May 12, 2026

The Architecture of a Generational Gold Thesis

Few financial frameworks capture the imagination of institutional investors quite like a well-reasoned, historically grounded price target that departs radically from consensus. When a decades-long veteran of the mining industry, someone who helped pioneer an entirely new business model within it, states a price target with conviction and outlines the precise mechanics behind it, it warrants serious examination rather than dismissal.

The framework underpinning the Pierre Lassonde gold price target of $17,250 is not a speculative number plucked from enthusiasm. It is rooted in ratio analysis, monetary history, structural supply constraints, and a generational theory of fiscal memory that has proven surprisingly consistent across two centuries of economic cycles. Understanding why this target may be more credible than it first appears requires unpacking each of these layers individually.

When big ASX news breaks, our subscribers know first

Is the Global Financial System Quietly Repricing Gold as a Reserve Asset?

How Central Bank Accumulation Is Rewriting the Rules of Reserve Management

The most significant and often underappreciated development in global gold markets over the past several years has been the systematic accumulation of physical gold by sovereign reserve managers. These are not speculative traders. They are the most conservative capital allocators on the planet, and their behaviour is changing in ways that have profound structural implications.

Global gold mine production runs at approximately 3,800 tonnes per year. Of that, central bank gold reserves are absorbing nearly half, representing over 1,700 tonnes flowing into sovereign vaults annually. This is not tactical opportunism. It represents a structural repositioning in reserve portfolio construction that has been building for years.

The evidence is visible in reserve composition data:

- The US dollar's share of global foreign exchange reserves has declined from over 80% to approximately 56%

- Gold's weighting in central bank reserves has more than doubled, now exceeding 20%

- Nations ranging from Poland to Azerbaijan to Russia have actively increased gold allocations

- China and its domestic population collectively absorb more than half of all gold mined annually

Pierre Lassonde, co-founder of Franco-Nevada and a former chairman of the World Gold Council, has observed this shift firsthand. During his tenure leading the World Gold Council, India alone was consuming over 1,000 tonnes annually for jewellery. Today, the demand profile has fundamentally changed: the central banks of China and the Chinese people collectively dominate physical demand. The jewellery market, once the backbone of gold demand, is described as a shadow of what it was two decades ago.

When sovereign reserve managers, the most conservative capital allocators on earth, systematically increase gold exposure over multiple years, it signals a fundamental reassessment of monetary risk, not a speculative trade.

The Dollar's Dual Role: Reserve Currency vs. Fiscal Liability

Gold operates as a commodity approximately 90% of the time. The other 10% is where its true monetary character emerges: when the credibility of the US dollar as the global reserve currency is in question, gold assumes the role of currency of last resort.

That 10% scenario is not a distant hypothetical. The US fiscal deficit for 2026 is projected to exceed 7.9% of GDP, a ratio historically associated with emerging market stress rather than reserve currency issuers. Total US national debt is approaching $40 trillion, with annual interest payments alone exceeding $1 trillion.

This debt load creates what Lassonde describes as a policy trap. The Federal Reserve cannot replicate the Volcker-era rate shock of the early 1980s because the leverage embedded in today's economy, across sovereign, corporate, and consumer balance sheets, would make such a move systemically destabilising. In 1981 when Reagan took office, total US national debt stood at $1 trillion. Today, that figure represents only what the US pays in interest each year. The structural constraint on monetary policy normalisation does not weaken the gold thesis — it strengthens it considerably.

Compounding this dynamic is the emergence of parallel financial infrastructure designed to bypass dollar-denominated settlement. China has constructed an alternative payment network to the SWIFT system, enabling countries like Iran to receive oil payments in yuan and recirculate those funds entirely outside the dollar architecture. Lassonde notes this system is growing at a pace that can only be described as exponential, with usage reportedly expanding by 50 to 100% every six months as more nations seek to reduce their exposure to dollar weaponisation through sanctions.

What Is Pierre Lassonde's $17,250 Gold Price Target Based On?

