June 22, 2026

The Geography of Risk: Why One Waterway Holds the World's Energy System Hostage

Every energy supply chain has a point of maximum vulnerability. In the case of liquefied natural gas, that point is a strip of contested water just 21 nautical miles wide at its narrowest navigable channel. The Strait of Hormuz has long been described as the world's most critical energy chokepoint, but the events unfolding across June 2026 have shifted that description from analytical observation to lived commercial reality for utilities, shipping operators, and sovereign energy planners across three continents.

Understanding what is happening with Qatar LNG tankers in the Strait of Hormuz requires more than tracking vessel movements. It demands a clear-eyed examination of how a geopolitical conflict has fractured what was previously one of the most predictable supply chains in global energy markets, and what the structural consequences of that fracture are likely to be for years to come.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is Structurally Irreplaceable for LNG Markets

Approximately one-fifth of all globally traded LNG transits the Strait of Hormuz each year, with Qatar accounting for the dominant share of that volume. This concentration of supply through a single geographic passage creates what supply chain theorists call a single-point-of-failure dynamic, where the disruption of one node can cascade throughout an entire interconnected system.

What makes LNG categorically different from crude oil in this context is the near-impossibility of rapid supply rerouting. Unlike crude, which can be redirected across multiple pipeline networks and loading terminals, LNG requires purpose-built liquefaction facilities, specialised cryogenic vessels, and regasification infrastructure at the receiving end. The broader LNG supply outlook for 2025 and beyond had already flagged structural tightness before this disruption compounded existing pressures.

Long-term supply contracts add another layer of rigidity. When a Qatari LNG cargo contracted for delivery to a Japanese utility cannot exit the Gulf, that utility cannot simply source an equivalent volume from a different supplier at short notice. The infrastructure, the contractual obligations, and the vessel specifications all constrain flexibility in ways that crude oil logistics do not.

This physical and contractual inflexibility is precisely why partial disruptions to Hormuz transit create effects that are disproportionate to the volume of cargo actually blocked. Even limited interference with transit schedules propagates through spot pricing, utility procurement calendars, and national energy security planning across dozens of importing countries simultaneously.

From Ceasefire to Renewed Blockade: The Escalation Timeline

How Did the Current Disruption Begin?

The current disruption to Qatar LNG tankers in the Strait of Hormuz did not emerge suddenly. It is the product of a conflict that began on February 28, 2026, when US-Israeli military operations against Iran triggered an effective blockade of the waterway by Iran's Islamic Revolutionary Guard Corps. A ceasefire agreed between Washington and Tehran in April 2026 partially reopened the strait, and a 60-day extension of that agreement appeared to offer a window toward normalisation.

That window closed sharply when the IRGC declared the strait closed again over the weekend of June 21–22, 2026, citing Israeli military strikes in Lebanon as justification. The renewed declaration produced an immediate collapse in vessel traffic.

| Event | Date | Strait Status | Vessel Traffic |

|---|---|---|---|

| US-Israeli conflict with Iran begins | February 28, 2026 | Effectively closed | Near zero |

| US-Iran ceasefire agreed | April 2026 | Partially reopened | Limited |

| 60-day ceasefire extension | June 2026 | Reopened | Recovering |

| IRGC renewed closure declaration | June 21–22, 2026 | Contested | Sharply reduced |

| Four Qatari LNG tankers re-enter | June 23, 2026 | Contested | Selective commercial transit |

