June 8, 2026

The Hidden Architecture of Rare Earth Supply Chain Security

Global supply chains for critical minerals have entered a new era, one where governments no longer wait for markets to solve strategic vulnerabilities. For decades, the United States relied on trade policy, diplomatic relationships, and market incentives to secure access to the raw materials powering its defence and industrial base. That model has been quietly abandoned. In its place, a new architecture of direct government capital deployment is taking shape, and nowhere is this shift more visible than in the US government partner in rare earths project in Brazil arrangement now reshaping rare earth supply chains across Latin America.

Brazil has emerged as a focal point of this transformation, attracting direct financial commitments from the U.S. government through its primary development finance institution. The country's geological endowment, particularly its ionic clay deposits in the state of Goiás, has drawn attention not just for the volume of rare earth resources it contains, but for the specific mix of magnetic elements that align precisely with America's most pressing supply chain vulnerabilities.

Understanding why the US government partner in rare earths project in Brazil arrangement matters requires unpacking several layers of strategy, geology, finance, and geopolitics that rarely appear in the same analysis.

When big ASX news breaks, our subscribers know first

What Makes Rare Earth Elements Different From Other Strategic Commodities

The Permanent Magnet Problem and Why It Changes Everything

Not all rare earth elements carry equal strategic weight. While the periodic table includes 17 elements classified as rare earths, the investment and security calculus orbits around a narrow cluster of four: neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). These are the magnetic rare earth elements, and their importance stems from a single application that has quietly become foundational to both clean energy and modern defence.

Neodymium-iron-boron (NdFeB) permanent magnets are the strongest permanent magnets known to materials science. They are the core component in:

- Electric vehicle traction motors, where a single EV can require 1 to 2 kilograms of rare earth magnet material

- Direct-drive offshore wind turbine generators, where a single large turbine can contain 600 kilograms or more of rare earth magnets

- Precision-guided munitions, radar systems, sonar equipment, and advanced aircraft propulsion used by U.S. defence contractors

- Consumer electronics including hard drives, speakers, and industrial robotics

The strategic problem is not the rarity of these elements in the earth's crust. They are actually more abundant than gold or platinum. The problem is the concentration of processing and magnet manufacturing capacity. China controls an estimated 85 to 90 percent of global rare earth permanent magnet production, a dominance built through decades of state-directed industrial policy and investment in separation and metallurgical infrastructure that the West largely ceded during the 1990s and 2000s.

Furthermore, China's export restrictions have demonstrated just how weaponisable this dominance can be, adding urgency to efforts to diversify supply.

This is not a commodity market dynamic. It is a structural dependency embedded deep within Western industrial and defence supply chains, one that cannot be resolved through tariffs or diplomatic communiqués alone.

Light vs. Heavy Rare Earths: A Critical Distinction for Investors

One aspect of rare earth geology that is frequently misunderstood outside specialist circles is the distinction between light rare earth elements (LREEs) and heavy rare earth elements (HREEs). This distinction carries significant implications for both project economics and strategic value.

| Category | Elements | Primary Use | Chinese Processing Control |

|---|---|---|---|

| Light REEs (LREEs) | Neodymium, Praseodymium, Cerium, Lanthanum | EV motors, catalysts, polishing compounds | Very High |

| Heavy REEs (HREEs) | Dysprosium, Terbium, Yttrium, Europium | High-performance magnets, phosphors, defence systems | Near Total |

Heavy rare earth elements are particularly critical because dysprosium and terbium are added to NdFeB magnets to improve their thermal stability, allowing them to function in high-temperature environments such as EV motors under load and military jet engines. Without these additives, permanent magnets lose their magnetic properties at elevated temperatures, making them unsuitable for demanding applications.

Brazil's ionic clay deposits in northern Goiás are notable for containing concentrations of both light and heavy magnetic rare earths, a geological profile that meaningfully elevates their strategic value relative to many other non-Chinese rare earth deposits globally.

The DFC: Understanding the Financial Instrument Reshaping Global Resource Security

How America's Development Finance Institution Works

The U.S. International Development Finance Corporation came into existence through the Better Utilization of Investments Leading to Development Act of 2018, which consolidated and expanded the mandate of its predecessor institution, the Overseas Private Investment Corporation. The legislative intent was to create a more capable, more flexible development finance tool that could compete with state-backed financing institutions from China and other strategic rivals in emerging markets.

