May 17, 2026

Qatar's Position as a Global LNG Supply Hub

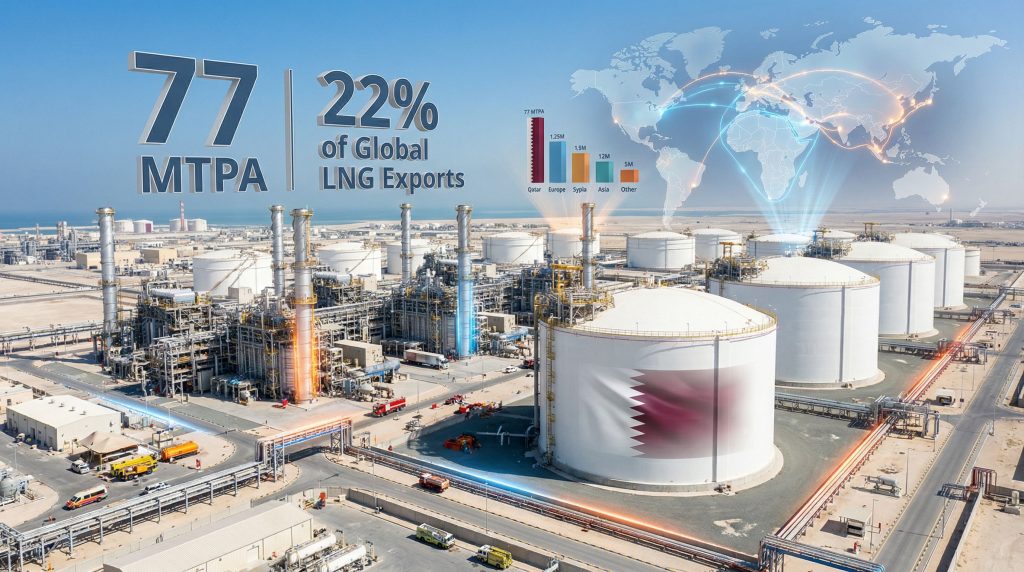

Qatar maintains its status as the world's largest LNG provider through a combination of massive production capacity, strategic geographic positioning, and extensive maritime logistics capabilities. The nation's total LNG production capacity reaches approximately 77 million tons per annum (MTPA), positioning it as a critical supplier to both European and Asian markets. Furthermore, these capabilities directly influence global energy security strategies as nations seek reliable supply sources.

Geographic and Logistical Advantages

QatarEnergy leverages its position between major consuming regions, operating what the company describes as the world's largest fleet of LNG carriers. This geographic advantage translates into operational flexibility for serving diverse market demands across different time zones and seasonal patterns.

The Ras Laffan Industrial Complex operates 14 LNG trains in total, representing a massive concentration of processing capability at a single location. The facility also integrates Gas-to-Liquids (GTL) operations through the Pearl facility, which converts natural gas into premium fuels, engine oils, lubricants, paraffins, and waxes.

Integrated Production Capabilities

Beyond LNG, Qatar's energy infrastructure produces multiple associated products that demonstrate the interconnected nature of modern gas processing:

- Condensates: High-value liquid hydrocarbons

- Liquefied Petroleum Gas (LPG): Essential for industrial and residential applications

- Naphtha: Critical petrochemical feedstock

- Sulfur: Industrial chemical applications

- Helium: Specialized industrial and medical applications

This product integration means that disruptions to LNG facilities create ripple effects across multiple commodity markets simultaneously.

When big ASX news breaks, our subscribers know first

Quantifying the March 2026 Production Disruptions

The QatarEnergy missile strikes impact on LNG exports resulted in the offline status of two major production trains, representing substantial capacity losses across multiple product streams. Train 4 and Train 6, totaling 12.8 MTPA of production capacity, went offline following missile strikes on March 18 and March 19, 2026.

Immediate Capacity Losses

The damaged facilities represent 17 percent of Qatar's total LNG export capacity, creating immediate supply constraints for long-term contract customers. Both affected trains operate as joint ventures between QatarEnergy and ExxonMobil, with ownership structures of 66-34 percent and 70-30 percent respectively.

| Product Stream | Annual Loss | Percentage of Qatar's Exports |

|---|---|---|

| LNG Production | 12.8 MTPA | 17% |

| Condensates | 18.6 million barrels | 24% |

| LPG | 1.281 million tons | 13% |

| Naphtha | 0.594 million tons | 6% |

| Sulfur | 0.18 million tons | 6% |

| Helium | 309.54 MCFA | 14% |

Associated Infrastructure Damage

The Pearl GTL facility sustained damage to one of its two production trains, with operations expected to remain offline for a minimum of one year. This facility represents critical Gas-to-Liquids technology that produces premium fuel products and specialty chemicals.

