August 9, 2026

What Does Political Transition Mean for Venezuela's Oil Production Capacity?

Maduro's capture impact on Venezuelan oil industry has created unprecedented opportunities for energy sector transformation, though significant infrastructure constraints and capital requirements will define the pace of recovery. Global energy markets face unprecedented disruption as political transformation in Venezuela creates new pathways for hydrocarbon sector recovery. The fundamental question extends beyond immediate political changes to encompass structural constraints that have plagued Venezuelan oil production for over a decade. Understanding this transformation requires analyzing current infrastructure limitations, capital requirements for restoration, and the complex interplay between political stability and operational capacity.

Current Production Baseline and Infrastructure Assessment

Venezuela's crude oil production currently operates at approximately 0.75-1.0 million barrels per day, representing a dramatic decline from historical peaks of 3-4 million barrels per day achieved during the pre-sanctions era. This reduction reflects more than political instability; it demonstrates the consequences of systematic underinvestment in critical infrastructure maintained by Petróleos de Venezuela (PDVSA).

The aging infrastructure presents immediate operational challenges requiring substantial capital injection for basic maintenance protocols. Years of deferred maintenance have resulted in severely reduced operational efficiency across PDVSA facilities, creating bottlenecks in extraction rates, processing capacity, and export capabilities. Current vessel loading operations illustrate both the potential and constraints facing Venezuelan oil recovery efforts.

Technical Infrastructure Constraints:

• Extraction rates limited by wellhead capacity and reservoir management systems

• Processing capacity constrained by crude stabilization and treatment facilities

• Transportation logistics hampered by deteriorated pipeline systems and storage facilities

• Export capabilities restricted by loading facility conditions and vessel infrastructure

Short-Term Recovery Scenarios (12-24 Months)

Multiple recovery pathways exist depending on the intensity of political reform and international investment attraction. Each scenario presents different operational intensities and capital deployment strategies, with corresponding production targets and financial requirements.

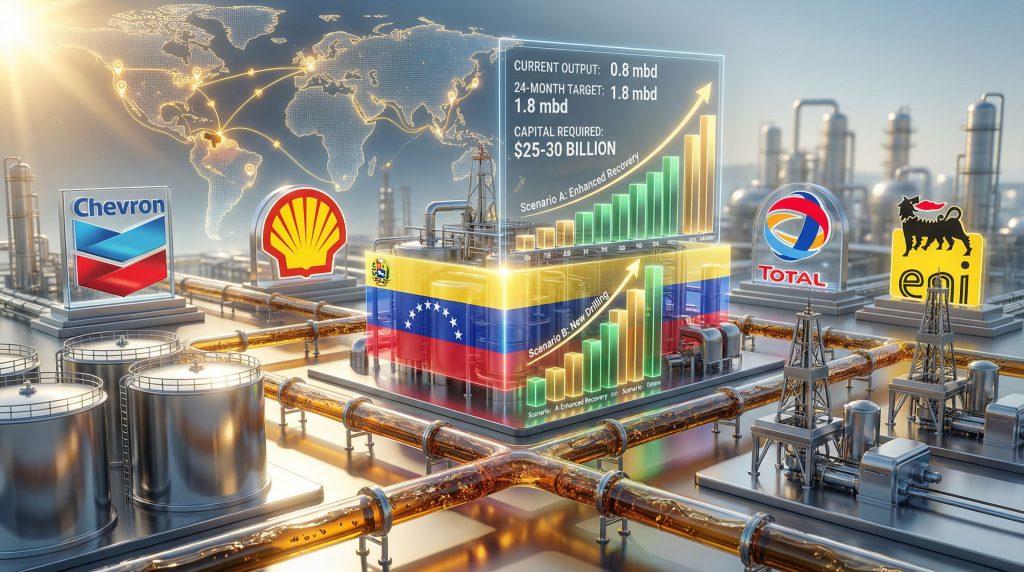

Production Recovery Timeline Under Different Political Scenarios

| Scenario | Current Output | 12-Month Target | 24-Month Target | Capital Required |

