July 12, 2026

Global agricultural markets are experiencing unprecedented upheaval as fundamental supply chain disruptions reshape commodity flows across multiple continents. The convergence of geopolitical tensions, logistics bottlenecks, and inflationary pressures has created a perfect storm affecting fertilizer accessibility in regions dependent on international trade. Moreover, US economy and tariffs considerations are adding complexity to global agricultural supply chains.

Southern Latin America's agricultural sector faces particular vulnerability due to its reliance on imported phosphate fertilizers during critical planting seasons. The region's corn, soybean, and wheat production systems depend heavily on external suppliers, making farmers susceptible to global price volatility and supply disruptions that extend far beyond their immediate control. These high prices to curb southern Latam phosphate imports represent a significant challenge for regional agricultural competitiveness.

Understanding the Regional Phosphate Import Landscape

The Southern Cone's fertilizer import dependency represents a structural vulnerability that has become increasingly apparent during 2026's market disruptions. Argentina, Uruguay, and Paraguay collectively absorbed approximately 599,000 tonnes of DAP, MAP, and TSP between January and May during the 2021-2025 period, establishing a baseline that demonstrates the region's substantial import requirements.

Furthermore, tariff impacts on markets have created additional pressures on international trade flows affecting fertilizer imports.

Market Size and Consumption Patterns

Regional demand concentrates heavily on diammonium phosphate (DAP) and monoammonium phosphate (MAP) formulations, which provide both nitrogen and phosphorus nutrients essential for corn cultivation. These dual-nutrient compounds command premium pricing compared to triple superphosphate (TSP), which contains only phosphorus, making product substitution difficult for farmers focused on corn production.

Key Regional Import Statistics:

• Argentina: Dominates regional consumption with the largest agricultural area

• Uruguay: Maintains steady import volumes relative to agricultural scale

• Paraguay: Represents smallest but consistent market segment

• Combined baseline: 599,000 tonnes annually during peak season months

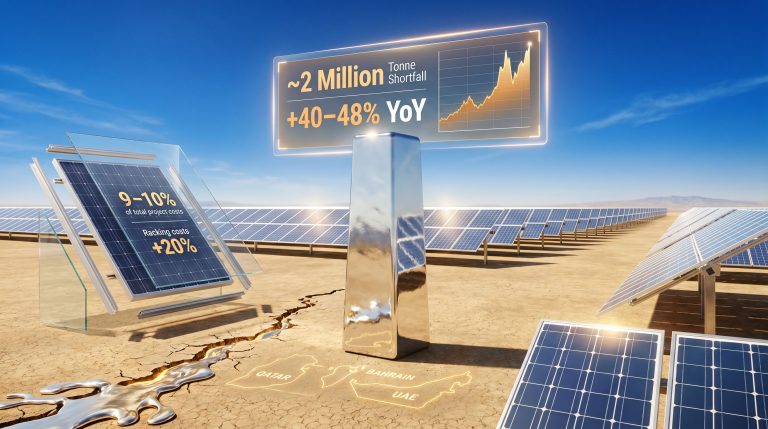

The spot market has delivered approximately 488,000 tonnes of phosphate fertilizers for regional shipment in 2026, representing roughly 81.5% of typical five-month import volumes. This shortfall indicates that supply constraints are already impacting traditional purchasing patterns before seasonal demand peaks.

Traditional Supplier Relationships and Dependency Structures

The region's supply base spans multiple continents, creating both diversification benefits and coordination challenges. Morocco, Russia, Saudi Arabia, and US Gulf Coast exporters have historically provided the bulk of phosphate imports, but geopolitical developments have disrupted these established trading relationships.

Current supplier dynamics reveal significant variations in pricing and reliability:

| Source Region | Product Focus | Current Challenges |

|---|---|---|

| Morocco | MAP/DAP | Freight rate escalation |

| Russia | MAP | Sanctions impact, premium pricing |

| Saudi Arabia | DAP/MAP | Red Sea shipping disruption |

| US Gulf Coast | DAP re-exports | Limited MAP availability |

At least five major importers remain active in the market, seeking approximately 25,000-30,000 tonnes for April-May loading. This fragmented import structure limits collective bargaining power and exposes individual buyers to greater price volatility compared to consolidated procurement systems.

