June 23, 2026

Why the rare earth magnet race is really about manufacturing choke points

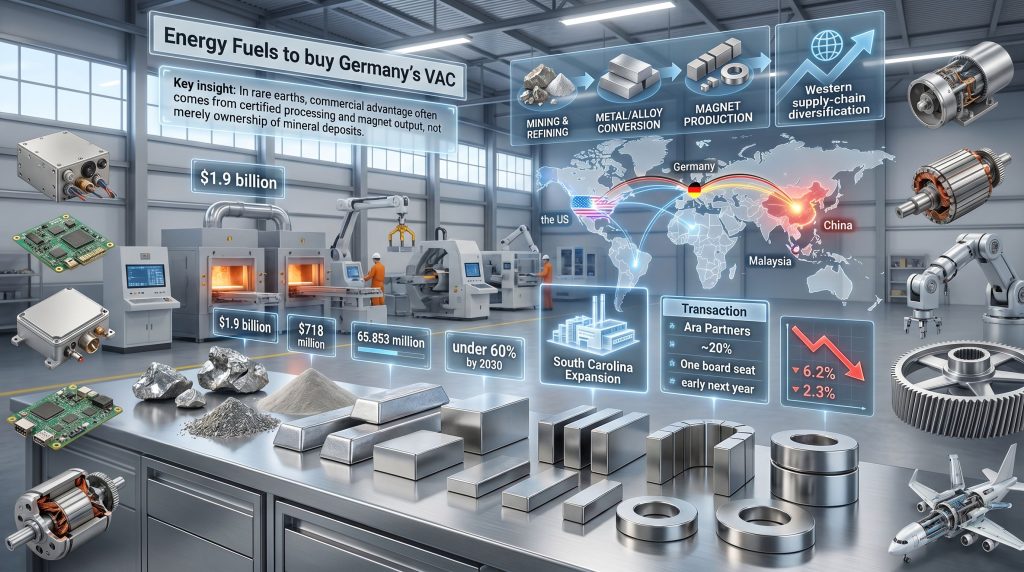

In critical minerals, headlines usually begin at the mine. However, the harder commercial problem often starts much later, when a company must turn refined material into a component that can survive years of qualification, meet tight tolerance requirements, and enter mission-critical supply chains. That is especially true in permanent magnets, where Energy Fuels to buy Germany's VAC highlights a bottleneck in manufacturing rather than mining alone.

That context explains why the phrase matters far beyond a routine mining-sector acquisition. The announced $1.9 billion transaction links an upstream critical minerals strategy with an established downstream magnet platform, offering a potentially faster path into higher-value manufacturing tied to defence, aerospace, electric vehicles, industrial automation, and renewable energy.

Energy Fuels, known primarily as a US uranium producer that has broadened its focus to critical minerals, said it will acquire Vacuumschmelze, or VAC, from Ara Partners for $718 million in cash plus 65.853 million newly issued common shares. The transaction is expected to close early next year, subject to customary conditions and approvals.

After completion, Ara Partners is expected to hold roughly 20% of Energy Fuels and receive one board seat. Furthermore, reporting from BNN Bloomberg’s deal coverage suggests the acquisition is being closely watched as the magnet race intensifies across Western supply chains.

For readers trying to understand why this matters, the key questions are straightforward:

- What does VAC actually make?

- Why buy a magnet producer instead of building one?

- How does this change the non-Chinese rare earth supply chain?

- What does it mean for defence and industrial buyers?

- Is this about vertical integration, geopolitics, or both?

When big ASX news breaks, our subscribers know first

Why this acquisition stands out in the non-Chinese supply chain buildout

The strategic significance of this deal lies in value-chain depth. Rare earths are not a single-step business. Instead, each stage introduces different technical risks, capital needs, and competitive barriers.

The rare earth value chain, simplified

- Mining and mineral feedstock

- Separation and refining into oxides

- Metal and alloy conversion

- Magnet production

- Customer qualification and long-term supply acceptance

Many investors focus heavily on stages one and two because those are easier to describe. Yet downstream steps often create the true moat. A company can possess feedstock and still struggle to earn meaningful margins if it lacks metallisation skill, magnet engineering capability, and trusted customer relationships.

“In rare earths, durable commercial advantage often comes from certified processing capability and qualified magnet output, not from mineral ownership alone.”

For that reason, understanding rare earth processing challenges is essential to grasp why downstream assets can command such strategic value.

Why buying magnet capacity may be faster than building it

Energy Fuels management has indicated that magnet manufacturing is a technically demanding business and that customer acceptance can take a long time. In advanced materials markets, qualification is not a box-ticking exercise.

