July 10, 2026

The Quiet Metal Making the Loudest Statement in Chinese Retail Investment

Precious metals markets have always moved in cycles shaped by industrial necessity, monetary anxiety, and shifting cultural attitudes toward wealth preservation. Gold dominated the twentieth century. Silver has ebbed and flowed with industrial demand. But platinum, for much of its modern history, has been caught between two identities: a critical industrial catalyst and an aspirational luxury metal. Understanding the full precious metals market context helps explain why platinum never quite anchored itself in the retail investment consciousness the way gold has.

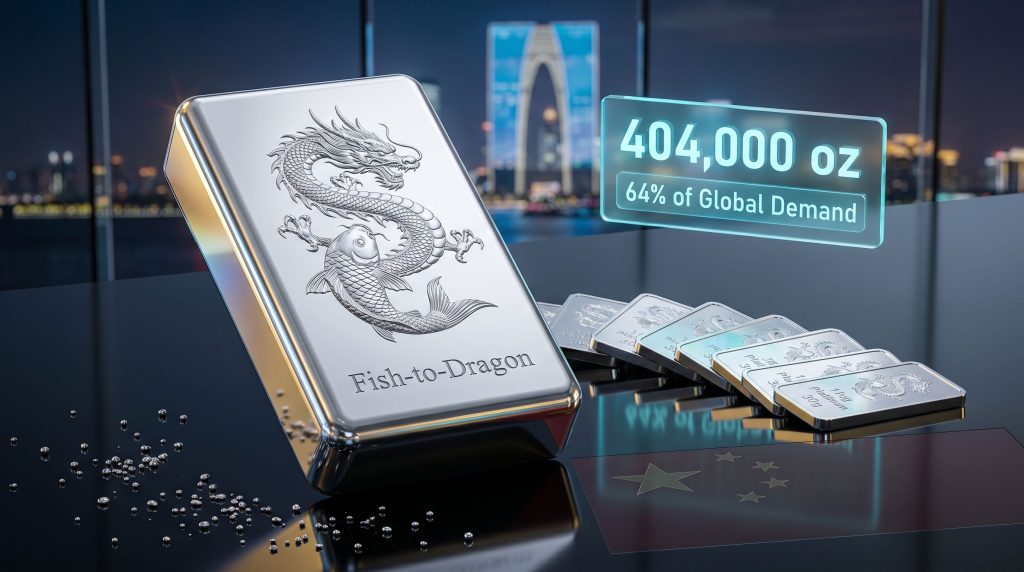

That identity ambiguity is dissolving with remarkable speed in China. What was effectively a negligible market for platinum bars and coins in 2018 has transformed into an estimated 404,000 oz of annual demand by 2025. This trajectory has repositioned China as the dominant force in global physical platinum investment. Understanding how this happened, and what Shanghai Platinum Week platinum investment bars revealed about where things go next, requires looking beyond headlines and into the structural mechanics of how Chinese consumers think about metal as money.

When big ASX news breaks, our subscribers know first

China's Platinum Bar Market: From Negligible to Dominant in Seven Years

The speed of China's entry into physical platinum investment is, by any historical standard, extraordinary. By 2024, China accounted for approximately 64% of global platinum bar and coin demand, including bars weighing 500 grams or more. No other country has achieved this kind of market concentration in a major precious metal investment category within a single decade.

Several forces converged to produce this outcome:

- Platinum's price positioning relative to gold created a perceived value opportunity for cost-conscious Chinese investors seeking precious metal exposure without gold's premium price point.

- Cultural familiarity with physical metal as a store of value meant that platinum bars required minimal behavioural change from consumers already active in gold and silver markets.

- The rise of larger-format bars (500g and above) attracted high-net-worth investors seeking lower fabrication premiums per ounce, improving the economics of platinum versus alternative precious metals.

- Growing awareness of platinum's dual industrial and monetary role made it increasingly compelling as a portfolio diversifier with real-world demand underpinning.

The shift from near-zero volumes in 2018 to 404,000 oz by 2025 is not simply a demand story. It is evidence of a structural reclassification of platinum within China's investment culture, from niche industrial metal to recognised retail asset class.

What makes this trajectory particularly significant is that it has occurred largely independent of the automotive catalysis narrative that dominates Western platinum commentary. Chinese retail investors have been drawn to platinum on its own investment merits, not primarily as a proxy for emission control policy. Furthermore, this organic adoption suggests the demand base is more structurally durable than sentiment-driven purchasing.

Shanghai Platinum Week 2026: What Happened and Why It Matters

Held from 6 to 10 July 2026 in Suzhou, China, the annual Shanghai Platinum Week, organised by the World Platinum Investment Council (WPIC), brought together industry leaders from across the global platinum group metals value chain. Suzhou, as a major commercial and cultural hub adjacent to Shanghai's financial ecosystem, provided a fitting backdrop for an event increasingly focused on China's role as a demand engine for the global PGM sector. According to Mining Weekly, China's strategic interest in platinum has been sharpening considerably in recent years.