Emergency response teams successfully contained resulting fires with no reported casualties, indicating effective crisis management protocols. However, damage assessment processes revealed extensive infrastructure impacts requiring multi-year reconstruction timelines.

Financial Impact Projections and Recovery Scenarios

QatarEnergy projects approximately $20 billion in annual lost revenue from the facility damage, with repair and reconstruction timelines estimated at 3 to 5 years. These projections reflect not only direct production losses but also the complex logistics of specialized equipment procurement and installation.

Force Majeure Declarations and Contract Implications

The company announced force majeure declarations lasting up to five years on selected long-term LNG contracts, affecting supply agreements with major consumers including:

- China: Primary Asian market destination

- South Korea: Key Northeast Asian consumer

- Italy: European distribution hub

- Belgium: Northwestern European market access

The damage sustained by the LNG facilities will take between three to five years to repair, compelling force majeure declarations that will impact global energy security and stability.

Force majeure provisions in LNG contracts typically include specific criteria for infrastructure damage, supply interruption duration, and alternative sourcing obligations. The activation of these clauses creates legal frameworks for contract renegotiation and alternative supply arrangements.

Reconstruction Complexity and Timeline Factors

LNG train reconstruction involves specialized cryogenic equipment, proprietary processing technology, and extensive safety certification processes. Historical precedents suggest that major facility reconstruction projects require:

- Damage assessment and engineering design (6-12 months)

- Specialized equipment procurement (12-24 months)

- Construction and installation (18-36 months)

- Testing and commissioning (6-12 months)

The sequential nature of these phases, combined with global supply chain constraints for specialized LNG equipment, supports the projected 3-5 year recovery timeline.

Global Gas Market Price Responses and Volatility

European natural gas benchmarks experienced immediate and substantial price increases following confirmation of the facility damage. The Dutch TTF (Title Transfer Facility) benchmark opened at €72.0/MWh on March 19, 2026, representing a 32 percent overnight surge from the previous close of €54.7/MWh.

European Market Benchmark Reactions

| Benchmark | March 18 Close | March 19 Open | Percentage Change |

|---|---|---|---|

| Dutch TTF | €54.7/MWh | €72.0/MWh | +32% |

| UK NBP | 139.5p/therm | 178p/therm | +28% |

The UK NBP (National Balancing Point) similarly surged from 139.5p/therm to 178p/therm, reflecting widespread concern about European gas supply security during winter heating seasons. These movements align with broader natural gas price trends observed in global markets.

Regional Price Divergence Patterns

Market analysis reveals divergent price responses across different regional hubs, with European and Asian benchmarks experiencing more pronounced increases than North American markets. The U.S. Henry Hub prices remained relatively muted compared to international benchmarks, reflecting domestic supply abundance and pipeline infrastructure isolation from global LNG disruptions.

Asian JKM (Japan Korea Marker) prices tracked closely with European increases, demonstrating the interconnected nature of global LNG spot markets. This correlation reflects competition between European and Asian buyers for alternative supply sources during periods of constraint.

Risk Premium Integration and Market Psychology

Energy analysts project sustained risk premiums in global natural gas pricing, reflecting ongoing geopolitical tensions and infrastructure vulnerability concerns. Market psychology shifts toward supply security prioritisation over cost optimisation, potentially accelerating long-term contract renegotiation processes.

The price response patterns indicate market recognition that Qatar's LNG infrastructure represents a critical node in global energy supply chains, with limited short-term substitution possibilities for the affected volumes. These dynamics mirror broader oil market dynamics in response to supply disruptions.

Strategic Infrastructure Security and Vulnerability Assessment

The targeting of Qatar's Ras Laffan complex highlights fundamental vulnerabilities in concentrated energy infrastructure systems. As the world's largest LNG processing facility, Ras Laffan processes natural gas through 14 production trains, creating a single point of failure for substantial global supply volumes.

