June 15, 2026

How a Single Annual Forum in China Is Reshaping the Global Platinum Market

Few commodities tell a more compelling story about the collision of industrial policy, financial innovation, and energy transition than platinum group metals (PGMs). Shanghai Platinum Week and platinum demand in China have become central to understanding where the global PGM market is heading. For most of the twentieth century, platinum's demand profile was relatively predictable: jewellery fabrication, autocatalysts, and a modest industrial base. That architecture is now being dismantled and rebuilt from scratch.

Understanding where platinum demand is heading over the next decade requires looking beyond spot prices and mine supply schedules. It requires understanding how China's policy apparatus is reclassifying metals, how new financial infrastructure is shifting price discovery power eastward, and why an annual conference held in Chinese cities is increasingly functioning as one of the most consequential intelligence forums in global commodities markets.

When big ASX news breaks, our subscribers know first

Shanghai Platinum Week: Architecture of a Market-Shaping Forum

Shanghai Platinum Week has evolved considerably since its inaugural edition in 2021. What began as a regional engagement platform has matured into the world's most concentrated annual gathering of PGM producers, industrial consumers, financial market participants, recycling industry representatives, and policy-adjacent organisations.

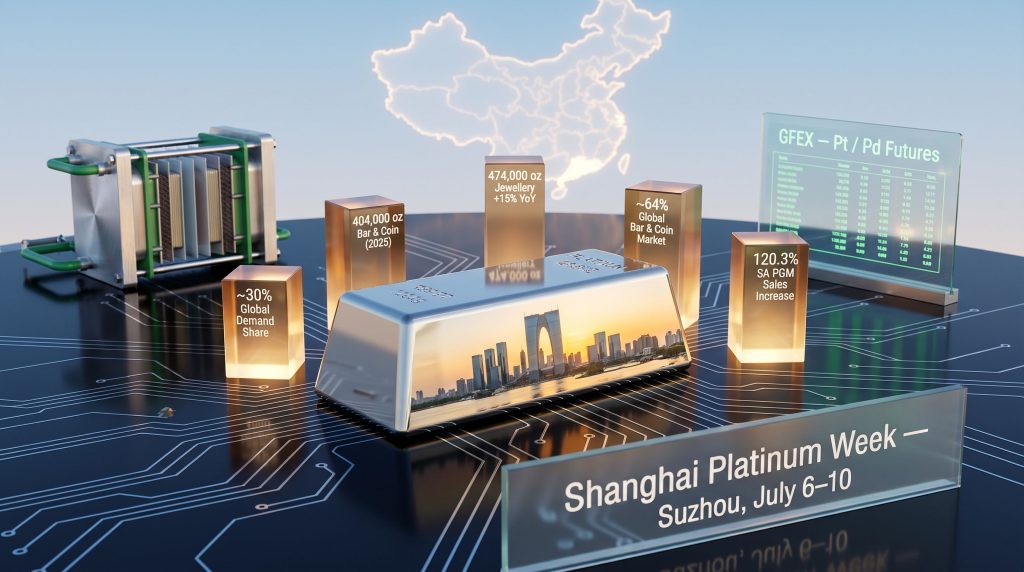

The 2026 edition is scheduled for July 6 to 10 in Suzhou, organised under the auspices of the World Platinum Investment Council (WPIC). The event's centrepiece is the China PGMs Market Summit, which brings together a wide cross-section of industry leaders to address demand trajectories, market infrastructure developments, and emerging end-use sectors. Supporting programming includes specialised conferences, product launches, research report releases, and structured networking.

A distinguishing feature of the event is its institutional connections. The precious metals industrial committee of the China Material Recycle Association participates actively, and its membership collectively represents:

- Approximately 85% of China's precious metal recycling and refining market share

- Approximately 60% of China's precious metal trading market share

This concentration of industry influence within a single forum means that the outcomes of Shanghai Platinum Week carry real economic weight. The creation of the Guangzhou Futures Exchange (GFEX) platinum and palladium futures contracts in late 2025 is itself a product of the relationships and policy dialogue cultivated through successive Shanghai Platinum Weeks, making the event a genuine market infrastructure catalyst rather than a ceremonial gathering.

What Is Shanghai Platinum Week?

