June 19, 2026

Portugal's critical minerals energy transition potential has captured significant attention as the geopolitical landscape for critical mineral supply chains experiences unprecedented transformation, driven by escalating tensions between major powers and Europe's urgent need for resource independence. Portugal finds itself positioned at the centre of this strategic shift, as policymakers and investors recognise the country's potential to reduce European dependence on Chinese-controlled rare earth supply chains.

This transformation extends beyond simple resource discovery into the complex realm of integrated supply chain development, where geological potential must align with processing capabilities, regulatory frameworks, and market dynamics to create viable commercial operations.

Geographic Distribution of Mineral Resources

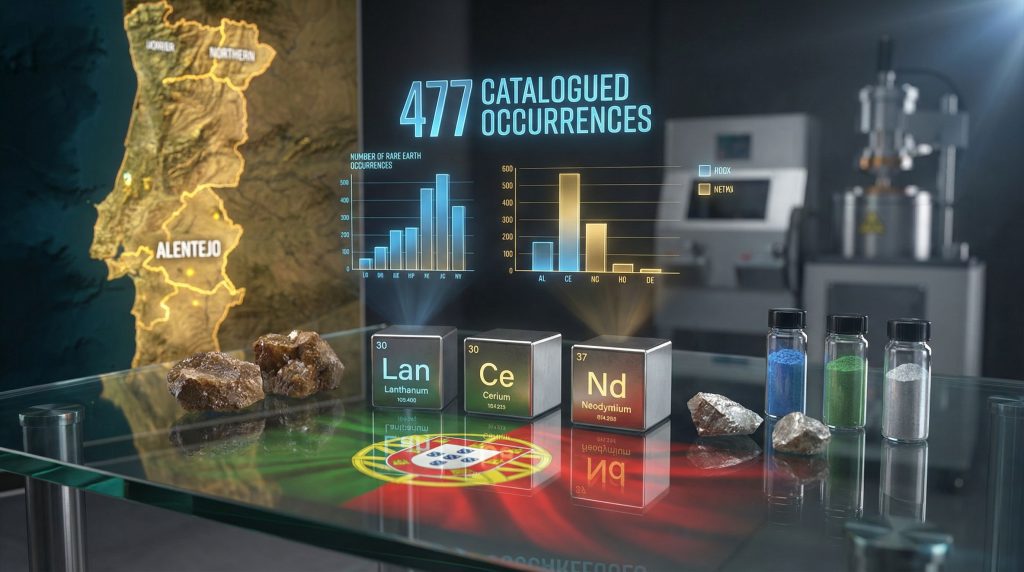

Portugal's geological diversity spans multiple provinces, each offering distinct mineralisation styles and development opportunities. The 477 catalogued critical mineral occurrences documented by the National Laboratory of Energy and Geology (LNEG) represent decades of systematic geological survey work, creating a comprehensive database that distinguishes Portugal from many European jurisdictions where mineral potential remains poorly understood.

The Alentejo region has emerged as a focal point for recent exploration activities, with field surveys in the Penedo Gordo area identifying a complex assemblage of strategic elements including zirconium, hafnium, titanium, niobium, tantalum, yttrium, and scandium. This polymetallic character reflects the region's diverse geological evolution and suggests potential for integrated extraction strategies that could improve project economics through multiple revenue streams.

Furthermore, northern Portugal leverages established mining heritage and infrastructure advantages accumulated through decades of tungsten and base metal production. The region hosts documented monazite occurrences within the Moncorvo iron ore deposits, providing a known geological context where rare earth elements occur alongside traditional mining operations. This integration offers potential pathways for rare earth recovery as byproducts of existing mining activities, reducing standalone development costs and technical risks.

Portugal's Position in Europe's Resource Security Strategy

The European Union's Critical Raw Materials Act creates accelerated permitting pathways specifically designed to fast-track strategic mineral projects that enhance European resource security. Portugal benefits from this policy framework through its stable political environment, established regulatory systems, and geographic position within European transportation networks.

Within the broader European context, Portugal's documented mineral inventory positions the country among the continent's most extensively surveyed critical mineral provinces. This advantage stems from sustained geological research by institutions such as LNEG and the National Laboratory for Civil Engineering (LNEC), creating technical foundations that reduce early-stage exploration risks for potential investors.

