August 9, 2026

The Electrochemical Foundation of PGM-Catalyzed Water Splitting

Green hydrogen production represents one of the most significant technological shifts in energy infrastructure since the advent of petroleum refining. At its core lies a fundamental electrochemical process that depends entirely on platinum group metals to achieve the efficiency levels necessary for commercial viability. Understanding these mechanisms reveals why platinum group metals in green hydrogen systems have become indispensable for the global energy transition and energy transition security.

Proton Exchange Membrane Electrolysis Mechanisms

The hydrogen evolution reaction occurring at platinum cathodes operates through a sophisticated electron transfer process that maximizes hydrogen gas production while minimising energy losses. Platinum's unique crystalline structure enables rapid adsorption and desorption of hydrogen atoms, creating an optimal surface for continuous gas generation. This process requires precise control of current density, typically operating between 1.5 to 2.0 amperes per square centimetre to maintain efficiency above 80%.

Iridium-based anodes facilitate the oxygen evolution reaction through a different but equally critical pathway. Unlike platinum, iridium oxide demonstrates exceptional stability in acidic electrolyte environments, withstanding the corrosive conditions that would rapidly degrade alternative materials. The membrane electrode assembly configuration distributes these precious metals in thin layers, typically requiring 0.3 to 0.8 milligrams of platinum per square centimetre for cathode applications.

| Technology | Operating Efficiency | PGM Loading (mg/cm²) | Operating Pressure |

|---|---|---|---|

| PEM Electrolysis | 75-85% | 0.5-1.2 | 30-80 bar |

| Alkaline Electrolysis | 65-75% | None required | 1-30 bar |

| High-pressure PEM | 80-90% | 0.8-1.5 | 80-200 bar |

Catalyst Surface Chemistry and Electron Transfer Dynamics

Platinum's effectiveness stems from its d-orbital electron configuration, which creates optimal binding energies for hydrogen intermediates. The metal surface facilitates a two-step process where hydrogen ions first adsorb onto platinum sites, then combine with electrons to form molecular hydrogen. This binding energy relationship, known as the Sabatier principle, positions platinum at the theoretical optimum for hydrogen evolution kinetics.

Iridium oxide exhibits different surface chemistry characteristics that make it uniquely suited for oxygen evolution. The formation of higher oxidation states during the reaction cycle enables efficient water molecule splitting while maintaining structural integrity. Research indicates that iridium-based catalysts maintain 95% of their initial activity after 10,000 operating hours under standard conditions.

Furthermore, ruthenium's role in mixed-metal oxide formulations enhances overall catalyst durability through electronic modification effects. When combined with iridium in specific ratios, ruthenium creates surface sites that reduce the energy barriers for oxygen evolution while providing cost advantages compared to pure iridium systems.