Critical Infrastructure Concentration Risks

Modern LNG systems concentrate massive processing capabilities at individual facilities to achieve economies of scale and operational efficiency. However, this concentration creates systemic risks when facilities face operational disruptions from:

- Geopolitical conflicts and military targeting

- Natural disasters including hurricanes and earthquakes

- Industrial accidents and technical failures

- Cyberattacks on control systems and operations

The Ras Laffan complex demonstrates these concentration risks, with two damaged trains representing 17 percent of Qatar's total export capacity. Alternative global LNG sources cannot immediately replace this volume without significant price premiums and logistical adjustments.

Regional Conflict Escalation and Energy Targeting

The March 2026 missile strikes occurred within the context of broader U.S.-Iran regional tensions, illustrating how energy infrastructure becomes strategic targets during geopolitical conflicts. Critical energy facilities represent high-value targets that can disrupt opponent economic capabilities while avoiding direct military confrontation escalation.

Historical precedent suggests that energy infrastructure targeting creates lasting impacts that extend beyond immediate conflict resolution, as reconstruction timelines often span multiple years regardless of political settlement timelines. These patterns reflect broader trade war impacts on global supply chains.

Alternative Supply Sources and Market Rebalancing

Global LNG markets must redistribute approximately 12.8 MTPA of annual supply capacity across alternative sources and consumption adjustments. This rebalancing process involves both increased production from existing facilities and demand destruction through higher pricing.

Competing LNG Supplier Opportunities

Major LNG exporting nations stand to benefit from Qatar's reduced export capacity through increased market share and premium pricing opportunities:

United States: Flexible production from shale gas resources with multiple Gulf Coast export facilities

Australia: Established LNG infrastructure with expansion capabilities in Queensland and Western Australia

Russia: Pipeline and LNG export capabilities, though constrained by ongoing geopolitical sanctions

Algeria: Mediterranean proximity to European markets with pipeline and LNG export options

Supply Chain Flexibility and Constraints

Alternative LNG sources face various constraints in rapidly scaling production to replace Qatari volumes:

- Technical production limits at existing facilities

- Long-term contract commitments to existing customers

- Transportation logistics and vessel availability

- Seasonal demand variations affecting supply allocation flexibility

The global LNG carrier fleet represents another potential constraint, as vessels are often committed to specific routes and loading terminals under long-term charter agreements.

The next major ASX story will hit our subscribers first

Energy Transition Acceleration and Policy Responses

Extended LNG supply disruptions may accelerate renewable energy adoption timelines as governments and corporations seek supply security through diversification. The crisis demonstrates the vulnerability of fossil fuel supply chains to geopolitical disruption, potentially strengthening arguments for domestic renewable energy development.

Corporate Energy Procurement Strategy Shifts

Large industrial energy consumers face immediate decisions about supply security versus cost optimisation. Extended force majeure periods on Qatar LNG contracts may drive corporate procurement strategies toward:

- Renewable energy power purchase agreements (PPAs)

- On-site renewable generation installations

- Energy storage systems for supply security

- Industrial process electrification to reduce gas dependence

Policy Framework Acceleration Scenarios

European energy policy frameworks, particularly the REPowerEU initiative, may experience acceleration in response to demonstrated supply vulnerability. Policy responses could include:

Enhanced renewable energy targets with accelerated deployment timelines

Strategic gas storage requirements for supply security buffers

Critical infrastructure protection investments and protocols

Alternative energy source development and import diversification

However, near-term energy security requirements may necessitate continued reliance on available fossil fuel sources while renewable capacity scales to meet demand.

Recovery Pathways and Reconstruction Scenarios

Restoring Qatar's full LNG export capacity requires complex reconstruction processes involving specialised equipment, international expertise, and extensive quality assurance protocols. The projected 3-5 year timeline reflects both technical complexity and global supply chain constraints for LNG processing equipment.

Technical Reconstruction Challenges

LNG train reconstruction involves multiple specialised systems that must be rebuilt and integrated:

Cryogenic processing equipment: Ultra-low temperature gas liquefaction systems requiring specialised materials and manufacturing

Safety and control systems: Complex automation and emergency shutdown systems meeting international safety standards

Structural infrastructure: Concrete foundations, pipe networks, and support systems designed for extreme operating conditions

Power generation systems: Dedicated electrical generation and distribution for massive processing operations

Parallel Construction and Optimisation Strategies

QatarEnergy may pursue parallel reconstruction approaches to minimise total recovery time:

- Simultaneous train reconstruction rather than sequential approaches

- Pre-fabricated module installation to reduce on-site construction time

- Alternative supplier diversification for critical equipment components

- Fast-track permitting processes for reconstruction activities

The success of parallel construction strategies depends on equipment availability, skilled labour mobilisation, and financial resources allocation across multiple simultaneous projects.