|---|---|---|---|---|

| Gradual Transition | 0.8 mbd | 1.1 mbd | 1.4 mbd | $8-12 billion |

| Rapid Reform | 0.8 mbd | 1.3 mbd | 1.6 mbd | $15-20 billion |

| Full Liberalization | 0.8 mbd | 1.5 mbd | 1.8 mbd | $25-30 billion |

The Gradual Transition pathway assumes measured infrastructure rehabilitation with conservative capital deployment, focusing on stabilizing existing production before expanding capacity. This approach prioritizes operational reliability over aggressive expansion, targeting incremental improvements in facility efficiency and basic maintenance restoration.

Furthermore, Rapid Reform scenarios suggest accelerated facility restoration with parallel institutional changes, requiring higher capital deployment but offering faster production recovery. This pathway demands simultaneous investment in infrastructure modernization and regulatory framework development to attract international operators.

Full Liberalization scenarios indicate comprehensive operational restructuring with maximum capital influx, representing the most ambitious recovery timeline but requiring extensive political stability and investor confidence to succeed. However, the OPEC production impact on global markets could significantly influence these recovery trajectories.

Long-Term Restoration Potential (5-10 Years)

Historical production capacity of 3-4 million barrels per day represents the theoretical ceiling for Venezuelan oil output, though achieving this level requires sustained capital investment exceeding $100 billion over the restoration period. Full capacity restoration demands comprehensive institutional reforms essential for attracting major international operators capable of deploying advanced extraction technologies and management systems.

The timeline for complete restoration extends beyond infrastructure rehabilitation to encompass regulatory framework development, contract dispute resolution, and establishment of transparent fiscal terms attractive to foreign direct investment. These institutional requirements often prove more challenging than technical infrastructure restoration, as they demand sustained political commitment across multiple electoral cycles.

Consequently, the Maduro's capture impact on Venezuelan oil industry will require coordinated efforts across political, economic, and technical domains to achieve successful restoration.

When big ASX news breaks, our subscribers know first

How Would Sanctions Relief Transform Global Oil Market Dynamics?

The reintegration of Venezuelan crude oil into global markets represents a structural shift affecting pricing architecture, refinery investment decisions, and upstream development strategies across competing regions. Understanding these dynamics requires examining immediate market response mechanisms, strategic supply chain rebalancing, and competitive pressure on regional producers operating in similar market segments.

Immediate Market Response Mechanisms

Venezuelan heavy crude grades, primarily Merey and Boscan blends, compete directly with Canadian oil sands bitumen and Mexican Maya crude in specialized refining markets. These heavy crude grades require advanced coking or hydrocracking units for processing, creating natural market segmentation that limits competitive substitution with light crude varieties.

Heavy Crude Quality Specifications:

• API Gravity: 8-12° (extra-heavy classification)

• Sulfur Content: 3.5-4.5% (high-sulfur crude requiring extensive processing)

• Viscosity at 60°F: 1,000-5,000 centipoise (requiring heating and dilution for transport)

Price differentials for heavy crude grades could narrow by $5-15 per barrel under sanctions relief scenarios, as increased Venezuelan supply competes with established Canadian and Mexican market share. US Gulf Coast refineries positioned to benefit from increased heavy crude availability include facilities operated by Chevron, Phillips 66, and Valero Energy, which possess the specialized processing capabilities required for Venezuelan crude grades.

Current loading operations demonstrate market reintegration potential, with vessel movement data indicating significant increases in Venezuelan crude exports during early 2026. These shipments primarily target US refineries equipped with advanced heavy crude processing capabilities, illustrating the immediate market response to sanctions relief measures. Moreover, ongoing oil price stagnation could create additional opportunities for Venezuelan crude market penetration.