It can involve:

- Material traceability requirements

- Batch-to-batch consistency checks

- Performance validation under extreme conditions

- Long procurement review cycles

- Re-certification costs if a supplier changes processes disruptively

A buyer like VAC already has those relationships and process know-how in place. Consequently, that can be worth more than simply owning a greenfield facility design.

| Strategic path | Likely advantage | Key risk | Why it matters |

|---|---|---|---|

| Build magnet business from scratch | Full operational control | Long qualification cycle | Slow route to revenue and customer trust |

| Acquire established producer | Immediate manufacturing platform | Integration complexity | Faster access to approved customers |

| Partner via JV or offtake | Lower upfront capital | Less control over execution | Flexible but dependent on third parties |

Who VAC is and why it is a hard asset to replicate

VAC is not valuable merely because it makes magnets. Rather, it is valuable because it combines age, process knowledge, industrial relationships, and a global operating footprint in a segment where learning curves are steep.

According to disclosed details, VAC has:

- More than 100 years of operating history

- More than 1,000 customers

- Manufacturing facilities in Germany, the United States, Malaysia, and other locations

- Exposure to demanding markets such as aerospace, defence, automotive, and renewables

That sort of installed manufacturing base is difficult to reproduce quickly. In specialty materials, a century of accumulated process control can justify premium valuation because know-how is not fully visible on a balance sheet.

Why customer acceptance is a hidden barrier to entry

Permanent magnet buyers, especially in defence, aerospace, and automotive supply chains, generally do not switch suppliers casually. They care about:

- Magnetic performance consistency

- Mechanical strength and dimensional accuracy

- Thermal stability

- Corrosion behaviour and coating reliability

- Documentation and traceability

- On-time delivery over long production cycles

This is one reason downstream manufacturing matters more than raw material headlines suggest. In other words, the market often treats rare earth supply as a mining issue, while industrial customers experience it as a fabrication and qualification issue.

Why governments want more non-Chinese rare earth and magnet supply

This deal should be read within a wider effort by Western economies to diversify critical supply chains. Although that does not mean project-specific government support, it does reflect a policy environment that increasingly emphasises resilience in materials needed for advanced manufacturing and defence readiness.

Recent trade tensions and export restrictions have reinforced how concentrated the America’s rare earth chain and broader global magnet ecosystem remain. That concern is shared across the US, Europe, Japan, and G7 economies.

What the G7 target signals

G7 leaders recently set an aim to reduce dependence on any single supplier for rare earths and permanent magnets to below 60% by 2030, with a longer-term ambition of 50%. That target matters because it captures how governments are framing magnet supply as a strategic industrial issue.

The policy logic is simple:

- Reduce single-country concentration risk

- Improve defence supply assurance

- Support clean energy manufacturing

- Build allied-country industrial capacity

In addition, policy momentum behind a critical minerals coalition underlines how magnets are increasingly viewed as strategic infrastructure rather than niche industrial components.

Why magnets are treated as strategic capability

Rare earth permanent magnets are important in:

- Guided systems and defence electronics

- Radar, sensors, and avionics

- Electric motors and traction systems

- Robotics and industrial automation

- Wind turbines and other electrification technologies

Not every end market uses the same chemistry, geometry, or performance standard. Therefore, magnet demand is not one homogeneous pool. Product mix can shape margins, qualification complexity, and the strategic value of individual facilities.

Deal structure, ownership implications, and governance watchpoints

The mechanics of the transaction are straightforward on paper, but meaningful for shareholders and industry observers.

| Component | Detail |

|---|---|

| Buyer | Energy Fuels |

| Target | VAC / Vacuumschmelze |

| Deal value | $1.9 billion |

| Cash portion | $718 million |

| Equity portion | 65.853 million new shares |

| Seller | Ara Partners |

| Post-close ownership | Around 20% stake for seller |

| Board impact | One board seat |

| Expected close | Early next year |

What the 20% stake could mean

A shareholder with roughly one-fifth ownership and board representation can have real influence over strategy. That can be positive if incentives are aligned around long-term downstream expansion.

However, it can also become a focal point in debates over:

- Capital allocation priorities

- Expansion pacing

- Further acquisitions or partnerships

- Balance sheet risk tolerance

Investors will likely monitor whether the enlarged company behaves more like a miner pursuing processing optionality or a vertically integrated advanced materials platform. The company’s own Energy Fuels critical minerals strategy gives useful context for that broader shift.

Operational synergies and the execution risks that matter most

The industrial case for the acquisition rests on a simple thesis: controlled feedstock plus qualified magnet manufacturing could create a stronger non-Chinese supply platform over time. That is why Energy Fuels to buy Germany's VAC is best understood as a long-term industrial bet rather than a short-term mining trade.