What distinguishes the DFC from a commercial lender or a traditional foreign aid programme is the breadth of financial instruments it can deploy:

- Direct loans at concessional or market-equivalent rates, providing capital for project development

- Loan guarantees that reduce risk for private co-investors and catalyse larger capital pools

- Equity investments that make the U.S. government a direct shareholder in foreign enterprises

- Convertible financing instruments that begin as debt but can transition to equity under defined conditions

- Political risk insurance that protects investors against nationalisation, currency inconvertibility, and political violence

This toolkit gives the DFC capabilities that extend far beyond traditional aid and far closer to the strategic capital deployment model employed by sovereign wealth funds and state-owned enterprises in countries like China. The critical minerals initiative formally embedded within the DFC's mandate represents the application of these tools specifically to the problem of supply chain security. In addition, America's rare earth supply chain strategy has increasingly relied on the DFC as a primary vehicle for projecting financial influence into critical mineral jurisdictions.

The DFC's ability to convert debt financing into equity represents a structural evolution in how the U.S. government participates in foreign resource development, moving beyond diplomatic encouragement into direct ownership stakes.

DFC Investment Criteria for Rare Earth Projects

Projects seeking DFC financing in the critical minerals space must satisfy a demanding set of criteria that blend commercial viability with national security alignment:

- Demonstrated alignment with U.S. national security priorities, particularly those tied to defence-grade permanent magnets and clean energy supply chains

- Transparent ownership structures with no problematic third-country involvement in project governance or offtake arrangements

- Environmental compliance frameworks consistent with international standards, addressing reputational risks for the U.S. government as a co-investor

- Offtake agreements or credible pathways to offtake linked to U.S. or allied-nation buyers, ensuring that the strategic supply chain benefit actually materialises

- Near-term production scalability, reflecting a preference for projects that can deliver supply within actionable planning horizons rather than speculative timelines

The Serra Verde and Aclara Investments: What the Numbers Reveal

Breaking Down the DFC's Financial Commitments in Brazil

The two most publicly documented DFC commitments in Brazil's rare earth sector differ substantially in scale, structure, and strategic purpose, yet together they illustrate the range of tools the U.S. government is deploying.

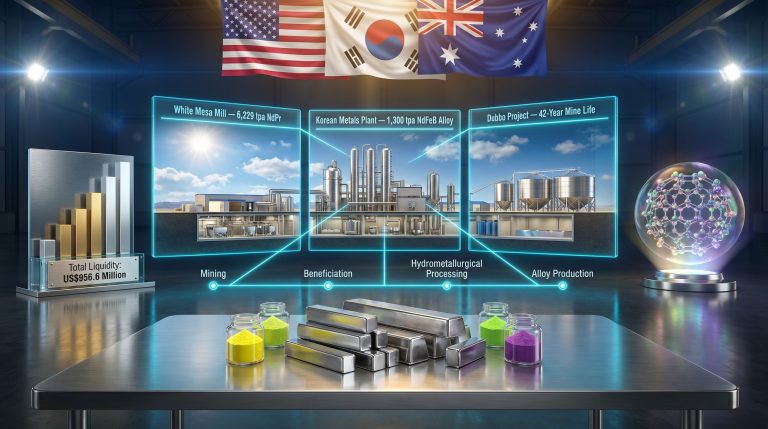

Serra Verde operates a rare earth mine in northern Goiás that has achieved commercial production status, making it one of the few operational rare earth mines outside China producing magnetic rare earth elements at scale. The DFC approved a $465 million loan to support the mine's expansion, representing one of the largest single critical minerals commitments the institution has made in Latin America. The U.S. government formally welcomed this investment as a milestone in securing non-Chinese rare earth production.

Serra Verde's deposit is an ionic clay-hosted rare earth system. The extraction methodology involves applying an ammonium sulphate or similar leaching solution to the clay-rich ore, which displaces the adsorbed rare earth ions and allows them to be collected in solution. This is a fundamentally different and generally lower-impact process than the crushing and chemical processing required for hard-rock rare earth deposits.

The expansion financing is anchored by a 15-year offtake agreement connecting Serra Verde's rare earth output to U.S.-aligned buyers including government agencies and private capital partners. An offtake agreement of this duration functions as far more than a commercial contract. It establishes a durable supply corridor between Brazil and the United States that persists through political cycles and market volatility.

Aclara Resources received a comparatively modest $5 million financing package, but the strategic significance of this commitment may exceed its dollar value. The Aclara package includes a convertibility clause that allows the DFC to convert its debt position into an equity stake under defined conditions. This creates an option for the U.S. government to become a direct shareholder in a Brazilian rare earth mining operation.

| Project | DFC Instrument | Committed Value | Equity Convertibility | Development Stage |

|---|---|---|---|---|

| Serra Verde | Loan | $465 million | Not specified | Expansion/Commercial |

| Aclara Resources | Financing Package | $5 million | Yes | Early-stage |

What a Senior Creditor Position Actually Means in Practice

A detail that receives insufficient attention in coverage of DFC loans is the governance influence that accompanies senior creditor status. When the DFC lends $465 million to a project, it does not simply transfer funds and wait for repayment. Standard DFC loan covenants typically include:

- Environmental and social performance requirements with independent monitoring mechanisms

- Restrictions on changes in project ownership or control without DFC consent

- Reporting obligations on production, revenue, and offtake delivery performance

- Limitations on additional debt that could subordinate the DFC's position

- Clauses relating to the nationality and strategic alignment of future offtake counterparties

This suite of covenants effectively gives the DFC meaningful oversight over project governance even without formal equity ownership, making the distinction between debt and equity less sharp in practice than it appears on paper.

