June 21, 2026

Global polymer supply networks face unprecedented stress as Middle East security concerns reshape traditional trade corridors. The intricate web connecting crude oil production, petrochemical manufacturing, and downstream polymer distribution spans thousands of nautical miles, making it vulnerable to geopolitical disruptions. Recent developments have exposed the fragility of these interconnected systems, particularly affecting regions heavily dependent on Middle Eastern polymer imports. Furthermore, the Middle East shock to tighten LatAm polymer supply has become a critical concern for industry stakeholders.

Latin American economies, with their substantial reliance on imported petrochemicals, find themselves at the center of a supply chain transformation. The region's polymer consumption patterns, built around decades of stable Middle Eastern supply relationships, now confront the reality of maritime route uncertainties and escalating transportation costs. This disruption extends far beyond immediate price adjustments, fundamentally challenging the economic foundations of polymer-dependent industries across the continent.

Understanding Maritime Supply Chain Vulnerabilities in Global Polymer Trade

Critical Shipping Route Dependencies and Risk Concentration

The global polymer supply chain's vulnerability stems from its heavy concentration through specific maritime corridors. Container shipping networks connecting Middle Eastern production hubs to Latin American ports rely on predictable transit schedules and standardized freight rates. When security concerns force route modifications, the entire cost structure shifts dramatically. However, these US tariff impacts add another layer of complexity to an already strained system.

Key vulnerability factors include:

- Transit time extensions requiring vessel rerouting around the Cape of Good Hope

- Container capacity constraints affecting short-notice shipments to South America's eastern ports

- Equipment imbalancing as vessel repositioning creates shortages on feeder services

- Port operational delays due to enhanced security protocols

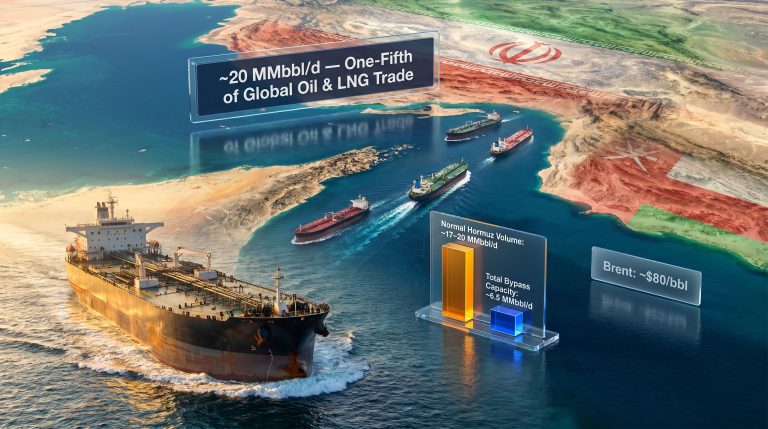

According to major polymer operations reports, emergency and war-risk shipping surcharges have reached initial guidance levels near $1,500 per 20-foot equivalent unit, with prompt offers approaching $3,000 per 40-foot container. These surcharges represent immediate cost increases that import-dependent economies must absorb through their supply chains.

Economic Transmission Through Freight Cost Multipliers

The mathematical relationship between shipping disruptions and delivered polymer costs creates compounding effects throughout Latin American markets. Import-parity pricing formulas automatically incorporate new surcharges and extended routing costs, lifting delivered prices independent of upstream production costs. In addition, the oil price rally compounds these pressures.

Cost escalation mechanisms operate through:

- Direct freight surcharge pass-through to import prices

- Insurance premium adjustments reflecting elevated maritime risk

- Currency volatility amplifying dollar-denominated shipping costs

- Inventory carrying cost increases due to extended lead times

Market participants report that container shipping space remains severely constrained as vessel operators reduce departures on high-exposure routes and implement booking deferrals. This capacity tightness particularly affects time-sensitive shipments to major Brazilian import terminals including Santos and Manaus.

