July 10, 2026

Why the Global Helium Supply Chain Is Closer to Breaking Point Than Most Investors Realise

The industries that underpin modern civilisation rarely advertise their vulnerabilities until those vulnerabilities become crises. Semiconductor fabrication, MRI technology, quantum computing, and space launch systems share a common dependency that receives almost no mainstream attention: helium. The Pulsar Helium Topaz project in Minnesota has emerged against precisely this backdrop, representing a rare primary helium discovery in a market that is structurally running out of options. Not the kind that fills party balloons, which accounts for barely one to two percent of total consumption, but industrial helium operating at temperatures just fractionally above absolute zero, doing work that no substitute can replicate.

What makes the current moment genuinely unusual is that the structural fragility of the global helium supply crisis, long understood by industry insiders, has moved from a theoretical concern to an active reality. Roughly 45% of the world's helium supply is simultaneously offline or restricted, a convergence of geopolitical and infrastructure failures that the market has no mechanism to quickly reverse.

When big ASX news breaks, our subscribers know first

The Byproduct Trap: Why Helium Supply Cannot Simply Scale Up

To understand why the current shortage is so difficult to resolve, it helps to understand how the vast majority of helium reaches the market in the first place.

More than 95% of global helium production is extracted as a byproduct of natural gas liquefaction. This means helium output is not governed by helium demand. It is governed by decisions made by hydrocarbon producers based on energy economics, pipeline commitments, and LNG pricing. When a semiconductor manufacturer needs more helium, there is no upstream lever available to pull. The supply system structurally cannot respond.

End users are locked into long-term take-or-pay contracts that offer minimal flexibility. Growth industries requiring increased helium volumes have nowhere to go when demand outpaces allocated supply. This rigidity was always an inherent weakness in the system. Recent geopolitical events have simply made that weakness impossible to ignore.

The Simultaneous Shock: What Is Actually Offline Right Now?

| Supply Source | Estimated Global Share | Status as of 2025 |

|---|---|---|

| Qatar (QatarEnergy LNG) | ~35% | Production facility damaged; Strait of Hormuz closed |

| United States | ~20% | Domestic allocations reportedly diverted toward Asian markets |

| Russia | ~10% | Export controls imposed |

| Combined offline or restricted | ~45% | Active supply deficit conditions |

The Qatar situation is particularly significant. The QatarEnergy LNG facility, which processes the natural gas from which Qatar's helium is extracted, sustained damage during the conflict in the Middle East. The facility's leadership has indicated a recovery timeline of three to five years to restore full operational capacity. This is not a short-term supply blip. It represents a medium-term structural deficit with no rapid resolution pathway.

Compounding this, US helium customers have already been experiencing the downstream effects. Some buyers have reportedly been receiving only 50% of their typical allocation volumes whilst simultaneously paying premiums for that reduced supply. A significant portion of US-origin helium output appears to be moving toward Asian semiconductor markets in Taiwan, South Korea, and Japan, leaving domestic customers underserved.

When nearly half of the world's helium supply is simultaneously constrained, the market is not experiencing a temporary disruption. It is revealing the complete absence of any meaningful supply redundancy built into the system.

What the Pulsar Helium Topaz Project in Minnesota Actually Is

Against this backdrop, the Pulsar Helium Topaz project in Minnesota represents something the global helium market has rarely encountered: a high-grade, primary helium discovery with no dependency on natural gas production whatsoever.

Located in Lake County, northern Minnesota, near the town of Babbitt, Topaz sits in a region with no prior hydrocarbon production history. This is not coincidental. Helium and natural gas do not always share the same geological origins. They can co-mingle, but they can also occur entirely independently. The Topaz area has no meaningful hydrocarbon potential, but it sits directly adjacent to the source rock responsible for helium generation, which the company describes as an optimal proximity zone for high-concentration helium accumulation.

The discovery itself was entirely accidental. Exploration drilling targeting nickel and copper mineralisation unexpectedly intersected a pressurised gas pocket. When that gas was tested, it registered at one of the highest helium concentrations ever recorded in a single discovery well, with initial readings between 10% and 12% helium. The event triggered the founding of Pulsar Helium and the subsequent consolidation of the surrounding land position.

Why Grade Matters More Than Volume in Helium Economics

The distinction between a primary helium project and a byproduct helium operation is not merely semantic. It is the fundamental economic difference between a project whose viability stands alone and one whose viability is tied to someone else's production decisions.