Why Brazil Stands Apart From Other Latin American REE Jurisdictions

A Regional Comparison of Rare Earth Investment Potential

Latin America hosts significant critical mineral resources across multiple countries, but the rare earth landscape is not evenly distributed. Brazil's combination of geological endowment, political environment, and existing infrastructure creates a differentiated profile relative to regional peers. The surge in critical minerals demand has further intensified competition among jurisdictions seeking to attract strategic capital.

| Factor | Brazil | Chile | Peru | Argentina |

|---|---|---|---|---|

| Known REE Reserves | Very High | Moderate | Low | Low-Moderate |

| Ionic Clay Deposits | Yes (Goiás) | Limited | Limited | Limited |

| DFC Active REE Investment | Yes | Limited | Limited | Primarily lithium |

| Political Stability | Moderate-High | High | Moderate | Low-Moderate |

| Existing Processing Infrastructure | Developing | Limited | Limited | Developing |

| Mining Governance Maturity | High | Very High | Moderate | Moderate |

The Ionic Clay Advantage: Geology as a Competitive Moat

The concentration of ionic clay rare earth deposits in northern Goiás is not merely a geological curiosity. It is a competitive advantage that materially differentiates Brazilian rare earth projects from most non-Chinese alternatives. Several technical characteristics explain why:

- Ionic clay deposits typically have lower strip ratios than hard-rock mining operations, reducing waste generation and mining costs

- The leaching process used to extract rare earths from ionic clays operates at ambient temperatures, eliminating the energy-intensive roasting and cracking steps required for hard-rock rare earth ores

- Recovery rates for critical magnetic rare earth elements from ionic clay systems can reach 70 to 80 percent with established processing methods

- The absence of thorium and uranium co-contamination in many ionic clay systems reduces regulatory complexity around radioactive waste management

- Shorter mine-to-production timelines compared to greenfield hard-rock rare earth mines make ionic clay projects more responsive to urgent supply chain timelines

These geological advantages are not universally distributed across all Brazilian rare earth deposits. The ionic clay systems of Goiás are geologically analogous to the southern Chinese ionic clay deposits in Jiangxi and Fujian provinces, which have supplied the bulk of global heavy rare earth production for decades. This geological parallel is precisely what makes the Goiás deposits strategically compelling to U.S. planners.

The Absence of a Bilateral Treaty: A Structural Vulnerability

Why the Project-Level Approach Creates Risk

One of the more nuanced aspects of the US government partner in rare earths project in Brazil arrangement is the reported absence of a formal bilateral critical minerals agreement at the time these investments were structured. This matters considerably for how the partnership should be assessed from both an investment and a geopolitical standpoint.

A government-to-government critical minerals agreement typically provides:

- Legal protections for investments that operate under treaty law rather than purely domestic contract law

- Streamlined regulatory pathways for project development, permitting, and environmental approvals

- Dispute resolution mechanisms with international arbitration backstops

- Mutual commitments on supply chain security that create political accountability on both sides

- Preferential offtake frameworks that formally integrate the partner country's resources into the investing country's supply chain planning

Without this treaty foundation, the DFC's commitments in Brazil operate through commercial financial instruments subject to Brazilian domestic law, regulatory decisions, and the policy priorities of successive governments. This introduces a meaningful degree of political risk not present in investments structured under formal bilateral agreements. According to Columbia University's energy policy research, Brazil's potential role in diversifying U.S. critical mineral supply is substantial but contingent on precisely this kind of institutional framework being strengthened.

The DFC's involvement in Brazilian rare earth projects does not constitute a formal government-to-government minerals treaty. These are commercially structured financial instruments deployed by a U.S. government agency, a meaningful but legally distinct form of partnership.

The practical implication for investors and project operators is that changes in Brazil's domestic mining policy, environmental regulations, or government priorities could affect DFC-backed projects in ways that would not occur under a treaty-protected framework. The current Brazilian administration's general openness to foreign investment in critical minerals has been constructive, but the durability of that orientation across future electoral cycles cannot be guaranteed.