Two product launches defined the investment narrative of the week.

The Caibai Partnership: Legacy Retail Meets a New Asset Class

Beijing's Caibai, a bullion retailer with 50 years of institutional history, formalised a strategic partnership with the WPIC, marking the first time the company has added a platinum investment bar series to its product range. The immediate result was the launch of a series of seven 30g platinum investment bars, now available to Caibai's established customer base.

This is not simply a product launch. It represents a deliberate distribution strategy by the WPIC to embed platinum within China's most trusted retail precious metals infrastructure, rather than building new channels from scratch. Caibai's half-century of credibility in gold bullion gives platinum immediate legitimacy in the eyes of consumers who might otherwise approach a new metal category with hesitation.

WPIC's Asia Pacific Regional Head Weibin Deng articulated the logic clearly: Caibai's strong reputation and high customer footfall provide a platform capable of introducing platinum investment to a substantially broader segment of Chinese retail investors than could be reached through newer or less established distribution partners.

The 30g format is also strategically deliberate. While larger bars offer lower fabrication premiums, the 30g size sits at an accessible price point that reduces the capital commitment required for a first-time platinum investor, consequently lowering the barrier to trial and adoption.

The China Gold Coin Group's Fish-to-Dragon 1kg Platinum Bar

The second landmark product debut came from China Gold Coin Group (CGCG), whose Fish-to-Dragon 1kg platinum bar (99.95% purity) made its market debut at the event. Exclusively distributed by Shenzhen China Gold Coin Distribution Co. Ltd (SCGCD), the bar features a design by Professor Chen Nan of Tsinghua University's Academy of Arts and Design.

| Feature | Details |

|---|---|

| Bar Name | Fish-to-Dragon (Fish Transforming into a Dragon) |

| Issuer | China Gold Coin Group (CGCG) |

| Purity | 99.95% platinum |

| Weight | 1 kilogram |

| Designer | Professor Chen Nan, Tsinghua University Academy of Arts and Design |

| Exclusive Distributor | Shenzhen China Gold Coin Distribution Co. Ltd (SCGCD) |

The cultural symbolism embedded in the bar's design is not incidental. The fish-to-dragon transformation is a classical Chinese metaphor for achievement and transformation, making it a natural fit for gift-giving, milestone celebrations, and long-term wealth preservation purchases. This positions the bar not merely as a commodity investment but as a collectible asset, a distinction that matters enormously in the Chinese luxury goods and gifting market.

Why Caibai's Dual Role Is a Distribution Advantage, Not Just a Detail

One of the less widely understood dynamics in Asian precious metals markets is the structural overlap between jewellery retail and investment bullion distribution. In China, high-purity jewellery has long functioned as a quasi-investment product, with pricing tied closely to underlying metal content and resale expectations embedded in the original purchase decision.

This creates a behavioural environment where consumers are already accustomed to treating physical metal as a store of value, even when purchasing it in decorative form. The transition from buying high-purity gold jewellery to purchasing a platinum investment bar requires relatively little cognitive or behavioural shift for a Caibai customer. In addition, for those already interested in physical metals investing, this distribution model provides a familiar and accessible entry point.

Three structural advantages make Caibai an unusually powerful distribution partner for platinum:

- Trust capital built over five decades reduces the scepticism that typically accompanies a new investment product category.

- Existing customer relationships across wealth segments mean platinum investment bars reach investors who are already engaged with precious metals, minimising education costs.

- The quasi-investment function of jewellery in Chinese retail culture creates a natural stepping stone from decorative metal purchases to formalised investment bar ownership.

The Guangzhou Futures Exchange and the Infrastructure of Price Discovery

Physical investment demand tells only part of the platinum story in China. The development of pricing and hedging infrastructure is equally important for establishing platinum as a mature investment market. Indeed, global precious metals pricing mechanisms are evolving rapidly as new exchanges gain prominence.

The Guangzhou Futures Exchange launched its platinum and palladium futures and options contracts following the previous year's Shanghai Platinum Week. The early performance indicators have been encouraging: platinum open interest has averaged approximately 620,000 oz, while average daily trading volumes have reached approximately 186,000 oz, signalling genuine market liquidity rather than speculative froth.

The GFEX figures matter because liquidity is the prerequisite for institutional participation. Without credible daily trading volumes, sophisticated investors cannot efficiently enter or exit platinum positions, limiting the market to retail participants only.

The most consequential potential development for the GFEX's role in global platinum pricing is the possible granting of Qualified Foreign Investor (QFI) status. If approved, QFI designation would allow international investors to participate directly in GFEX contracts, enabling natural arbitrage flows between GFEX and major global exchanges including the London Platinum and Palladium Market (LPPM) and the NYMEX.

This matters for global platinum price formation. A China-based futures exchange with meaningful international participation would add a third major pricing node to the global platinum market, potentially shifting how price discovery occurs and giving Chinese demand fundamentals more direct influence over international platinum valuations.