Strategic Supply Chain Rebalancing

The return of Venezuelan crude represents one of the largest potential supply additions in the Western Hemisphere, fundamentally altering North American energy security calculations.

This market reintegration extends beyond simple supply additions to encompass strategic supply chain rebalancing affecting multiple market segments. North American energy market integration under expanded Venezuelan production creates new pricing dynamics and competitive pressures for established suppliers operating in heavy crude markets.

Refinery Processing Requirements for Venezuelan Heavy Crude:

• Advanced coking or hydrocracking units for complex molecular restructuring

• Hydrogen production capacity for desulfurization processes

• Delayed coking facilities or fluid catalytic cracking capability for yield optimization

• Specialized storage and handling equipment for high-viscosity crude management

Market price formation mechanisms for heavy crude differentials depend on transportation costs from production points to refineries, quality adjustment factors including sulfur content and gravity specifications, and refinery capacity utilization rates in competing markets including Canada, Mexico, and Middle Eastern suppliers. In addition, the broader oil price movements will significantly influence these market dynamics.

Competitive Pressure on Regional Producers

PEMEX faces intensified competition in heavy crude markets as Venezuelan production expands under international operator management. Mexico's Maya blend crude, with API gravity of 22° and sulfur content of 3.3%, competes directly with Venezuelan Merey crude in similar refinery configurations designed for heavy crude processing.

Increased Venezuelan supply typically compresses price differentials between competing heavy crude grades, reducing per-barrel revenue for existing suppliers while creating margin pressure on upstream development projects. This competitive dynamic affects investment attractiveness for marginal Canadian oil sands developments and Brazilian pre-salt projects competing for refinery capacity and long-term supply contracts.

Regional Heavy Crude Market Competition:

• Mexican Maya Blend: API 22°, 3.3% sulfur content serving Gulf Coast refineries

• Venezuelan Merey: API 16°, 3.5% sulfur content targeting similar processing facilities

• Canadian Bitumen: API 8-10°, requiring specialized upgrading and transportation infrastructure

Which International Oil Companies Stand to Benefit Most?

Market reentry opportunities following Venezuelan political transition create competitive advantages for companies with established operational presence, historical relationships, and specialized heavy oil expertise. Understanding these advantages requires examining current market positioning, licensing frameworks, and strategic capabilities necessary for successful Venezuelan operations.

Chevron's Strategic Advantage

Chevron operates in Venezuela under special authorization from the US government that exempts it from broader sanctions on the country's energy sector, providing significant first-mover advantages in expanded market access. Current oil market dynamics suggest that companies with established infrastructure will benefit most from rapid market changes. Current loading operations demonstrate this operational capability, with vessel movement data indicating 1.68 million barrels per day of Venezuelan crude oil loaded during the first week of January 2026.

This loading volume represents nearly five times the amount compared with late December 2025, marking the most intense export period since May 2025. For comparative context, this single-week loading capacity approaches Mexico's total 2025 crude oil production of approximately 1.7 million barrels per day, illustrating the scale of potential Venezuelan market reintegration.

Chevron's Operational Advantages:

• Established relationships with PDVSA technical personnel and operational protocols

• Existing infrastructure knowledge and logistics arrangements developed through historical operations

• Pre-positioned equipment and specialized heavy crude handling capabilities

• Regulatory relationships with US government agencies authorizing Venezuelan operations

Current negotiations with US government officials focus on expanding Chevron's operating license, potentially allowing increased crude exports and reopening access to buyers beyond US refineries. License expansion could restore export levels previously curtailed under tightened sanctions, which had reduced Chevron's Venezuelan exports from approximately 250,000 barrels per day to around 100,000 barrels per day in late 2025.

European Majors Positioning for Reentry

International oil companies evaluate Venezuelan opportunities based on historical experience, technical capabilities, and strategic positioning for heavy oil operations. Several European majors possess specific advantages for Venezuelan market reentry under expanded licensing frameworks.