Breaking Down the Dow-to-Gold Ratio Framework

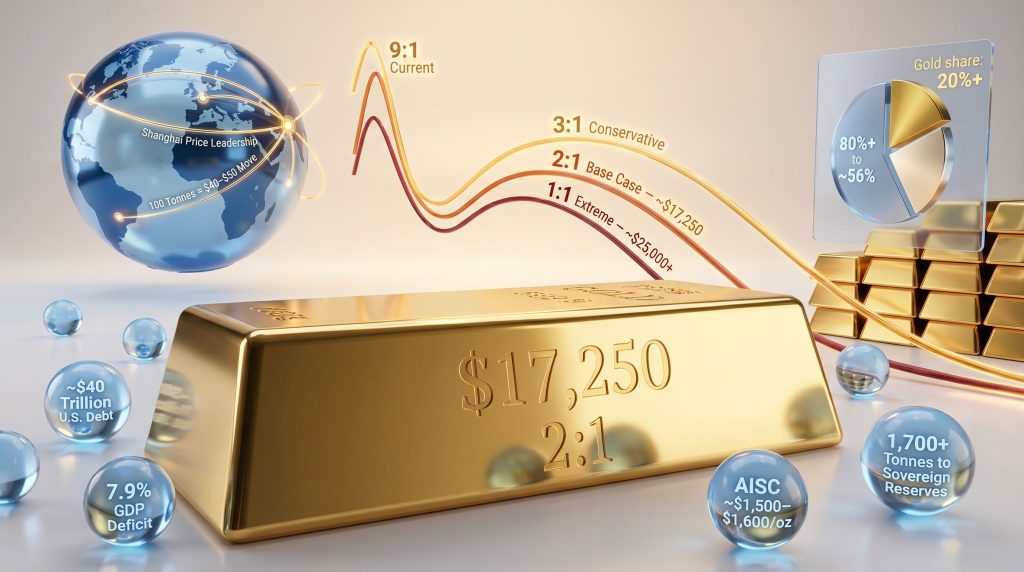

The analytical foundation of the Pierre Lassonde gold price target of $17,250 is the Dow-to-Gold ratio, a measure of how many ounces of gold are required to purchase the Dow Jones Industrial Average. Historically, this ratio has converged toward 1:1 or 2:1 at the climax of major gold bull markets. Furthermore, gold's $3,000 milestone earlier in this cycle reinforced just how rapidly structural macro forces can drive price discovery beyond consensus expectations.

| Scenario | Dow Jones Level | Dow-to-Gold Ratio | Implied Gold Price |

|---|---|---|---|

| Extreme Reversion (1:1) | ~$25,000–$50,000 | 1:1 | ~$25,000–$50,000 |

| Base Case (Lassonde) | ~$34,500 | 2:1 | ~$17,250 |

| Conservative Scenario | ~$42,000 | 3:1 | ~$14,000 |

| Current Market | ~$40,000–$42,000 | ~9:1 | ~$4,700 |

Lassonde's base case targets a 2:1 ratio, implying gold at approximately $17,250, which he describes with considerable conviction as a figure he believes the market will reach within approximately three years, though he acknowledges the timeline could compress or extend depending on fiscal policy trajectories and macro velocity. The more extreme 1:1 scenario remains a tail risk rather than his primary working assumption.

The generational cycle theory underlying this framework is particularly compelling. Lassonde draws on a pattern observable across modern monetary history: roughly every two and a half generations, societies repeat the same fiscal and monetary mistakes, having lost the institutional memory of the consequences from the prior episode. The 1930s mirrored the conditions of the late 1970s approximately 50 years later. The current period, spanning roughly 2026 to 2030, sits another 50 years beyond that inflection point.

The 1% Capital Flow Theorem

The supply-side constraint on gold is perhaps the most underappreciated dimension of Lassonde's framework. Consider the numbers:

- Total above-ground gold ever mined: approximately 222,000 tonnes

- Held in central bank vaults as permanent strategic reserves: approximately 50,000 tonnes

- Locked in heirloom jewellery across generations: approximately 100,000 tonnes

- Annually transactable supply: approximately 5,000 to 6,000 tonnes

- Even at $20,000 per ounce, analysts estimate no more than 10,000 tonnes could realistically be extracted annually from existing and undiscovered reserves

Against this backdrop, consider what happens if just 1% of total global savings were redirected into gold. According to Lassonde's analysis, gold would exceed $25,000 per ounce essentially overnight, because the market is structurally too small to absorb capital of that scale at anywhere near current prices. The gold market is a niche. The entire investable universe of senior and intermediate mining companies — roughly 40 companies — carries a combined market capitalisation that is a fraction of a single large-cap technology company.