Shanghai Platinum Week is an annual PGM industry summit held in China, organised in partnership with the World Platinum Investment Council (WPIC). It brings together producers, industrial users, financial institutions, and market participants to assess China's PGM demand outlook, financial market infrastructure developments, and emerging end-use sectors. The 2026 event takes place July 6 to 10 in Suzhou.

China's Structural Reclassification of Platinum: From Ornament to Strategic Asset

The most underappreciated dimension of China's platinum story is not the volume of demand, but the nature of its reclassification within China's industrial policy framework. Platinum has been formally designated as a strategic metal under China's New Energy Vehicle Industrial Development Plan, and the recently adopted 15th Five-Year Plan embeds PGMs across a remarkably broad range of national priorities.

The five-year plan explicitly identifies platinum's role in accelerating:

- AI infrastructure buildout and semiconductor manufacturing

- New energy systems, including hydrogen production and fuel cell vehicles

- Environmental protection through advanced catalysis

- Carbon reduction programmes across heavy industry

This policy architecture matters because it transforms platinum demand from a market-discretionary variable into something closer to a mandated input. Unlike Western markets where end-use demand responds to economic cycles, China's platinum consumption in these sectors is increasingly tied to national targets. Furthermore, understanding the broader platinum and palladium market dynamics helps contextualise why China's strategic reclassification carries such significant global implications.

The WPIC's Asia Pacific regional head, Weibin Deng, has noted publicly that China's PGMs market is entering a new development phase where traditional consumption drivers are being augmented by structurally new growth areas across investment, futures markets, artificial intelligence, and hydrogen, with Shanghai Platinum Week serving as the primary forum for understanding these shifts.

Platinum Demand in China: A Sector-by-Sector Analysis

China now accounts for approximately 30% of total worldwide platinum consumption, making it the single largest national market globally. Crucially, that share is built on an increasingly diversified demand base that reduces the vulnerability of any single sector downturn.

Demand Sector Overview (2024–2025)

| Demand Sector | 2025 Estimate | Key Growth Driver | Forward Outlook |

|---|---|---|---|

| Jewellery Fabrication | 474,000 oz (+15% YoY) | Platinum's price discount to gold | Continued recovery as gold premium widens |

| Bar and Coin Investment | ~404,000 oz | Investable product expansion since 2018 | Structural growth phase underway |

| Automotive Catalysis | Tightening regulatory horizon | Stricter emissions standards pending | Positive catalyst approaching |

| Hydrogen and Fuel Cells | Rapid scale-up phase | 15th Five-Year Plan FCEV targets | High-growth, long-duration trajectory |

| AI and Semiconductor Infrastructure | Emerging category | Data centre energy and materials needs | Early-stage but accelerating |

Jewellery: A Price-Arbitrage Recovery, Not a Fashion Cycle

Chinese platinum jewellery fabrication has been revised upward to 474,000 oz in 2025, representing 15% year-on-year growth. The mechanism driving this recovery is not a shift in aesthetic preferences but a straightforward price arbitrage: as gold trades at a significant premium to platinum, cost-conscious Chinese consumers are gravitating toward platinum as a more accessible luxury alternative.

This is a dynamic that is frequently mischaracterised in Western market commentary. The price-spread mechanism is more analytically reliable and more measurable. Jewellery partners reported early-stage physical restocking in Q1 2025 data, suggesting the fabrication recovery had genuine downstream support rather than being an inventory-building artefact.

Investment Demand: The Most Dramatic Transformation in Any PGM Sub-Market

Perhaps the most structurally significant development in Chinese platinum markets over the past decade has received comparatively little attention in Western financial media. China's platinum bar and coin market grew from near-zero levels in 2018 to an estimated 404,000 oz in 2025, positioning China as the world's largest platinum bar and coin market, accounting for approximately 64% of total global bar-and-coin demand.

April 2025 platinum import data reached a 12-month high, functioning as a leading indicator of sustained physical accumulation behaviour rather than speculative positioning. The growth of retail investment channels, product diversification, and growing Chinese investor appetite for hard assets with industrial utility credentials have all contributed to this trajectory.

Hydrogen and Fuel Cells: The Long-Duration Demand Story

China is executing the most ambitious national hydrogen scale-up programme on the planet, and PEM technology expansion sits at the intersection of that programme and platinum demand. PEM electrolysers and fuel cell electric vehicles (FCEVs) both require platinum-group catalysts in quantities that scale with deployment volume.