Companies Evaluating Venezuelan Opportunities:

• Shell: Historical presence in the Orinoco Belt with experience in extra-heavy crude development

• Total Energies: Previous joint venture experience through the Petrozuata project operated until 2012

• Eni: Latin American expansion strategy focus with heavy oil technical expertise

• Equinor: Heavy oil expertise developed through North Sea and Brazilian operations

These companies bring specialized technical capabilities for heavy crude development, including enhanced oil recovery techniques, upgrading technologies, and complex project management systems required for Venezuelan oilfield restoration. Historical experience provides operational knowledge of Venezuelan geological conditions, regulatory frameworks, and infrastructure requirements necessary for successful project development.

Furthermore, the broader global market impact from recent policy changes could influence these companies' strategic decisions regarding Venezuelan investments.

Trading House Competition Dynamics

Global trading houses actively negotiate US-supervised export arrangements as Venezuelan crude reintegration creates opportunities in international crude distribution channels. Vitol and Trafigura represent major competitors for Venezuelan crude trading rights, bringing established global distribution networks and specialized heavy crude marketing capabilities.

This competition underscores how geopolitical shifts recalibrate global crude distribution channels beyond immediate regional impacts. Trading house participation requires coordination with US government oversight while managing inventory flows and storage capacity optimization across multiple markets.

Storage capacity management becomes critical operational factor as Venezuelan crude volumes increase, requiring coordination between production rates, export scheduling, and global storage availability. Trading houses must balance immediate arbitrage opportunities with long-term supply contract commitments to refineries capable of processing Venezuelan heavy crude grades.

What Investment Risks Must Energy Companies Navigate?

Venezuelan energy sector investment involves complex risk assessment frameworks encompassing political stability, regulatory continuity, and operational security considerations. Understanding these risks requires systematic evaluation of probability factors, impact assessments, and mitigation strategies applicable to different investment scenarios and timeframes.

Political Stability Assessment Framework

Risk Factors for Venezuelan Energy Investment

| Risk Category | Probability | Impact Level | Mitigation Strategy |

|---|---|---|---|

| Regulatory Reversal | Medium | High | Phased investment approach |

| Currency Volatility | High | Medium | USD-denominated contracts |

| Infrastructure Sabotage | Low | High | Enhanced security protocols |

| Contract Disputes | Medium | High | International arbitration clauses |

Regulatory Reversal Risk encompasses potential policy changes affecting foreign investment terms, fiscal frameworks, and operational permits. Medium probability reflects ongoing political uncertainty despite current leadership changes, while high impact rating acknowledges potential project delays or contract modifications that could significantly affect investment returns.

Currency Volatility Risk presents high probability due to Venezuela's historical monetary instability and ongoing economic restructuring requirements. Medium impact rating assumes USD-denominated contract structures that limit direct currency exposure while acknowledging indirect effects on local operational costs and workforce management.

Infrastructure Sabotage Risk receives low probability rating based on current security conditions but high impact rating recognizing potential operational disruptions and safety concerns. Enhanced security protocols including international coordination and technological monitoring systems provide mitigation approaches for this risk category.

Legal and Contractual Complexities

Resolution of past expropriation claims against PDVSA represents prerequisite for major international investment, as outstanding arbitration awards create legal uncertainties affecting contract enforceability and asset security. International arbitration awards must be addressed through comprehensive settlement frameworks before companies commit substantial capital to Venezuelan operations.

New fiscal terms likely favour foreign investors over historical arrangements, reflecting government incentives to attract international capital and technology transfer. However, contract negotiation complexity increases due to multiple stakeholder interests including US government oversight, Venezuelan institutional requirements, and international legal framework compliance.