In addition, strategic importance within European supply chain diversification goals extends beyond raw material extraction into processing and manufacturing capabilities. Portugal's Atlantic port access at Setúbal and Sines provides infrastructure for bulk mineral logistics, while proximity to major European end-users in automotive, renewable energy, and aerospace sectors reduces transportation costs compared to extra-European sourcing alternatives.

When big ASX news breaks, our subscribers know first

What Makes Portugal's Rare Earth Deposits Unique?

The fundamental challenge facing global rare earth supply chains lies not in mineral scarcity, but in processing bottlenecks and geographic concentration of value-added manufacturing. China maintains control over approximately 61% of global rare earth mining capacity, yet dominates 80% or greater of global rare earth processing capacity and roughly 90% of rare-earth magnet manufacturing. This disproportion reveals that mineral extraction represents only the initial stage of value creation, with downstream processing representing the critical constraint for European independence.

Consequently, Portugal's geological characteristics present both opportunities and challenges within this global context. The country's mineral occurrences demonstrate complex polymetallic associations that distinguish them from monometallic rare earth districts typical of established global operations.

Geological Characteristics and Mineralisation Types

Portuguese rare earth occurrences primarily associate with iron-oxide-copper-gold (IOCG) systems, representing a recognised metallogenic style that produces multi-element deposits with varying rare earth concentrations. This geological framework suggests that Portuguese rare earth development could integrate within broader iron and copper production systems, potentially enabling co-product recovery scenarios rather than standalone rare earth mining operations.

Monazite mineralisation within polymetallic environments provides established processing pathways but requires integrated recovery strategies due to associated iron and copper mineralisation. The crystalline structure of monazite incorporates thorium and uranium as trace elements in many global deposits, introducing radioactive material handling requirements that elevate processing complexity and regulatory oversight in European operating environments.

However, alkaline intrusion-hosted rare earth potential identified through recent geochemical surveys in Alentejo represents a distinct geological environment historically associated with nepheline-syenite and carbonatite-hosted rare earth deposits. This geological setting typically produces enriched rare earth concentrations but demands distinctive processing approaches compared to IOCG mineralisation, suggesting site-specific metallurgical development requirements.

Critical Elements Beyond Traditional Rare Earths

| Element Category | Key Elements | Primary Locations | Development Stage |

|---|---|---|---|

| Light REEs | Lanthanum, Cerium, Neodymium | Moncorvo, Alentejo | Early exploration |

| Heavy REEs | Yttrium, Scandium | Penedo Gordo | Prospecting |

| Strategic Metals | Zirconium, Hafnium, Niobium | Multiple regions | Resource definition |

| Battery Metals | Lithium, Cobalt | Barroso, various | Advanced development |

Critical to technical understanding is the distinction between true rare earth elements and strategic metals commonly grouped with them in media reporting. While yttrium and scandium qualify as rare earth elements per International Union of Pure and Applied Chemistry (IUPAC) classification, materials such as zirconium, hafnium, titanium, and niobium represent distinct commodity markets with separate processing routes, geopolitical supply dynamics, and end-user applications.

For instance, this technical distinction carries significant investment implications due to different economic thresholds and market demand profiles. Zirconium and hafnium markets centre on nuclear and aerospace applications with distinct supply-demand dynamics compared to rare earth permanent magnet markets. Understanding these distinctions prevents misallocation of capital and enables appropriate risk assessment for investors considering Portuguese mineral opportunities.

How Do Portugal's 477 Catalogued Occurrences Compare Globally?

Portugal's extensive mineral inventory reflects systematic geological survey work spanning multiple decades, creating a technical foundation that distinguishes the country from jurisdictions where mineral potential remains poorly documented. However, critical limitations exist in translating geological potential into commercial viability, particularly regarding resource estimation and economic evaluation.

Resource Scale and Grade Considerations

No published NI 43-101 compliant resource estimates exist for Portuguese rare earth projects as of current assessment periods. The absence of bankable resource statements represents a fundamental limitation in comparative analysis, as grade distributions, tonnage estimates, and mining reserve calculations remain undefined at all major Portuguese occurrences.