When big ASX news breaks, our subscribers know first

Regional Import Dependency Analysis: Quantifying Vulnerability

Brazil's Structural Exposure to Middle Eastern Polymer Sources

Brazil's polymer import statistics reveal the depth of regional dependency on Middle Eastern suppliers. The country's import profile demonstrates concentrated exposure that cannot be easily diversified in short timeframes. Consequently, the tariff market effects further complicate sourcing strategies.

| Polymer Grade | Source Country | 2025 Volume (tonnes) | Market Share | Supply Rank |

|---|---|---|---|---|

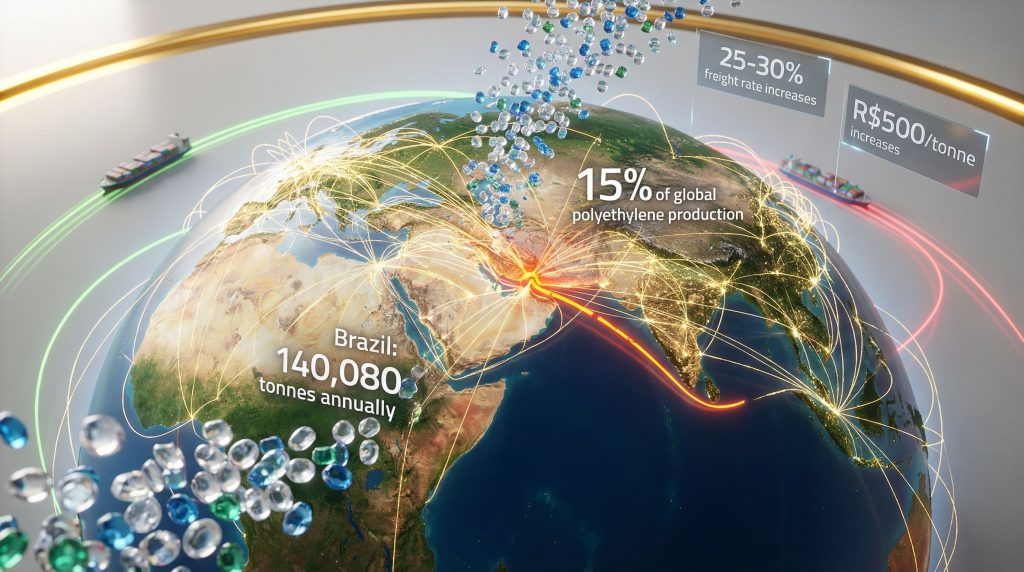

| Polypropylene | Saudi Arabia | 140,080 | 20% of total imports | 2nd largest |

| Polyethylene | Saudi Arabia | 56,445 | Not specified | 3rd largest |

| Polyethylene | Egypt | 47,795 | Not specified | 5th largest |

| PVC | Egypt | 100,090 | 68% YoY increase | Major growth |

These volumes represent substantial supply relationships built over years of commercial partnerships. The combined Middle Eastern exposure across polypropylene and polyethylene categories indicates that 35-40% of Brazil's polymer imports originate from suppliers now facing shipping constraints.

Brazilian chemical industry association Abiquim identified three primary transmission mechanisms affecting the country's petrochemical sector: elevated crude oil prices increasing feedstock costs, exchange rate volatility raising import expenses, and reduced availability of traditional feedstock sources. The association specifically warned that sustained increases in Brent crude pricing would elevate petrochemical naphtha costs, representing a structural vulnerability for Brazil as a net importer of chemical derivatives.

Manufacturing Sector Impact Assessment

The Middle East shock to tighten LatAm polymer supply creates cascading effects through Brazil's manufacturing base. Industries dependent on consistent polymer inputs face operational planning challenges as delivery schedules become unpredictable and material costs fluctuate.

Immediate operational impacts include:

- Production scheduling disruptions due to uncertain delivery windows

- Increased working capital requirements for extended inventory cycles

- Quality control challenges when sourcing from alternative suppliers

- Contract renegotiation pressures in long-term supply agreements

Braskem, Brazil's largest petrochemical producer, demonstrated rapid market response by withdrawing its February 28, 2026 pricing policy and issuing revised schedules on March 2, 2026. The company implemented price increases of R$500 per metric tonne (approximately $95/tonne) for LDPE, HDPE, LLDPE, and metallocene PE grades, with R$250/tonne increases for PP homopolymer and copolymer grades.