Legal Risk Mitigation Approaches:

• International arbitration clauses providing dispute resolution outside Venezuelan jurisdiction

• Phased investment structures reducing exposure while maintaining development optionality

• Political risk insurance through multilateral institutions and specialised providers

• Joint venture partnerships spreading risk across multiple international operators

Capital Allocation Timing Strategies

First-mover advantages must be balanced against wait-and-see approaches that reduce exposure while potentially sacrificing optimal asset acquisition opportunities. Phased development strategies offer compromise solutions, allowing companies to establish market presence while limiting initial capital commitments until political and regulatory frameworks stabilise.

Strategic Investment Timing Considerations:

• Early Entry Benefits: Prime asset acquisition, favourable contract terms, market share establishment

• Delayed Entry Benefits: Reduced political risk, proven regulatory stability, clearer operational frameworks

• Phased Development: Gradual exposure increase, operational experience accumulation, optionality preservation

Joint venture structures provide risk distribution mechanisms while maintaining access to Venezuelan opportunities. International partnerships combine technical expertise, financial resources, and risk tolerance across multiple companies, creating more robust operational frameworks capable of managing complex political and operational environments.

Consequently, the Maduro's capture impact on Venezuelan oil industry requires sophisticated risk management approaches that balance opportunity capitalisation with prudent exposure management across multiple timeframes.

How Does This Impact Mexico's Energy Security Position?

Venezuelan oil sector transformation under international oversight creates strategic challenges for Mexico's energy security framework, affecting PEMEX's competitive positioning, regional market dynamics, and national energy sovereignty principles. Understanding these impacts requires analysing competitive pressures, market integration implications, and strategic response options available to Mexican energy policy makers.

PEMEX Competitive Challenges

Direct competition in heavy crude export markets presents immediate challenges for PEMEX's commercial strategy and revenue optimisation efforts. Mexican Maya crude blend faces intensified price competition from Venezuelan Merey crude as both grades target similar Gulf Coast refinery configurations equipped for heavy crude processing.

Crude Grade Competition Analysis:

• Maya Blend Specifications: API 22°, sulfur content 3.3%, established Gulf Coast market presence

• Venezuelan Merey: API 16°, sulfur content 3.5%, competing for similar refinery capacity

• Market Impact: Price differential compression reducing per-barrel revenue margins for PEMEX

Potential loss of pricing power for Maya crude blend affects PEMEX's financial performance and upstream investment capacity, as reduced export revenues limit available capital for exploration, development, and infrastructure maintenance. This competitive pressure compounds existing challenges facing PEMEX operations including production decline rates and maintenance requirements across aging oilfield infrastructure.

Reduced investment attractiveness for Mexican upstream projects results from margin compression and increased competition for international capital allocation. Energy companies evaluating North American investment opportunities may prioritise Venezuelan assets under international operator management over Mexican projects constrained by national energy policies limiting foreign participation.

Regional Energy Integration Implications

North American energy market integration under expanded Venezuelan production creates new competitive dynamics affecting Mexico's energy policy framework. Increased US regional control over Venezuelan resources alters bargaining power relationships and strategic autonomy considerations for Mexican energy security planning.

Mexico's energy sovereignty principles face testing through increased US regional control over critical hydrocarbon supplies. National energy policies emphasising state control and limited foreign participation may require adjustment to remain competitive in evolving North American energy markets characterised by greater integration and cross-border investment flows.

Energy Market Integration Factors:

• Refinery feedstock sourcing patterns shifting toward Venezuelan crude availability

• Pipeline capacity and transportation logistics favouring US-controlled supply chains

• Investment capital flows redirecting toward Venezuelan opportunities under international management

• Regional pricing mechanisms influenced by expanded US energy sector oversight

Moreover, the ongoing US–China trade war adds additional complexity to regional energy market dynamics, potentially affecting Mexico's strategic positioning.

Strategic Response Options for Mexico

Mexican energy strategy requires adaptation to address increased competitive pressures while maintaining energy sovereignty principles and national development objectives. Multiple policy alternatives exist for positioning Mexico's energy sector within evolving regional market dynamics.