This resource maturity gap positions Portuguese projects significantly behind established global operations where detailed geological modelling, metallurgical testing, and economic evaluation have progressed through feasibility study stages. Expert geological assessment emphasises that Portuguese discoveries remain at prospecting stage classification, indicating that preliminary exploration has identified mineralisation but systematic resource estimation has not commenced.

Furthermore, preliminary assay results from recent exploration campaigns provide encouraging indicators but require substantial additional work to establish economic viability. The progression from geological discovery to resource definition typically requires three to five years of systematic drilling, sampling, and metallurgical testing, followed by additional feasibility assessment phases before commercial development decisions can proceed.

Infrastructure and Logistical Advantages

Portugal benefits from substantial infrastructure advantages compared to frontier rare earth jurisdictions. Deep-water Atlantic port facilities at Setúbal and Sines provide capacity for bulk mineral concentrate export without requiring port development investments. These facilities currently handle iron ore, copper concentrates, and industrial minerals, demonstrating operational experience relevant to rare earth logistics requirements.

Transportation network integration within European systems enables rail and truck logistics to major processing centres in Central Europe without extra-territorial bottlenecks. This connectivity reduces logistics costs and timeline uncertainties compared to offshore sourcing alternatives from Africa or Southeast Asia.

Skilled workforce availability stems from Portugal's mining heritage, particularly tungsten, copper, and base metal operations that maintained experienced personnel through recent operational periods. The Borralha tungsten mining operation retained skilled workforce through commercial production phases, providing a technical personnel base for potential rare earth development without requiring extensive workforce development programmes.

Technical services infrastructure includes established mining engineering firms, environmental assessment companies, and geological consultancies operating within Portuguese jurisdiction. Portuguese universities maintain mining engineering and geological programmes that provide ongoing technical education and research capabilities relevant to rare earth development.

Critical Supply Chain Reality: While China controls 61% of global rare earth mining, it dominates 80%+ of processing capacity and 90% of magnet manufacturing, highlighting the downstream bottleneck that Portuguese discoveries must address.

What Are the Primary Investment Challenges?

Investment decision frameworks for Portuguese rare earth opportunities must account for multiple technical, regulatory, and economic constraints that distinguish European development from operations in jurisdictions with established rare earth production infrastructure. Understanding the current critical minerals strategy becomes essential when evaluating these challenges.

Processing Infrastructure Gap Analysis

The fundamental constraint facing Portuguese rare earth development lies in downstream processing capability rather than geological potential. European rare earth processing infrastructure remains severely limited compared to Asian facilities, creating potential bottlenecks that could strand mineral resources despite successful extraction operations.

Integration requirements for polymetallic Portuguese deposits present elevated complexity compared to monometallic rare earth operations. The simultaneous presence of iron, copper, zirconium, hafnium, and rare earth minerals within single deposits requires coordinated beneficiation strategies and shared processing infrastructure, complicating project economics and demanding metallurgical innovation specific to Portuguese ore characteristics.

Technology transfer challenges emerge from limited European experience with integrated rare earth processing. Acquiring proven metallurgical expertise requires partnerships with established operators or substantial investment in process development and pilot plant testing to adapt global technologies to Portuguese mineral characteristics.

Regulatory and Environmental Hurdles

European Union environmental legislation creates comprehensive assessment requirements that extend development timelines compared to jurisdictions with streamlined permitting processes. Environmental impact assessments must address air quality, water resources, biodiversity protection, and community consultation requirements that can require two to four years for completion depending on project scale and environmental sensitivity. A comprehensive mining permitting guide helps navigate these complex requirements.

Community engagement challenges have emerged prominently in Portugal's lithium development experience, where rural opposition has created substantial delays and legal challenges for proposed operations. The high-profile Barroso lithium project has encountered sustained community pushback and legal proceedings that demonstrate potential social licence risks for future rare earth development.

Permitting timeline coordination between multiple regulatory agencies creates potential bottlenecks where environmental, mining, and processing permits must align for integrated operations. European regulatory harmonisation provides framework consistency but cannot eliminate inherent complexity in multi-jurisdictional approval processes.

