May 13, 2026

The Hidden Architecture of a Fragile Market

Most commodity markets absorb geopolitical shocks through redundancy. When one supply corridor falters, alternatives exist. Phosphate markets do not operate this way. The global trade architecture for phosphate fertilizers is built around a remarkably thin set of export nodes and maritime passages, meaning that instability in a single region can transmit pricing pressure across every major agricultural economy on earth within weeks.

The phosphate market outlook Middle East conflict dynamic has moved from theoretical vulnerability to lived market experience as hostilities have intensified through 2026. Understanding why conditions look so different from typical commodity disruptions requires examining both the chemistry of fertilizer production and the geography of global trade flows simultaneously.

When big ASX news breaks, our subscribers know first

Why Phosphate Supply Chains Break Differently Than Other Commodities

The Chemistry That Creates Dependency

Phosphate fertilizers are not simply mined and shipped. Producing the two dominant traded products, diammonium phosphate (DAP) and monoammonium phosphate (MAP), requires combining phosphate rock with two critical inputs: ammonia and sulphuric acid. Ammonia is synthesised from natural gas, while sulphuric acid is derived from elemental sulphur. Both of these upstream inputs are heavily produced in or transited through the Middle East.

This chemical dependency is the first layer of vulnerability that most market observers underestimate. A disruption to phosphate rock supply gets attention. A simultaneous disruption to ammonia and sulphur supply, however, attacks the production economics of phosphate fertilizers even in countries that hold their own rock reserves. Furthermore, projects like the Ammaroo phosphate project and the Toolse phosphate project highlight how global players are racing to develop alternative supply sources outside conflict-exposed regions.

The Hormuz Chokepoint and Its Fertilizer Consequences

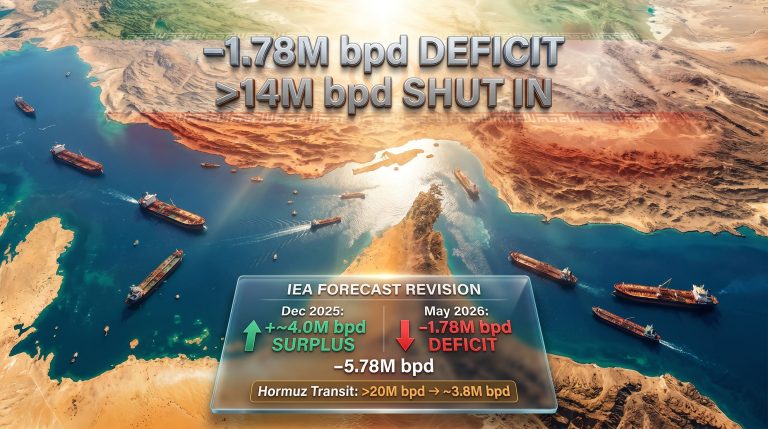

The Strait of Hormuz functions as the single most consequential maritime passage in global agricultural input logistics. Approximately 25 to 30% of the world's nitrogen fertilizer exports move through this corridor annually, along with substantial ammonia and sulphur volumes that feed directly into phosphate manufacturing elsewhere in the world.

Since early March 2026, effective disruption to this passage has placed an estimated ~16 million tonnes per year of total fertilizer export volumes at risk. To contextualise that figure: global DAP trade volumes run at roughly 40 to 45 million tonnes annually, meaning the at-risk volume represents a genuinely material share of the market rather than a marginal rounding error.

The critical insight that distinguishes phosphate markets from oil markets is the complete absence of any strategic buffer mechanism. Major economies hold strategic petroleum reserves specifically to dampen supply shocks. No equivalent institutional structure exists for fertilizers, meaning supply disruptions transmit directly and immediately into agricultural input pricing with nothing to absorb the impact.

What Middle East Conflict Has Done to Phosphate Pricing

From Anticipatory Risk to Confirmed Disruption

A useful analytical distinction separates the 2025 Israel-Iran conflict from the current 2026 disruption. During 2025, markets priced in potential supply loss, generating a precautionary risk premium that stayed partially anchored to fundamental supply reality. The 2026 escalation has crossed into confirmed physical disruption territory, where shipping is not merely threatened but actively constrained.