It is worth clarifying the technical mechanism for readers less familiar with PEM systems:

- PEM electrolysers use platinum and iridium as catalysts to split water molecules into hydrogen and oxygen using electrical current

- PEM fuel cells use platinum catalysts on both the anode and cathode to convert hydrogen back into electricity with water as the only byproduct

- These catalysts cannot currently be replaced by cheaper materials without significant efficiency losses, meaning platinum intensity per unit of hydrogen produced or consumed remains high

China's 15th Five-Year Plan includes specific FCEV deployment targets that represent a structural demand commitment. The international validation of this technology pathway is accumulating rapidly. Hyundai Motor Group has outlined a comprehensive hydrogen system for Europe encompassing production, infrastructure, fuel cells, and zero-emission vehicles. In Nova Scotia, Bosch Hybrion is delivering a 1.25 MW PEM electrolyser system integrated with Hygreen Energy's balance-of-plant infrastructure, targeting heavy-duty truck refuelling and industrial applications, with commissioning planned for 2027.

The global distribution of these projects confirms that PEM-grade platinum demand is not a China-specific thesis. It is a geographically distributed, multi-jurisdiction demand base that is scaling simultaneously across three continents.

AI Infrastructure: The Demand Vector That Did Not Exist in Prior Forecasting Models

Perhaps the most speculative but increasingly substantiated dimension of platinum's demand evolution is its intersection with artificial intelligence infrastructure. Platinum's distinctive combination of catalytic stability, thermal conductivity, corrosion resistance, and electrical properties makes it functionally relevant across several AI hardware categories:

- Semiconductor fabrication processes requiring platinum-group catalysts

- Optical interconnects in high-bandwidth data transmission systems

- Printed circuit boards where platinum-group materials improve reliability under thermal stress

- Advanced sensors embedded in autonomous and robotics applications

- Data storage media requiring high-stability materials

- Energy systems for power-intensive data centre operations

What makes this demand category structurally different from historical platinum end-uses is that AI infrastructure growth in China is policy-mandated. Unlike market-driven demand that fluctuates with economic conditions, AI infrastructure spending in China is tied to national competitiveness objectives. This creates a compounding effect: rising physical volumes meet policy-backed procurement, generating a demand floor that is relatively inelastic to short-term price changes.

The Guangzhou Futures Exchange and the Eastward Migration of PGM Price Discovery

The launch of platinum and palladium futures on the Guangzhou Futures Exchange (GFEX) in late 2025 represents one of the most consequential structural developments in PGM markets in decades. Prior to GFEX, Chinese end-users of platinum and palladium had no domestic mechanism through which to hedge their price exposure. All price risk management required accessing London or New York markets, creating currency risk, operational complexity, and dependence on Western market infrastructure.

GFEX changes this dynamic in three distinct ways:

- Domestic hedging capability: Chinese industrial users can now manage PGM price risk without accessing foreign exchanges, reducing friction and transaction costs

- Independent price discovery: A new pricing node operating in Chinese market hours creates reference prices that reflect Chinese supply-demand conditions rather than Western sentiment

- Arbitrage channel creation: Price differentials between GFEX and international benchmarks create arbitrage opportunities that will gradually align global pricing more closely with Chinese physical market conditions

GFEX's planned expansion to accommodate international participation will deepen liquidity and extend this influence further. Complementing the exchange is the recent launch of a precious metals clearing system in Hong Kong, which provides the regional settlement infrastructure to support growing cross-border PGM flows within the Greater China financial ecosystem.

Global PGM Financial Market Infrastructure Comparison

| Exchange / Platform | Location | Primary Function | Key Significance |

|---|---|---|---|

| London Platinum and Palladium Market (LPPM) | London, UK | Global OTC benchmark pricing | Historical pricing authority |

| NYMEX (CME Group) | New York, USA | Futures and hedging | Western financial market access |

| Guangzhou Futures Exchange (GFEX) | Guangzhou, China | Domestic PGM futures | Chinese price discovery and hedging |

| Hong Kong Precious Metals Clearing | Hong Kong | Regional settlement | Greater China market infrastructure |

Regulatory Crosscurrents: VAT Reform, Emissions Standards, and Supply Chain Realignment

Two regulatory developments deserve particular attention for investors and market participants assessing platinum demand in China over the near to medium term.