Seasonal Demand Cycles and Agricultural Timing Factors

Southern hemisphere agricultural calendars create concentrated demand periods that amplify supply-demand imbalances. The January-May timeframe represents peak fertilizer application season, coinciding with corn planting across Argentina, Uruguay, and Paraguay.

Critical Seasonal Factors:

• Planting window constraints: Delayed fertilizer applications reduce crop yield potential

• Storage limitations: Port and inland storage capacity restricts inventory accumulation

• Weather dependencies: Soil conditions and precipitation patterns influence application timing

• Crop rotation schedules: Multi-year planning affects phosphate demand intensity

The seasonal concentration means that supply disruptions during peak months cannot easily be compensated through off-season purchasing, intensifying price pressure during critical agricultural periods. However, global recession risks may influence global demand patterns and pricing dynamics.

When big ASX news breaks, our subscribers know first

What Economic Forces Are Driving Phosphate Price Volatility in 2026?

Multiple macroeconomic forces have converged to create exceptional volatility in phosphate markets during 2026. Middle East conflicts, currency fluctuations, freight disruptions, and raw material inflation have combined to push prices to levels not seen since August 2022.

Middle East Conflict Impact on Global Supply Chains

Geopolitical tensions in the Middle East have fundamentally altered global phosphate trade flows. The war has caused phosphate prices to Argentina, Uruguay, and Paraguay to increase dramatically, with Argentinian DAP/MAP prices reaching $825/t CFR at the midpoint on March 19, 2026.

The conflict's impact extends beyond direct supply disruption to include:

• Route closures: Strait of Hormuz effectively closed to commercial shipping

• Insurance premiums: Marine war risk coverage costs escalated sharply

• Alternative routing: Extended voyage distances increase freight costs

• Supply uncertainty: Producers unable to guarantee delivery schedules

Recent transactions demonstrate the severity of price escalation. A 40,000-tonne Russian MAP cargo for April-May Southern Cone delivery was priced in the $910s/t CFR Argentina, representing the highest reference level documented in current market assessments.

Currency Fluctuations Affecting Import Purchasing Power

Local currency depreciation has compounded dollar-denominated fertilizer price increases across the Southern Cone. While specific exchange rate impacts vary by country, the general pattern shows that grain prices are not rising proportionally to match fertilizer cost inflation, creating unfavourable input-output price ratios for farmers.

Agricultural economists project that sustained phosphate prices above $850/t CFR could reduce regional corn planting intentions by 8-12%, as farmers shift toward crops with lower nutrient requirements or delay applications until more favourable pricing emerges.

Freight Rate Escalation and Logistics Bottlenecks

Maritime logistics constraints have added substantial costs to fertilizer imports. The differential between US Gulf prices and delivered costs to Argentina illustrates freight rate pressure:

• NOLA DAP barge prices: $640-690/st FOB

• Translated CFR Argentina: $740s-800s/t

• Freight, insurance, handling: Approximately $100-160/t premium

Red Sea shipping disruptions have forced vessels onto longer routes around Africa, adding 10-14 days to voyage times and increasing fuel consumption. Saudi suppliers face particular challenges, with 55,000 tonnes of DAP/MAP scheduled to load at Yanbu, but delivery timing remains uncertain due to route constraints.

According to research on global trade pinch points, these strategic shipping bottlenecks continue to create significant vulnerabilities in global supply chains.

Raw Material Cost Inflation Across the Fertilizer Value Chain

Upstream cost pressures have amplified finished fertilizer price increases. Higher raw material costs driven by Middle East supply disruptions affect multiple production inputs:

Primary Cost Components:

• Phosphate rock: Mining and transportation costs elevated

• Sulfur: Regional supply tightness increases acid production costs

• Ammonia: Energy-intensive production affected by gas price volatility

• Freight: Raw material shipping costs compound finished product logistics

The weekly price assessment for Moroccan MAP would translate to between the mid-$860s/t CFR and mid-$900s/t CFR, indicating that suppliers are pricing forward to account for continued cost pressures and supply uncertainty.

How Are Regional Farmers Adapting to Elevated Input Costs?

Agricultural producers across Argentina, Uruguay, and Paraguay are implementing various adaptation strategies to manage fertilizer cost inflation. These responses range from precision agriculture adoption to crop selection modifications and delayed purchasing decisions.

Soil Nutrient Testing and Precision Application Strategies

Farmers have begun conducting comprehensive soil studies to optimise phosphate application rates. This represents a shift from conventional blanket application toward variable-rate technology based on actual soil nutrient requirements.