Furthermore, consider the grade comparison:

- Qatar helium concentration from LNG processing: approximately 0.04%

- Industry accepted high-grade threshold: approximately 2%

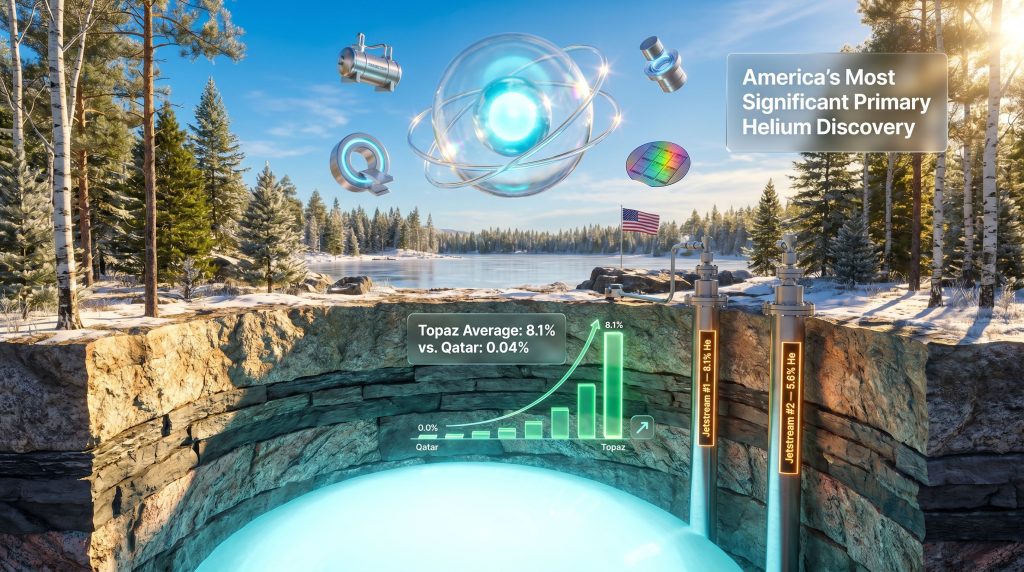

- Topaz well average across all drilled wells: 8.1%

- Original discovery well concentration: 10% to 12%

- Jetstream #1 confirmed grade: 8.1%

- Jetstream #2 confirmed grade: 5.6%

- A separate helium occurrence 100 miles to the south: 2% (still considered high-grade by industry standards)

Qatar's 0.04% concentration becomes economically meaningful only because of the enormous volumes of natural gas being processed. At Topaz, helium is the primary economic driver at every concentration recorded across the drill program. The project requires no hydrocarbon rationale to justify its existence.

Why Helium Demand Is Structurally Set to Double by 2035

Projections from multiple independent sources point toward helium demand doubling by 2035, driven not by one sector but by a convergence of technology dependencies that are each accelerating simultaneously.

The Applications That Cannot Substitute Away From Helium

Semiconductor fabrication is the single largest application globally. Helium's inert, non-reactive properties and its capacity to maintain near-absolute-zero temperatures make it an essential process gas in chip manufacturing environments. As data centre buildout, artificial intelligence infrastructure, and consumer electronics production all accelerate, each adds incremental helium consumption pressure to an already constrained supply system.

Beyond semiconductors, the critical applications include:

- Space launch systems: Helium serves as both a pressurising agent and a leak detection medium in rocket propulsion. Usage scales with launch frequency, which is rising globally.

- MRI and medical imaging: Liquid helium maintains the superconducting state of MRI magnets. No commercially viable substitute currently exists. Replacing liquid helium cooling in installed MRI infrastructure is not a practical near-term option.

- Quantum computing: Helium enables ultra-low temperature operating environments required for quantum processor function. The race for quantum computing supremacy between nations is, at its foundation, a race for helium access.

Helium's physical properties, being inert, non-flammable, and non-hazardous, make it the only gas suitable for many of these roles. Its liquefaction point sits just fractionally above absolute zero, making it the coldest non-solid liquid substance available. That physical reality is not something any policy decision or materials science breakthrough can easily bypass.

The Domestic Supply Advantage: Why Helium Does Not Travel Well

An underappreciated dimension of the Topaz project's strategic positioning involves helium's physical behaviour during transport. In addition, this factor sets domestic primary sources apart from imported supply in ways that are often overlooked.

Helium holds the distinction of being the second-smallest atom on the periodic table. At this atomic scale, helium permeates most containment materials over time. Global bulk liquid helium is transported in specialised 40-foot cryogenic containers that represent a deliberate engineering compromise between vessel integrity and cargo volume. Over transport journeys exceeding approximately four weeks, measurable product loss through permeation becomes a real and quantifiable cost.