China's 2024 VAT changes affecting platinum sales have introduced asymmetric consequences across different market segments. The reforms are expected to carry long-term positive implications for PGM recycling economics and refining volumes. However, there is a near-term consideration for jewellery fabrication and physical investment demand, where the changed VAT treatment may create temporary headwinds as supply chain participants recalibrate their inventory and procurement strategies.

The second regulatory development concerns vehicle emissions standards tightening in China. The timing of this regulatory shift matters considerably for automotive PGM demand, since stricter emissions requirements increase the platinum and palladium loading per catalytic converter. Critically, even as battery electric vehicle (BEV) adoption accelerates, hybrid powertrains and FCEVs continue to require PGM-based emissions control systems. The net effect on automotive platinum demand depends more on the pace of emissions standard implementation than on EV adoption rates alone.

The next major ASX story will hit our subscribers first

South Africa's Supply Position: The Other Side of the Equation

Any comprehensive analysis of Shanghai Platinum Week and platinum demand in China must acknowledge the supply-side counterpart to China's demand dominance. South Africa hosts the overwhelming majority of global PGM resources, and the health of the supply relationship between South African producers and Chinese end-markets is a critical variable in global PGM pricing dynamics.

South Africa recorded a 120.3% increase in PGM sales over the three months to April 30, 2026, a supply-side signal that strongly corroborates the demand accumulation patterns visible on the Chinese import side. This scale of increase suggests that South African producers were responding to real offtake demand rather than building speculative inventory positions. Furthermore, the broader role of critical minerals demand in shaping these supply relationships cannot be understated.

China Platinum Market: Key Statistics at a Glance (2024–2026)

| Metric | Data Point | Context |

|---|---|---|

| China's share of global platinum demand | ~30% | Largest single national market globally |

| Platinum bar and coin demand (2025 est.) | ~404,000 oz | Up from near-zero in 2018 |

| China's share of global bar and coin demand | ~64% | Dominant investment market globally |

| Jewellery fabrication growth (2025 est.) | +15% YoY, 474,000 oz | Driven by gold-platinum price spread |

| April 2025 platinum imports | 12-month high | Physical accumulation signal |

| South Africa PGM sales increase (Q1 2026) | +120.3% YoY | Supply-side confirmation of strong offtake |

| GFEX futures launch | Late 2025 | First domestic Chinese PGM futures market |

Three Structural Themes That Will Define Platinum Markets Beyond 2026

Theme 1: Demand Diversification Reduces Structural Vulnerability

Platinum's historical dependence on jewellery fabrication as its primary demand driver made the metal unusually sensitive to shifts in consumer discretionary spending and gold price relativities. The progressive buildout of investment, hydrogen, AI, and automotive demand creates a multi-sector architecture. In addition, the role of energy transition minerals across these sectors further reinforces the case for structural demand resilience beyond any single category's performance.

Theme 2: Chinese Control Over PGM Price Discovery Is Increasing

The combination of GFEX futures infrastructure, Hong Kong clearing capabilities, and dominant physical demand positions China as a progressively more influential force in PGM price formation. For South African producers and Western financial market participants, this represents a structural shift in pricing dynamics that will take years to fully manifest but is now clearly underway. Consequently, China's commodity market evolution provides a useful lens through which to understand the pace and direction of this transition.

Theme 3: Policy-Mandated Demand Creates a More Durable Demand Floor

Unlike Western PGM demand, which is largely market-driven and therefore cyclically sensitive, an increasing share of Chinese platinum consumption is tied to policy mandates across hydrogen deployment, AI infrastructure, and emissions compliance. This structural difference means that Shanghai Platinum Week and platinum demand in China are likely to exhibit lower cyclicality than historical patterns would suggest, providing a more predictable base case for long-term supply planning and investment decisions.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instrument. Data points, forecasts, and estimates referenced throughout reflect publicly available market intelligence and should be verified independently. Forward-looking statements involve inherent uncertainty, and actual outcomes may differ materially from projections. Readers should conduct their own due diligence before making any investment decisions.

Readers seeking additional context on platinum group metals market dynamics and China's evolving role in global commodity markets may find value in exploring industry publications and educational resources available through the World Platinum Investment Council (WPIC), as well as platinum market coverage published by Shanghai Platinum Week's official programme at shanghaiplatinumweek.com.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex data across 30-plus commodities to surface actionable opportunities the moment they are announced. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.