Macroeconomic Transmission Mechanisms: From Energy Markets to Consumer Prices

Crude Oil Price Sensitivity in Polymer Production Economics

The relationship between crude oil benchmarks and polymer pricing operates through multiple channels, creating both direct and indirect cost pressures. Naphtha, a key petrochemical feedstock derived from crude oil refining, serves as the primary input for ethylene and propylene production. These building blocks form the foundation of polyethylene and polypropylene manufacturing. Furthermore, the US–China trade war adds geopolitical complexity to these supply chains.

Feedstock cost escalation pathway:

- Brent crude price increases → Naphtha feedstock cost elevation

- Higher naphtha prices → Increased ethylene/propylene production costs

- Elevated monomer costs → Rising polyethylene/polypropylene production expenses

- Producer margin compression without complete customer price pass-through

Brazil's position as a net importer of chemical derivatives amplifies these pressures. The country imports approximately 85% of its fertilizer requirements and remains exposed to nitrogen fertilizer price volatility due to Iran's significant role as an exporter of urea, ammonia, and methanol.

Currency and Financial Market Dynamics

Geopolitical uncertainty typically drives US dollar appreciation, creating additional cost pressures for import-dependent Latin American economies. The dual impact of rising commodity prices and strengthening dollars compounds the financial stress on polymer supply chains. Moreover, oil price movements influence currency volatility.

Financial transmission channels include:

- Dollar strengthening increasing landed costs for all polymer imports

- Local currency depreciation amplifying feedstock price increases

- Central bank policy responses affecting domestic interest rates

- Credit market conditions influencing working capital availability

Exchange rate volatility creates particular challenges for companies with natural hedges between export revenues and import costs. Polymer converters typically lack such natural hedging, making them vulnerable to sustained currency movements.

Supply Chain Resilience and Alternative Sourcing Dynamics

Geographic Diversification Challenges and Opportunities

The current supply disruption accelerates long-term strategic planning around geographic diversification. However, alternative sourcing presents its own complexities in terms of logistics, quality specifications, and commercial relationships.

Alternative sourcing considerations:

- Asian suppliers balancing domestic demand growth against export commitments

- North American producers evaluating export capacity amid strong domestic markets

- European chemical industry competitiveness in Latin American markets

- Transportation cost differentials affecting delivered pricing comparisons

Market participants describe converter responses including front-loaded purchasing to secure supply, acceptance of wider delivery windows to reduce costs, and evaluation of alternative origins despite higher nominal prices. This behavioral shift indicates supply security concerns outweighing traditional cost optimization strategies.

Logistics Network Reconfiguration Requirements

The transition to alternative shipping routes requires comprehensive logistics planning extending beyond simple freight cost calculations. Container availability, port capacity constraints, and storage limitations create bottlenecks that affect supply chain efficiency.

Infrastructure considerations:

- Container equipment positioning for alternative routes

- Port storage capacity for delayed shipments

- Inland transportation connections from alternative ports

- Customs processing capabilities for increased import volumes

Equipment shortages on feeder services compound these challenges as vessel repositioning creates imbalances in container availability. Rising premiums for guaranteed shipping space indicate market recognition of these capacity constraints.

Long-term Market Structure Evolution

Investment Flow Redirection and Capacity Planning

Supply chain disruptions often catalyse long-term structural changes in industrial investment patterns. The current situation may accelerate domestic polymer production capacity development in Latin America, though such projects require substantial capital and multi-year development timelines.

Investment considerations include:

- Foreign direct investment in regional polymer production facilities

- Technology transfer opportunities arising from supply diversification

- Regional integration initiatives for chemical industry development

- Strategic reserve policies for critical chemical inputs

The economic justification for domestic capacity expansion depends on sustained price differentials and supply security concerns. Historical precedent suggests that temporary disruptions rarely support long-term investment decisions unless they reveal persistent structural vulnerabilities.