When big ASX news breaks, our subscribers know first

Critical Supply Chain Vulnerabilities for PGM-Based Hydrogen Systems

Global Production Bottlenecks and Geographic Concentration

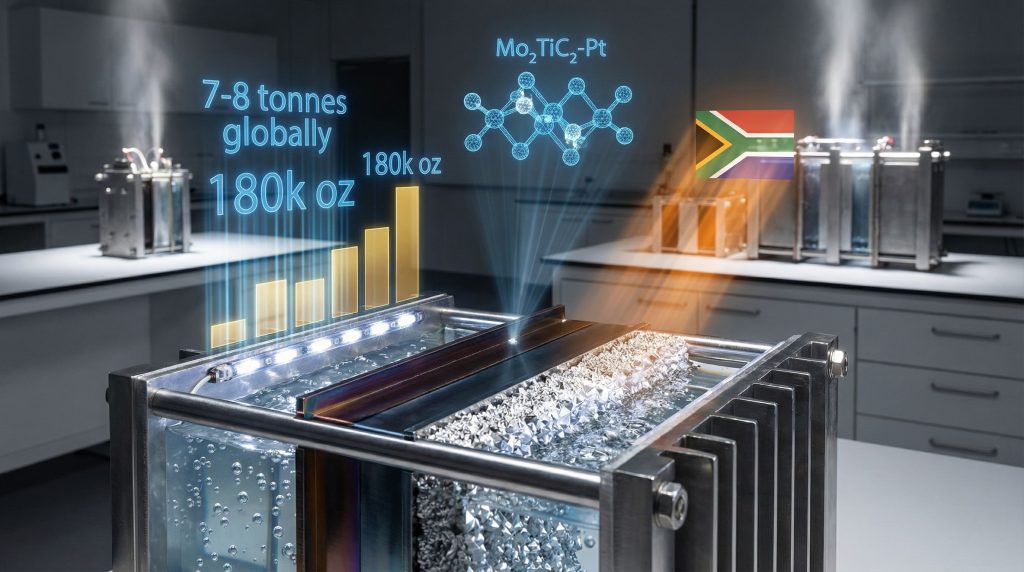

South Africa's position as the world's largest provider of platinum group metals creates both opportunities and risks for hydrogen infrastructure development. The country controls approximately 70% of global platinum reserves and an even higher percentage of iridium production capacity. This geographic concentration represents a significant supply chain vulnerability as hydrogen deployment accelerates globally.

Annual iridium production constraints present the most immediate challenge for large-scale electrolyzer manufacturing. Global production reaches only 7-8 tonnes annually, with industrial applications already consuming substantial portions of this supply. Unlike platinum, which benefits from significant secondary production through catalytic converter recycling, iridium recovery remains limited due to lower historical usage volumes.

In addition, secondary production through urban mining offers potential relief for supply constraints. Spent fuel cell systems contain recoverable quantities of platinum group metals, though the infrastructure for large-scale recovery remains underdeveloped. Recovery rates from end-of-life electrolyzers can achieve 85-95% efficiency for platinum and palladium, with slightly lower rates for iridium due to processing complexities.

| Metal | Global Reserves (tonnes) | Annual Production (tonnes) | South Africa Share |

|---|---|---|---|

| Platinum | 63,000 | 190 | 71% |

| Palladium | 69,000 | 210 | 37% |

| Rhodium | 9,000 | 32 | 81% |

| Iridium | 2,600 | 7.5 | 87% |

Price Volatility and Investment Risk Assessment

Historical platinum group metal price cycles demonstrate significant volatility that directly impacts electrolyzer economics. Iridium prices have experienced 300-500% fluctuations over five-year periods, primarily driven by supply disruptions and industrial demand changes. This volatility creates substantial uncertainty for hydrogen project developers attempting to secure long-term equipment supply agreements.

Mining disruptions in South Africa historically correlate with immediate price spikes across all platinum group metals. Labour disputes, power outages, and geological challenges can reduce production capacity by 15-25% during peak disruption periods. These supply shocks propagate through the entire hydrogen value chain, affecting electrolyzer costs and project viability assessments.

However, hedging strategies for hydrogen project developers include long-term purchase agreements with PGM suppliers and catalyst leasing arrangements. Some manufacturers offer catalyst recycling programmes that guarantee recovery of precious metal content at project end-of-life, effectively reducing exposure to price volatility during operational periods.

Advanced Catalyst Designs Reducing PGM Requirements

Nanostructured Catalyst Development

MXene-supported platinum nanocomposites represent a breakthrough in catalyst efficiency, utilising Mo₂TiC₂-Pt structures that maximise surface area utilisation. These advanced materials achieve identical catalytic performance with 60-70% lower platinum loading compared to conventional catalyst designs. The MXene support structure provides enhanced electrical conductivity while preventing platinum nanoparticle agglomeration during extended operation.

Core-shell architectures optimise precious metal utilisation by placing platinum in thin surface layers over less expensive metal cores. Platinum shells of 2-3 atomic layers thickness maintain full catalytic activity while reducing total metal requirements by up to 80%. These structures require sophisticated manufacturing processes but offer substantial cost reduction potential for large-scale deployment.

