July 10, 2026

Understanding Platinum's Unique Market Position

The precious metals sector operates through complex supply-demand dynamics that vary dramatically across different metals, with the platinum price rally occupying a distinctly specialised position that sets it apart from traditional monetary metals like gold and silver. Unlike these purely investment-focused commodities, platinum functions simultaneously as an industrial necessity, a strategic material, and an alternative store of value, creating multifaceted pricing pressures that respond to diverse economic and geopolitical forces.

Industrial applications dominate platinum consumption patterns, with automotive catalysts representing approximately 38-40% of annual demand according to World Platinum Investment Council data. This automotive dependency creates unique vulnerability to transportation sector transitions, particularly the ongoing shift toward electric vehicles. However, platinum's role extends far beyond automotive applications, encompassing critical functions in chemical processing, petroleum refining, electronics manufacturing, and medical device production that provide demand stability independent of transportation trends.

The geographic concentration of platinum supply presents significant structural constraints that amplify price volatility during periods of disruption. South Africa accounts for approximately 71% of global production through major operations including Anglo American Platinum, Impala Platinum Holdings, and Sibanye-Stillwater facilities concentrated in the Bushveld Complex. This geographic concentration, combined with operational challenges including power supply constraints and labour relations issues, creates supply vulnerabilities that support elevated pricing during periods of market stress.

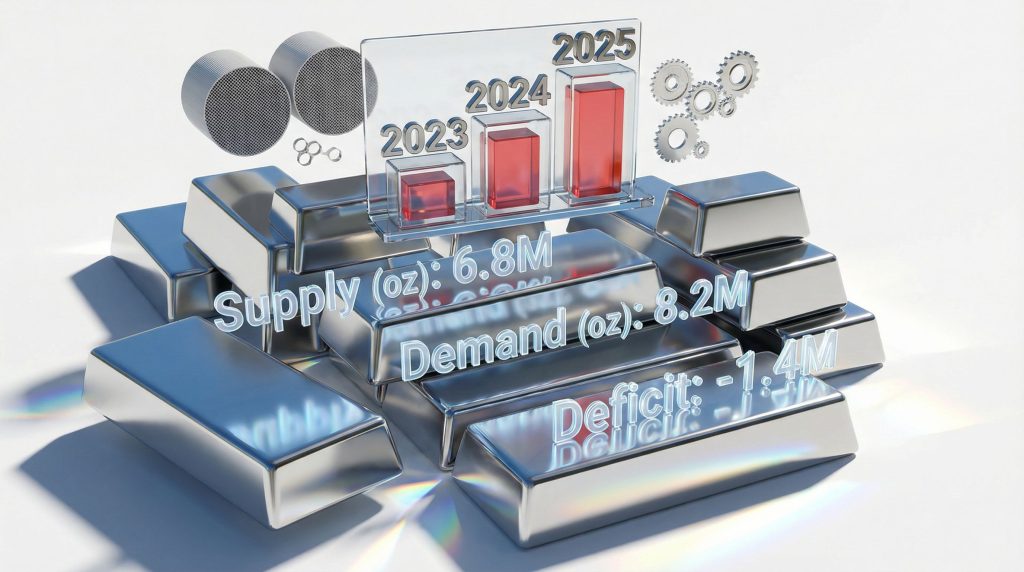

Key Supply-Demand Metrics for Platinum (2023-2025)

| Year | Mine Supply | Total Demand | Annual Balance | Price Impact |

|---|---|---|---|---|

| 2023 | 7.2M oz | 7.8M oz | -600K deficit | Moderate support |

| 2024 | 7.1M oz | 7.9M oz | -800K deficit | Significant strength |

| 2025 | 6.8M oz | 8.2M oz | -1.4M deficit | Extreme rally |

Physical inventory constraints distinguish platinum from gold's abundant above-ground stockpiles. While gold maintains approximately 200,000 metric tons of refined inventory representing roughly 60 years of annual production, platinum's above-ground stocks total only 5-7 million ounces according to industry estimates. This inventory scarcity amplifies the impact of supply disruptions and creates mathematical support for sustained price premiums during deficit periods.