Precision Agriculture Adoption Benefits:

• Reduced application rates: Soil testing identifies areas with adequate phosphorus levels

• Targeted applications: Variable-rate equipment optimises fertilizer placement

• Cost savings: Elimination of unnecessary applications in nutrient-sufficient zones

• Yield maintenance: Scientific approach maintains productivity while reducing inputs

However, soil testing and precision equipment require upfront investment and technical expertise, creating adoption barriers for smaller farming operations with limited capital and technical resources.

Alternative Fertilizer Sourcing and Substitution Patterns

Despite cost pressures, product substitution options remain limited due to crop nutritional requirements. Cheaper TSP alternatives are unlikely to replace DAP/MAP because the lack of nitrogen content makes them less attractive to corn farmers.

Substitution Constraints:

• Corn nitrogen requirements: Dual-nutrient fertilizers provide essential nitrogen component

• Application timing: Single-nutrient products require separate nitrogen applications

• Labour costs: Multiple application passes increase operational expenses

• Equipment limitations: Existing application equipment optimised for blended products

Some farmers are exploring alternative sourcing arrangements, including group purchasing initiatives and direct supplier relationships to bypass traditional distribution channels and reduce mark-up costs.

Crop Selection Modifications Based on Input Cost Ratios

High prices to curb southern Latam phosphate imports are influencing crop selection decisions as farmers evaluate input-output price ratios across different commodities. Crops with lower phosphate requirements or higher price premiums become more attractive under current cost structures.

Crop Selection Considerations:

• Soybeans: Lower phosphate requirements due to nitrogen fixation capability

• Wheat: Different application timing may allow price improvement waiting

• Corn: High nutrient requirements make input costs particularly impactful

• Pasture renovation: Delayed or reduced applications on forage areas

Last week's MAP price increases translate to over $1,000-1,020/t delivered to Argentinian farmers compared to $875-900/t delivered the previous week, representing a 14-16% cost increase in seven days.

Delayed Purchasing Decisions and Inventory Management

Farmers are implementing strategic purchasing delays, hoping for cost reductions or grain price improvements that would restore favourable input-output ratios. This approach carries yield risk but reflects rational economic decision-making under extreme price volatility.

Risk Management Approaches:

• Seasonal timing: Delaying purchases until late in application window

• Partial applications: Reducing rates rather than eliminating applications entirely

• Contract farming: Forward sales arrangements to secure revenue streams

• Input financing: Extended payment terms to manage cash flow impact

Import demand patterns indicate that farmers will probably delay remaining purchases, hoping for cost drops or crop price improvements. This behavioural shift prompts importers to remain cautious about forward commitments, potentially creating inventory shortages during peak application periods.

Which Supply Routes Remain Viable Despite Geopolitical Tensions?

Global shipping disruptions have forced phosphate suppliers and importers to identify alternative routing options while maintaining cost-effectiveness. Traditional trade flows through the Strait of Hormuz and Red Sea face significant constraints, necessitating creative logistics solutions. Additionally, US-China trade strategies are influencing global supply chain adaptations.

Red Sea Shipping Disruptions and Alternative Routing

The Red Sea corridor, historically a critical route for Middle Eastern phosphate exports, faces severe operational constraints. Saudi suppliers have 55,000 tonnes of DAP/MAP scheduled to load at Yanbu on the Red Sea, but shipment logistics for remaining volumes remain unclear while the Strait of Hormuz remains effectively closed.

Alternative Routing Options:

• Cape of Good Hope: Extended voyage time adds 10-14 days to South American delivery

• Suez Canal availability: Variable based on security conditions and insurance coverage

• Trans-Pacific routes: Limited capacity for Middle Eastern suppliers

• Regional transshipment: Mediterranean and Atlantic hub utilisation

Freight rates have escalated significantly due to longer routing requirements, with additional costs of $100-160/t affecting delivered prices to Southern Latin America. Insurance premiums for war risk coverage add further cost layers to already elevated transportation expenses.

US Gulf Coast Re-export Opportunities and Limitations

American Gulf Coast facilities have emerged as alternative supply sources through re-export activities. DAP barge sales at New Orleans (NOLA) have targeted Southern Cone re-export markets, with prices of $640-690/st FOB translating to $740s-$800s/t CFR Argentina.