Policy Alternatives for Mexican Energy Strategy:

• Accelerated PEMEX Modernisation Programmes: Infrastructure investment, technology upgrade, operational efficiency improvement

• Enhanced Focus on Natural Gas and Renewable Energy: Market diversification reducing crude oil export dependence

• Deeper Integration with Central American Energy Markets: Alternative market development beyond North American competition

• Strategic Partnerships with Non-US International Operators: Technology transfer and investment attraction within sovereignty constraints

Accelerated PEMEX modernisation programmes offer direct competitive response options, though implementation requires substantial capital investment and operational restructuring. Technology upgrade initiatives and efficiency improvement programmes could help maintain market competitiveness while preserving state control over strategic energy assets.

Enhanced focus on natural gas and renewable energy development provides market diversification strategies reducing crude oil export dependence and creating new revenue streams. Mexico's renewable energy potential and natural gas reserve development offer alternative pathways for energy sector growth not directly competing with Venezuelan crude oil expansion.

Deeper integration with Central American energy markets creates alternative demand centres for Mexican energy exports, reducing dependence on North American markets increasingly dominated by US energy security priorities. Regional energy cooperation frameworks could provide strategic autonomy while maintaining commercial viability.

What Are the Broader Geopolitical Implications?

The transformation of Venezuela's energy sector under international oversight represents more than commercial market adjustment; it demonstrates evolving principles of resource sovereignty, international law application, and hemispheric power dynamics. Understanding these implications requires examining US energy dominance strategy, Latin American sovereignty concerns, and international legal framework challenges created by direct resource control precedents.

US Energy Dominance Strategy

Venezuelan oil control aligns with explicit America First resource security doctrine prioritising direct access to strategic hydrocarbon reserves over multilateral consensus mechanisms. This approach reflects systematic strategy to reassert control over resources deemed essential for economic resilience, energy security, and geopolitical competition with strategic rivals including China and Russia.

Direct access to Venezuelan strategic hydrocarbon reserves reduces US import dependency while creating leverage in global energy markets. Recent market developments demonstrate the significance of this strategic positioning. Current arrangements provide up to 50 million barrels of Venezuelan oil supplies to US markets as part of initial agreements, with broader control over future sales extending beyond immediate supply requirements to encompass long-term strategic positioning.

Strategic Resource Control Elements:

• Direct oversight of production rates and export destination management

• Revenue stream control through US-supervised account management systems

• Technology transfer limitations preventing strategic competitor access to Venezuelan energy infrastructure

• Investment framework favouring US corporate interests and security priorities

Geopolitical competition with China over Latin American energy assets intensifies through Venezuelan control mechanisms that prevent alternative strategic partnerships. Previous Chinese investment in Venezuelan energy infrastructure becomes subordinated to US operational oversight, creating template for broader regional resource access management.

Latin American Sovereignty Concerns

The precedent of direct US control over another nation's oil resources raises fundamental questions about territorial sovereignty and international law in the Western Hemisphere.

Regional governments express concerns about territorial sovereignty implications and broader precedent-setting effects of direct resource control mechanisms. Several Latin American governments, including Mexico, have publicly opposed what they characterise as attempts to control crude oil resources belonging to sovereign nations, raising diplomatic tensions and institutional governance questions.

These sovereignty concerns extend beyond Venezuelan territorial issues to encompass potential template creation for future US interventions in resource-rich nations. Countries possessing strategic minerals, hydrocarbon reserves, or critical infrastructure may face increased pressure to accommodate US strategic interests under similar frameworks prioritising resource access over institutional norms.

Regional Sovereignty Impact Assessment:

• Precedent establishment for resource control mechanisms bypassing traditional diplomatic channels

• Bilateral relationship transformation from cooperative development to transactional access arrangements

• Institutional governance frameworks challenged by unilateral resource management decisions

• Investment climate uncertainty for projects involving strategic resource development

Regional policy analysis indicates this doctrine risks reinforcing asymmetrical power dynamics as countries rich in natural resources face increased pressure to accommodate US strategic interests. State-owned companies including PEMEX could find themselves competing not only in commercial markets but against geopolitical frameworks favouring US corporate and security priorities above regional energy sovereignty principles.