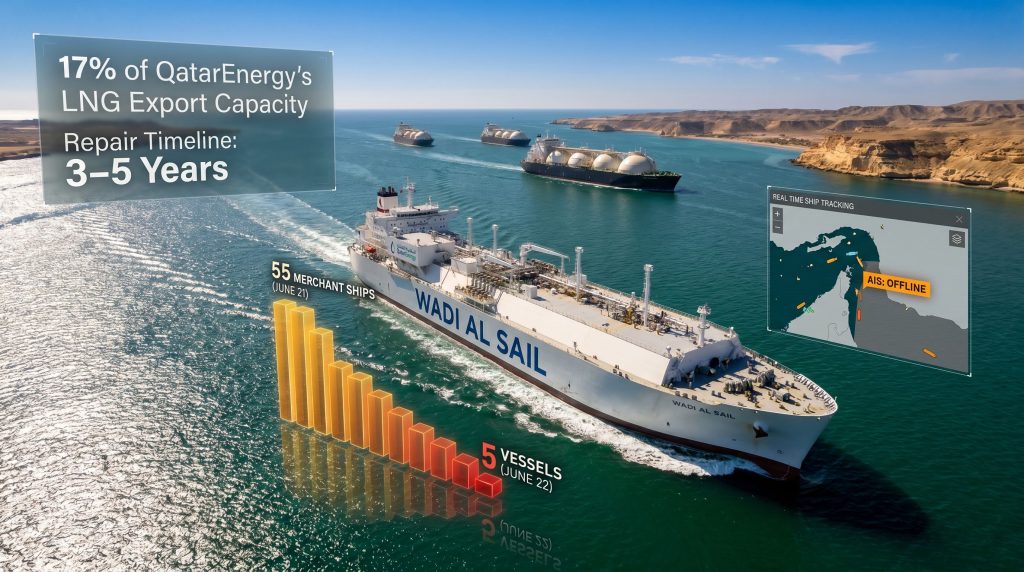

The data tells a stark story. Ship traffic dropped from 26 vessels on Saturday June 21 to just five on Sunday June 22, according to tracking data from analytics platform Kpler. The speed of that decline illustrates how quickly commercial operators respond to closure declarations, even when enforcement remains selective.

Four Vessels and What Their Transit Actually Signals

What Do the Latest Tanker Movements Reveal?

On June 23, 2026, four QatarEnergy-controlled LNG tankers entered the Strait of Hormuz via the Iranian route. The vessels, identified through ship-tracking data as the Wadi Al Sail, Mekaines, Al Sadd, and Mesaimeer, represented the first passage by Qatar LNG tankers in the Strait of Hormuz since the conflict began in late February. The Marshall Islands-flagged dry bulk vessel Summit Success also entered the Gulf on the same day, according to LSEG data.

These transits should not be interpreted as a restoration of normal commercial operations. They occurred against the backdrop of an active IRGC closure declaration, meaning passage was neither sanctioned nor guaranteed safe. The commercial determination to push cargo through a contested waterway reflects the enormous contractual and financial pressure that LNG suppliers face when supply obligations go unmet over extended periods.

Earlier transit attempts had not always succeeded. The tanker Al Daayen had previously approached the strait but reversed course following Iranian intervention, before subsequently completing a passage and being tracked heading eastward toward China. The pattern of approach, reversal, and eventual transit describes a commercial environment where every voyage is a calculated risk assessment rather than a routine shipping operation.

Dark Voyages: The Hidden Dimension of LNG Transit Under Conflict

Perhaps the most operationally significant development to emerge from the Hormuz disruption is the proliferation of what maritime analysts call dark voyages. A dark voyage occurs when a vessel deactivates its Automatic Identification System transponder, rendering it invisible to commercial ship-tracking platforms and, by extension, to the buyers, regulators, and market analysts who rely on AIS data for supply chain visibility.

Two ADNOC-controlled LNG tankers, the Al Hamra and the Mubaraz, had each completed two dark voyages out of Hormuz by June 23, 2026. Both vessels had disappeared from tracking systems between late May and early June before reappearing off the Indian coast with loaded cargoes. The Al Hamra was discharging at India's Ennore LNG terminal, while the Mubaraz was scheduled to offload at the Kochi terminal on June 23. ADNOC's stated position is that it does not comment on vessel positioning, movements, or routing as a matter of policy.

Why vessels go dark in contested waters involves a clear risk-transparency trade-off:

- AIS deactivation reduces the targeting risk of a vessel transiting a waterway where hostile military forces are operating

- Commercial buyers lose real-time visibility over their contracted cargo, creating pricing uncertainty and procurement scheduling disruptions

- Regulators and maritime law enforcement agencies face compliance questions that existing international maritime law frameworks were not designed to address in an active conflict scenario

- LNG importers relying on near-real-time supply tracking to manage storage levels and grid planning face a significant information gap

The normalisation of dark voyages as a risk management tool represents a structural shift in how the LNG shipping industry operates under geopolitical stress. It is one thing for sanctioned vessels carrying Iranian crude to deactivate transponders. It is a qualitatively different development when state-owned energy company tankers supplying contracted volumes to allied nations begin doing the same.

Oil and LNG Flows: What the Numbers Actually Reveal

Despite the IRGC's renewed closure declaration, significant volumes of hydrocarbons continued to move through the waterway in the days surrounding the announcement. US Central Command confirmed that 55 merchant ships transited the strait on Saturday June 21, collectively carrying more than 17 million barrels of oil destined for global markets.