US Gulf Coast Advantages:

• Established logistics: Direct shipping routes to South American ports

• Product availability: DAP supplies more readily available than MAP

• Credit arrangements: US suppliers offer established financing relationships

• Delivery reliability: Lower geopolitical risk compared to Middle Eastern sources

However, MAP supply tightness at NOLA limits re-export focus to DAP products, creating product mix constraints for importers requiring balanced nitrogen-phosphorus formulations for corn production systems.

Brazilian Transshipment Potential for Regional Distribution

Brazil's extensive port infrastructure and fertilizer handling capacity present opportunities for regional transshipment arrangements. While specific volumes remain limited, Brazilian facilities could serve as intermediate storage and distribution points for smaller regional markets.

Transshipment Benefits:

• Storage capacity: Large-scale facilities accommodate bulk shipments

• Freight optimisation: Consolidation of smaller parcels for onward shipment

• Supply security: Inventory buffer against supply chain disruptions

• Currency advantages: Brazilian real arrangements may offer cost benefits

Regional cooperation initiatives for bulk purchasing could leverage Brazilian infrastructure to achieve economies of scale and improve negotiating power with global suppliers.

Domestic Production Capacity Constraints and Expansion Plans

Southern Cone domestic phosphate production remains minimal, creating structural dependency on international suppliers. Argentina, Uruguay, and Paraguay lack significant phosphate rock deposits or integrated fertilizer manufacturing capacity.

Production Limitations:

• Raw material availability: Limited phosphate rock resources in region

• Capital requirements: Fertilizer plants require substantial upfront investment

• Technical expertise: Specialised knowledge for phosphoric acid production

• Market scale: Regional demand may not support efficient production scale

| Country | Historical Average (Jan-May) | 2026 Projected | Variance (%) |

|---|---|---|---|

| Argentina | 450,000t | 380,000t | -15.6% |

| Uruguay | 95,000t | 85,000t | -10.5% |

| Paraguay | 54,000t | 48,000t | -11.1% |

Long-term food system resilience may require regional investment in fertilizer production infrastructure, though current high prices to curb southern Latam phosphate imports make import substitution economically challenging without substantial policy support.

What Are the Macro-Economic Implications for Regional Agriculture?

Sustained phosphate price elevations carry profound implications for Southern Latin America's agricultural competitiveness, food security, and economic stability. The region's position as a major grain and oilseed exporter faces pressure from input cost inflation that may not be fully recoverable through commodity price increases.

Food Security Considerations Across the Southern Cone

High fertilizer costs create cascading effects throughout agricultural production systems, potentially affecting both export revenues and domestic food availability. While the region generally maintains food surpluses, input cost pressures could influence crop selection and yield optimisation decisions.

Food System Impacts:

• Crop yield reductions: Lower fertilizer applications may reduce per-hectare productivity

• Area allocation shifts: Farmers may reduce plantings of nutrient-intensive crops

• Product quality concerns: Reduced nutrient applications affect grain quality characteristics

• Price transmission: Higher production costs eventually influence food prices

Corn crop quality concerns have emerged following high yields but low nutrient content in recent harvests. Poor quality outlooks for upcoming crops may further discourage phosphate purchases, creating potential yield and quality trade-offs.

Export Competitiveness Impact on Grain and Oilseed Sectors

Regional agricultural exports compete in global markets where international competitors may face different input cost structures. Sustained fertilizer price premiums could erode South American competitiveness in corn, soybean, and wheat markets.

Competitiveness Factors:

• Cost structure comparison: Relative input costs versus major agricultural exporters

• Currency exchange effects: Local currency depreciation impacts competitiveness

• Yield productivity: Fertilizer reductions may affect yield competitiveness

• Quality premiums: High-quality grain commands price premiums in international markets

Grain prices in the region are not rising proportionally to match fertilizer costs, creating margin pressure that may persist throughout the 2026 crop cycle and affect planting decisions for subsequent seasons.

Furthermore, energy security transition considerations are affecting global commodity flows and pricing structures.

Government Policy Responses and Potential Subsidy Mechanisms

Policymakers across Argentina, Uruguay, and Paraguay face difficult decisions regarding agricultural input support programs. Budget constraints limit subsidy options, while agricultural sector health affects broader economic performance.