Capital Requirements and Technical Complexity

Development cost estimates for integrated rare earth operations range substantially depending on processing strategy, production scale, and infrastructure requirements. European labour costs, environmental standards, and regulatory compliance expenses typically exceed those in developing jurisdictions, requiring higher ore grades or processing efficiencies to maintain economic viability.

Metallurgical innovation requirements specific to Portuguese polymetallic mineralisation may necessitate substantial process development investments before commercial operations can commence. Adapting proven rare earth processing technologies to Portuguese ore characteristics requires pilot plant testing and metallurgical optimisation that extends development timelines and capital requirements.

Technology partnership strategies become essential for accessing established rare earth processing expertise while maintaining European operational control. Joint venture structures with experienced rare earth operators provide technical capabilities but require careful structuring to align partner incentives and maintain strategic independence objectives.

Which Projects Show the Most Promise?

Portuguese rare earth development potential concentrates in several distinct geological environments, each presenting unique technical characteristics and development pathways that influence investment attractiveness and commercial viability timelines. These developments align with broader mining industry trends towards polymetallic recovery systems.

Advanced-Stage Developments

The Barroso lithium project provides a development template demonstrating how large-scale mineral extraction can progress through European regulatory processes, despite encountering community opposition and environmental challenges. This project's advancement through feasibility stages offers insights into permitting timelines, capital requirements, and operational strategies applicable to rare earth development in similar Portuguese geological environments.

Borralha tungsten project revival presents opportunities for rare earth co-product development within established mining infrastructure. Historical tungsten operations provide existing permits, waste management systems, and community familiarity with mining activities that could expedite rare earth development compared to greenfield projects requiring comprehensive new permitting processes.

Integration opportunities between existing and emerging projects enable potential cost sharing for processing infrastructure, transportation systems, and regulatory compliance that improves individual project economics through operational synergies and reduced capital intensity per project.

Early-Stage Exploration Targets

• Monforte-Tinoca occurrence characteristics indicate polymetallic mineralisation with rare earth associations requiring detailed geological evaluation to establish resource potential and processing requirements for commercial development timelines

• Assumar project geology demonstrates typical Portuguese multi-element mineral systems where rare earth concentration occurs alongside strategic metals, necessitating integrated extraction strategies and metallurgical innovation for economic viability

• Crato-Arronches multi-element potential reflects complex mineralisation patterns requiring systematic exploration and resource definition before development strategies can be finalised and investment decisions can proceed with confidence

• Penedo Gordo heavy rare earth enrichment presents particular interest due to elevated economic value of heavy rare earth elements and limited global supply sources, though processing complexity requires substantial technical evaluation and development

How Does Market Timing Affect Portugal's Opportunities?

Global rare earth market dynamics continue evolving through supply chain diversification initiatives, technological advancement in end-user applications, and shifting geopolitical relationships that influence long-term demand patterns and pricing structures. Understanding the trade war impact on these dynamics remains crucial for market timing assessments.

Global Supply-Demand Dynamics

Projected demand growth through 2030 reflects accelerating adoption of permanent magnet technologies in automotive electrification, wind energy expansion, and consumer electronics advancement. European automotive manufacturers increasingly require rare earth permanent magnets for electric vehicle motor systems, creating regional demand that could support Portuguese production development.

European renewable energy sector requirements drive substantial neodymium and dysprosium demand for wind turbine generator systems, where proximity to Portuguese production could reduce supply chain risks and transportation costs compared to Asian sourcing alternatives. This aligns with Europe's growing focus on critical mineral independence.

Defence and aerospace applications create additional demand streams for specific rare earth elements used in guidance systems, communications equipment, and advanced materials applications where supply security considerations may justify premium pricing for European sources.

Geopolitical Risk Considerations

Trade policy impacts on China-Europe rare earth flows create potential market opportunities for alternative suppliers, though policy volatility introduces uncertainty regarding long-term market access and pricing stability that complicates investment planning and project financing decisions.

Strategic partnership opportunities with allied nations enable potential technology sharing, market access coordination, and financing support that could accelerate Portuguese project development while maintaining European strategic independence objectives.