When big ASX news breaks, our subscribers know first

Economic Forces Driving Investment Demand

The platinum price rally of 2025 reflects a convergence of macroeconomic pressures that extend beyond traditional commodity cycles, incorporating geopolitical tensions, currency debasement concerns, and strategic resource positioning into precious metals allocation decisions. Fund positioning reached $7.4 billion in bets supporting the rally according to December 2025 market data, representing approximately 13% of the metal's total above-ground value and indicating concentrated institutional conviction in sustained price strength.

Furthermore, critical minerals energy security designation by the U.S. Department of Interior in 2024 fundamentally altered platinum's strategic importance, elevating it to essential material status for national defence and technology applications. This designation triggered defensive stock-building among government agencies and defence contractors, creating structural demand that operates independently of traditional market cycles. The implications extend beyond direct government purchases to encompass supply chain localisation initiatives and strategic reserve accumulation across aerospace, electronics, and hydrogen fuel cell sectors.

Chinese market participation has intensified dramatically following the November 2025 launch of platinum and palladium futures contracts on the Guangzhou Futures Exchange. These contracts represent the first domestic price-hedging mechanism for platinum group metals in the world's largest consuming economy, fundamentally altering price discovery mechanisms that were previously dominated by London over-the-counter trading and New York COMEX futures. Chinese platinum imports reached 2.1 million ounces through the first three quarters of 2025, compared to 1.8 million ounces in the comparable 2024 period, representing a 16.7% increase despite stable automotive production levels.

The integration of Chinese domestic futures trading eliminated structural advantages previously enjoyed by Western financial intermediaries and created direct price linkages between Chinese spot demand and globally accessible futures pricing.

Currency debasement narratives have gained traction among institutional investors as global central bank balance sheets remained elevated at approximately $42-45 trillion across major developed and emerging market central banks through Q3 2025, according to Bank for International Settlements data. Within this monetary expansion context, platinum's industrial utility distinguishes it from pure monetary metals, resonating with investors seeking real asset exposure that combines inflation-hedge characteristics with genuine productive demand.

Investment Flow Analysis

• Exchange-traded fund inflows accelerated to 340,000 ounces during December 2025 alone

• Total precious metals ETF inflows reached $18.3 billion in 2025 versus $7.2 billion in 2024

• Lease rates spiked above 350 basis points annually, indicating physical market tightness

• Speculative positioning concentrated among sophisticated institutional investors rather than retail participants

Automotive Policy Shifts Reshaping Demand Trajectories

The European Union's December 2025 policy reversal regarding combustion engine phase-out timelines created immediate structural support for platinum group metals demand, extending the operational lifecycle of internal combustion engines indefinitely whilst simultaneously requiring progressively stricter emission standards. This policy combination necessitates substantially higher platinum loadings per vehicle to achieve incremental reductions in nitrogen oxides and particulate matter emissions.

Modern three-way catalytic converters contain approximately 2-5 grams of platinum group metals per vehicle under current Euro 6 emission standards, with platinum typically comprising 50-60% of the total PGM loading. The EU's announced Euro 7 and subsequent standards would require increases to 4-8 grams per vehicle by 2030-2035 to meet tighter emission thresholds, representing a mathematical doubling of platinum consumption per vehicle despite potential volume declines from electric vehicle adoption.

In addition, the mining industry evolution has been influenced by these automotive policy changes, prompting companies to adapt their production strategies accordingly. Mitsubishi Corporation analysts characterised the EU policy shift as providing platinum group metals with extended utility in catalytic converter applications, noting that the extension carries no defined endpoint whilst requiring ongoing emission reductions. This combination creates sustained demand visibility that was previously threatened by the 2035 combustion engine ban, fundamentally altering long-term supply-demand projections for the platinum market.

