July 8, 2026

The Mine-to-Magnet Problem Western Industry Has Spent Decades Ignoring

For most of the past three decades, Western industrial policy treated rare earth supply chains as a procurement footnote rather than a strategic priority. Minerals were mined, often exported, and the value-added processing steps that transformed raw ore into finished permanent magnets happened elsewhere, almost exclusively in China. The result is a structural vulnerability that now sits at the centre of defence procurement debates, electric vehicle supply chain audits, and advanced manufacturing policy discussions across North America and allied nations.

Understanding why this gap exists, and why it has proven so difficult to close, requires looking at the supply chain not as a single problem but as four distinct industrial challenges stacked on top of one another: feedstock sourcing, rare earth separation and refining, metallization into magnet-ready alloys, and finally, the manufacturing of finished permanent magnets. Each stage requires different capital infrastructure, technical expertise, and regulatory frameworks.

China built all four over several decades of deliberate industrial policy. The West, broadly speaking, built almost none of them. That context is essential for understanding what the REalloys JS Link rare earth magnet manufacturing platform is actually attempting, and why, if it reaches completion, it would represent something genuinely uncommon in Western critical minerals history.

When big ASX news breaks, our subscribers know first

Why Neodymium-Iron-Boron Magnets Are at the Centre of This Debate

The Physics Behind the Strategic Urgency

Neodymium-iron-boron (NdFeB) magnets are the strongest type of permanent magnet produced commercially. Their exceptional magnetic energy density, measured in units of megagauss-oersteds (MGOe), allows engineers to achieve powerful magnetic fields in compact form factors, which is precisely why they appear in electric vehicle traction motors, wind turbine generators, defence guidance systems, industrial robotics, and consumer electronics.

The elemental composition of these magnets is more complex than the name implies. The primary inputs are:

- Neodymium (Nd) and praseodymium (Pr) as the core light rare earth elements that provide base magnetic strength

- Dysprosium (Dy) and terbium (Tb) as heavy rare earth additions that enhance coercivity, meaning resistance to demagnetisation at elevated temperatures

- Iron (Fe) as the structural matrix element

- Boron (B) as the phase-boundary element that stabilises the crystal structure

The addition of dysprosium and terbium is not optional for high-performance applications. Defence systems, aerospace actuators, and high-temperature automotive motors require coercivity levels that light rare earths alone cannot achieve. This makes heavy rare earth metallization one of the most technically demanding and geopolitically sensitive steps in the entire supply chain.

China controls an estimated 85 to 90 percent of global rare earth separation capacity and an even higher share of NdFeB permanent magnet output, according to industry estimates cited in U.S. Congressional Research Service reports. For dysprosium and terbium specifically, Chinese processing dominance approaches near-totality.

What Happens When a Single Supplier Controls Every Stage

The industrial risk embedded in this supply structure is not theoretical. Export restrictions, licensing controls, and quota adjustments imposed by Chinese authorities have historically disrupted non-Chinese access to both rare earth materials and finished magnets. Each episode has reinforced the same conclusion: vertical integration outside China is not merely commercially desirable — it is a national security requirement for advanced industrial economies.

Furthermore, the critical minerals demand surge driven by electrification and defence spending has only amplified this urgency, making the development of alternative supply chains a top-tier policy priority across allied nations.

Building the Platform: How REalloys Assembled Its Upstream and Midstream Position