Consequently, technology transfer restrictions increasingly limit access to advanced rare earth processing technologies, creating incentives for European innovation and domestic capability development that could benefit Portuguese operations through policy support and market protection measures.

The next major ASX story will hit our subscribers first

What Should Investors Watch For?

Investment monitoring frameworks for Portugal rare earth potential must track technical advancement, regulatory progression, and market development indicators that signal commercial viability and development timeline acceleration or delays.

Key Development Milestones

The most critical near-term indicators for Portugal rare earth potential include completion of NI 43-101 compliant resource estimates, environmental permitting approvals, offtake agreement announcements, and EU Critical Raw Materials Act funding decisions.

Resource estimation completion represents the fundamental transition from geological potential to economic evaluation, enabling detailed technical and financial assessment that supports investment decision-making and project financing discussions.

Environmental permitting progression through Portuguese and European regulatory systems provides critical timeline indicators for commercial development, as permitting delays can extend development schedules by multiple years and substantially increase capital requirements.

Offtake agreement announcements signal market validation of Portuguese rare earth production and provide revenue certainty that enables project financing while demonstrating end-user confidence in technical and operational capabilities.

Funding allocation under European Union strategic programmes indicates policy support levels and provides non-dilutive capital that improves project economics and reduces private investment requirements for development advancement. Recent developments show Portugal's rare mineral potential gaining international recognition.

Risk Management Strategies

Diversification across multiple projects and commodities reduces concentration risk while providing exposure to different geological environments, development timelines, and market opportunities that may progress at different rates through technical and regulatory advancement phases.

Environmental and social governance compliance requirements demand proactive community engagement, environmental monitoring, and regulatory coordination that prevents development delays and maintains social licence for long-term operations.

Currency and regulatory risk hedging becomes essential for long-term investment strategies where development timelines span multiple years and expose investors to policy changes, currency fluctuations, and regulatory modifications that could impact project economics and commercial viability.

Frequently Asked Questions About Portugal Rare Earth Investment

Timeline and Development Expectations

When might Portugal's rare earth projects reach commercial production?

Based on current development stages and typical rare earth project timelines, Portuguese projects currently at prospecting stage require approximately 8-12 years to reach commercial production, assuming successful resource definition, permitting approval, and project financing. This timeline reflects the complex technical, regulatory, and financial requirements specific to rare earth development in European regulatory environments.

What are the typical development costs for European rare earth operations?

European rare earth development costs typically range from $200-500 million for integrated extraction and processing operations, depending on production scale, processing complexity, and infrastructure requirements. Portuguese projects may benefit from existing port and transportation infrastructure, but higher European labour costs and environmental standards generally exceed development costs in other global jurisdictions.

How do Portuguese projects compare to Australian and North American alternatives?

Portuguese projects offer European Union regulatory harmonisation and proximity to end-user markets, while Australian and North American operations typically demonstrate more advanced development stages, established resource estimates, and proven processing technologies. Investment decision frameworks must balance political stability, market access, and development risk factors specific to each jurisdictional environment.

Market Access and Competitiveness

Can Portuguese rare earths compete with Chinese production costs?

Direct cost competition with Chinese operations remains challenging due to lower labour costs, established processing infrastructure, and economies of scale in Chinese operations. Portuguese competitiveness depends on European policy support, supply security premiums, and potential carbon footprint advantages that may justify higher production costs for European end-users prioritising supply chain security.

What downstream processing capabilities exist in Europe?

European rare earth processing capabilities remain limited, with most operations focused on specific niche applications rather than comprehensive rare earth separation and magnet manufacturing. Developing integrated European processing infrastructure represents a critical requirement for Portuguese mine development and may require substantial additional investment beyond extraction operations.

Which end-user industries offer the strongest demand growth?

European automotive electrification drives the strongest near-term demand growth for rare earth permanent magnets, followed by offshore wind energy development and industrial automation applications. Defence and aerospace sectors provide additional demand with supply security requirements that may support premium pricing for European sources.

