May 20, 2026

The Strategic Imperative for Processing Infrastructure Development Outside China

Battery material supply chains have reached an inflection point where geographic concentration poses systemic risks to global energy transition objectives. The NextSource Abu Dhabi graphite processing facility represents a pivotal development in addressing China's dominant position in critical minerals energy transition, particularly for graphite anode materials. Furthermore, this has created vulnerabilities that Western governments and automotive manufacturers are actively seeking to address through strategic diversification initiatives.

The development of alternative processing capabilities represents more than a simple supply chain optimisation exercise. It fundamentally challenges the economic assumptions underlying decades of specialised manufacturing concentration and requires sophisticated understanding of industrial infrastructure development, technology transfer dynamics, and market positioning strategies.

Understanding China's Processing Dominance and Market Dynamics

China controls approximately 90% of global graphite processing capacity, extending from raw flake graphite refinement through battery-grade anode material production. This concentration emerged through decades of industrial policy coordination, environmental regulation arbitrage, and technology development investments. Consequently, this created substantial barriers to entry for alternative processing locations.

The processing stages involve complex chemical and mechanical treatments including micronisation (particle size reduction to specific distributions), spheronisation (forming spherical particles for optimal battery performance), and coating applications. These processes enhance electrochemical properties and require specialised equipment, technical expertise, and quality control systems refined over decades within China's expansion strategy industrial ecosystem.

NextSource's Abu Dhabi facility represents a significant departure from traditional approaches by leveraging existing industrial infrastructure. This approach contrasts sharply with pursuing greenfield development, whilst understanding permitting process insights becomes crucial. The Industrial City of Abu Dhabi provides pre-permitted industrial zones that eliminate many regulatory hurdles.

Abu Dhabi's Industrial Infrastructure Advantages for Battery Materials Processing

The UAE's positioning as a Middle East industrial hub creates unique advantages for graphite processing operations. The Industrial City of Abu Dhabi offers established warehouse facilities that can be converted for specialised processing equipment installation. This significantly reduces capital expenditure requirements compared to greenfield construction projects.

The regulatory framework allows for post-construction permitting for what authorities term civil defence permits. This contrasts sharply with traditional jurisdictions requiring comprehensive pre-construction approvals. However, this regulatory efficiency could compress project delivery timelines substantially, providing competitive advantages in rapidly evolving battery material markets.

Port access and logistics infrastructure connect directly to global shipping routes, enabling cost-effective feedstock importation and finished product distribution. The existing industrial workforce and chemical processing ecosystem reduce operational risk compared to locations requiring comprehensive capability development.

When big ASX news breaks, our subscribers know first

NextSource's Vertical Integration Strategy for Market Positioning

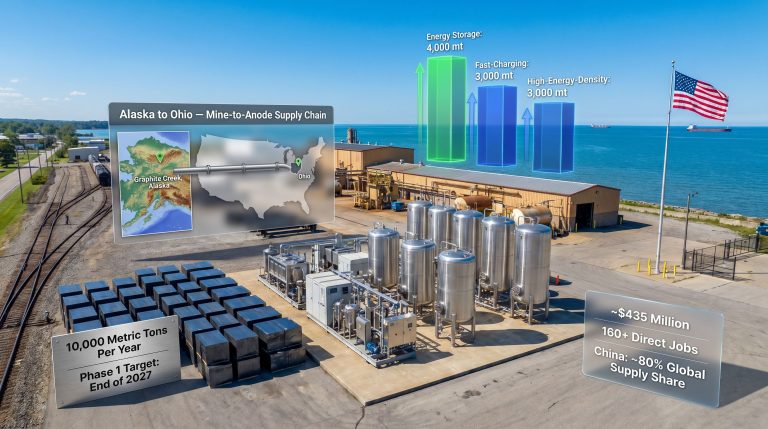

The company's approach integrates upstream mining operations at the Molo project in Madagascar with midstream processing in Abu Dhabi. This creates supply chain control that addresses feedstock security concerns while enabling quality standardisation throughout production stages.

From Madagascar Flake Graphite to Battery-Ready Anode Materials

The Molo mine produces high-purity flake graphite with specifications optimised for battery anode material applications. The feedstock characteristics include carbon content exceeding 95% and flake size distributions that facilitate downstream processing efficiency. In addition, this integration eliminates third-party supplier dependencies that could compromise production scheduling or quality consistency.

However, NextSource's strategy incorporates third-party feedstock testing capabilities to ensure operational flexibility and risk mitigation. This approach enables production scaling that exceeds single-mine capacity limitations whilst providing supply security during potential operational disruptions.

The processing technology involves proprietary methods for particle size optimisation and surface treatment applications. These meet automotive industry quality standards and major battery manufacturers, including Mitsubishi Chemical, require consistent particle morphology, purity specifications, and electrochemical performance characteristics.