Furthermore, single-atom catalysts achieve the theoretical maximum efficiency for platinum utilisation by dispersing individual platinum atoms on support materials. Research indicates these systems can reduce platinum requirements by 75-85% while maintaining competitive activity levels. However, single-atom stability under industrial operating conditions remains a challenge for commercial implementation.

Alternative Material Research Pathways

Non-precious metal catalysts for alkaline electrolysis systems show promise for specific applications where pure water and controlled operating conditions are available. Nickel-iron oxides and cobalt phosphides demonstrate acceptable performance in alkaline environments, though they require higher operating temperatures and cannot match PGM efficiency levels.

Hybrid systems combining precious and earth-abundant materials offer intermediate solutions that balance cost and performance. These approaches typically maintain 20-30% of original PGM loading while incorporating base metal catalysts to handle specific reaction steps. Performance trade-offs include reduced efficiency and shorter operational lifespans compared to full-PGM systems.

Moreover, the critical minerals strategy emphasises the importance of developing supply chain resilience for platinum group metals whilst pursuing alternative material research.

The hydrogen economy represents the largest potential demand shift for platinum group metals since automotive catalytic converter adoption in the 1970s, but supply chain resilience will determine scaling success.

PGM Role Across the Complete Hydrogen Value Chain

Upstream Production Technologies

PEM electrolyzer stack design requires careful distribution of platinum group metals to optimise both performance and cost. Modern systems employ gradient loading strategies where catalyst concentration varies across the electrode surface to match local current density distributions. This approach reduces total PGM requirements by 15-25% while maintaining overall system efficiency.

High-pressure electrolysis systems demand enhanced catalyst durability due to increased mechanical and chemical stresses. Operating pressures of 30-80 bar accelerate degradation mechanisms, requiring specialised catalyst formulations with improved stability. Advanced support materials and protective coatings extend catalyst lifetime under these demanding conditions.

Consequently, integration with renewable energy sources creates additional challenges for catalyst systems due to intermittent operation cycles. Start-stop cycling and variable load conditions stress catalyst structures differently than steady-state operation. PGM catalysts demonstrate superior tolerance to these conditions compared to alternative materials, justifying their continued use despite cost considerations.

Midstream Processing and Purification

Platinum-catalysed hydrogen purification removes trace impurities from mixed gas streams through selective oxidation reactions. These systems achieve 99.999% hydrogen purity levels required for fuel cell applications while operating at relatively low temperatures of 200-300°C. Platinum loading requirements for purification applications are typically 5-10 times lower than electrolysis systems.

Ammonia cracking processes for hydrogen carrier systems utilise ruthenium-based catalysts to decompose ammonia back into hydrogen and nitrogen. This application requires exceptional thermal stability and resistance to nitrogen poisoning, characteristics where ruthenium excels compared to other platinum group metals in various industrial applications. Operating temperatures of 400-500°C demand robust catalyst formulations.

For instance, liquid organic hydrogen carrier dehydrogenation reactions employ platinum catalysts to release hydrogen from organic compounds like toluene-methylcyclohexane systems. These processes operate at 300-400°C and require precise control of reaction kinetics to prevent unwanted side reactions that reduce efficiency.

Downstream Energy Conversion Applications

Fuel cell vehicle powertrains represent the largest current application for platinum group metals in hydrogen systems. Modern automotive fuel cells require 10-30 grams of platinum per vehicle, with ongoing research focused on reducing these requirements through improved catalyst utilisation. Vehicle manufacturers target 50% reduction in PGM loading by 2030 through advanced catalyst designs.

Stationary fuel cell systems for grid-scale energy storage operate under different conditions that influence catalyst requirements. Constant load operation and controlled environments enable longer catalyst lifetimes, justifying higher initial PGM loading for improved efficiency. These systems typically achieve 20,000-40,000 operating hours before catalyst replacement.