Disclaimer: QFI approval has not been confirmed at the time of writing. The implications described above are contingent on regulatory outcomes that remain uncertain.

Industrial Demand Channels That Rarely Make the Headlines

Beyond investment bars and futures markets, Shanghai Platinum Week 2026 highlighted several industrial PGM demand drivers that receive comparatively little attention in mainstream precious metals commentary.

AI Infrastructure and Optical Crystal Production

The global buildout of artificial intelligence data centres is generating demand growth through an indirect but meaningful channel: printed circuit board manufacturing. PCBs are embedded throughout AI server infrastructure, and their production consumes platinum group metals at scale.

Less widely appreciated is the platinum and iridium intensity of optical crystal production, where crucibles used in the crystal growth process require significant quantities of both metals. As AI-related photonics demand expands, this represents a structurally new and growing consumption channel for PGMs that is fundamentally different from the automotive catalysis demand that has historically dominated supply planning.

Fibreglass Production and PGM Bushing Demand

China's fibreglass sector has undergone substantial capacity expansion over recent years, with measurable implications for PGM consumption:

| Metric | 2021 | 2025 | Change |

|---|---|---|---|

| China fibreglass production | 5.8 million tonnes | 8.13 million tonnes | +40% |

| China fibreglass exports | ~0.975 million tonnes | 1.95 million tonnes | +100% |

PGM bushings are integral to fibreglass manufacturing, acting as the forming tools through which molten glass is drawn into continuous filaments. A 40% increase in domestic production volume, combined with a doubling of export volumes, translates directly into expanded bushing capacity requirements.

The emerging demand for low dielectric constant/low-loss yarn, used in high-frequency electronics and telecommunications infrastructure, adds a further dimension to this demand picture. Expanding production capacity for this specialised material requires additional PGM bushing investment, creating a capital expenditure cycle with embedded PGM consumption.

The next major ASX story will hit our subscribers first

Comparing Platinum Bar Formats: A Practical Framework for Investors

For investors considering entry into China's platinum bar market, the choice of bar format involves genuine economic and practical trade-offs. The broader platinum and palladium outlook also influences which format may suit different investor profiles.

| Bar Format | Target Investor | Key Advantage | Key Consideration |

|---|---|---|---|

| 30g retail bars (e.g., Caibai series) | Mass market/first-time investors | Low capital commitment, high accessibility | Higher fabrication premium per oz |

| 500g to 1kg bars (e.g., CGCG Fish-to-Dragon) | High-net-worth individuals | Lower fabrication premium, collectible value | Larger capital required |

| Institutional-grade bars | Funds and institutional investors | Maximum cost efficiency | Limited retail accessibility |

Several considerations are worth weighing carefully:

- Fabrication premiums are inversely related to bar size. Smaller bars cost more per ounce to produce, and this cost is typically passed to the buyer through a higher premium over spot price.

- Liquidity differs significantly between formats. Retail-sized bars are easier to sell in smaller transactions but may attract wider bid-ask spreads at resale.

- Storage and insurance costs scale with metal value, not bar count, making larger bars proportionally more cost-efficient to hold over time.

- Platinum's current price positioning relative to both gold and palladium may represent a historically interesting entry point, though this assessment carries inherent uncertainty and should not be construed as financial advice.

The WPIC's Retail Expansion Strategy and What It Signals

The Caibai partnership is consistent with a broader WPIC approach of working through established retail institutions rather than investing in new distribution infrastructure. This strategy has several advantages: it leverages existing consumer trust, avoids the time and capital cost of brand building, and allows platinum investment products to reach consumers who are already transacting in precious metals. Central bank metals demand patterns suggest institutional confidence in precious metals more broadly, providing a supportive macro backdrop for this retail expansion.

If Chinese retail demand for platinum continues on its current trajectory, the implications for global supply and demand balances are significant. A market that grew from near-zero to 404,000 oz in seven years, with new distribution channels being added and pricing infrastructure maturing, has the structural conditions in place to continue expanding. Investing News Network's coverage has highlighted how China's role in setting platinum's global demand narrative is only strengthening.

Shanghai Platinum Week platinum investment bars mark a qualitative transition: platinum is no longer working to establish itself in China's investment landscape. It is consolidating a position it has already earned, and building the institutional and retail architecture needed to sustain long-term, broad-based demand growth.

For global investors monitoring PGM fundamentals, China's platinum bar market is no longer a speculative future scenario. It is a measurable, growing, and increasingly sophisticated market reality, one whose scale and trajectory deserve serious attention in any forward-looking analysis of platinum supply and demand.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts and projections referenced herein involve inherent uncertainty. Readers should conduct their own due diligence before making investment decisions.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex data across more than 30 commodities into clear, actionable insights for both short-term traders and long-term investors — explore historic discoveries and their exceptional returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.