The core structural reality: supply cannot respond fast enough to moderate a demand surge of any meaningful scale. Even a small reallocation from global institutional portfolios would overwhelm available physical supply.

How Does the 1970s Macro Cycle Compare to Today's Setup?

Structural Parallels: Then vs. Now

The parallels between the late 1970s macro environment and the current period are striking, though the critical differences are equally instructive.

| Macro Variable | Late 1970s | 2025–2026 |

|---|---|---|

| Inflation Trajectory | Rising annually, peaked ~13–14% | Sticky; US CPI potentially heading toward 4–4.5% by year-end |

| Interest Rate Direction | Rising, peaked ~17% mortgage rates | Constrained by debt load; Fed policy structurally limited |

| Dollar Purchasing Power | Declining | Under structural pressure from deficit monetisation |

| Gold Performance | Rose from ~$90 (1975) to $800 (1980), nearly 9x | Multi-year bull cycle from ~$1,200 base |

| Total US Debt | ~$1 trillion in 1981 | Approaching $40 trillion |

| Leverage in Economy | Very low | Extreme across sovereign, corporate, and consumer |

The critical distinction is leverage. In the late 1970s, the Federal Reserve under Paul Volcker could raise rates to 17% because the economy carried minimal debt. Today, with approaching $40 trillion in national debt, an equivalent rate shock would trigger cascading defaults across every leveraged sector of the economy. This is not a sign that the gold thesis is weaker than it was in the 1970s. It is precisely the reason the thesis is arguably stronger: the policy tools that ended the previous gold cycle are no longer available.

Lassonde uses the lens of his own investment history to illustrate the leverage embedded in mining equities during this kind of cycle. He recalls purchasing shares in Free State Geduld, a South African underground gold mine, at $5 per share in 1976 and selling them at $105 in 1980 — a more than twenty-fold return driven by the operating leverage inherent in a mine with stable costs during a period of surging gold prices. The mechanics of that trade are directly applicable today. In addition, understanding gold's impact on mining equities in the current cycle reveals how underappreciated this operating leverage remains across institutional portfolios.

What Could Break the Gold Bull Case?

While the structural backdrop is strongly gold-positive, intellectual honesty requires acknowledging the scenarios that could disrupt this framework:

- A recession severe enough to force broad asset liquidation, including physical gold positions, though historically such episodes prove temporary for monetary metals

- A credible political pivot toward fiscal consolidation requiring a leader willing to simultaneously raise taxes and reduce entitlements — a combination that is historically rare and electorally costly

- A Volcker-style rate shock, theoretically possible but practically constrained by the existing $40 trillion debt burden

- Until any of these conditions materialise at sufficient scale, the structural backdrop remains oriented toward hard asset appreciation

Lassonde is direct on this point: the United States has a demonstrated historical capacity to walk right to the edge of a financial precipice, examine it, and step back. The question is not whether course correction is possible, but when the political will to execute it materialises. Until it does, the gold thesis remains intact. Consequently, forecasts of major price spikes as global currencies face devaluation continue to gain credibility among institutional analysts.

Is Eastern Price Discovery Permanently Shifting Gold's Centre of Gravity?

The Shanghai Gold Exchange and the Redistribution of Pricing Power

One of the most consequential and least understood shifts in global gold markets is the migration of physical price discovery from London and New York toward Shanghai. The LBMA and COMEX gold markets still influence screen prices, but as Lassonde articulates with precision: whoever buys the last ounce of physical gold sets the marginal price.

Chinese investors, operating in a domestic market where cryptocurrency is banned, treat gold as the primary alternative store of value. This demand is not purely financial. It is culturally embedded across generations in ways that Western investment frameworks struggle to fully model. Lassonde recalls visiting a three-story gold store in Beijing where every product — from jewellery to bullion bars to decorative items — is purchased by consumers who describe their motivation as aesthetic but carry a financial insurance mentality in parallel.