This distinction matters enormously for price trajectory analysis. Reactive pricing regimes — those responding to confirmed rather than anticipated disruption — tend to overshoot equilibrium. This creates meaningful near-term upside price risk followed by an equally sharp correction once supply normalises, a pattern that creates both risk and opportunity depending on positioning. The broader oil price rally triggered by regional instability has compounded these dynamics, adding further cost pressure across the energy-intensive fertilizer production chain.

Price Movement Across the Fertilizer Complex

The pricing impact has not been uniform across all fertilizer products. The table below captures the key movements observed across the complex following the escalation of hostilities:

| Commodity | Pre-Conflict Trend | Post-Conflict Movement | Primary Mechanism |

|---|---|---|---|

| DAP (Chinese export) | Stable baseline | +1.45% spot movement | Supply chain anxiety, input cost pressure |

| Ammonia (Middle East) | Declining trajectory | +5 to 6% uplift | Feedstock shortage, Hormuz shipping risk |

| Ammonia (Chinese domestic) | Declining trajectory | +7.53% uplift | Export uncertainty, sympathy move |

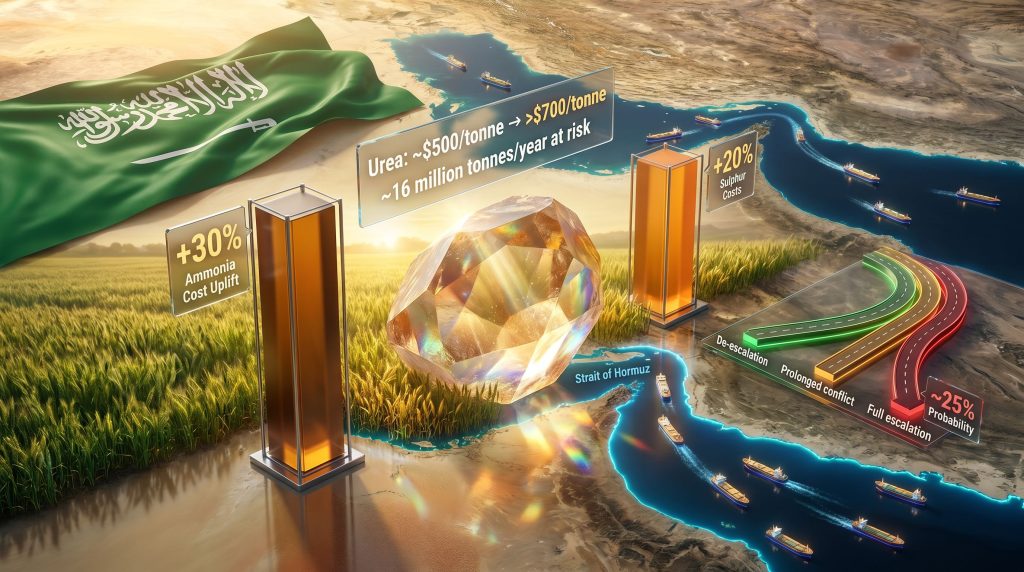

| Urea (Middle East/North Africa) | ~$500/tonne | Above $700/tonne (+40%) | Direct export curtailment |

The urea price trajectory is particularly instructive. A 40% price surge in a major nitrogen fertilizer reflects not incremental tightening but structural supply removal, and urea price dynamics typically foreshadow where phosphate pricing will travel over the following 4 to 8 weeks as input costs work their way through production economics.

The Input Cost Squeeze That Compounds Physical Disruption

Beyond the direct trade disruption, phosphate producers worldwide are absorbing a three-way cost-push shock:

- Ammonia input costs have risen approximately 30%, directly increasing the variable cost of producing every tonne of DAP and MAP

- Sulphur and sulphuric acid costs have increased roughly 20%, attacking the acid digestion stage of phosphate processing

- European natural gas prices have risen approximately 45%, feeding into production economics for European phosphate and compound fertilizer manufacturers

The combined effect compresses producer margins even where physical supply has not been interrupted, creating secondary incentives to reduce output volumes or redirect product toward higher-margin regional markets. This supply-side rationing can occur entirely independently of any direct trade route disruption. According to Rabobank's analysis of global fertilizer markets, these cost pressures are expected to persist well beyond any near-term resolution of hostilities.

Saudi Arabia's Structural Role and Why It Amplifies Risk

Saudi Arabia is not merely a participant in global phosphate trade. In 2024, the Kingdom exported approximately 3.9 million tonnes of DAP, valued at roughly $2.3 billion, representing a significant share of global seaborne phosphate supply. This production is concentrated at the Ma'aden phosphate complex, one of the largest integrated phosphate operations in the world, which depends on the same regional shipping infrastructure that the Hormuz disruption has compromised.