Policy Consideration Areas:

• Direct subsidies: Financial support for fertilizer purchases

• Import duty adjustments: Temporary tariff reductions on agricultural inputs

• Credit programs: Government-backed financing for seasonal input purchases

• Strategic reserves: Public sector fertilizer inventory management

Regional cooperation initiatives could provide collective negotiating power and bulk purchasing advantages that individual countries cannot achieve independently. Joint procurement mechanisms may offer cost savings and supply security benefits.

Long-term Agricultural Productivity and Soil Health Trade-offs

Reduced phosphate applications carry long-term implications for soil fertility and agricultural sustainability. Phosphorus is a non-renewable resource that, unlike nitrogen, cannot be replaced through biological processes or atmospheric fixation.

Sustainability Considerations:

• Soil phosphorus depletion: Reduced applications may lead to soil fertility decline

• Yield sustainability: Long-term productivity depends on adequate nutrient maintenance

• Environmental impacts: Precision application reduces environmental phosphorus loading

• Technology adoption: Sustainable intensification through precision agriculture

Soil testing initiatives represent positive developments toward sustainable nutrient management, potentially reducing total phosphate requirements while maintaining crop productivity through optimised application strategies.

How Do Current Prices Compare to Historical Volatility Patterns?

The 2026 phosphate price spike represents the most severe market disruption since August 2022, but historical analysis reveals recurring patterns of extreme volatility followed by market corrections. Understanding these cycles provides context for current conditions and potential future developments.

2008 and 2022 Price Spike Comparisons and Recovery Timelines

Previous fertilizer price crises offer insights into potential duration and recovery patterns for current market conditions. The 2008 food crisis and 2022 Ukraine war impacts created similar supply disruptions and price escalations.

Historical Price Spike Characteristics:

• 2008 Crisis: Food riots and export restrictions drove fertilizer prices to record levels

• 2022 Ukraine War: Black Sea grain corridor disruption and Russian supply sanctions

• 2026 Middle East War: Strait of Hormuz closure and Red Sea shipping disruption

• Recovery patterns: Typically 12-18 months for price normalisation following geopolitical resolution

Current prices reaching $825/t CFR Argentina for DAP/MAP represent the highest levels since August 2022, indicating that 2026 conditions have created comparable market stress to previous major disruption events.

Seasonal Pricing Patterns and Optimal Purchasing Windows

Fertilizer markets typically exhibit seasonal patterns aligned with global planting cycles, though geopolitical disruptions can overwhelm normal seasonal effects. Understanding these patterns helps importers optimise purchasing timing.

Normal Seasonal Patterns:

• Q1-Q2: Peak demand in Southern Hemisphere creates price strength

• Q3: Summer lull typically provides price relief opportunities

• Q4: Northern Hemisphere demand preparation begins price recovery

• Current disruption: Geopolitical factors override normal seasonal dynamics

Importers are reluctant to accept higher price levels while maintaining cautious purchasing approaches, suggesting that normal seasonal demand patterns may not apply under current extraordinary market conditions.

Forward Curve Analysis and Market Expectations

Forward pricing curves reflect market expectations for supply disruption duration and recovery timelines. Current forward assessments suggest continued elevated pricing through peak application seasons.

Moroccan MAP forward pricing between the mid-$860s/t CFR and mid-$900s/t CFR indicates suppliers expect continued supply constraints and elevated costs through the remainder of the 2026 season.

Forward Market Indicators:

• Contango structure: Forward prices higher than spot prices indicate expected supply improvement

• Backwardation: Spot premiums suggest immediate supply tightness

• Volatility expectations: Options pricing reflects uncertainty about resolution timing

• Basis patterns: Regional price differentials indicate logistics constraints

Correlation with Global Grain Price Movements

Fertilizer and grain price correlations typically strengthen during supply disruption periods, though 2026 patterns show divergence as grain prices fail to rise proportionally to input cost increases.

This decoupling creates unfavourable economics for farmers and suggests that either grain prices must rise or fertilizer prices must decline for normal planting patterns to resume. Historical precedent suggests that such imbalances eventually correct through supply-demand adjustments.

The next major ASX story will hit our subscribers first

What Market Dynamics Will Shape Future Phosphate Accessibility?

Long-term phosphate market accessibility depends on production capacity expansions, supplier diversification, technology adoption, and regional cooperation initiatives. Current high prices to curb southern Latam phosphate imports may accelerate structural changes that improve supply security.