The next major ASX story will hit our subscribers first

Geopolitical Acceleration: Tariffs, Trade Tensions, and the Investment Case

How U.S.-China Trade Dynamics Are Reshaping Capital Flows Into Brazilian REE Projects

The broader context of escalating U.S.-China trade tensions has created an economic urgency that compounds the strategic rationale for DFC investment in Brazilian rare earths. China's demonstrated willingness to weaponise rare earth supply, evidenced by export restrictions to Japan in 2010 and more recently through controls on rare earth processing technologies and refined products, has shifted the risk calculus for U.S. industrial planners. These dynamics are inseparable from the broader rare earth processing challenges that non-Chinese projects must navigate to deliver material at the required specification.

The introduction of tariffs on Chinese rare earth products entering the United States creates a direct economic incentive to develop non-Chinese supply sources. From a project finance perspective, tariff-driven price differentials on Chinese-origin rare earths effectively improve the economics of Brazilian supply alternatives. This creates a commercial foundation that overlays the strategic rationale, making DFC-backed Brazilian projects attractive not just as security hedges but as potentially competitive commercial propositions.

However, several risks and limitations of the current approach deserve acknowledgment:

- Processing capacity constraints: Brazil currently lacks the downstream rare earth separation and metallurgical infrastructure needed to deliver finished rare earth oxides or metals at scale, requiring processing partnerships with allied nations

- Currency exposure: Long-duration loan repayment structures create exposure to Brazilian real depreciation, which can affect project economics and repayment capacity

- Infrastructure gaps: Northern Goiás requires continued development of transport, power, and logistics infrastructure to support expanding mining operations at the scale DFC financing envisions

- Processing technology transfer: Ensuring that processing knowledge developed with U.S. financial backing remains within the Western supply chain ecosystem requires careful contractual structuring

Forward Scenarios: What Comes Next for U.S.-Brazil Rare Earth Cooperation

Three Pathways That Will Define the Partnership's Long-Term Value

The current state of U.S. government engagement in Brazil's rare earth sector represents an inflection point. The direction it develops over the next three to five years will be shaped by decisions at multiple levels of both governments, as well as by market forces and the competitive dynamics of the global rare earth sector.

Scenario 1: Formalisation Through a Bilateral Critical Minerals Agreement

If the United States and Brazil conclude a formal critical minerals agreement, the existing project-level DFC investments would be elevated into a treaty-protected framework. This would expand the protections available to U.S.-aligned capital, potentially unlock additional DFC commitments to other Brazilian rare earth projects, and signal a durable strategic alignment that could attract substantial private capital. The concluding of such an agreement would represent a structural upgrade from transactional finance to systemic partnership.

Scenario 2: DFC Equity Conversion in Aclara Resources

If Aclara's project reaches the development milestones specified in its convertibility clause, the DFC would have the option to transition from creditor to co-owner. This would establish a precedent for direct U.S. government equity participation in a Latin American rare earth mining operation, a qualitatively different form of engagement with long-term governance implications.

Scenario 3: Serra Verde Reaches Target Production Capacity

The $465 million loan expansion thesis depends on Serra Verde successfully scaling its ionic clay rare earth operations to a level that materially contributes to U.S. magnetic rare earth supply requirements. Achieving this would validate the DFC's project-finance model for critical minerals security and potentially catalyse replication of the Serra Verde model across other Brazilian and Latin American rare earth deposits.

Key Metrics for Monitoring Progress

Investors and policy observers tracking the evolution of this partnership should monitor the following indicators:

- Progress toward a formal U.S.-Brazil bilateral critical minerals agreement and any communiqués from the Minerals Security Partnership framework

- DFC equity conversion decisions related to the Aclara Resources financing package and any announced milestone triggers

- Serra Verde quarterly production reports and offtake delivery performance against the 15-year supply agreement

- Brazilian federal government mining policy developments, particularly regulations affecting foreign investment in strategic minerals

- Expansion of DFC commitments to additional Brazilian rare earth projects beyond Serra Verde and Aclara, which would indicate systemic commitment rather than opportunistic project selection

- Progress on downstream processing infrastructure in Brazil or allied-nation processing partnerships that would allow Brazilian rare earth feedstocks to move through the supply chain without Chinese intermediation

The emergence of the US government partner in rare earths project in Brazil as a defining feature of Western supply chain strategy represents more than a financial transaction. It marks a fundamental reconfiguration of how the Western world is choosing to contest China's dominance: not through market appeals or diplomatic encouragement, but through direct government capital deployment into strategically located geological assets. Whether this approach proves sufficient to the scale of the challenge it addresses will depend on execution, political durability, and the speed at which Brazilian rare earth projects can translate geological potential into reliable supply.

This article is intended for informational purposes only and does not constitute financial or investment advice. Projections and scenario analyses involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct their own due diligence before making investment decisions.

Want to Track the Next Major Rare Earth Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including critical and rare earth minerals — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.