What makes Saudi Arabia's position particularly sensitive is the co-location of its export dependency and its vulnerability. Unlike Moroccan phosphate exports, which route through Atlantic corridors entirely disconnected from Hormuz, Saudi volumes must navigate the very passage that conflict has placed under pressure.

Why U.S. and Brazilian Buyers Face Compounding Exposure

Two of the world's most agriculturally significant economies have simultaneously increased their structural reliance on imported phosphate. U.S. phosphate import dependence approximately doubled to around 16% by 2025, a trajectory driven partly by the decline of domestic phosphate mining in Florida and Idaho and partly by the cost competitiveness of Middle Eastern and North African exporters.

Brazil presents an analogous but more acute vulnerability. As the world's largest agricultural exporter by value, Brazil runs among the highest per-hectare fertilizer consumption rates globally while possessing comparatively limited domestic phosphate production capacity. Brazilian agricultural buyers are therefore simultaneously exposed to supply tightening, elevated freight costs, and USD-denominated pricing pressure. Consequently, the broader critical minerals demand picture is being reshaped as nations scramble to secure reliable fertilizer input supply chains outside vulnerable corridors.

Three Scenarios for the Phosphate Market Outlook

Scenario 1: Rapid De-escalation (Transitory Disruption)

This pathway assumes Hormuz reopens within weeks and shipping normalises relatively quickly. Even under this optimistic scenario, embedded risk premiums do not fully unwind. Historical precedent from previous geopolitical commodity shocks consistently shows that insurance and freight cost premiums persist for 3 to 6 months after physical disruption resolves, as shipping companies and insurers recalibrate risk models. Phosphate buyers should expect a 5 to 15% residual cost pass-through even in the best-case resolution scenario.

Scenario 2: Prolonged Conflict Without Escalation (Base Case)

Under this pathway, sustained shipping risk maintains elevated freight and insurance costs across the region. Saudi DAP export volumes remain curtailed or rerouted at higher cost, while ammonia and sulphur input prices stay structurally elevated. Agricultural buyers in the U.S. and Brazil face compressed application economics heading into the 2026 to 2027 growing season, with purchasing decisions becoming genuinely difficult as planting windows approach.

Scenario 3: Full Escalation and Structural Supply Disruption

Carrying an estimated probability of around 25%, this scenario involves extended Hormuz closure triggering a structural tightening across the global phosphate supply chain. Producers enter sustained margin squeezes and output reductions follow. The downstream consequence most concerning for food security analysts is the potential for food price inflation of 5 to 12% within 3 to 6 months in import-dependent economies, given that fertilizers underpin approximately 50% of global food production capacity. Fertilizer maker Mosaic has already begun cutting output in response to rising costs, illustrating how quickly operational decisions follow from geopolitical disruption.

The absence of strategic fertilizer reserves is the single most important structural gap in the global food security architecture. Every G7 economy holds petroleum reserves for precisely this kind of supply shock scenario. The equivalent mechanism for fertilizers simply does not exist, meaning the speed of transmission from supply disruption to food price inflation is far faster in agricultural input markets than in energy markets.

The Potash Exception: Not All Fertilizers Face the Same Risk

One analytically important distinction that separates sophisticated market participants from generalist observers involves potash. Global potash supply is dominated by Canada, Russia, and Belarus, geographies entirely disconnected from the Hormuz corridor and the broader Middle East conflict zone. Potash prices have remained comparatively insulated from the current disruption.

This divergence within the fertilizer complex creates what commodity traders describe as a relative value dynamic. Buyers who can substitute potash application timing without yield consequence gain flexibility that phosphate and nitrogen buyers do not have. Agricultural buyers facing compressed budgets may accelerate potash purchases while deferring more expensive phosphate inputs, creating secondary demand distortions in both markets. However, the impact of global commodity tariffs continues to add a further layer of pricing complexity across all fertilizer categories.

The next major ASX story will hit our subscribers first

Seasonal Timing as a Market Amplifier

The Northern Hemisphere spring planting season collides directly with the current disruption window. This timing removes the single most important price-dampening mechanism available in agricultural commodity markets: the ability of buyers to defer purchases until prices normalise.