Global Production Capacity Expansions and Timeline Expectations

High phosphate prices incentivise production capacity investments worldwide, though development timelines extend several years due to mining and processing infrastructure requirements.

Capacity Development Factors:

• Investment horizons: New phosphate mines require 5-7 years development time

• Capital intensity: Mining and processing facilities require substantial upfront investment

• Regulatory approvals: Environmental and mining permits extend development timelines

• Technical challenges: Phosphoric acid production requires specialised expertise

Current price levels provide economic incentives for capacity expansion, but relief from new supply sources will not materialise until late in the decade at earliest.

Alternative Supplier Development in Africa and Asia

Emerging phosphate producers in Africa and Asia may provide supply diversification opportunities for South American importers. Countries with significant phosphate rock reserves are developing export-oriented production capacity.

Emerging Supplier Regions:

• West Africa: Senegal and Togo phosphate development projects

• East Africa: Tanzania and Mozambique mineral resource development

• Central Asia: Kazakhstan and Uzbekistan fertilizer industry expansion

• Southeast Asia: Vietnam and Indonesia domestic capacity growth

These alternative sources could provide supply diversification benefits and competitive pricing pressure on traditional suppliers, though establishing new trade relationships requires time and investment.

Technology Adoption for Enhanced Nutrient Efficiency

Agricultural technology advances offer potential for reduced fertilizer requirements through precision application, enhanced formulations, and biological supplements that improve nutrient efficiency.

Efficiency Enhancement Technologies:

• Variable rate application: GPS-guided equipment optimises fertilizer placement

• Enhanced efficiency fertilizers: Controlled-release and inhibitor technologies

• Biological supplements: Microbial inoculants improve phosphorus availability

• Soil health practices: Cover crops and organic matter improve nutrient retention

Farmer adoption of soil testing and precision agriculture represents positive progress toward sustainable intensification that maintains yields while reducing input requirements and environmental impact.

Regional Cooperation Initiatives for Bulk Purchasing Power

Collective procurement mechanisms could provide Southern Cone countries with enhanced negotiating power and supply security compared to individual national purchasing programs.

Cooperation Benefits:

• Volume aggregation: Combined purchases achieve economies of scale

• Risk distribution: Shared supply sources reduce individual country exposure

• Infrastructure utilisation: Shared storage and logistics facilities

• Technical expertise: Collaborative research and development initiatives

Regional integration efforts could extend to fertilizer infrastructure development, though political and economic coordination challenges require sustained commitment from participating governments.

How Are Financial Markets Responding to Agricultural Input Inflation?

Financial markets are adapting to agricultural input volatility through modified trading strategies, adjusted credit policies, and enhanced risk management products. These adaptations affect capital availability and risk pricing for agricultural enterprises.

Commodity Trading Patterns and Hedging Strategies

Fertilizer price volatility has intensified interest in hedging mechanisms, though limited financial instrument availability constrains risk management options for many agricultural enterprises.

Risk Management Developments:

• Forward contracting: Increased use of supply agreements with price protection

• Financial derivatives: Limited options for phosphate price hedging

• Basis trading: Regional price differential management strategies

• Currency hedging: Exchange rate protection for import-dependent operations

The absence of liquid phosphate futures markets limits hedging options compared to grain and oilseed commodities, creating asymmetric risk exposure for agricultural producers.

Agricultural Credit Availability and Financing Conditions

Lenders are adjusting credit policies to account for increased input cost volatility and margin pressure affecting agricultural borrowers. Risk assessment models incorporate fertilizer cost projections and crop price expectations.

Credit Market Adjustments:

• Margin requirements: Higher equity requirements for seasonal financing

• Interest rate adjustments: Risk premiums reflect input cost volatility

• Collateral valuations: Asset values adjusted for margin pressure impacts

• Repayment terms: Extended payment schedules accommodate cost pressures

Input financing programs through fertilizer suppliers and equipment manufacturers provide alternative credit sources, though often at premium rates compared to traditional agricultural lending.

Currency Hedging Considerations for Import-Dependent Economies

Exchange rate volatility compounds fertilizer cost uncertainty for South American importers purchasing dollar-denominated commodities with local currencies subject to depreciation pressure.