Additionally, industrial process heating applications in steel and cement production utilise high-temperature fuel cells that require specialised platinum-based catalysts. Operating temperatures of 600-800°C demand exceptional thermal stability while maintaining catalytic activity for hydrogen oxidation reactions.

Market Segments Driving Highest PGM Demand Growth

Transportation Sector Transformation

Heavy-duty trucking applications drive substantial PGM demand due to higher power requirements compared to passenger vehicles. Commercial trucks require 3-5 times the catalyst loading of passenger cars, with fuel cell systems sized for 100-200 kW continuous operation. Industry projections suggest 500,000 hydrogen trucks globally by 2030, representing significant platinum demand growth.

Maritime shipping adoption presents the largest long-term opportunity for PGM consumption in transportation. Ocean-going vessels require multi-megawatt fuel cell systems with correspondingly high catalyst loading requirements. A single large container ship conversion could consume 200-500 kilograms of platinum group metals, equivalent to thousands of passenger vehicles.

Furthermore, infrastructure development requirements create additional PGM demand through refuelling station electrolyzer systems. Each hydrogen refuelling station requires 1-5 MW of electrolysis capacity, consuming 50-250 grams of platinum group metals per installation. Planned infrastructure expansion suggests 10,000 stations globally by 2030.

Industrial Decarbonisation Applications

Steel production using hydrogen direct reduction processes represents a transformative application for PGM-catalysed systems. Modern direct reduction plants require 100-500 MW of electrolysis capacity to produce sufficient hydrogen for steel production. Each major steel plant conversion consumes 5-25 kilograms of platinum group metals for electrolyzer systems.

Chemical industry feedstock replacement strategies focus on producing hydrogen for ammonia, methanol, and other chemical processes. These applications demand 99.9%+ purity hydrogen, requiring sophisticated purification systems with additional PGM catalyst requirements. Industrial hydrogen production facilities typically require 10-100 kg of platinum group metals depending on scale.

However, refinery operations transitioning from fossil hydrogen sources create immediate demand for electrolytic hydrogen production. Existing refinery hydrogen consumption exceeds 50 million tonnes annually globally, representing massive potential for PGM-catalysed electrolysis systems as facilities decarbonise their operations. This aligns with broader mining industry innovation trends towards cleaner production methods.

Policy Frameworks Accelerating PGM-Hydrogen Market Development

Regional Investment Incentive Structures

US Inflation Reduction Act hydrogen production tax credits provide $3 per kilogram for qualifying clean hydrogen production, significantly improving project economics. This policy framework makes PGM-based electrolysis economically competitive with fossil hydrogen in many applications, accelerating deployment and driving catalyst demand growth.

European Union REPowerEU targets establish 80 GW of electrolyzer capacity by 2030, representing the world's most ambitious hydrogen scaling programme. This capacity target requires approximately 240-400 tonnes of platinum group metals for electrolyzer catalyst systems, assuming current technology loading rates.

In addition, China's national hydrogen strategy includes manufacturing scaling initiatives that target domestic PGM catalyst production capabilities. Chinese policy frameworks emphasise supply chain security and cost reduction through advanced manufacturing and recycling infrastructure development.

Technology Standardisation and Certification Requirements

International electrolyzer performance standards increasingly specify minimum efficiency and durability requirements that favour PGM-based catalyst systems. IEC 62282 standards establish testing protocols that demonstrate platinum group metal advantages in reliability and performance consistency.

Fuel cell durability testing protocols require 8,000-hour minimum lifetimes for automotive applications, with stationary systems targeting 40,000+ hours. These requirements effectively mandate PGM catalyst use due to superior stability characteristics compared to alternative materials.

Moreover, carbon intensity verification systems for green hydrogen certification create quality premiums for high-efficiency production methods. PEM electrolysis systems achieve lower carbon intensities due to higher efficiency and better renewable energy integration capabilities, supporting continued PGM utilisation. This connects to research on platinum's critical role in hydrogen development.