The United States is the world's single largest consumer of helium. A domestic primary source fundamentally changes the economics and reliability of supply for US end users. With a domestic reservoir, the containment clock does not start until the customer places an order. Extraction, containerisation, and delivery can be completed within days, eliminating the transit loss and supply chain risk inherent in importing helium from Qatar or other distant sources.

The Helium-3 Layer: A Discovery With Implications Beyond Conventional Energy

What Makes Helium-3 Exceptional and Exceptionally Rare

Helium-3 is a stable isotope of conventional helium, and its physical properties allow cooling to even lower temperatures than helium-4. This makes it relevant to the most advanced technology frontiers, including fusion energy reactors and quantum computing systems that require temperature environments beyond what helium-4 can achieve.

On Earth, helium-3 currently comes from only two sources:

- The radioactive decay of tritium within nuclear warhead maintenance programmes.

- Certain CANDU-type nuclear reactors.

No significant commercial terrestrial source has historically existed. The largest known concentration of helium-3 on or near Earth is on the surface of the Moon, a fact that has led the US Department of Energy to begin funding companies developing lunar resource extraction capabilities.

Topaz's Helium-3 Confirmation and Its Strategic Significance

Independent gas analysis conducted at the Topaz project, including verification by two US federal government laboratories, confirmed the presence of helium-3 within the Topaz gas stream. This represents one of the first significant terrestrial discoveries of helium-3 outside of nuclear programme byproducts.

The reference pricing for helium-3 sits at approximately $18.7 million per kilogram, though this figure reflects intra-government transfer pricing between US federal agencies rather than an open-market rate. No true commercial market for helium-3 exists yet, partly because no commercial-scale source has existed to create one.

Six known separation processes exist for extracting helium-3 from a mixed helium stream. None have been demonstrated at commercial scale. The company's stated approach is to establish helium-4 production first, with helium-3 treated as a high-value optionality layer rather than the core investment thesis.

Helium-3 is not the foundation of the Topaz investment case. It is a potential amplifier sitting on top of helium-4 economics that already stand independently. Even small quantities delivered to end users in quantum computing or fusion energy could materially alter project economics.

Drilling Results, Land Position, and Geological Derisking

What Seven Wells Across the Topaz Footprint Have Confirmed

The Topaz drilling programme to date has achieved a 100% success rate across all seven wells drilled, covering exploration steps to the east, west, and south of the original discovery location. Consequently, interpreting drill results across such a consistent dataset meaningfully reduces geological uncertainty for interpreting drill results at comparable primary helium projects.

Key outcomes include:

- Two production-ready wells (Jetstream #1 and #2) confirmed and drilled.

- Five appraisal and exploration wells subsequently drilled, each encountering high-pressure helium gas.

- Downhole logging and pressure testing confirm continuous reservoir geology across the expanded drill footprint.

- The resource remains open in all directions with no boundary yet defined.

The distinction between production-ready wells and exploration wells is operationally important. Exploration wells are narrower, uncased wells used purely for resource delineation. They cannot be directly connected to production infrastructure. The two production-ready wells drilled to date represent the foundation of any initial production scenario, with additional production-ready wells planned for the next drilling phase.

One practical consideration that highlights the project's value density: flow testing on exploration wells has been deliberately deferred to avoid venting high-concentration helium to atmosphere before a capture facility exists. At current market pricing, the cost of running unnecessary open-flow tests on exploration wells represents a meaningful dollar value released into the atmosphere with no commercial return.

Land Consolidation and the Michigan Expansion

Pulsar has acquired approximately 1,360 acres of surface land in the Topaz project area. Additional acquisitions have extended the broader regional footprint as the company moved to secure ground surrounding the discovery zone.

Beyond Minnesota, a new land package in Michigan has been secured where geological characteristics are described as analogous to the Minnesota setting, suggesting the regional helium system may extend across a wider geographic area than the current drill programme has tested.

The next major ASX story will hit our subscribers first

Minnesota's Regulatory Evolution: From Blank Slate to Production-Ready Framework

Minnesota had no prior history of gas production regulation when Pulsar began operating there in 2019. This created both a challenge and an opportunity. The company effectively pioneered the regulatory framework for a new industry within the state, engaging directly with legislators and demonstrating the non-hazardous, low-footprint nature of helium production.

The legislative outcome unfolded in two stages:

- In 2024, the State of Minnesota passed legislation formally classifying helium as a regulable resource.

- In 2025, the implementing regulations were formally enacted, providing the legal and operational certainty required to progress toward production.

This regulatory clarity is a material de-risking milestone. The absence of an applicable regulatory framework is a genuine barrier to project financing and development decision-making. Its resolution removes one of the most significant non-geological risks facing the project.