Currency Risk Factors:

• Dollar strength: US dollar appreciation increases local currency costs

• Central bank policies: Interest rate differentials affect exchange rates

• Commodity revenues: Export earnings provide natural currency hedge for some producers

• Economic uncertainty: Political and economic instability affects currency stability

Large-scale agricultural operations increasingly utilise currency hedging strategies to manage exchange rate exposure on input purchases, though smaller operations often lack access to sophisticated financial instruments.

Investment Flows into Regional Fertilizer Infrastructure

High fertilizer prices are attracting investment interest in regional production capacity, storage infrastructure, and logistics capabilities that could improve long-term supply security.

Investment Opportunities:

• Storage facilities: Strategic inventory capacity for price volatility management

• Blending operations: Local formulation capabilities for customised products

• Logistics infrastructure: Port and transportation efficiency improvements

• Technology adoption: Precision agriculture equipment and services

Private equity and infrastructure funds are evaluating agricultural input supply chain investments, though regulatory environments and return requirements influence capital allocation decisions.

According to fertilizer trade analysis, global fertilizer markets have experienced significant restructuring following recent geopolitical disruptions.

Strategic Implications for Regional Food System Resilience

Current phosphate market disruptions highlight structural vulnerabilities in South American agricultural input systems. Building resilience requires coordinated efforts across supply chain diversification, domestic production development, and policy framework enhancement.

Supply Chain Diversification Imperatives

Over-reliance on specific supplier regions and shipping routes creates systemic vulnerability to geopolitical disruptions. Strategic diversification across multiple dimensions reduces exposure to individual supply source failures.

Diversification Strategies:

• Geographic suppliers: Balanced sourcing across multiple continents

• Product formulations: Flexible application of different phosphate products

• Shipping routes: Multiple logistics pathways reduce transportation risk

• Contract terms: Varied supplier relationships and pricing mechanisms

Current supply data showing 488,000 tonnes from multiple sources demonstrates existing diversification, though concentration in conflict-affected regions created vulnerability during 2026 disruptions.

Domestic Production Investment Opportunities

Long-term food security may require regional investment in fertilizer production capacity, despite current economic challenges for import substitution projects.

Production Development Considerations:

• Resource availability: Limited phosphate rock deposits constrain raw material access

• Technology transfer: International partnerships could provide technical expertise

• Market integration: Regional cooperation could support viable production scale

• Policy support: Government incentives may be necessary for economic viability

Current price levels of $825-910/t CFR create potential economic justification for regional production investment, though sustainable economics depend on long-term price expectations rather than temporary disruption premiums.

Regional Integration Potential for Fertilizer Procurement

Collective action across Argentina, Uruguay, and Paraguay could enhance negotiating power and supply security through coordinated purchasing and infrastructure development.

Integration Benefits:

• Bulk purchasing power: Combined volumes improve supplier negotiating position

• Risk sharing: Distributed supply arrangements reduce individual country exposure

• Infrastructure efficiency: Shared storage and logistics reduce per-unit costs

• Technical cooperation: Collaborative research and development initiatives

Regional fertilizer integration could follow successful models in other commodity sectors, though political coordination and economic burden-sharing arrangements require careful negotiation.

Policy Framework Development for Agricultural Input Security

Governments across the Southern Cone may need to develop comprehensive policy frameworks addressing agricultural input security as a component of national food security strategy.

Policy Framework Elements:

• Strategic reserves: Government-managed fertilizer inventory systems

• Trade facilitation: Streamlined import procedures for agricultural inputs

• Emergency protocols: Crisis response mechanisms for supply disruptions

• Investment incentives: Support for domestic production and storage infrastructure

The current crisis demonstrates that agricultural input security deserves policy attention comparable to energy security, given agriculture's fundamental importance to economic stability and food security.

Disclaimer: This analysis is based on market data and industry observations as of March 2026. Fertilizer markets remain highly volatile due to ongoing geopolitical developments. Investment and purchasing decisions should incorporate comprehensive risk assessment and professional consultation. Price projections and market forecasts represent estimates based on current information and are subject to significant uncertainty.

Looking to Capitalise on Commodity Market Volatility?

Discovery Alert's proprietary Discovery IQ model provides instant notifications on significant ASX mineral discoveries, helping investors identify actionable opportunities ahead of broader market movements during periods of global supply chain disruption and commodity price volatility. Explore how historic discoveries have delivered substantial returns and begin your 14-day free trial today to position yourself strategically in dynamic resource markets.