International Legal Framework Challenges

Principles of national resource sovereignty face unprecedented challenge through direct control mechanisms operating outside traditional international law frameworks. Legal scholars and diplomatic observers question whether current arrangements constitute unauthorised appropriation of sovereign nation natural resources, creating potential violations of international legal principles governing territorial sovereignty and resource ownership.

Multilateral institutions face pressure to address precedent-setting actions that could undermine established international law principles. The precedent of resource control without formal territorial annexation creates new categories of international governance requiring institutional response and legal framework development.

International Legal Considerations:

• United Nations Charter principles regarding territorial sovereignty and resource ownership rights

• International Court of Justice precedents governing resource extraction and revenue distribution

• Bilateral investment treaty implications for future resource development agreements

• Regional organisation responses to unilateral resource control mechanisms

These legal framework challenges extend beyond immediate Venezuelan context to encompass broader questions about international system governance and institutional authority. Future resource conflicts may reference Venezuelan precedents, creating systematic challenges for multilateral institutions designed to mediate territorial and commercial disputes through established legal frameworks.

The next major ASX story will hit our subscribers first

What Does the Future Hold for Venezuelan Natural Gas Development?

Venezuela's natural gas sector represents untapped potential that could fundamentally alter regional energy markets and provide long-term revenue diversification beyond crude oil exports. Understanding this potential requires examining reserve capacity, infrastructure development requirements, and regional market integration opportunities that extend beyond immediate oil sector transformation.

Untapped Gas Reserve Potential

Venezuela possesses approximately 6,300 billion cubic metres of proven natural gas reserves, ranking seventh globally in total reserve capacity. Current production of only 30 billion cubic metres annually for primarily domestic consumption demonstrates vast underdevelopment relative to geological potential and market opportunity.

These reserves exist primarily as associated gas from oil production operations and non-associated gas in dedicated reservoirs requiring independent development. Associated gas development offers near-term monetisation opportunities as oil production expansion increases gas availability, while non-associated gas development requires dedicated infrastructure investment and long-term market development strategies.

Natural Gas Reserve Distribution:

• Associated Gas: Tied to oil production expansion, immediate availability increase potential

• Non-Associated Gas: Independent reservoir development requiring dedicated infrastructure

• Unconventional Resources: Shale gas and tight gas formations requiring advanced extraction technologies

• Offshore Reserves: Maritime gas fields requiring specialised development and transportation infrastructure

Export infrastructure development requires substantial capital investment exceeding current oil sector rehabilitation estimates. Gas monetisation demands compression facilities, pipeline networks, and either regional pipeline connections or liquefied natural gas (LNG) export terminal development for global market access.

Regional Gas Market Integration Opportunities

Pipeline connections to Colombia could enable regional gas trade development, creating new revenue streams and market diversification opportunities. Existing pipeline infrastructure requires rehabilitation and expansion to accommodate increased Venezuelan gas production, while new cross-border connections demand bilateral agreements and regulatory coordination.

LNG export terminal development provides global market access opportunities, though implementation timelines extend significantly beyond oil sector recovery periods. LNG infrastructure requires port facilities, liquefaction plants, and storage capacity representing multi-billion dollar investment commitments with longer payback periods than crude oil infrastructure rehabilitation.

Regional Integration Pathways:

• Colombian Pipeline Connection: Regional market access through existing South American gas network integration

• Caribbean Gas Hub Development: Island nation supply arrangements through marine transportation

• Central American Market Access: Pipeline extension and distribution network development

• Brazilian Market Integration: Long-term supply agreements leveraging geographical proximity

Integration with Caribbean and Central American gas demand centres offers immediate market opportunities for Venezuelan gas exports. Island economies dependent on fuel oil or diesel generation could provide stable demand for Venezuelan gas through marine transportation systems requiring less infrastructure investment than major pipeline projects.