The Road to Production: Milestones, Partners, and Timeline

The 2025 to 2028 Development Pathway

| Milestone | Target Period |

|---|---|

| Additional production-ready wells (2 to 4) drilled | September 2025 |

| Independent resource assessment update | 2025 to 2026 |

| Pre-feasibility study and economic assessment | 2026 |

| Development decision | 2026 |

| Production commencement target | 2027 to early 2028 |

The September 2025 drilling programme is the critical near-term catalyst. Data from production-ready wells feeds directly into the production model in a way that data from exploration wells cannot. The distinction matters because facility design, economic modelling, and offtake discussions all depend on production well data rather than exploration well results. Mining feasibility studies for resource projects of comparable scale illustrate how significantly robust well data can de-risk the path to a development decision.

Chart Industries: Why the Engineering Partnership Signals Seriousness

Chart Industries, a NYSE-listed US industrial gas engineering company with a major fabrication facility in Minnesota, has been engaged to design the helium processing facility at Topaz. Work is already underway, with Chart analysing downhole gas composition data to engineer a processing facility matched specifically to Topaz's gas characteristics.

Every helium plant requires engineering customisation to the specific gas composition it will process. Chart's involvement at this early stage, before the resource assessment is finalised, reflects both the seriousness of the development pathway and the practical advantage of working with a Minnesota-based fabricator that eliminates complex logistics from the construction phase.

The broader principle here is deliberate: the entire value chain from resource assessment to facility engineering to operational delivery is being structured around US-based expertise and infrastructure, keeping supply chain risk within the domestic ecosystem. This approach stands in contrast to the complex international dependencies that characterise space resource extraction ventures, where supply chains span multiple jurisdictions and regulatory environments.

Key Risks and Considerations for Investors

The following section contains forward-looking analysis and should not be construed as financial advice. Investors should conduct their own due diligence and consider their individual risk tolerance before making any investment decisions.

What Remains Unresolved and Requires Monitoring

- Resource size: No resource boundary has been defined. The size of the Topaz reservoir remains open in all directions, with quantification dependent on the upcoming drilling programme and independent resource assessment.

- Helium-3 commercial pathway: Six separation processes exist but none have been demonstrated at commercial scale. The economics of helium-3 extraction, processing, and delivery remain to be established.

- Financing and offtake: Production development will require capital commitment and likely offtake agreements. The terms and timeline of those arrangements have not yet been disclosed.

- Timeline execution risk: The 2027 production target depends on drilling success, study outcomes, and regulatory processing proceeding without material delay.

- Price volatility: Whilst the current supply disruption environment is a near-term tailwind for project economics, helium pricing over the longer development horizon carries uncertainty.

Frequently Asked Questions: Pulsar Helium Topaz Project in Minnesota

What is the Topaz helium project?

Topaz is a primary helium discovery in northern Minnesota owned by Pulsar Helium Inc. It is characterised by exceptionally high helium concentrations, averaging 8.1% across all drilled wells, and is being developed as a standalone helium production asset with no dependence on natural gas production economics.

What helium grades has Topaz confirmed across its drill programme?

The confirmed grades to date are as follows: the original discovery well registered between 10% and 12% helium; Jetstream #1 confirmed at 8.1%; Jetstream #2 confirmed at 5.6%; and a separate occurrence 100 miles to the south registered at 2%, which is independently considered a high-grade result by industry standards.

When could Topaz begin producing helium?

The company is targeting a production start in 2027, with a development decision anticipated in 2026 following completion of the pre-feasibility study and independent resource assessment update.

What is helium-3 and why does its presence at Topaz matter?

Helium-3 is a rare stable isotope with applications in quantum computing and fusion energy research. Verified by two US federal laboratories, its confirmed presence at Topaz represents one of the only known significant terrestrial sources outside nuclear weapons maintenance programmes. Commercial extraction processes do not yet exist at scale, but the reference pricing of approximately $18.7 million per kilogram illustrates the potential economic significance even in small quantities.

Who is Chart Industries and what is their role at Topaz?

Chart Industries is a NYSE-listed US industrial gas engineering company with fabrication infrastructure in Minnesota. They have been engaged to design and engineer the helium processing facility at Topaz, with facility design work already underway based on Topaz's specific downhole gas composition data.

Does a spot market for helium currently exist?

No commercial spot market for helium currently exists. All supply moves through long-term take-or-pay contracts. A domestic primary source with sufficient scale could, for the first time in decades, introduce spot market flexibility and serve as a swing supplier to fill gaps when other US or global sources experience disruption.

Want to Stay Ahead of the Next Major Resource Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex resource data into actionable insights for investors at every level. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the market.