August 7, 2026

The Carbon Cost Divide Reshaping Aluminium Markets

For decades, the economics of aluminium recycling rested on a single, reliable truth: scrap was cheaper than ore. That fundamental assumption is now under structural pressure from two directions simultaneously. On one side, aluminium scrap prices have surged to levels that make secondary feedstock economically comparable to primary ingot. On the other, the European Union's Carbon Border Adjustment Mechanism is introducing a carbon liability framework that permanently alters the competitive calculus between primary smelting and secondary remelting.

The result is not a cyclical correction. It is a permanent bifurcation of the aluminium value chain into two distinct cost economies, separated not by geography or ore quality, but by carbon intensity. Understanding where the dividing line falls, and why it runs directly through the primary vs secondary aluminium scrap and CBAM nexus, is now a prerequisite for any serious procurement or investment strategy in this sector.

When big ASX news breaks, our subscribers know first

Two Production Routes, One Widening Carbon Gap

The Thermodynamics That Drive Everything

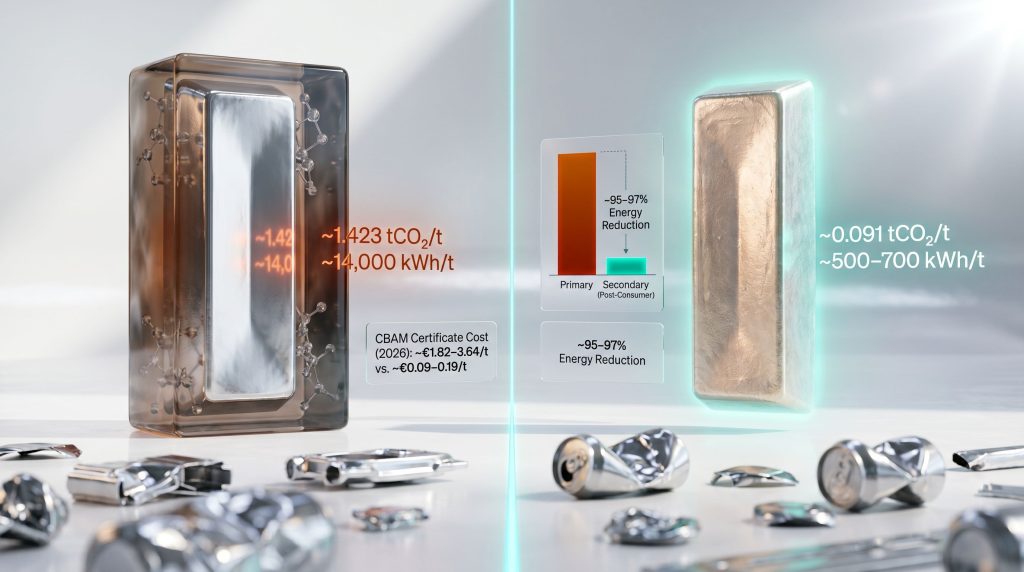

The energy physics of aluminium production are not negotiable. Producing one tonne of primary aluminium through the Hall-Héroult electrolytic reduction process requires approximately 14,000 kilowatt-hours of electricity. This is not an engineering inefficiency that can be optimised away; it is a thermodynamic requirement of reducing aluminium oxide into metallic aluminium through electrolysis.

Remelting the equivalent mass of aluminium scrap requires approximately 500 to 700 kilowatt-hours per tonne. That represents a 95 to 97 percent reduction in energy consumption relative to primary production. At current industrial electricity rates, that differential translates to roughly USD 1.47 saved per kilogram of metal produced. For a mid-scale remelter processing 200,000 tonnes annually, the theoretical operating energy advantage exceeds USD 290 million before a single carbon tariff enters the calculation.

This energy advantage has always existed. What has changed is that carbon regulation is now converting that thermodynamic advantage into a measurable, quantifiable, and escalating financial premium. Consequently, the broader shifts already visible across aluminum and alumina markets are accelerating the urgency of this strategic reorientation.

| Production Metric | Primary Aluminium | Secondary Aluminium |

|---|---|---|

| Energy Consumption (kWh/t) | ~14,000 | ~500–700 |

| Energy Reduction vs. Primary | Baseline | ~95–97% |

| Direct CO₂ Emissions (tCO₂/t) | ~1.5 | ~0.05–0.10 |

| CBAM Benchmark Emission Factor (2026) | ~1.423 tCO₂/t | ~0.091 tCO₂/t |

| Estimated CBAM Certificate Cost (2026) | ~€1.82–3.64/t | ~€0.09–0.19/t |

How CBAM Prices the Gap Between Primary and Secondary

The Mechanism Behind the Carbon Border Adjustment

The EU's Carbon Border Adjustment Mechanism entered its transitional phase in October 2023 and is progressively tightening through full implementation from 2026 onwards. For aluminium imports, CBAM applies a carbon certificate cost calibrated to a product's embedded direct emissions, specifically capturing:

- Anode consumption emissions during electrolytic smelting

- Perfluorocarbon gas emissions generated during the Hall-Héroult process

- Direct process emissions attributable to the production pathway

One structurally important design feature: CBAM excludes indirect emissions from grid electricity consumption. This exclusion means that the carbon cost applied to primary aluminium focuses on process chemistry rather than power source, though the direct emission factors are still substantial. Furthermore, understanding the full scope of aluminium tariffs impact provides important context for how overlapping trade and carbon policies are reshaping import economics simultaneously.

The EU has set its initial CBAM certificate price at €75.36 per tonne of CO₂ for Q1 2026. Applying this to the respective emission factors produces a stark cost divergence. Primary aluminium imports face a CBAM liability in the range of €1.82 to €3.64 per tonne under 2026 benchmark rates, while secondary aluminium derived from post-consumer scrap carries an obligation of approximately €0.09 to €0.19 per tonne, reflecting its near-zero direct process emissions.

"The long-term trajectory is more significant still. As EU ETS free allocations are phased out and carbon prices rise, consensus projections suggest the cumulative CBAM cost advantage for secondary aluminium over primary could exceed €200 per tonne by 2035, representing a structural margin shift that compounds with every year of regulatory tightening."

The Scrap Loophole: A Contested Regulatory Fault Line

Post-Consumer vs. Pre-Consumer Scrap Under CBAM

One of the most consequential and least widely understood aspects of CBAM's current design is how it treats different categories of aluminium scrap. The distinction is not merely technical; it has direct implications for import strategy and competitive positioning.

Post-consumer scrap, derived from end-of-life products including used beverage cans, automotive components, and construction demolition material, is currently zero-rated under CBAM. This classification holds regardless of where the remelting occurs or what energy source powers it. The embedded carbon burden is treated as negligible.

Pre-consumer scrap, comprising manufacturing offcuts and production process waste, occupies a different and more contested regulatory position. The European Commission has flagged this category as a candidate for inclusion in future CBAM revisions, with proposals aimed at closing what critics characterise as a structural loophole enabling non-EU producers to circumvent carbon obligations through scrap classification. For a detailed breakdown of how CBAM applies specifically to aluminium sectors, industry participants should review the current regulatory scope closely.

The competitive distortion this creates is material:

- Non-EU producers remelting scrap can import into Europe under a zero-emissions classification, carrying no CBAM certificate obligation

- EU-based remelters face carbon costs through the EU Emissions Trading System on their own domestic operations

- The estimated competitive disadvantage for EU recyclers relative to non-EU remelters importing zero-rated remelted scrap is projected at over €200 per tonne by 2035 if the pre-consumer scrap loophole remains unaddressed

Regulatory Watch: As of mid-2026, the European Commission has proposed bringing pre-consumer scrap-derived secondary aluminium within CBAM scope, but post-consumer scrap remains explicitly excluded. Procurement teams and remelters should treat this as a live regulatory risk requiring active monitoring, as any reclassification would materially alter import cost structures for affected product categories.

When Secondary Stops Being Cheap: The Scrap Price Paradox

The Collapse of the Traditional Cost Arbitrage

A foundational assumption underpinning secondary aluminium economics for generations was that scrap commanded a significant discount to primary ingot. That discount justified the entire business model of the independent remelter. However, the discount has now largely disappeared.

Industry data indicates that aluminium scrap now frequently trades at more than 90 percent of the LME primary ingot price. The Federation of European Secondary Aluminium Producers has noted this convergence as a defining challenge for European remelters, whose margins depended on buying scrap well below ingot parity and selling the remelt output at or near primary prices.

This creates a genuine strategic paradox. Secondary aluminium retains its carbon cost advantage under CBAM. Its direct emission factor remains approximately 15 times lower than primary production. But its raw material cost advantage has been structurally eroded. The procurement logic must therefore shift entirely:

| Traditional Procurement Logic | Emerging Procurement Logic (Post-CBAM) |

|---|---|

| Scrap is cheap; maximise volume purchase | Scrap is carbon-advantaged; price in CBAM savings |

| Primary ingot is the quality benchmark | Verified low-carbon secondary commands a green premium |

| Energy cost is the primary operating variable | Carbon liability is the primary regulatory variable |

| Scrap discount to LME drives margin | CBAM certificate avoidance drives margin |

| Secondary production is cost arbitrage | Secondary production is carbon arbitrage |

Why Scrap Prices Are Structurally High

Several reinforcing dynamics explain why the scrap price compression is unlikely to reverse:

- Scrap leakage to non-EU markets has tightened European supply, as buyers in Asia and the Middle East compete aggressively for available post-consumer material

- CBAM-driven demand intensification within Europe has increased competition among EU remelters for zero-rated feedstock

- Structural undersupply relative to collection potential means scrap volumes remain constrained well below theoretical maximum recovery rates

- Competition from primary producers pursuing secondary integration as a carbon risk management strategy has added a new category of buyer to an already tight market

The Dirty Alloy Problem: Technology Closing the Quality Gap

Why Alloy Contamination Has Historically Limited Secondary Substitution

Secondary aluminium has long carried a technical limitation that constrained its substitutability with primary metal in high-specification applications. Mixed scrap streams accumulate tramp elements, including iron, copper, zinc, and silicon, through co-mingling of different alloy families during collection and processing. These contaminants degrade mechanical properties and restrict end-use eligibility, particularly in aerospace, automotive structural, and high-strength applications.

Historically, the solution was dilution with primary metal, blending clean virgin aluminium into the remelt to bring tramp element concentrations within specification. This dilution requirement imposed a ceiling on secondary content in demanding applications and created a structural dependency on primary metal that limited the carbon advantage secondary producers could claim. In addition, the rising significance of secondary aluminium as a strategic input is increasingly acknowledged across global supply chain frameworks.

Two Technological Pathways Removing the Contamination Barrier

Two converging technological developments are progressively dismantling this constraint:

- Advanced Photonic Sorting Systems: Laser-induced breakdown spectroscopy (LIBS) and hyperspectral imaging technologies now enable alloy-grade separation at industrial throughput rates. Rather than processing all inputs as undifferentiated mixed metal, operators can segregate scrap streams by precise elemental composition, maintaining alloy family integrity from collection through remelting. This eliminates the contamination that previously made dilution unavoidable.

- Design for Recycling (DfR) Frameworks: Upstream product design standards specifying alloy-compatible architectures, particularly in automotive and aerospace manufacturing, reduce contamination burden at end-of-life by ensuring that components within a single product family use compatible alloy compositions. When a vehicle designed under DfR principles reaches end-of-life, the aluminium content can be recovered without the cross-alloy contamination that historically degraded post-consumer scrap quality.

As photonic sorting scale and DfR adoption accelerates across major manufacturing sectors, the technical case for primary dilution weakens substantially. Secondary producers investing in sorting infrastructure today are positioning to capture the full margin growth embedded in the green premium without carrying the carbon liability of primary metal blending.

The next major ASX story will hit our subscribers first

The Global Production Balance and Where It Is Heading

Current Market Structure

Secondary recycled aluminium accounted for approximately 35 percent of global aluminium production in 2025, with primary smelting representing the remaining 65 percent. However, the marginal dynamics of the market are increasingly shaped by scrap availability, processing sophistication, and carbon regulation rather than smelter capacity expansion.

Key structural observations for investors and procurement strategists:

- Global scrap collection rates remain significantly below theoretical maximum recovery potential, creating both a supply constraint and a long-term investment opportunity in collection infrastructure

- The competitive advantage in aluminium is migrating from ore access and electricity pricing toward scrap procurement networks, quality sorting technology, and alloy management capability

- Regions with advanced recycling infrastructure, particularly Western Europe and North America, are positioned to capture disproportionate value as CBAM costs escalate and the green premium widens

- The carbon intensity of the electricity grid powering primary smelters remains a secondary CBAM factor that, while excluded from direct calculations, influences the long-term competitiveness of different smelting jurisdictions under broader decarbonisation frameworks

Strategic Implications Across the Value Chain

A Framework for Different Industry Participants

For EU Importers and Downstream Manufacturers:

- Restructure procurement frameworks to explicitly price CBAM avoidance value into secondary aluminium sourcing decisions

- Develop supplier verification systems capable of documenting embedded emissions for accurate CBAM certificate calculations

- Monitor pre-consumer scrap reclassification proposals closely, as any change would alter the cost structure of current zero-rated import strategies

- Begin building commercial relationships with verified low-carbon secondary producers before the green premium fully prices into the market

For Secondary Producers and Remelters:

- Invest in alloy-grade photonic sorting capability to expand the addressable application range for secondary metal

- Develop commercial frameworks that translate CBAM cost avoidance into explicit green premium pricing, capturing the carbon arbitrage as margin rather than passing it to buyers

- Engage proactively with EU policy processes on the scrap loophole debate to protect the competitive position of post-consumer recycling operations

For Primary Producers and Smelters:

- Accelerate renewable energy transition to reduce direct emission factors and lower CBAM certificate obligations

- Evaluate strategic integration into secondary processing as a portfolio approach to carbon risk diversification

- Invest in carbon accounting documentation infrastructure capable of verifying actual emission factors below EU benchmark levels, potentially reducing certificate costs for demonstrably cleaner operations

For instance, top aluminium companies are already restructuring capital allocation priorities to reflect these emerging carbon cost realities. Similarly, large-scale renewable energy transitions such as those underway at Gladstone aluminium operations demonstrate how primary producers are responding to escalating carbon obligations.