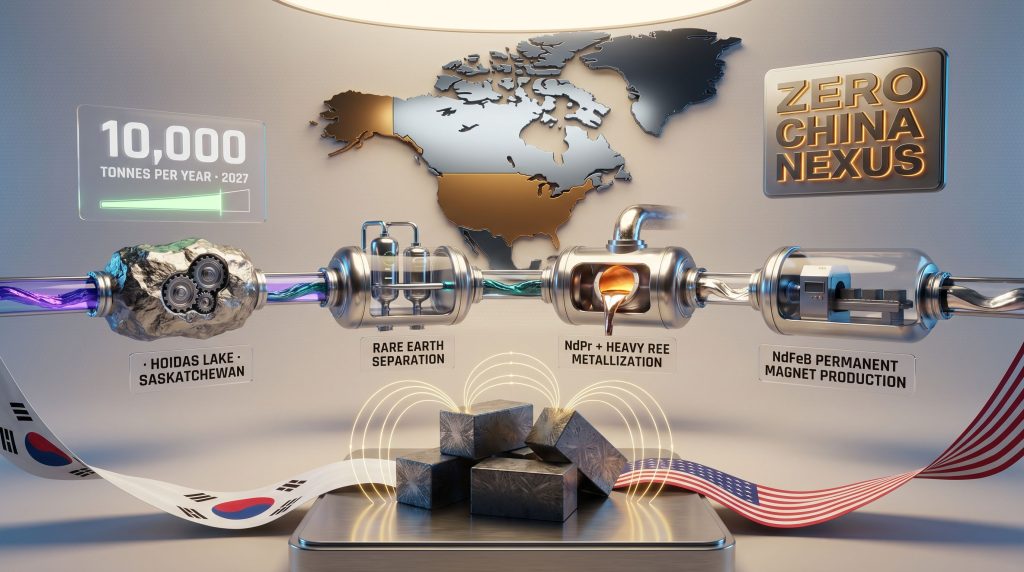

Hoidas Lake and the North American Feedstock Foundation

REalloys' strategic positioning begins with the Hoidas Lake rare earth project in Saskatchewan, Canada. This asset provides a North American-origin feedstock base, establishing the first link in a supply chain that does not depend on Chinese or geopolitically sensitive raw material sources. Importantly, REalloys has supplemented this domestic anchor with a growing portfolio of global feedstock agreements, creating supply diversification that a single project geography could not deliver alone.

The Saskatchewan feedstock position is not simply a mining play. It functions as the foundation for downstream processing ambitions, ensuring that whatever separation, metallization, and magnet manufacturing capacity REalloys builds above it has access to material inputs with provenance documentation that defence and government customers increasingly require.

The Saskatchewan Research Council Partnership: Closing the Refining Gap

One of the less-discussed but technically critical elements of REalloys' platform is its strategic alliance with the Saskatchewan Research Council (SRC). The SRC operates sophisticated rare earth processing infrastructure and has been developing Canadian rare earth refining capabilities that sit between mine output and finished metal production.

Through this partnership, REalloys gains access to expanded rare earth refining and metalmaking capacity, including the production of high-purity neodymium-praseodymium (NdPr) metal, which is the direct feedstock for NdFeB magnet alloy production. This step is frequently underestimated by observers focused on mining or magnet manufacturing, but NdPr metal production is where most non-Chinese supply chain projects have historically stalled due to technical complexity and capital requirements.

PMT Critical Metals: The Heavy Rare Earth Metallization Acquisition

The acquisition of PMT Critical Metals addressed what was arguably the hardest gap to fill in the midstream: commercial-scale heavy rare earth metallization. Dysprosium and terbium metal production requires specialised reduction furnace technology, handling procedures for highly reactive rare earth metals, and quality control systems capable of producing alloy-grade material with the purity specifications that magnet manufacturers require.

Heavy rare earth metallization is the stage where Western supply chain development efforts most commonly fail. The technical barriers are high, the capital requirements are significant, and the market for dysprosium and terbium metal outside China has historically been too thin to justify standalone investment. PMT's existing capabilities therefore represent infrastructure that would be extremely difficult to replicate from scratch.

JS Link's Manufacturing Expertise and the Permanent Magnet Manufacturing Gap

What South Korea's Magnet Industry Brings to North America

JS Link operates commercial permanent magnet manufacturing facilities in South Korea, a country that has developed significant rare earth processing and magnet manufacturing capabilities outside China. The South Korean magnet industry benefits from decades of materials science investment and a manufacturing culture oriented toward precision and consistency — qualities that defence and aerospace customers require.

JS Link's planned expansions into Malaysia and the United States position the company as a multi-geography producer deliberately constructing its business around non-Chinese supply chain architecture. This is strategically important because it means JS Link's growth model is already aligned with the policy environment that Western governments are creating, rather than being adapted to it after the fact.

The Integrated Platform: Mapping Each Stage of the Value Chain

The following table illustrates how the combined REalloys and JS Link capabilities map across the complete mine-to-magnet value chain:

| Supply Chain Stage | Contributor | Key Asset or Capability |

|---|---|---|

| Feedstock Supply | REalloys | Hoidas Lake, Saskatchewan + global feedstock agreements |

| Rare Earth Separation and Refining | REalloys + SRC | Saskatchewan Research Council partnership, NdPr metal production |

| Light REE Metallization | REalloys | NdPr metal production capacity |

| Heavy REE Metallization | REalloys (PMT) | Commercial-scale Dy and Tb metallization |

| Permanent Magnet Manufacturing | JS Link | Korea operations, Malaysia and U.S. expansion |

| Defence and Government Access | REalloys | U.S. Army Strategic Capital Initiatives program, Tooele Army Depot |

| Capital Position | REalloys | $100 million private placement completed |

The Zero-China-Nexus Objective: Why It Matters Beyond Marketing

The stated objective of establishing a supply chain with no dependency on Chinese feedstock, separation, metalmaking, or magnet manufacturing is not simply a marketing position. It responds to a specific and growing customer requirement across defence procurement and allied government supply chain assurance programmes.