The result of this physical accumulation concentrated in the East is measurable price volatility:

- Gold can move $100 or more per ounce during the Shanghai session before London even opens

- A single 200-tonne dump in a morning session can move the market by approximately $100 per ounce

- One trader on the Shanghai exchange reportedly generated approximately $500 million in profit by effectively cornering the silver market, illustrating the concentrated physical power now residing in Asian markets

The Elasticity of Gold Price to Volume

During his tenure as chairman of the World Gold Council, Lassonde commissioned a study on the price elasticity of gold relative to volume. The findings are instructive for understanding current market dynamics:

- Every 100 tonnes of gold bought or sold moves the gold price by approximately $40 to $50

- A 200-tonne transaction therefore carries the capacity to move prices by roughly $100

- This sensitivity makes the shift of physical settlement toward the East a development with direct and immediate implications for Western investors still relying primarily on paper-based exposure

Furthermore, monitoring gold-silver ratio insights alongside these Eastern volume dynamics provides a useful complementary lens for assessing relative monetary metal valuations in real time.

Tether Gold and the Emergence of Gold-Backed Digital Currencies

A new and structurally significant demand vector has emerged outside both the traditional jewellery market and institutional frameworks: gold-backed digital currencies. Tether Gold is currently purchasing approximately 3 tonnes of gold per month to back a platform operating approximately 540 million wallets with $150 to $160 billion in backing. This represents a new class of demand that functions as a parallel monetary system anchored to physical gold, yet accessible across digital infrastructure globally.

This development is particularly meaningful in economies where dollar alternatives are actively sought. Gold-backed digital currencies could become a sustained and growing demand vector that existing supply and price models have not yet fully incorporated.

Why Are Gold Mining Equities Still Undervalued Despite Record Gold Prices?

The Margin Expansion Equation the Market Has Not Priced

With all-in sustaining costs for well-run miners running at approximately $1,500 to $1,600 per ounce, the margin expansion available at current gold prices is extraordinary. Yet equity markets are largely valuing mining companies on prevailing prices rather than the forward margin trajectory implied by the structural macro setup.

Consider the arithmetic:

- At $4,700 gold: operating margin approximately $3,000+ per ounce

- At $7,000 gold: margins more than double from today's levels

- At $17,250 gold: margins expand by a factor of approximately five

- Cash operating costs for well-run operators run at approximately $1,000 to $1,200 per ounce, with the gap between cash cost and AISC representing sustaining capital investment

The core mispricing: equity markets are applying today's gold prices to valuation models, not the forward margin trajectory implied by structural monetary deterioration. The operating leverage embedded in mining equities at these cost structures remains largely unrecognised in current share prices.

Lassonde is unambiguous about the implication: any mining company not generating strong cash flow, paying dividends, and returning capital to shareholders at these gold prices has a management problem, not a gold price problem.

What Separates Structurally Sound Miners from Metal-Price Beneficiaries?

The framework for distinguishing genuinely well-managed operators from companies simply being rescued by a rising gold price comes down to several compounding metrics:

- Ounces per share growth: is management increasing production per share, or diluting shareholders through repeated equity issuances to fund growth?

- Free cash flow per share: is cash generation being returned to shareholders or recycled into marginal projects with questionable returns?

- Share buyback programmes: historically absent from the gold sector for approximately 50 years, now emerging for the first time in this cycle

- Dividend initiation and growth: companies generating surplus cash at current gold prices should be initiating or expanding distributions

- Internal growth funding: projects funded from operating cash flow rather than equity raises signal genuine financial health and management discipline

- Reserve life and jurisdictional quality: long-life assets in stable, well-regulated jurisdictions command a structural valuation premium that compounds over time

The Golden Halo Premium

Lassonde identifies a specific valuation premium he calls the golden halo, earned by companies that combine exceptional ore body quality, disciplined capital allocation, and consistent shareholder return programmes. This premium manifests as an elevated share price per ounce of production relative to peers. It is earned through sustained execution, not asset scale alone, and it represents the market's recognition that management can be trusted to convert a rising gold price into per-share value rather than dilute it away.

The next major ASX story will hit our subscribers first

How Has Capital Discipline Changed the Gold Mining Sector in This Cycle?