Among the vessels tracked exiting the strait on that day were three Very Large Crude Carriers hauling crude from the UAE, Kuwait, and Iraq, alongside three product tankers. Three VLCCs carrying approximately 2 million barrels each of Saudi crude and fuel oil were also tracked, with at least one bound for Japan.

Hamid Bovard, head of the National Iranian Oil Company, stated through state television that more than 25 million barrels of Iranian oil had passed through the contested waterway since the Monday preceding the announcement. Three sanctioned VLCCs, identified as the Elva, Virgo, and Vigor, loaded from Kharg Island between late April and early May 2026, were tracked exiting the strait on June 23.

The continued movement of sanctioned Iranian vessels through a waterway that Iran itself has declared closed is among the more paradoxical aspects of the current situation. It reveals that the blockade functions less as a physical enforcement mechanism and more as a selective political instrument, applied asymmetrically depending on whose cargo is aboard.

The next major ASX story will hit our subscribers first

The Structural Damage to Qatar's LNG Export Capacity

Beyond the immediate logistics disruption, the conflict has inflicted lasting damage to Qatar's production infrastructure. Iranian strikes have destroyed an estimated 17% of QatarEnergy's LNG export capacity, with industry assessments projecting a repair timeline of three to five years. This is not a temporary outage that resolves when the geopolitical situation stabilises. It is a structural reduction in global LNG supply that will persist regardless of how quickly a diplomatic resolution emerges.

By early June 2026, a total of just nine loaded LNG carriers had exited the strait since the conflict began in late February, a figure that illustrates the severity of the volumetric reduction when set against Qatar's pre-conflict export pace, which made it consistently one of the world's top two LNG exporters.

How the Qatar disruption compares to historical LNG supply shocks:

| Disruption Event | Estimated Capacity Impact | Duration |

|---|---|---|

| 2022 Freeport LNG outage (US) | Approximately 17 million tonnes per year offline | Around 12 months |

| 2011 Fukushima nuclear incident | Structural demand surge across Japan | Multi-year |

| Qatar Hormuz conflict (2026) | 17% of QatarEnergy capacity damaged | 3–5 years estimated repair |

| Yemen Houthi Red Sea disruptions | Rerouting cost increases and delays | Ongoing |

The three-to-five-year repair horizon is particularly consequential because it bridges multiple LNG contracting cycles. Utilities and national gas companies that held long-term supply agreements with QatarEnergy must now navigate the spot market, pursue alternative supply agreements, or manage demand-side adjustments. Furthermore, alternative LNG supply additions are themselves constrained by project development lead times.

How Regional Producers and Importing Nations Are Adapting

The commercial response to the disruption has been rapid and, in some respects, inventive. Gulf producers ADNOC and Kuwait Petroleum Corporation have issued flexible loading tenders that allow buyers to take delivery of crude from either inside or outside the Strait of Hormuz. This preserves commercial relationships while acknowledging that routing certainty no longer exists. This dual-loading tender structure represents a meaningful innovation in how Gulf energy exporters manage logistics uncertainty.

Gulf producer response strategies at a glance:

| Producer | Primary Response | Flexibility Mechanism |

|---|---|---|

| QatarEnergy | Limited transits, no public commentary | Vessel-by-vessel routing decisions |

| ADNOC | Dark voyage transits confirmed, India deliveries | Dual-loading tender options |

| Kuwait Petroleum Corp | Flexible loading tenders issued | Inside and outside strait loading options |

| Saudi Aramco | VLCC transits continuing with Saudi crude | Standard commercial routing |

South Korean vessels resumed strait transits following the interim ceasefire, with Seoul's Ministry of Oceans and Fisheries confirming two passages without identifying the specific ships. Japanese-affiliated vessel exposure in the Gulf has declined materially, with the Japan Shipowners' Association reporting a reduction from 45 vessels at the conflict's outset to 37 by late June 2026, reflecting the ongoing risk aversion among major Asian shipping operators.

The oil market disruption stemming from Hormuz uncertainty has, moreover, compounded pressures already flagged in assessments of the broader geopolitical risk landscape for commodity markets. Consequently, this has accelerated conversations about supply chain resilience that were previously treated as medium-term strategic concerns.