Interim Capacity Management

During the reconstruction period, QatarEnergy must optimise remaining operational capacity across undamaged facilities. This optimisation involves:

- Production scheduling adjustments to maximise throughput from operational trains

- Contract allocation prioritisation among existing long-term customers

- Spot market participation to capture premium pricing opportunities

- Maintenance scheduling coordination to minimise additional downtime

Strategic customer relationship management becomes critical during capacity constraints, as contract modifications and alternative arrangement negotiations will influence long-term market position post-recovery.

Long-Term Market Structure Evolution

The QatarEnergy missile strikes impact on LNG exports may catalyse structural changes in global natural gas markets that persist beyond facility reconstruction completion. These changes include contract term modifications, pricing mechanism evolution, and supply source diversification requirements.

Contract Structure Innovation

Traditional long-term LNG contracts typically span 15-20 years with fixed volume commitments and oil-indexed pricing mechanisms. The Qatar disruption may accelerate evolution toward more flexible contract structures including:

Shorter contract terms with renewal options providing buyer flexibility

Multiple supply source provisions reducing single-supplier dependency risks

Force majeure compensation mechanisms protecting buyers during supply disruptions

Flexible volume commitments allowing demand adjustments during market volatility

Spot Market Development and Liquidity

Extended supply constraints may accelerate spot market development as buyers seek flexible sourcing options. Increased spot market activity could drive:

- Price discovery mechanisms more responsive to real-time supply/demand balance

- Financial market instruments including LNG futures and derivatives contracts

- Regional hub development creating multiple pricing reference points

- Storage infrastructure investment enabling temporal arbitrage opportunities

Enhanced spot market liquidity may reduce the premium associated with long-term contract security, creating more competitive pricing dynamics across the global LNG market.

Risk Management and Investment Implications

The Qatar facility disruption provides critical insights for energy infrastructure investment evaluation and risk management frameworks. Investors must reassess single-asset concentration risks and geographic diversification strategies within energy portfolios.

Infrastructure Investment Risk Assessment

Energy infrastructure investments require comprehensive risk evaluation incorporating:

Geopolitical stability assessment of operating jurisdictions and regional conflict potential

Geographic diversification across multiple facilities and regulatory environments

Technical redundancy planning including backup systems and alternative operational pathways

Insurance coverage adequacy for political risk and business interruption scenarios

Portfolio Diversification Strategies

Investment portfolios concentrated in Middle Eastern energy infrastructure face demonstrated volatility risks that may require rebalancing toward:

- Geographic diversification across stable political jurisdictions

- Technology diversification including renewable energy infrastructure

- Supply chain integration from production through distribution systems

- Demand sector diversification across industrial, residential, and transportation markets

The QatarEnergy missile strikes impact on LNG exports demonstrates that individual facility outages can create systemic market impacts when production capacity is highly concentrated. Consequently, diversified portfolio approaches may provide superior risk-adjusted returns over extended time horizons.

What Are the Long-Term Implications for Global Energy Markets?

The current supply disruption reveals fundamental questions about energy system resilience that extend beyond immediate reconstruction timelines. As reported by QatarEnergy officials, the facility damage represents the most significant infrastructure challenge in the company's history, requiring unprecedented reconstruction efforts.

Industry analysis from Offshore Energy indicates that the $20 billion revenue loss projection may be conservative, considering potential secondary effects on related petrochemical operations and long-term market share impacts.

The QatarEnergy missile strikes impact on LNG exports ultimately highlights the delicate balance between energy efficiency through concentrated production and supply security through diversification. Market participants must now weigh these competing priorities as global energy systems evolve in response to demonstrated infrastructure vulnerabilities.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and publicly available information. Actual outcomes may differ significantly from projections due to unforeseen technical, political, or economic factors. Readers should conduct independent research and consult qualified professionals before making investment decisions related to energy infrastructure or commodity markets.

Are You Positioned to Capitalise on Energy Market Disruptions?

Qatar's LNG facility disruptions demonstrate how geopolitical events can create immediate trading opportunities and reshape entire commodity markets. Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral and energy discoveries, empowering subscribers to identify actionable opportunities ahead of the broader market during periods of heightened volatility. Begin your 14-day free trial today to secure your market-leading advantage in energy and critical minerals investing.