Primary vs. Secondary Aluminium Under CBAM: The Full Comparison

| Decision Variable | Primary Aluminium | Secondary Aluminium (Post-Consumer) |

|---|---|---|

| CBAM Emission Factor (2026) | ~1.423 tCO₂/t | ~0.091 tCO₂/t |

| Real-World Direct Emissions | ~1.5 tCO₂/t | ~0.05–0.10 tCO₂/t |

| Estimated CBAM Cost (2026) | ~€1.82–3.64/t | ~€0.09–0.19/t |

| Long-Term CBAM Cost (2035) | Significantly escalating | Structurally low |

| Energy Intensity | ~14,000 kWh/t | ~500–700 kWh/t |

| Raw Material Cost Trend | Stable to rising | Rising (scrap now >90% of LME) |

| Green Premium Eligibility | Limited without renewables | High, near-zero carbon burden |

| Alloy Quality Ceiling | Unrestricted (virgin composition) | Improving with sorting technology |

| Regulatory Risk | High (CBAM escalation, ETS tightening) | Low-to-moderate (loophole review risk) |

| Strategic Procurement Value | Declining under carbon pricing | Increasing as carbon costs compound |

Key Questions Answered

Does CBAM Apply to All Aluminium Imports?

CBAM applies to aluminium products imported into the EU based on their direct embedded emissions. Primary aluminium carries significant CBAM liability due to electrolytic smelting process emissions. Secondary aluminium derived from post-consumer scrap is currently zero-rated, though the regulatory status of pre-consumer scrap remains under active review. The evolving relationship between primary vs secondary aluminium scrap and CBAM is therefore central to any EU import strategy.

Why Has the Scrap Discount to Primary Collapsed?

Structural tightening of European scrap supply, intensified demand from CBAM-aware remelters, and competition from non-EU buyers have collectively pushed aluminium scrap prices to above 90 percent of LME primary ingot levels. This eliminates the traditional raw material cost arbitrage and reorients secondary production economics around carbon liability avoidance rather than input cost savings.

What Is the Green Premium and How Is It Measured?

The green premium in aluminium markets refers to the price differential that verified low-carbon secondary metal commands over standard primary ingot, driven by CBAM certificate cost avoidance, corporate sustainability commitments, and downstream customer decarbonisation requirements. Broader patterns in green metals pricing across steel and aluminium sectors suggest this premium will widen materially as regulatory frameworks tighten. As CBAM certificate prices escalate from their Q1 2026 benchmark of €75.36 per tonne of CO₂, the green premium embedded in secondary aluminium is expected to compound accordingly.

Disclaimer: Forward-looking statements regarding CBAM certificate prices, green premium trajectories, and long-term cost projections are based on current regulatory frameworks and market consensus estimates. Actual outcomes will depend on EU policy evolution, EU ETS price developments, scrap supply dynamics, and technological adoption rates. This analysis does not constitute financial or investment advice.

The Structural Verdict

The aluminium industry is not experiencing a temporary cost dislocation. It is undergoing a permanent structural realignment driven by the intersection of carbon regulation, thermodynamic reality, and scrap market dynamics. The core conclusions for any serious market participant are clear:

- Carbon liability has replaced energy cost as the primary regulatory differentiator between primary and secondary aluminium economics in the EU market

- Secondary post-consumer scrap carries near-zero CBAM exposure relative to primary aluminium, and that advantage compounds as carbon prices rise

- The traditional scrap discount to primary has largely collapsed, requiring a fundamental reframing of secondary aluminium as a carbon-advantaged strategic asset rather than a low-cost commodity input

- Photonic sorting and Design for Recycling frameworks are progressively closing the alloy quality gap that previously limited secondary substitution in high-specification applications

- The pre-consumer scrap loophole remains the most significant near-term regulatory risk for current zero-rated import strategies

Organisations that restructure their procurement, processing, and commercial frameworks around carbon advantage rather than commodity price arbitrage are positioned to capture the margin growth embedded in the primary vs secondary aluminium scrap and CBAM transition. Those operating on pre-2023 assumptions will, consequently, absorb an escalating and largely avoidable carbon cost burden as the regulatory framework reaches full maturity.

Want to Stay Ahead of the Next Major Shift in Metals and Mining Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity and market data into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the market.