A Structural Break from the Boom-Bust Playbook

The 2010 to 2013 period stands as a cautionary study in how not to manage a gold mining company during a bull market. Massive acquisition premiums, cost blowouts, over-leveraged balance sheets, and growth-at-any-cost strategies destroyed hundreds of billions in shareholder value. Lassonde is direct: the CEOs responsible for those disasters were largely removed, and the generation of management teams that replaced them absorbed the lessons completely.

The current cycle represents a structural departure:

- Mergers of equals with no control premiums are the new M&A template

- Internal growth pipelines are funded from operating cash flow, not equity issuance

- Buybacks have become a feature of the sector for the first time in approximately 50 years

- Shareholder activism has intensified, and management compensation is increasingly aligned with per-share value creation rather than production growth

| Metric | Benchmark for Well-Run Operators |

|---|---|

| All-In Sustaining Cost | Up to $1,600/oz |

| Cash Cost (operating only) | ~$1,000–$1,200/oz |

| Free Cash Flow Generation | Positive at current gold prices |

| Dividend Policy | Initiated or growing |

| Share Buyback Activity | Active or authorised |

| Dilution Rate | Minimal; ounces per share growing |

| Internal Growth Funding | Self-funded from operations |

Is the Royalty and Streaming Model Still the Optimal Gold Exposure Vehicle?

Price Optionality vs. Land Optionality

Lassonde, who pioneered the royalty and streaming model through the founding of Franco-Nevada, identifies two distinct forms of optionality available to gold investors:

- Price optionality: exposure to gold price appreciation through operating leverage, highest in well-run producers with low all-in sustaining costs

- Land optionality: exposure to discovery upside on large, infrastructure-rich land packages, highest in senior and intermediate miners with extensive tenement holdings and skilled geological teams

The oldest adage in the mining business — that the best place to find a gold mine is right beside an existing one — encapsulates why large land packages with existing infrastructure are disproportionately valuable. The Carlin Trend in Nevada has yielded approximately 25 separate deposits, with Barrick's Gold Strike mine alone containing 15 million ounces, found adjacent to Newmont's existing operation. Infrastructure already in place collapses development timelines and capital requirements dramatically.

A balanced hard asset allocation in this cycle may include a royalty company for stability and diversification, combined with a high-quality intermediate producer for operating leverage, capturing both forms of optionality simultaneously.

Why Copper-Gold Deposits Represent the Highest-Conviction Mining Asset

Lassonde is categorical in identifying copper-gold deposits as the most strategically valuable mining assets available for this cycle, drawing on a dual thesis:

- The global energy transition requires doubling copper consumption over the next 20 years, as electricity must displace carbon molecules across terminal energy use

- Currently, approximately 80% of terminal energy is carbon-based and 20% is electricity — reaching climate targets requires inverting that ratio

- Copper is the only viable conductor of electricity at scale, with no substitution available in the required timeframe

- Copper prices have moved from approximately $2 per pound to approximately $6 per pound, reflecting structural supply deficits beginning to emerge

- Long-life copper-gold porphyry systems carry 50 to 100-year mine lives, a durability unmatched in single-commodity gold mining

- Freeport-McMoRan's deposit in Indonesia, for example, produces approximately 2 million ounces of gold as a byproduct of copper operations, illustrating the scale of value achievable from these combined systems

Deposits with roughly a two-thirds copper and one-third gold composition represent what Lassonde describes as the closest thing to a perfect mining asset: simultaneous exposure to industrial energy demand and monetary stress — two of the most powerful structural tailwinds of the current decade.

What Is Canada's Role in the Next Global Mining Cycle?

The Policy Environment and the Structural Obstacles

Canada holds the second-largest land mass in the world and carries significant undiscovered mineral endowment, particularly across its northern territories. Yet the early 2000s saw the departure of Canada's major mining champions, including Noranda, Falconbridge, Inco, and Alcan, representing a generational loss of domestic mining capacity that the country has spent two decades attempting to rebuild.

The current federal government has signalled a more constructive posture toward resource development, with stated intentions to reduce permitting timelines and support mine construction. However, Canada's permitting environment remains structurally complex due to overlapping federal, provincial, and Indigenous jurisdictions — a challenge without equivalent in comparable mining jurisdictions like Nevada, which Lassonde describes as probably the easiest place in the world to conduct mining business.