Planting windows are biologically fixed. A farmer who misses the optimal application window for phosphate fertilizer does not simply wait for the next price cycle. They face a direct yield consequence. This inelastic demand structure means that even relatively small supply shortfalls can generate disproportionately large price responses during the February-to-May window, as buyers compete for constrained volumes regardless of cost.

The implication for market timing analysis is significant. Price peaks during planting season conflicts tend to be sharp and rapid, followed by equally sharp corrections once seasonal demand subsides, even if the underlying supply situation has not materially changed.

Downstream Consequences in Vulnerable Economies

The food security implications of sustained phosphate supply tightening extend beyond commodity price movements into territory that carries genuine social and political risk. The economies most exposed share three compounding characteristics:

- Heavy dependence on food imports, leaving them unable to offset supply shortfalls through domestic production

- Reliance on externally sourced fertilizer inputs, meaning they cannot isolate their agricultural sector from global input cost movements

- Exposure to USD-denominated commodity pricing, meaning currency depreciation amplifies import cost pressure simultaneously

Sub-Saharan Africa, South Asia, and parts of Southeast Asia sit at the intersection of all three vulnerabilities. The 5 to 12% food price inflation estimate for a full escalation scenario represents a meaningful social and political destabilising force in economies where food expenditure already consumes 40 to 60% of household income for significant portions of the population.

Frequently Asked Questions: Phosphate Market Outlook and Middle East Conflict

What is the primary mechanism through which Middle East conflict affects phosphate prices?

The conflict disrupts the Strait of Hormuz, a critical maritime passage for fertilizer exports. This reduces available supply volumes, elevates shipping and insurance costs, and increases the price of key phosphate production inputs, particularly ammonia and sulphur, creating simultaneous supply-side constraint and cost-push price pressure.

Which phosphate products are most directly affected?

DAP and MAP are the most directly exposed products, given their reliance on ammonia as a production input and their concentration in Middle Eastern and North African export flows. The phosphate market outlook Middle East conflict analysis consistently identifies these two products as the highest-risk positions within the broader fertilizer complex.

How significant is Saudi Arabia's role in global phosphate supply?

Saudi Arabia exported approximately 3.9 million tonnes of DAP in 2024. Any sustained disruption to Saudi export capacity or access through Hormuz creates immediate tightening in global DAP availability.

Are there fertilizer markets not significantly affected by this conflict?

Potash markets have remained largely insulated, as global potash supply is concentrated in Canada, Russia, and Belarus, regions geographically and logistically disconnected from the Middle East conflict zone.

What would full escalation mean for food prices?

Analysts estimate that a full escalation scenario could generate food price inflation of 5 to 12% within 3 to 6 months in the most import-dependent economies, given fertilizers' foundational role in supporting approximately 50% of global food production output. The phosphate market outlook Middle East conflict trajectory under this scenario represents one of the more acute near-term risks to global food security.

Key Takeaways

- The Strait of Hormuz disruption since early March 2026 has placed approximately 16 million tonnes per year of fertilizer export volumes at risk

- Saudi Arabia's roughly 3.9 million tonne annual DAP export capacity is directly exposed to regional shipping constraints

- Phosphate input costs have surged, with ammonia up approximately 30% and sulphur up approximately 20%, compressing producer margins independently of direct trade disruption

- Urea prices have risen more than 40% in some corridors, signalling the severity of nitrogen market tightening that typically foreshadows downstream phosphate price pressure

- Three scenario pathways carry distinct price and supply implications, from transitory disruption with residual cost pass-through to full escalation with food price inflation risk

- The complete absence of strategic fertilizer reserves means supply shocks transmit into agricultural input and food pricing faster and more directly than equivalent energy market disruptions

- Potash markets remain structurally insulated, creating relative value dynamics within the broader fertilizer complex

Disclaimer: This article contains forward-looking analysis and scenario projections based on information available at time of writing. Commodity markets are subject to rapid change, and readers should not interpret any scenario analysis as a price forecast or investment recommendation. Investors and agricultural buyers should seek independent professional advice before making financial or purchasing decisions based on market outlook information.

Want to Position Ahead of the Next Major Commodity Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across phosphate, critical minerals, and over 30 other commodities — turning complex market data into actionable investment insights before the broader market reacts. Explore how historic discoveries have generated substantial returns and begin a 14-day free trial at Discovery Alert to gain your market-leading edge.