Defence customers in particular are increasingly requiring provenance documentation and supply chain audits that trace materials back to their point of origin. A supply chain with a Chinese nexus at any stage, even if that stage is geographically distant from final magnet production, creates compliance risk under evolving procurement frameworks in the United States, Australia, and the United Kingdom.

The target production capacity of 10,000 tonnes per year by 2027 would, if achieved, represent a material contribution to Western non-Chinese magnet supply at a time when global NdFeB demand is projected to grow substantially through 2030, driven by electric vehicle adoption, offshore wind turbine deployment, and expanding defence hardware requirements.

The Defence Dimension: Tooele Army Depot and the Strategic Capital Initiatives Programme

Why Military Facilities Make Unusual Sense for Rare Earth Processing

REalloys' partnership with the United States Army under the Army Strategic Capital Initiatives programme — which includes evaluation of a rare earth processing facility at Tooele Army Depot in Utah — reflects an underappreciated logic: military base infrastructure offers security clearances, physical security, utility connections, and regulatory environments that are difficult to replicate at commercial greenfield sites.

For rare earth processing in particular, the combination of environmental permitting complexity and physical security requirements creates a strong argument for co-locating critical mineral infrastructure within existing defence installations. Consequently, the use of wartime powers for minerals and defence-adjacent frameworks is increasingly being explored to accelerate this kind of strategic co-location across allied nations.

Heavy Rare Earth Qualification for Defence Applications

Within its defence-focused work, REalloys has begun the qualification of heavy rare earth materials — a process that involves demonstrating to defence procurement agencies that produced materials meet the compositional purity, consistency, and traceability requirements embedded in defence specifications. Qualification is often a multi-year process, which means REalloys' early progress in this area represents a meaningful lead time advantage over potential competitors entering the space later.

Demand Drivers in Defence Procurement

Key NdFeB magnet applications across the defence sector include:

- Guidance and navigation systems in precision munitions

- Electric propulsion motors in naval surface vessels and submarines

- Drone and unmanned aerial vehicle propulsion systems

- Radar and electronic warfare antenna actuators

- Exoskeleton and robotic system actuators for ground forces

- Directed energy weapon cooling and power management systems

Each of these applications has demand characteristics that differ from commercial markets: longer procurement cycles, stricter specifications, higher price tolerance, and strong preference for domestically sourced supply chains.

How the REalloys JS Link Platform Compares to Other Western Magnet Initiatives

The Competitive Landscape Is Moving Quickly

The broader Western rare earth magnet industry has seen accelerating investment activity in 2025 and 2026, with several initiatives attempting to address different portions of the mine-to-magnet gap.

| Initiative | Structure | Stage | Geographic Focus |

|---|---|---|---|

| REalloys + JS Link | Non-binding LOI (July 2026) | Pre-definitive agreement | North America (Canada + U.S.) |

| ReElement + POSCO | Joint Venture | Active development | United States |

| USA Rare Earth | Standalone company | Processing and magnet | United States |

| Energy Fuels + VAC | Acquisition ($1.9 billion) | Completed acquisition | United States and Europe |

What Distinguishes the REalloys JS Link Approach

Several structural characteristics differentiate the proposed REalloys JS Link rare earth magnet manufacturing platform from peer initiatives. In addition, the platform's critical minerals strategy reflects a broader industry shift toward fully integrated, non-Chinese supply chains. These distinguishing features include:

- Full vertical integration scope: The platform addresses every stage from Canadian feedstock to finished magnets, rather than focusing on two or three stages

- Existing defence partnership: The Tooele Army Depot framework provides a defence-anchored demand pathway that most commercial magnet initiatives lack

- Completed capital raise: The $100 million private placement provides execution capital without requiring immediate external financing to begin development activities

- Operational magnet manufacturing: JS Link's existing South Korean operations reduce technology development risk compared to ventures building magnet manufacturing from a greenfield position

- Heavy rare earth capability: The PMT acquisition addresses the stage where Western supply chain gaps are most pronounced and hardest to fill

The next major ASX story will hit our subscribers first

Key Risks That Investors and Industry Observers Must Understand

The LOI Is a Framework, Not a Transaction

The July 7, 2026 Letter of Intent is explicitly non-binding. It establishes the scope of what the two companies intend to evaluate and a framework for negotiating definitive agreements, but it does not guarantee that a transaction will close. Due diligence processes, commercial term negotiations, regulatory reviews, and board approvals all remain ahead.