Investment Timeline for Gas Monetisation

Near-term focus on associated gas from oil production increases provides immediate monetisation opportunities requiring minimal additional infrastructure investment. Associated gas capture and processing facilities could begin operation within 2-3 years of oil sector rehabilitation, generating revenue streams supporting broader infrastructure development.

Medium-term pipeline infrastructure development targets regional market integration within 3-5 years, requiring bilateral agreements and cross-border infrastructure coordination. Pipeline projects demand substantial capital investment but offer stable revenue streams and regional market integration benefits extending beyond immediate commercial returns.

Long-term LNG export capacity development represents 7-10 year implementation timeline requiring comprehensive port development, liquefaction facility construction, and global market contract development. LNG projects offer highest revenue potential but demand greatest capital investment and longest development timelines.

Gas Development Timeline Priorities:

• Years 1-2: Associated gas capture and domestic market optimisation

• Years 3-5: Regional pipeline development and Caribbean market integration

• Years 5-7: LNG terminal feasibility studies and construction commencement

• Years 7-10: LNG export capacity operational and global market development

Investment requirements for complete gas sector development could exceed oil sector rehabilitation costs, though revenue potential offers long-term diversification benefits reducing crude oil export dependence. Gas development represents strategic complement to oil sector recovery rather than competing priority, as associated gas monetisation supports oil production economics while creating independent revenue streams.

Conclusion: Strategic Scenarios for Energy Market Evolution

The potential transformation of Venezuela's oil sector under new political leadership represents a multi-year process requiring sustained capital investment, institutional reform, and international cooperation extending far beyond immediate production increases. While near-term infrastructure constraints limit immediate output expansion, the long-term implications for global energy markets, regional competition, and geopolitical dynamics prove substantial and far-reaching.

Energy companies must navigate complex risk-reward calculations that balance first-mover advantages against political and operational uncertainties inherent in Venezuelan operations. The framework for success demands comprehensive assessment of regulatory stability, contract enforceability, and operational security considerations that extend beyond traditional commercial risk evaluation. Phased development strategies offer compromise solutions allowing market presence establishment while limiting exposure until institutional frameworks stabilise.

For regional competitors like PEMEX, the challenge involves adapting to increased competition while maintaining strategic positioning in evolving North American energy markets. Mexican energy policy requires strategic adjustment to address competitive pressures while preserving energy sovereignty principles and national development objectives. Alternative market development, technology modernisation, and renewable energy diversification provide pathways for maintaining competitiveness within sovereignty constraints.

The broader implications extend beyond commercial considerations to encompass fundamental questions about resource sovereignty, international law application, and hemispheric energy relationship structures under increased US oversight and control. The precedent established through Venezuelan resource control mechanisms may influence future international governance frameworks affecting resource-rich nations throughout Latin America and beyond.

Venezuela's natural gas development potential offers long-term diversification opportunities that could fundamentally alter regional energy markets while providing revenue streams supporting oil sector rehabilitation. Gas development represents strategic complement to oil recovery rather than competing priority, creating synergistic opportunities for comprehensive energy sector transformation under appropriate investment frameworks.

The ultimate success of Venezuelan energy sector transformation depends on sustained political stability, international investment attraction, and institutional reform implementation across multiple sectors simultaneously. While immediate production increases remain constrained by infrastructure limitations, the strategic implications for global energy security, regional market dynamics, and international governance frameworks will influence hemispheric energy relationships for decades to come.

Exploring opportunities in energy sector transitions?

Discovery Alert's proprietary Discovery IQ model provides real-time alerts on significant ASX mineral discoveries, including strategic metals and energy transition commodities that could benefit from global market shifts. Understand why major mineral discoveries can lead to exceptional returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of substantial market outcomes.