Potential synergies across the chain

Possible benefits include:

- Better upstream-to-downstream traceability

- Stronger access to Western industrial customers

- Improved positioning in defence and specialty procurement channels

- Greater ability to align feedstock, alloying, and magnet output over time

- A clearer route towards value-added sales rather than pure commodity exposure

What management plans to retain

Energy Fuels has indicated that it intends to integrate VAC while preserving several continuity features:

- About 3,600 workers across the combined workforce

- Existing leadership continuity, including CEO Erik Eschen

- The Vacuumschmelze brand

Brand continuity can matter in industrial markets. For instance, an established name may reduce perceived disruption for customers that value stability in approved suppliers.

Why keeping current plants open matters

Management has also indicated that VAC’s current facilities, including a plant in China, are expected to remain open. Expansion is planned for the South Carolina facility that opened late last year.

On one hand, Western buyers want more diversification. On the other, operating reality often requires pragmatic continuity. Retaining established plants may protect customer service and production flow during transition, even if it complicates the geopolitical narrative.

“A magnet platform only creates strategic value if it preserves qualification status, delivery reliability, and customer trust during ownership change.”

Main integration risks to monitor

- Cross-border cultural and systems integration

- Customer attrition during ownership transition

- Margin pressure in specialty manufacturing

- Regulatory reviews across multiple jurisdictions

- Working-capital demands if expansion accelerates

- Political scrutiny related to retained Chinese operations

The next major ASX story will hit our subscribers first

Market reaction and what it says about investor psychology

The first share-price response was cautious. Energy Fuels shares fell as much as 6.2% in premarket trading and were later down 2.3%. That is not unusual for a large strategic acquisition, especially when the buyer is stepping deeper into a technically specialised business.

Why the stock sold off first

Possible reasons include:

- The size of the acquisition relative to the buyer

- Equity dilution from the new shares issued

- Integration uncertainty

- Limited familiarity among generalist investors with magnet manufacturing economics

Markets often discount complexity before they reward strategic positioning. Moreover, the definitive agreement announcement reinforces just how ambitious the move is for a company previously viewed mainly through a mining lens.

What could improve sentiment later

- Successful deal completion

- Evidence of customer retention

- Visible progress at South Carolina

- Higher-margin downstream revenue growth

- Clear execution milestones tied to integration

This is where market psychology becomes important. In critical minerals, investors frequently price near-term financing and execution risk more heavily than long-term geopolitical upside.

What this means for defence, autos, and renewable energy

The downstream relevance of this deal depends on where magnets end up. In practical terms, Energy Fuels to buy Germany's VAC matters because these components sit inside strategically sensitive products.

| End market | Why magnets matter | Strategic relevance |

|---|---|---|

| Defence and aerospace | Sensors, radar, actuators, specialty motors | High reliability and secure sourcing requirements |

| Automotive and EVs | Traction motors and efficiency-focused systems | Scale demand, qualification discipline, product-specific chemistry needs |

| Wind and renewables | Direct-drive turbine systems and electrification equipment | Long-cycle infrastructure demand |

| Industrial automation | Robotics, factory systems, precision motors | Performance consistency and recurring demand |

Defence and aerospace

Secure magnet supply can affect guided systems, avionics, radar, and other specialised applications where supplier reliability matters as much as price.

EVs and industrial motors

Permanent magnets are widely used in high-efficiency motors, though not all motors use identical rare earth content. As a result, the commercial opportunity depends on application mix, not just raw demand growth.

Renewable energy

Wind turbines, especially some direct-drive configurations, can increase demand for high-performance magnetic materials. Broader electrification trends also support industrial magnet consumption.

Bottom line on the deal

The most useful way to read Energy Fuels to buy Germany's VAC is not as a typical mining acquisition, but as a downstream manufacturing play in a supply chain where qualification and industrial know-how can matter more than ore headlines.

The headline figures are clear: $1.9 billion in total consideration, including $718 million in cash and 65.853 million new shares, with Ara Partners retaining a significant roughly 20% stake and one board seat.

What remains less clear, and far more important, is whether Energy Fuels can preserve VAC’s customer acceptance, integrate global operations effectively, and convert ownership of an established magnet producer into lasting non-Chinese supply-chain relevance. If execution is strong, the acquisition could become one of the more consequential vertical integration moves in Western rare earth magnets.

Ready To Spot The Next Strategic Discovery?

For investors following rare earths, critical minerals, and downstream manufacturing shifts, Discovery Alert delivers real-time ASX discovery alerts powered by Discovery Alert’s proprietary Discovery IQ model, helping identify actionable opportunities before the broader market reacts. To see how major discoveries have historically driven exceptional returns, explore Discovery Alert’s discoveries page and begin a 14-day free trial today.