Policy Framework Adaptation

According to global market analysis, industry experts note: "The situation underscores structural weaknesses in Brazil's chemical chain and the need for long-term policies that reduce dependence on imported naphtha, fertilizers and other strategic inputs."

Government policy responses typically evolve through multiple phases, beginning with emergency measures and progressing toward structural reforms. Current polymer supply disruptions may prompt regulatory frameworks addressing strategic material security and industrial resilience.

Potential policy developments:

- Strategic reserve establishment for critical chemical inputs

- Trade agreement modifications enhancing supply security

- Industrial policy coordination across regional economies

- Emergency import procedures and tariff adjustment mechanisms

Market Price Discovery and Risk Management Evolution

Contract vs. Spot Market Dynamics

The polymer market's price discovery mechanism faces stress as traditional supply relationships encounter disruption. Contract pricing formulas designed for stable supply conditions may require adjustment for extended periods of logistics volatility.

Price discovery challenges:

- Contract renegotiation triggers during extended force majeure periods

- Spot market price volatility affecting benchmark calculations

- Regional price differential expansion due to transportation cost variations

- Forward market development for polymer price risk management

Market participants indicate that sustained disruptions could force fundamental changes in commercial terms, including pricing mechanisms, delivery specifications, and force majeure definitions.

Competitive Positioning Shifts

The Middle East shock to tighten LatAm polymer supply creates temporary competitive advantages for producers with less exposure to affected shipping routes. Regional polymer manufacturers may experience margin expansion opportunities as import competition faces cost disadvantages.

Competitive dynamics include:

- Domestic producer margin expansion during import cost increases

- Import substitution acceleration in key polymer grades

- Export competitiveness shifts due to cost structure changes

- Market share redistribution based on supply reliability

These competitive shifts may persist beyond the immediate supply disruption if they demonstrate superior supply chain resilience.

The next major ASX story will hit our subscribers first

Strategic Planning Framework for Market Participants

Corporate Risk Management Adaptations

Companies operating in polymer supply chains must evaluate their risk management frameworks against demonstrated vulnerabilities. The current disruption provides practical insights into the effectiveness of existing contingency planning.

Risk management considerations:

- Supply chain diversification cost-benefit analysis

- Financial hedging instruments for commodity price and currency exposure

- Operational flexibility investments for demand uncertainty

- Supplier relationship management during crisis periods

The balance between supply security and cost optimisation requires careful calibration based on individual company circumstances and risk tolerance levels.

Investment Implications for Financial Markets

The Middle East shock to tighten LatAm polymer supply creates differentiated impacts across financial market sectors. Companies with high exposure to import costs face margin pressure, whilst those with domestic production capability or alternative supply sources may benefit from reduced competition.

Financial market considerations include:

- Equity market reactions in polymer-dependent manufacturing sectors

- Credit quality assessments for highly leveraged chemical companies

- Commodity fund positioning strategies during geopolitical volatility

- Currency hedging demand from import-dependent corporations

Disclaimer: This analysis is based on publicly available market information and industry reports. Commodity markets involve substantial risk, and past performance does not guarantee future results. Investors should conduct their own due diligence and consider consulting with qualified financial advisors before making investment decisions. Market conditions can change rapidly, and the scenarios discussed may not materialise as described.

The ongoing evolution of global polymer supply chains reflects broader themes of supply security, economic resilience, and geopolitical risk management. Whilst immediate disruptions create operational challenges, they also highlight opportunities for structural improvements in supply chain design and risk mitigation strategies. Market participants who successfully navigate these challenges may emerge with competitive advantages and more robust operational frameworks for future uncertainty.

Looking to Capitalise on Commodity Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex market disruptions like polymer supply chain shocks into actionable investment insights. Experience why historic commodity discoveries can generate substantial returns even during periods of global supply uncertainty, and begin your 14-day free trial today to position yourself ahead of the market.