Production Capacity and Phased Development Economics

Phase 1 development targets 14,000 tonnes annual production capacity with 9,000 tonnes secured through Mitsubishi Chemical's multi-year offtake agreement. The remaining 5,000 tonnes provides flexibility for additional customer relationships and spot market opportunities.

The 60,000 square metre facility footprint accommodates Phase 2 expansion of 16,000 tonnes additional capacity. Furthermore, this expansion requires no new land acquisition or major infrastructure development. This scalability addresses market growth projections whilst maintaining capital efficiency during initial operations.

Production economics benefit from the warehouse conversion approach, which reduces construction timelines and capital requirements. For instance, this compares favourably to purpose-built facilities, whilst the phased development model allows capacity expansion aligned with market demand growth.

Economic Positioning Compared to Traditional Processing Hubs

Cost structure analysis reveals several competitive advantages for Abu Dhabi operations compared to alternative processing locations. This becomes particularly evident when considering total project delivery timelines and operational flexibility.

Infrastructure and Regulatory Cost Advantages

| Cost Factor | Abu Dhabi Advantage | Traditional Locations | Impact Assessment |

|---|---|---|---|

| Permitting Timeline | Pre-approved industrial zones | 12-24 months regulatory approval | Significant timeline compression |

| Infrastructure Access | Existing warehouse conversion | Greenfield construction required | Reduced capital expenditure |

| Logistics Costs | Direct port access, global shipping | Multi-modal transport dependencies | Lower distribution costs |

| Labor Availability | Established industrial workforce | Variable skill availability | Reduced recruitment risk |

The pre-permitted status eliminates regulatory uncertainty that has delayed comparable projects in other jurisdictions. Traditional processing facility development requires extensive environmental impact assessments, zoning approvals, and construction permits that extend project timelines substantially.

Warehouse conversion costs represent a fraction of greenfield construction expenses. This becomes particularly significant when considering specialised equipment installation requirements and environmental control systems necessary for battery material processing.

Production Economics and Market Positioning

Labour costs in the UAE industrial sector provide competitive advantages compared to Western processing locations whilst maintaining quality standards. However, the established chemical processing ecosystem reduces training requirements and operational risk during facility commissioning.

Utility infrastructure and industrial support services availability eliminate development costs associated with power generation and water treatment. Consequently, waste management systems that greenfield projects must establish independently become unnecessary.

The 2026 production timeline targets capitalise on growing demand for non-Chinese sourced battery materials. Moreover, major automotive manufacturers implement supply chain diversification strategies incorporating critical minerals strategy considerations.

Market Positioning for Non-Chinese Graphite Processing Leadership

NextSource Abu Dhabi graphite processing facility development occurs within broader industry trends toward supply chain resilience. Furthermore, geographic diversification driven by geopolitical considerations and automotive industry risk management strategies becomes increasingly important.

First-Mover Advantages in Alternative Processing Capacity

The facility represents among the first major non-Chinese graphite processing operations specifically designed for battery anode material production. This positioning provides significant customer relationship development opportunities as Western automotive manufacturers seek qualified alternative suppliers.

Japanese and European battery manufacturers have indicated willingness to pay premium pricing for supply chain diversification. This creates market opportunities beyond traditional cost-based competition, whilst the Mitsubishi Chemical partnership validates technology capabilities and provides reference customer credibility.

Market share redistribution scenarios suggest potential for 5-10% reduction in Chinese processing dependency through successful alternative processing facility development. For instance, NextSource's facility capacity, when combined with other announced projects, could catalyse broader industry transition toward geographic diversification.

Strategic Customer Development and Regional Market Expansion

The Abu Dhabi location provides access to Middle East industrial markets requiring graphite-based products beyond battery applications. Industries including refractories, oil and gas operations, and steel production utilise graphite materials. Consequently, this creates revenue diversification opportunities through by-product sales.

Advanced discussions for additional offtake agreements encompass both remaining Phase 1 capacity and Phase 2 expansion potential. Customer development strategies target European battery manufacturers implementing supply chain resilience initiatives and Asian companies establishing manufacturing operations outside China.

The facility's positioning enables flexible customer relationship development rather than dependence on single-market concentration. However, this reduces commercial risk whilst maximising revenue optimisation opportunities, similar to the European supply facility approach.

Global Supply Chain Transformation Implications

NextSource Abu Dhabi graphite processing facility development represents a significant milestone in critical mineral processing diversification efforts. Furthermore, these extend beyond immediate commercial objectives to influence broader industry development patterns.

Catalyst Effects for Additional Processing Investment

Successful facility development and operations could demonstrate economic viability for alternative processing locations. This potentially encourages additional investment in non-Chinese processing capacity, whilst this catalyst effect addresses current market concentration through competitive alternative development.

Technology transfer validation through automotive industry partnerships establishes precedents for intellectual property protection. Moreover, operational excellence outside traditional processing hubs becomes achievable, whilst these precedents reduce perceived risks for additional processing facility development.

Market acceptance of non-Chinese processed materials creates demand certainty that supports financing and development of comparable projects. Customer willingness to pay premium pricing for supply chain diversification validates business models supporting alternative processing development.

