June 27, 2026

Europe's critical material dependencies face unprecedented transformation as demand for strategic minerals intensifies across renewable energy and advanced manufacturing sectors. The recent discovery of a massive rare earth deposit Europe could fundamentally reshape energy transition security strategies and reduce reliance on concentrated supply chains. Furthermore, this development occurs within evolving global mining landscape dynamics that demand comprehensive strategic analysis.

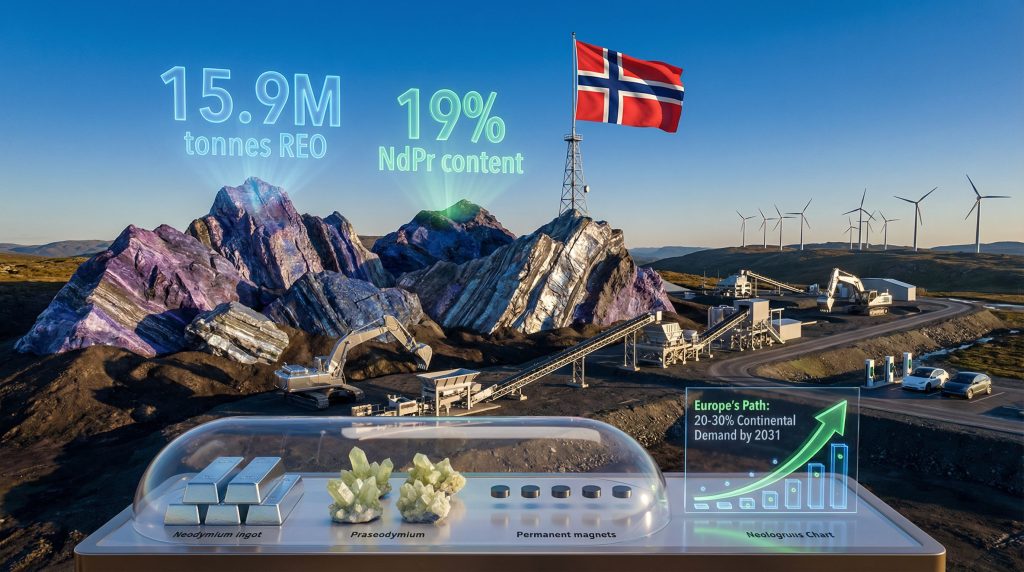

Norway's Game-Changing Resource Discovery

Norway's Fen Complex has emerged as a pivotal development in European resource strategy, following the announcement of substantially expanded resource estimates. The deposit now contains 15.9 million metric tons of total rare earth oxide content across indicated and inferred categories, representing an 81 percent increase from previous assessments of 8.8 million metric tons reported in 2024.

This massive expansion reflects comprehensive exploration drilling conducted throughout 2025, with third-party validation provided by consulting firm WSP. The resource upgrade positions the Fen Complex as the largest confirmed rare earth deposit in continental Europe, surpassing Sweden's Per Geijer deposit.

According to Reuters analysis, this discovery could significantly alter Europe's strategic mineral position. The deposit's 19 percent neodymium and praseodymium concentration translates to approximately 3.021 million metric tons of these critical permanent magnet elements.

Critical Resource Metrics:

• Total Resource Base: 15.9 million tonnes rare earth oxide content

• NdPr Concentration: 19% neodymium and praseodymium content

• Strategic Classification: Indicated and inferred resources

• Geographic Advantage: Southern Norway location with existing infrastructure

When big ASX news breaks, our subscribers know first

European Resource Portfolio in Global Context

Table: European Rare Earth Deposits Compared to Global Benchmarks

| Deposit Location | Total REO (Million Tonnes) | Key Characteristics | Development Status |

|---|---|---|---|

| Fen Complex, Norway | 15.9 | NdPr-rich (19%), carbonatite-hosted | Resource definition |

| Per Geijer, Sweden | 2.2 | Mixed REE, phosphorus-associated | Exploration stage |

| Kvanefjeld, Greenland | 11.0+ | Heavy REE enriched | Regulatory assessment |

| Mountain Pass, USA | 1.4 | Light REE dominated | Active production |

| Bayan Obo, China | 48.0+ | Mixed REE, world's largest | Major production center |

The collective European resource base exceeds 29 million metric tons of rare earth oxides, representing more than double North America's primary producing asset. However, resource abundance differs fundamentally from production capacity and processing capability.