Scenario Analysis: Three Possible Paths Through the Disruption

The trajectory of the Hormuz disruption is unlikely to resolve in a linear fashion. Three broad scenarios frame the range of outcomes for global LNG markets:

-

Negotiated Resolution: A durable diplomatic agreement between the United States and Iran restores full strait access within six to twelve months, allowing QatarEnergy to begin rebuilding export volumes as physical repair work progresses. Spot LNG pricing gradually normalises, though the three-to-five-year repair horizon keeps the structural supply shortfall in place regardless.

-

Managed Instability: Intermittent IRGC closure declarations continue to punctuate periods of commercial transit, making contested passage the operational baseline rather than the exception. Dark voyages, flexible loading tenders, and reduced vessel counts in the Gulf become normalised commercial tools. This scenario involves persistent spot market risk premiums and accelerated investment in non-Hormuz LNG supply.

-

Escalation: Further military action expands damage to Qatari or broader regional LNG infrastructure beyond the current 17% capacity loss, triggering a supply shock of a magnitude not seen since the 2022 European energy crisis. This scenario would materially accelerate LNG supply diversification investment in Australia, the United States, and East Africa, reshaping the global LNG supply map over the following decade.

The Long-Term Market Implications for Asian and European Importers

The countries bearing the greatest direct exposure to reduced Qatari LNG supply are those with the deepest long-term contracting relationships and the most geographically concentrated import portfolios. Japan, South Korea, China, and India collectively account for a substantial portion of Qatari LNG export volumes, with limited short-term ability to substitute equivalent volumes from alternative origins.

European nations that rapidly expanded LNG import infrastructure following Russia's curtailment of pipeline gas supplies in 2022 face a compounding risk profile. Having already pivoted away from one major supplier under crisis conditions, European utilities and grid operators now confront potential supply-side pressure from a second critical source, with fewer uncommitted LNG volumes available on the global spot market to fill the gap.

The broader consequences for resource and energy exports from alternative producing nations are already materialising, as importers accelerate efforts to diversify away from Hormuz-dependent supply. In addition, the oil price shock dynamics playing out across North American energy markets have been amplified by the Hormuz disruption, creating compounding pressure on global energy procurement strategies.

The persistent risk premium embedded in spot LNG pricing as a result of Hormuz uncertainty is not simply a short-term market distortion. It reflects a structural repricing of supply chain security risk that will influence long-term contracting decisions, infrastructure investment priorities, and energy policy frameworks across importing nations for years. The imperative to reduce Hormuz dependency is now a commercial reality, and the oil market disruption feeding into broader energy commodity markets reinforces why this moment marks a structural inflection point, rather than a temporary shock.

FAQ: Qatar LNG Tankers and the Strait of Hormuz

Why Are Qatar LNG Tankers Transiting the Strait Despite the IRGC's Closure Declaration?

Iran's closure declarations have not been uniformly enforced. Commercial pressure from long-term contract obligations, combined with diplomatic frameworks such as the US-Iran ceasefire extension, has created selective transit windows that some operators have chosen to use. The absence of absolute enforcement means that closure declarations function as risk signals rather than physical barriers.

What Percentage of Global LNG Trade Passes Through the Strait of Hormuz?

Approximately one-fifth of all globally traded LNG transits the Strait of Hormuz each year, with Qatar representing the dominant share of that volume.

How Much LNG Export Capacity Has Qatar Lost Due to the Conflict?

Iranian strikes have damaged an estimated 17% of QatarEnergy's LNG export capacity, with repairs projected to take between three and five years to complete.

What Is a Dark Voyage in LNG Shipping?

A dark voyage refers to a transit conducted with the AIS transponder deactivated, making the vessel undetectable on commercial tracking systems. This practice reduces targeting risk in conflict zones but creates significant supply chain transparency deficits for buyers, regulators, and market analysts.

Which Countries Face the Greatest Exposure to Reduced Qatari LNG Volumes?

Japan, South Korea, China, and India represent the primary importers of Qatari LNG and carry the greatest direct volumetric exposure. European nations that expanded LNG import capacity after 2022 also face elevated supply security risk.

Are Other Gulf Producers Able to Compensate for Reduced Qatari LNG Output?

ADNOC and Kuwait Petroleum Corporation have introduced flexible loading mechanisms to help buyers manage logistics uncertainty. However, neither producer holds sufficient spare LNG capacity to offset Qatar's structural volume reduction. The gap is real and will persist across multiple contracting cycles.

Want to Track the Next Major Energy and Resources Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex resource data into actionable opportunities for both short-term traders and long-term investors navigating an increasingly volatile commodities landscape. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the broader market.