Risk Assessment and Strategic Mitigation Factors

Geopolitical stability considerations favour Middle East processing operations compared to locations experiencing political uncertainty or regulatory instability. The UAE's established international business relationships and legal framework provide operational security for long-term industrial development.

Technology protection measures address intellectual property concerns whilst enabling knowledge transfer necessary for operational excellence. Feedstock supply security through Madagascar operations reduces dependency on third-party sources whilst maintaining flexibility for capacity expansion.

Timeline execution risk appears limited given existing infrastructure availability and regulatory pre-approval status. Construction timeline advantages provide competitive positioning during market development phases when customer relationship establishment offers maximum strategic value.

Investment Strategy Implications for Battery Material Processing

The NextSource Abu Dhabi graphite processing facility development illustrates evolving investment approaches prioritising infrastructure utilisation. Furthermore, market positioning takes precedence over traditional resource development models.

Capital Efficiency Through Infrastructure Conversion

Investment thesis validation centres on capital efficiency achieved through existing facility conversion rather than greenfield construction. This approach reduces capital requirements whilst accelerating cash flow generation through shortened development timelines.

Revenue visibility through secured offtake agreements provides financing certainty and risk mitigation compared to speculative capacity development. The Mitsubishi Chemical partnership establishes baseline economics whilst additional customer relationships offer upside potential.

Scalability advantages enable capacity expansion aligned with market demand growth rather than anticipatory overbuilding. Phased development reduces execution risk whilst maintaining strategic positioning for market share capture during industry transition phases.

Market Timing and Execution Considerations

The 2026 production timeline positions the facility to capitalise on accelerating demand for alternative processing capacity. Moreover, automotive manufacturers implement supply chain diversification strategies, whilst NextSource's strategic approach represents engineering completion and funding closure critical milestones.

Market dynamics favour early market entry with qualified processing capability over delayed entry. However, potentially superior technology or cost structure becomes secondary considerations, whilst customer relationship development and reference case establishment provide competitive advantages.

Successful execution could establish NextSource as a preferred alternative supplier for Western automotive supply chains. Consequently, this creates strategic value beyond immediate processing economics.

The next major ASX story will hit our subscribers first

Critical Success Factors and Strategic Monitoring Points

Several key factors will determine whether NextSource Abu Dhabi graphite processing facility achieves strategic objectives. Furthermore, these influence broader industry development patterns toward geographic diversification.

Engineering Completion and Funding Closure Milestones

Engineering design completion provides essential validation for production capacity targets, operational cost projections, and capital expenditure requirements. This technical validation supports financing discussions and customer relationship advancement.

Funding closure within projected timelines enables construction commencement aligned with 2026 production targets. Delays in financing could compromise market timing advantages and customer development opportunities.

The combination of engineering validation and financing completion establishes project execution credibility. This supports additional customer relationship development beyond current offtake commitments.

Production Ramp-Up and Quality Achievement

Operational excellence during production ramp-up phases determines long-term customer relationships and market positioning sustainability. Quality consistency meeting automotive industry standards requires sophisticated process control and continuous improvement capabilities.

Customer acceptance testing and qualification processes validate technology performance and establish reference case credibility. Successful qualification enables market expansion beyond initial customer commitments, whilst production cost achievement validates economic projections.

This supports pricing competitiveness during market development phases when alternative suppliers compete for customer relationships.

Long-Term Market Evolution and Strategic Positioning

NextSource Abu Dhabi graphite processing facility represents more than an isolated processing project. It embodies a strategic approach to critical mineral supply chain development that could influence global industry structure evolution.

Model for Critical Mineral Processing Diversification

Successful facility development demonstrates economic viability for alternative processing locations utilising existing industrial infrastructure. This model reduces barriers to entry for additional processing facility development rather than greenfield development.

Technology transfer validation establishes precedents for intellectual property protection and operational excellence outside traditional processing hubs. These precedents encourage additional investment in alternative processing capacity development.

Regional processing hub development integrates Middle East industrial capacity into global clean energy supply chains. This creates geographic diversification that enhances supply chain resilience whilst supporting regional economic development objectives.

The NextSource Abu Dhabi graphite processing facility development represents a strategic milestone in critical mineral supply chain evolution. Furthermore, it demonstrates practical approaches to geographic diversification whilst establishing competitive positioning in rapidly evolving battery material markets. Success factors centre on execution excellence, market timing, and customer relationship development that extends beyond immediate commercial objectives.

Disclaimer: This analysis contains forward-looking statements and projections that involve inherent risks and uncertainties. Actual results may differ materially from those projected. Investment decisions should be based on comprehensive due diligence and professional financial advice.

Looking to Capitalise on Critical Mineral Processing Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in critical minerals and battery materials companies ahead of the broader market. Explore Discovery Alert's dedicated discoveries page to understand why historic discoveries can generate substantial returns, and begin your 30-day free trial today to position yourself ahead of the market.