A practical path forward Lassonde has advocated involves the federal government deferring to provincial mineral jurisdiction and tagging along to deliver its component parts — such as water approvals — without directing the overall permitting process. This structural change alone could reduce permitting timelines by approximately 50%.

The Permitting Crisis: A Quantified Value Destruction Problem

Permitting timelines in Canada have extended from a historical norm of 2 to 3 years to current averages of 5 to 7 years in many cases. Lassonde describes this zone as the killing fields for project economics, and the mathematics support his assessment:

- A $10 billion project discounted at 10% per year over 10 years approaches zero net present value

- At zero NPV, institutional capital cannot be raised and projects cannot be financed regardless of the underlying mineral resource quality

- Cutting permitting timelines by 50%, to approximately 3 to 4 years, would materially restore project economics and reopen institutional capital to Canadian resource development

The Pension Fund Allocation Gap

Canada's Maple 8 pension funds collectively manage approximately $3 trillion in assets. The allocation pattern reveals a striking disconnect from the domestic resource sector:

| Fund Type | Allocation to Canadian Equities | Allocation to Private Equity | Notes |

|---|---|---|---|

| Canadian Pension Plan (CPP) | ~2% | ~34% | Private equity mark-to-market risk elevated |

| Australian Superannuation | Higher domestic weighting | ~5% | Franked dividend system incentivises domestic equity |

| Quebec Pension Fund (CDPQ) | Dual mandate: returns and domestic economy | Variable | Model for strategic domestic investment |

Lassonde is unsparing in his assessment of this allocation, describing it as an indictment of fund managers who have effectively declared their own domestic market uninvestable while concentrating approximately 34% of CPP assets in private equity — a concentration he identifies as carrying significant mark-to-market risk that may not yet be reflected in reported valuations.

By contrast, Australian superannuation funds carry approximately 5% in private equity, a fraction of CPP's exposure, and benefit from a franked dividend system where corporate profits already taxed at the company level can be distributed to shareholders without additional personal tax liability. In Canada, the combined corporate and personal tax burden on dividend income can approach 64 to 70%, a rate Lassonde characterises as economically confiscatory and structurally hostile to domestic equity investment.

What Are the Key Signals That Confirm a Full Mining Cycle Is Underway?

Indicators to Monitor Across the Remainder of 2026

Lassonde is clear that the current environment is already a full mining cycle, not a prelude to one. The evidence is visible across multiple dimensions simultaneously. Key signals worth monitoring for confirmation and acceleration include:

- Institutional allocation shift: evidence of pension funds, sovereign wealth funds, or large asset managers initiating or expanding hard asset allocations

- Junior discovery activity: high-grade discoveries feeding into the acquisition pipeline of intermediate and senior producers

- M&A premium discipline: continued absence of value-destructive takeover premiums, signalling management teams remain focused on per-share value creation

- Margin expansion recognition: equity re-ratings of producers as markets begin pricing forward margins rather than trailing earnings

- Shanghai price leadership: continued evidence that physical settlement in Asia drives price discovery ahead of Western paper markets

- Central bank reserve data: quarterly IMF reporting showing continued reduction in dollar reserve weighting and corresponding gold accumulation

Lassonde notes that investor psychology in this cycle still reflects a wall of worry: people are asking whether gold has risen too far, whether prices will revert, whether the thesis is played out. In his reading, this sentiment pattern is characteristic of the middle of a major gold cycle, not its end. The late stages of a gold bull market, particularly one influenced by Asian physical markets, will likely look considerably more euphoric — potentially approaching what he describes as a casino-type atmosphere emanating from Shanghai. For instance, Lassonde's complete interview on gold replacing the dollar provides a comprehensive account of his full framework and conviction behind the Pierre Lassonde gold price target of $17,250 by 2030.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any securities or commodities. All forecasts, price targets, and projections referenced herein represent the views of the individuals attributed and are inherently speculative. Past performance of gold or mining equities is not indicative of future results. Readers should conduct their own independent research and consult a qualified financial adviser before making any investment decisions.

Want to Position Yourself Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries hit the ASX, transforming complex geological and commodity data into actionable insights for both short-term traders and long-term investors — explore historic discoveries and their returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to secure your market-leading edge before the next major find is announced.