Geographic concentration in northern latitudes offers advantages in energy availability for processing-intensive operations. Conversely, regulatory coordination across multiple jurisdictions complicates development timelines compared to geographically concentrated deposits.

Geological Diversity and Processing Implications

European deposits demonstrate significant geological variation affecting processing requirements:

• Carbonatite-hosted deposits (Fen Complex): Require alkaline processing routes with specialised carbonate mineral separation

• REE-phosphorus deposits (Per Geijer): Need integrated rare earth-phosphate processing with dual product streams

• Polymetallic complexes (Kvanefjeld): Feature heavy rare earth enrichment but require complex multi-element separation

This geological diversity prevents standardised processing approaches, limiting economies of scale while potentially enabling complementary product portfolios for different market applications.

Addressing Critical Supply Chain Vulnerabilities

China maintains dominant control over approximately 75-85 percent of global rare earth oxide production and over 90 percent of downstream processing capacity. This concentration creates multiple vulnerability vectors across technology supply chains, particularly affecting permanent magnet-dependent applications.

Current Dependency Framework:

• Processing Bottleneck: Less than 5% of global separation capacity exists outside China

• Technology Gap: Limited Western expertise in advanced separation technologies

• Market Concentration: Single-source dependency for specialised rare earth chemicals

• Strategic Risk: Defence applications dependent on Chinese supply chains

European rare earth processing capacity currently accounts for less than 5 percent of global separation output. The supply gap between European processing capacity versus European demand reveals substantial infrastructure deficits requiring investment.

Permanent Magnet Supply Chain Criticality

Neodymium-iron-boron (NdFe-B) permanent magnets represent single-source components with limited substitutability in high-performance electric motors. Production facility disruptions could cascade through global automotive supply chains within weeks, as manufacturers maintain minimal inventories.

Strategic Applications at Risk:

• Electric Vehicle Motors: 200-400kg NdPr per 1000 vehicles produced

• Wind Turbine Generators: 150-600kg rare earths per MW capacity

• Defence Electronics: Precision-guided systems requiring stable supply

• Industrial Automation: High-efficiency motor applications

Processing Infrastructure Development Pathways

Europe's path toward rare earth independence requires coordinated processing infrastructure development, representing the critical constraint superseding raw material availability. Processing facility development typically requires 3-5 year timelines, whereas mining capacity additions require 4-7 years.

Emerging European Processing Initiatives

LKAB-REEtec Collaboration:

Sweden's state-owned mining company LKAB has partnered with specialised technology developer REEtec to create innovative separation methodologies. This technological approach reduces lock-in to specific ore chemistry profiles, enabling scalable processing solutions.

Advanced Processing Technologies:

• Solvent Extraction Systems: Multi-stage separation achieving 99.9%+ purity levels

• Ion Exchange Columns: Selective recovery of individual rare earth elements

• Integrated Recycling: Urban mining from electronic waste streams

• Magnetic Material Manufacturing: Direct integration with downstream applications

The separation of neodymium from praseodymium requires sophisticated solvent extraction technologies, representing technically specialised processes requiring substantial operational expertise and optimisation.

Investment Capital Requirements and Market Dynamics

Development of European rare earth independence requires substantial capital allocation across multiple infrastructure categories. Moreover, industry innovation trends indicate increasing focus on integrated processing solutions.

Primary Development Capital:

• Mining Infrastructure: €2-4 billion for extraction operations

• Environmental Systems: €500M-1B for compliance infrastructure

• Transportation Networks: €300-500M for logistics integration

Processing Infrastructure Investment:

• Separation Facilities: €1.5-3B across multiple European locations

• Magnetic Manufacturing: €800M-1.2B for permanent magnet production

• Recycling Systems: €400-600M for circular economy infrastructure

Price Discovery and Market Structure

Current rare earth pricing remains dominated by Chinese benchmarks with limited transparency in price formation mechanisms. Volatile pricing cycles typically correlate with export policy changes, creating 15-30 percent premium pricing for non-Chinese sources during supply constraint periods.

European market development requires establishment of regional pricing benchmarks and long-term supply agreements. Industry projections suggest 10-15 percent sustainable price premiums for European-sourced products, reflecting supply security value.

Demand Growth Projections:

• Electric Vehicle Adoption: 25-30% annual growth in rare earth demand

• Renewable Energy Expansion: 15-20% annual requirement increase

• Electronics Miniaturisation: 8-12% annual demand growth

• Total European Demand: 180,000-220,000 tonnes annually by 2030

Technology Applications and Strategic Priorities

European rare earth production will primarily benefit applications with highest strategic value and supply security premiums. Additionally, The Guardian reports on increasing Chinese interest in European rare earth assets.