Strategic Scenarios for Portugal's Rare Earth Future

Long-term assessment of Portugal rare earth potential requires scenario analysis that accounts for technical, regulatory, and market uncertainties that could substantially influence commercial outcomes and investment returns over development timelines spanning multiple decades.

Optimistic Development Pathway

Successful resource delineation leading to integrated production assumes completion of detailed geological evaluation, metallurgical testing, and resource estimation that demonstrates economic viability comparable to established global operations. This scenario requires sustained exploration investment, favourable geological results, and successful navigation of technical challenges specific to Portuguese polymetallic mineralisation.

European Union strategic funding supporting downstream processing development could provide substantial non-dilutive capital that improves project economics while advancing European strategic independence objectives. Policy coordination between member states could create integrated supply chain development programmes that accelerate individual project timelines through shared infrastructure and technology development.

Technology partnerships enabling competitive cost structures assume successful collaboration with established rare earth operators who provide technical expertise while maintaining European operational control and strategic independence. These partnerships could accelerate development timelines and reduce technical risks through proven processing technologies adapted to Portuguese geological characteristics.

Realistic Base Case Assessment

Selective project advancement based on economic viability reflects likely outcomes where only the highest-grade, most accessible Portuguese deposits progress through development while others remain undeveloped due to technical or economic constraints. This scenario assumes continued Chinese market dominance with gradual European market share gains in specific applications.

Continued dependence on Asian processing infrastructure indicates that Portuguese mining operations may require export of mineral concentrates for processing in established Asian facilities, limiting value addition and maintaining strategic dependence despite European extraction capabilities.

Gradual market share gains in specific niche applications where European production advantages (proximity, supply security, environmental standards) justify premium pricing while broader rare earth markets remain dominated by lower-cost Asian production.

Conservative Risk Scenario

Environmental and social opposition limiting development scope assumes continued community resistance similar to Portuguese lithium project experiences, where rural opposition creates sustained legal challenges and development delays that extend timelines and increase capital requirements beyond economic viability thresholds.

Insufficient capital availability for large-scale projects reflects potential constraints in European capital markets where rare earth investment remains limited due to technical complexity, long development timelines, and uncertain returns compared to alternative investment opportunities.

Continued Chinese market dominance despite European initiatives assumes successful Chinese adaptation to European supply security concerns through pricing strategies, technology advancement, and strategic partnerships that maintain market control while addressing European political requirements.

Conclusion: Balancing Promise with Pragmatism

Portugal rare earth potential represents genuine geological opportunity within European strategic resource development, yet translation of this potential into commercial operations requires realistic assessment of technical, regulatory, and economic challenges that distinguish rare earth development from conventional mining activities.

Investment Decision Framework

Criteria for evaluating Portuguese rare earth opportunities must prioritise geological validation through systematic resource estimation, metallurgical testing that addresses polymetallic processing complexity, and regulatory progression that demonstrates environmental and community acceptance. Technical due diligence should emphasise processing technology access, integration strategies for multi-element recovery, and comparison with global rare earth operations regarding costs, timelines, and market competitiveness.

Portfolio allocation strategies for European critical minerals exposure should consider Portuguese projects as long-term strategic positions rather than near-term production opportunities, given current early-stage development status and substantial technical work required before commercial operations become viable.

Long-term outlook for Portugal's role in global supply chains depends on successful coordination between geological potential, processing infrastructure development, and European policy support that creates sustainable competitive advantages beyond proximity and supply security considerations. Investment success requires patience for extended development timelines and acceptance of technical risks inherent in complex polymetallic rare earth systems.

Disclaimer: This analysis is provided for informational purposes only and does not constitute investment advice. Rare earth mining investments involve substantial risks, including technical, regulatory, and market uncertainties. Prospective investors should conduct independent due diligence and consult qualified professionals before making investment decisions.

Ready to Stay Ahead of the Next Major Mineral Discovery?

As Portugal's rare earth potential demonstrates the complex interplay between geological opportunity and commercial reality, savvy investors understand that significant discoveries across Australia's mining sector can emerge at any time. Discovery Alert's proprietary Discovery IQ model delivers instant notifications when major ASX mineral discoveries are announced, transforming complex geological data into actionable investment insights that position subscribers ahead of broader market awareness.