Automotive Demand Scenario Modelling

Optimistic Scenario (35% probability)

• Gradual electric vehicle transition maintains catalyst demand through 2035

• Hybrid vehicle adoption supports platinum consumption during transition period

• Stricter emission standards offset volume declines with higher per-unit loadings

• Regional policy divergence creates sustained combustion engine markets globally

Base Case Scenario (45% probability)

• Steady demand decline offset by regulatory requirements for emission improvements

• Electric vehicle penetration accelerates in premium segments whilst mass-market transitions slower

• Developing markets maintain combustion engine preference due to infrastructure constraints

• Net platinum demand stabilises rather than declining precipitously

Pessimistic Scenario (20% probability)

• Accelerated electric vehicle adoption reduces catalyst needs by 40% within five years

• Battery technology breakthroughs eliminate range and cost barriers to EV adoption

• Government incentives accelerate combustion engine retirement across major markets

• Platinum demand concentrated in industrial applications with automotive providing minimal support

Technical Trading Dynamics and Market Structure

Physical platinum lease rates reaching multi-year highs exceeding 350 basis points annually signal acute market tightness beyond normal commodity cycle variations. Lease rates measure the cost to borrow physical metal for specific periods, with elevated rates indicating insufficient physical availability to meet both industrial demand and speculative hedging requirements. This creates mathematical incentives for above-ground inventory mobilisation and recycling supply increases.

The mechanics of lease rate arbitrage function through simultaneous transactions where entities holding platinum inventory can lend physical metal whilst selling forward in futures markets. When forward prices exceed spot prices by more than the lease rate differential, arbitrageurs profit by securing metal in the spot market and selling forward delivery obligations. During periods of extreme tightness, lease rates spike to levels making previously uneconomical recycling operations profitable.

Managed money positioning in COMEX platinum futures indicated substantial speculative long positions concentrated among institutional participants rather than retail investors. This positioning structure suggests sophisticated analysis supporting sustained price strength rather than momentum-chasing behaviour typical of retail speculation. The concentration among professional investors typically provides more stable support during temporary price corrections.

Exchange-traded fund mechanics create direct physical demand pressure independent of fundamental supply-demand considerations. Each new ETF share issuance to accommodate investor demand requires corresponding allocated, segregated platinum inventory meeting London Bullion Market Association standards. As platinum ETFs experienced significant inflows during December 2025, custodians must replace depleted inventory through spot market purchases or leasing arrangements, creating mechanical buying pressure.

Technical Market Indicators

| Indicator | Current Level | Historical Average | Market Signal |

|---|---|---|---|

| Lease Rates | 350+ bps | 120-150 bps | Extreme tightness |

| ETF Holdings | +340K oz/month | +50K oz/month | Strong investment demand |

| Backwardation | $15-25/oz | $3-8/oz | Physical shortage |

| Open Interest | Elevated | Normal | Speculative positioning |

Supply Response Potential and Market Sustainability

South African production expansion capabilities remain constrained by infrastructure limitations rather than geological factors, with power supply reliability representing the primary obstacle to increased output. Eskom's rolling blackouts exceeded 200 days during 2024, directly impacting mining operations across the Bushveld Complex where major platinum producers maintain concentrated operations. Load shedding interruptions create extended maintenance periods and reduce annual throughput regardless of underlying demand strength.

Recycling supply elasticity provides potential price moderation mechanisms as elevated platinum prices make previously uneconomical recovery operations viable. Current recycling recovery rates for platinum from autocatalysts range from 70-85% in developed markets with established collection infrastructure, compared to 40-50% in emerging markets. Historical patterns suggest recycling supply typically represents 15-20% of total supply during normal market conditions but can escalate to 25-30% during extreme price cycles.

Substitution economics create theoretical price ceilings where alternative materials become economically attractive, though practical switching costs in automotive production typically require 18-36 months of development, testing, and regulatory approval. With palladium trading at approximately $1,720 per troy ounce compared to platinum's current levels above $2,240, economic incentives for substitution development have intensified significantly.

Above-ground inventory mobilisation represents the most immediate supply response mechanism during price rallies. Unlike primary mining production, which requires substantial lead times and capital investment, existing stockpiles can respond rapidly to price signals. However, platinum's limited above-ground inventory relative to annual consumption constrains this response mechanism compared to gold's abundant inventory buffers.

Investment Positioning and Risk Management

Portfolio allocation strategies for platinum exposure must balance the metal's industrial utility against its emerging role as a geopolitical hedge and currency debasement protection. Unlike pure monetary metals, platinum's price performance remains partially tied to automotive and industrial demand cycles, creating both diversification benefits and correlation risks depending on broader economic conditions.