Industry observers should assess the platform on the merits of its structural components rather than treating the LOI announcement as confirmation that an integrated company already exists.

Execution Complexity Across Multiple Geographies and Stages

Coordinating feedstock supply from Saskatchewan, refining through the SRC partnership, metallization from PMT's facilities, and magnet manufacturing across JS Link's Korea, Malaysia, and U.S. locations introduces supply chain coordination complexity that is not trivial. Each geographic node carries its own permitting environment, labour market dynamics, infrastructure requirements, and regulatory compliance obligations.

Rare Earth Price Volatility and Chinese Cost Competition

Rare earth oxide and metal prices have historically been volatile, with periods of extreme price elevation followed by sharp corrections. Chinese producers retain structural cost advantages at most stages of the supply chain — advantages that non-Chinese platforms must offset through long-term offtake contracts, government financing support, or premium pricing from defence and regulated commercial customers.

This article contains forward-looking statements and speculative projections regarding the REalloys JS Link rare earth magnet manufacturing platform. The LOI described herein is non-binding, and no assurance can be given that definitive agreements will be reached or that production targets will be achieved. Readers should conduct their own due diligence before making investment decisions based on information contained in this article.

Frequently Asked Questions: REalloys JS Link Rare Earth Magnet Manufacturing Platform

What is the REalloys JS Link rare earth magnet manufacturing platform?

It is a proposed integrated supply chain combining REalloys' North American rare earth feedstock, separation, and metallization capabilities with JS Link's permanent magnet manufacturing technology. The goal is to produce finished NdFeB permanent magnets through a supply chain with no dependency on Chinese processing infrastructure.

What rare earth elements does the platform focus on?

The platform targets neodymium and praseodymium as primary light rare earth inputs, with dysprosium and terbium as critical heavy rare earth additions for high-performance defence and aerospace magnet grades.

Is the July 2026 agreement legally binding?

No. The agreement signed on July 7, 2026 is a non-binding Letter of Intent. It provides a structured framework for evaluation and negotiation but does not constitute a completed commercial transaction.

What production capacity is REalloys targeting?

REalloys has outlined a target of 10,000 tonnes per year of magnet manufacturing capacity by 2027, though this represents a forward-looking target subject to the successful completion of definitive agreements and subsequent development activities.

What industries would benefit most from a completed platform?

Primary end markets include U.S. and allied defence procurement, electric vehicle traction motor manufacturing, offshore wind turbine production, aerospace actuation systems, advanced robotics, and artificial intelligence hardware infrastructure that relies on precision motors and actuators.

The Structural Shift This Platform Represents for Western Critical Minerals

Why Integration Matters More Than Individual Projects

The history of Western rare earth supply chain development is littered with projects that addressed one or two stages of the chain without connecting to the others. Mines were developed without separation plants. Separation plants were built without metalmaking capacity downstream. Each disconnected effort left the fundamental mine-to-magnet gap intact.

What makes the REalloys JS Link rare earth magnet manufacturing platform architecturally different — at least in its stated intent — is the explicit ambition to connect every stage. That vertical integration aspiration, if translated into definitive agreements and operational reality, would address the structural problem rather than one of its symptoms.

The Long-Term Value Creation Thesis

A publicly traded North American magnet platform, which the companies have identified as a potential long-term corporate structure, could attract institutional capital, strategic industrial partners, and government co-investment in ways that private development vehicles cannot. The combination of defence offtake, government financing pathways, and commercial demand across automotive and energy creates a diversified revenue foundation that reduces single-market dependency.

For the broader Western critical minerals sector, the convergence of initiatives — including the ReElement-POSCO joint venture, USA Rare Earth's federal financing access, and the Energy Fuels VAC acquisition — signals that the mine-to-magnet gap is finally being addressed with the capital and institutional commitment it has long required. Furthermore, the emergence of a critical minerals coalition across allied governments is reinforcing these private-sector efforts with policy frameworks and financing mechanisms that were largely absent a decade ago. Whether the REalloys JS Link platform becomes one of the defining structures in that emerging landscape will depend on what follows the Letter of Intent.

Readers seeking ongoing coverage of North American rare earth supply chain development, critical mineral policy, and strategic metals developments can follow reporting at Metal Tech News (metaltechnews.com).

Want to Capitalise on the Next Major Critical Minerals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex data to surface actionable opportunities the moment they are announced, from rare earths to strategic metals. Start your 14-day free trial today and explore historic discoveries that have delivered exceptional returns to understand why positioning early in transformative mineral finds can matter so profoundly.