The next major ASX story will hit our subscribers first

Long-Term Sustainability Considerations for PGM-Based Hydrogen Systems

Circular Economy Integration Strategies

End-of-life catalyst recovery and refining processes achieve 90-95% recovery rates for platinum and palladium from spent electrolyzer systems. Specialised recycling facilities are being developed to handle the unique characteristics of hydrogen production catalysts, which differ from automotive applications in contamination profiles and support materials.

Urban mining potential from decommissioned fuel cell systems creates a growing secondary supply source for platinum group metals. First-generation hydrogen vehicle fleets reaching end-of-life provide substantial recovery opportunities, with each vehicle containing 10-30 grams of recoverable platinum.

Consequently, closed-loop manufacturing approaches integrate recycled PGM content directly into new catalyst production. Catalyst manufacturers report 30-50% recycled content in new products, reducing primary metal demand while maintaining performance specifications. This approach supports the broader mining sustainability transformation taking place across the industry.

Environmental Impact Assessment

Life cycle analysis of PGM extraction versus hydrogen system benefits demonstrates favourable environmental outcomes despite mining impacts. Hydrogen fuel cell systems offset their PGM production emissions within 6-12 months of operation when displacing fossil fuel applications.

Water usage requirements for electrolysis operations create additional environmental considerations, particularly in water-stressed regions. PEM electrolysis requires 9-12 litres of purified water per kilogram of hydrogen produced, though most of this water can be recycled through system condensate recovery.

Furthermore, land use considerations for renewable energy-hydrogen integration favour compact PEM systems due to higher power density compared to alkaline alternatives. Space-constrained installations benefit from PGM catalyst efficiency, justifying premium costs through reduced infrastructure requirements. The industry recognises mine reclamation benefits as essential for sustainable PGM extraction.

Strategic Positioning for the PGM-Hydrogen Transition

Investment Risk-Reward Framework

Portfolio diversification across the platinum group metal supply chain offers multiple exposure points to hydrogen growth trends. Mining companies, catalyst manufacturers, and recycling operations each provide different risk-return profiles for investors seeking hydrogen economy exposure.

Technology risk assessment for alternative catalyst development suggests 5-10 year timelines for significant PGM replacement in electrolysis applications. While research continues on non-precious metal alternatives, current performance gaps maintain strong competitive positions for platinum group metals in green hydrogen systems.

However, geographic exposure considerations favour South African mining operations due to resource concentration, though political and operational risks require careful evaluation. Diversified mining companies with global operations offer reduced single-country exposure while maintaining PGM production capabilities.

Future Technology Roadmap Implications

Timeline projections for PGM demand peak suggest 2035-2040 maximum consumption driven by hydrogen infrastructure deployment, followed by gradual decline as catalyst efficiency improvements and recycling capacity reduce primary metal requirements.

Breakthrough catalyst technologies potentially disrupting current paradigms include single-atom catalysts and bio-inspired designs, though commercial viability remains uncertain. Industry consensus suggests evolutionary rather than revolutionary changes in catalyst technology over the next decade.

For instance, integration opportunities with battery storage and renewable energy systems create synergistic value propositions for PGM-hydrogen investments. Hybrid energy storage systems combining batteries and hydrogen provide grid-scale solutions that optimise both technologies' strengths.

The convergence of policy support, technological advancement, and environmental necessity positions platinum group metals in green hydrogen as essential enablers of the hydrogen economy transition, despite ongoing efforts to reduce their usage through improved efficiency and alternative material development. This strategic positioning becomes even more critical as the industry addresses the complex relationship between platinum group metals in green hydrogen applications and broader sustainability goals.

Disclaimer: This analysis contains forward-looking statements and projections about platinum group metals markets and hydrogen technology development. Actual results may differ materially due to technological breakthroughs, policy changes, market conditions, and other factors. Investment decisions should consider comprehensive risk assessments and professional financial advice.

Interested in Platinum Group Metal Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including platinum group metals and other critical minerals essential for the hydrogen economy. Access real-time alerts that help identify actionable opportunities in this rapidly evolving sector by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional market returns from major mineral discoveries.