Mining equity exposure provides leveraged participation in platinum price movements whilst introducing company-specific operational and financial risks. Major platinum producers including Anglo American Platinum, Impala Platinum Holdings, and Sibanye-Stillwater offer varying degrees of platinum price exposure, geographic diversification, and operational efficiency profiles that affect their relative performance during commodity price cycles.

Major Platinum Producer Analysis

• Anglo American Platinum: Largest global producer with integrated refining operations and lowest-cost asset base

• Impala Platinum Holdings: Diversified operations across multiple mining complexes with substantial palladium co-production

• Sibanye-Stillwater: Geographic diversification including U.S. operations and gold mining providing broader precious metals exposure

• Northam Platinum: Smaller producer with development pipeline offering growth potential during elevated price environments

Physical metal versus futures exposure considerations involve storage costs, insurance requirements, and liquidity differences that affect total return calculations. Physical platinum ownership provides direct commodity exposure without counterparty risks but requires secure storage and insurance arrangements. Futures contracts offer greater liquidity and leverage potential whilst introducing rollover costs and counterparty credit risks.

Options strategies can provide risk management tools during periods of heightened volatility, allowing investors to participate in upside price movements whilst limiting downside exposure. Protective put options, covered call writing, and collar strategies offer various risk-reward profiles depending on investor objectives and market outlook.

The next major ASX story will hit our subscribers first

How Does Platinum Compare to Gold's Performance?

The structural deficit projected for platinum markets through 2025 and beyond creates mathematical constraints supporting elevated price levels independent of speculative positioning. With annual deficits escalating to 1.4 million ounces in 2025 according to supply-demand modelling, the market faces inventory drawdown that must eventually prompt either demand destruction or supply increases to restore equilibrium.

However, when examining gold market performance, platinum demonstrates distinctly different characteristics due to its industrial applications. While gold benefits from its monetary heritage and acts as a traditional safe haven, platinum's dual nature as both an industrial metal and precious metal creates more complex dynamics. Furthermore, the gold inflation hedge dynamics differ significantly from platinum's inflation protection characteristics.

Hydrogen economy development provides potential demand diversification beyond traditional automotive and industrial applications. Fuel cell technology requires platinum catalysts for hydrogen-to-electricity conversion, with infrastructure investments across transportation, stationary power generation, and industrial applications creating new consumption categories. Whilst currently representing a small percentage of total demand, hydrogen applications could provide meaningful demand support during the electric vehicle transition.

Geopolitical supply concentration risks appear likely to intensify rather than diminish, with South African political and economic stability representing ongoing concerns for sustained production growth. Russian supply disruptions related to sanctions and trade restrictions have already reduced available metal flows, whilst alternative supply sources remain limited by geological factors and development timelines.

What Are the Long-term Investment Implications?

The convergence of supply constraints, policy support for combustion engines, and strategic metal designation suggests platinum's elevated price environment may persist longer than previous cycles, creating sustained investment opportunities for those positioned appropriately for continued volatility.

Investment demand patterns indicate institutional recognition of platinum's evolving role within precious metals portfolios, moving beyond traditional automotive-industrial correlation toward broader macroeconomic hedge functions. This evolution supports price stability during temporary industrial demand fluctuations whilst creating upside potential during periods of monetary expansion and geopolitical tension.

The gold price surge analysis provides valuable context for understanding how precious metals markets respond to similar macroeconomic pressures. However, according to recent market analysis, platinum has demonstrated unique characteristics that distinguish it from both gold and silver performance patterns.

The platinum price rally represents a fundamental revaluation reflecting supply scarcity, policy support, and strategic importance rather than purely speculative momentum. Investors must evaluate their risk tolerance and investment horizon when considering exposure to a market characterised by structural deficits, geographic concentration, and evolving demand patterns that extend well beyond traditional commodity cycles.

Looking to Capitalise on Platinum's Historic Rally?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant platinum and precious metals discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Discover how major mineral discoveries have generated substantial returns by exploring Discovery Alert's dedicated discoveries page and begin your 30-day free trial today to position yourself ahead of the market.