Electric Vehicle Sector Transformation

European automotive production of 15-18 million units annually requires substantial permanent magnet supply for electric powertrains. Each 1000 electric vehicles demand approximately 200-400kg of neodymium-praseodymium content, creating annual demand of 60,000-120,000 metric tons at full electrification.

Supply security commands 15-25 percent cost advantages for locally sourced materials compared to geopolitically vulnerable imports, justifying premium pricing for European production.

Renewable Energy Infrastructure Requirements

European wind capacity targets exceed 300 GW by 2030, with each MW requiring 150-600kg of rare earth content depending on generator design. This creates sustained demand for 45,000-180,000 metric tons annually, supporting long-term offtake agreements.

Grid Stability Implications:

• Direct Drive Turbines: Eliminate gearbox maintenance whilst requiring larger permanent magnets

• Offshore Applications: Premium pricing for reliable supply chains in harsh environments

• Energy Security: Reduced dependency on foreign supply chains for critical infrastructure

The next major ASX story will hit our subscribers first

Environmental Integration and Sustainability Frameworks

Sustainable development of European rare earth resources requires comprehensive environmental impact assessment spanning 18-24 months for regulatory approval processes. Furthermore, sustainable mining practices are becoming increasingly important for project approval.

Environmental Assessment Requirements:

• Ecosystem Impact Studies: Comprehensive biodiversity protection protocols

• Water Resource Management: Sustainable usage and contamination prevention

• Carbon Footprint Optimisation: Integration with renewable energy systems

• Cultural Heritage Protection: Stakeholder engagement and benefit-sharing

Circular Economy Integration

European rare earth strategy increasingly emphasises urban mining and recycling infrastructure development. End-of-life electronic products contain substantial rare earth content recoverable through sustainable recycling processes, potentially supplying 30-40 percent of total demand by 2035.

Recycling Infrastructure Components:

• Collection Networks: Systematic recovery from electronic waste streams

• Processing Facilities: Specialised separation from complex product matrices

• Quality Control: Certification for recycled rare earth product standards

• Logistics Integration: Coordination with primary production facilities

Geopolitical Scenarios and Strategic Independence

European rare earth development occurs within complex geopolitical dynamics requiring scenario analysis for strategic planning. Consequently, multiple development pathways must be evaluated.

What Could Accelerated Development Achieve?

Fast-track permitting combined with coordinated EU critical minerals policy could enable 25-30 percent European supply independence by 2032. This scenario requires sustained political commitment and substantial public-private partnerships.

How Might Regulatory Delays Impact Timelines?

Extended environmental assessment periods could delay production timelines, achieving 15-20 percent supply independence by 2037. Phased development approaches might reduce initial capital risk whilst extending timeline uncertainty.

What About Chinese Response Strategies?

Potential Chinese export restrictions on processing technology could necessitate hybrid supply chain models with 40 percent European content whilst maintaining strategic partnerships with established Asian producers.

Strategic Response Mechanisms:

• Technology Transfer Agreements: Partnerships with established rare earth producers

• Workforce Development: Specialised training programmes for separation technologies

• Government-Backed Financing: Risk mitigation through public investment guarantees

• Strategic Stockpiling: Buffer inventories for supply disruption scenarios

Future Outlook and Strategic Implications

Norway's Fen Complex discovery represents more than expanded resource availability – it signals Europe's potential transition toward strategic mineral independence. The 81 percent resource increase validates world-class deposit status whilst highlighting continental capabilities to reshape global supply architectures.

Success requires coordinated policy frameworks, substantial infrastructure investment, and environmental stewardship balancing resource development with sustainability mandates. European stakeholders must capitalise decisively on this strategic advantage whilst constructing resilient, diversified supply chains.

The rare earth deposit Europe has discovered could fundamentally alter global supply dynamics over the next decade. However, realising this potential depends on coordinated development strategies, processing infrastructure investment, and sustained political commitment to strategic mineral independence.

This analysis is based on publicly available information and industry reports. Investors should conduct independent research and consider multiple factors before making investment decisions. Rare earth projects involve substantial technical, regulatory, and market risks that may affect development timelines and commercial viability.

Want to Discover the Next Major Mineral Breakthrough?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, empowering investors to identify actionable opportunities before the broader market. Explore why major mineral discoveries can generate substantial returns by examining historic examples of exceptional outcomes, then begin your 14-day free trial today to position yourself ahead of the market.