reshaping India's cement sector illustrate just how rapidly commodity markets can move — and how quickly fortunes can change for investors positioned ahead of the curve. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity market signals into actionable investment opportunities the moment they emerge — start your 14-day free trial today and gain a market-leading edge.